Reports

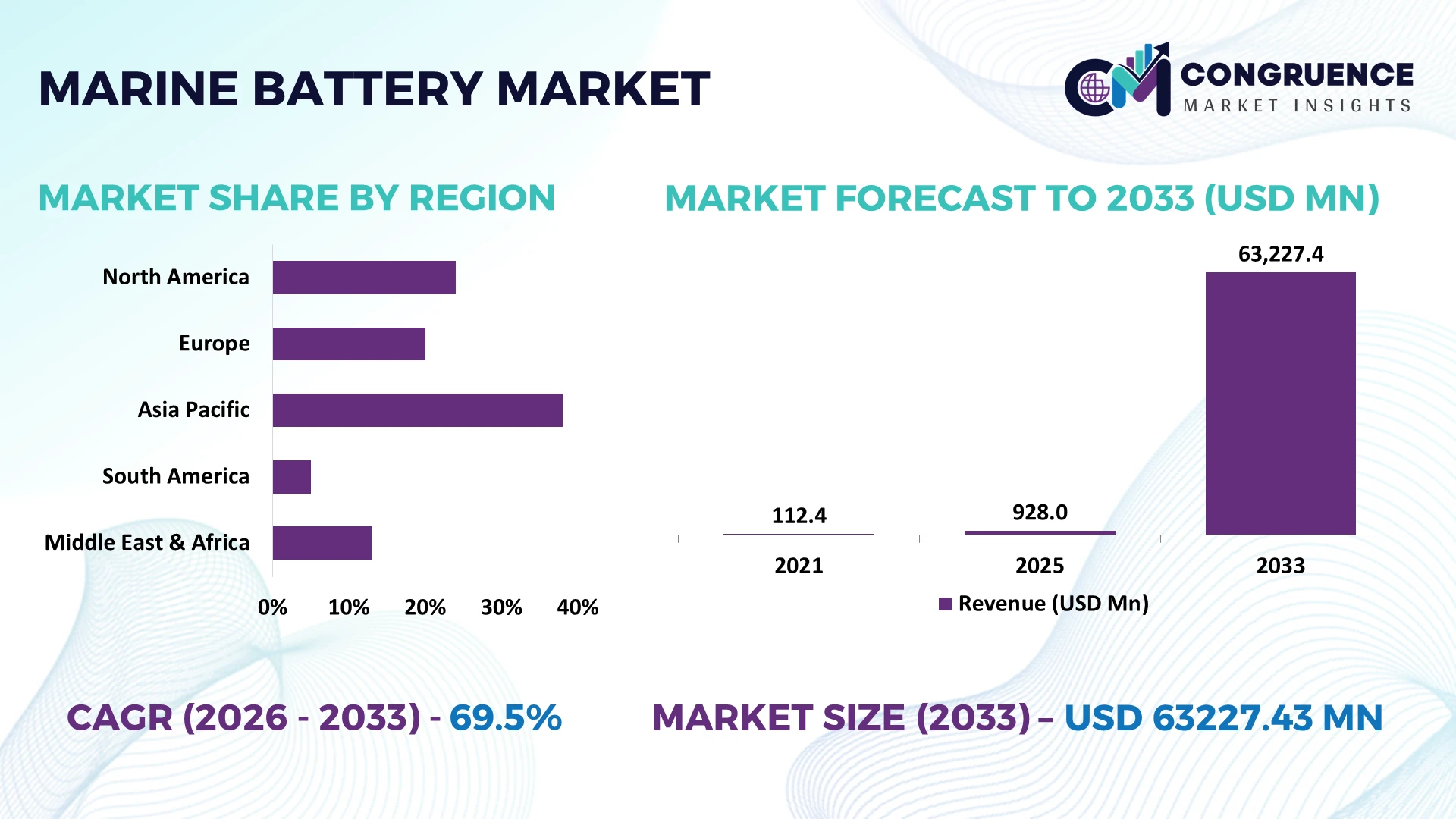

The Global Marine Battery Market was valued at USD 928 Million in 2025 and is anticipated to reach a value of USD 63227.43 Million by 2033 expanding at a CAGR of 69.5% between 2026 and 2033. Growth is driven by vessel electrification mandates, lithium-ion cost optimization, offshore energy integration, and increasing adoption of zero-emission propulsion systems across commercial shipping fleets.

China represents the dominant marine battery ecosystem, accounting for nearly 45% of global marine battery production capacity through advanced lithium supply chains, shipbuilding clusters, and EV battery expertise. South Korea and Japan are expanding investments in electric vessels and fuel-efficient maritime systems, while Europe is accelerating adoption through IMO decarbonization targets. China’s battery manufacturing scale exceeds Japan’s marine battery output by more than 30%, creating a competitive supply advantage. The U.S. market is expanding through naval electrification programs and commercial ferry modernization initiatives.

Strategic implication: Companies prioritizing localized battery production, vessel integration partnerships, and energy management innovation will gain stronger positioning in the rapidly transforming maritime electrification landscape.

Market Size & Growth: USD 928 Million in 2025 to USD 63227.43 Million by 2033, supported by 69.5% CAGR and rapid shift toward electric and hybrid marine propulsion.

Top Growth Drivers: Fleet electrification (45%), emission regulations (38%), and lithium battery adoption (32%) are reshaping marine power systems.

Short-Term Forecast: By 2028, advanced marine batteries achieve 25% lower system costs and 20% higher energy efficiency through improved cell chemistry.

Emerging Technologies: AI battery monitoring, automated energy management, and solid-state battery development are advancing high-performance marine applications.

Regional Leaders: China reaches USD 28000 Million scale with shipyard integration, Europe approaches USD 17000 Million through green shipping projects, and North America expands with ferry electrification.

Consumer/End-User Trends: Over 35% of new commercial vessel projects incorporate battery-based propulsion planning, especially in short-distance maritime operations.

Pilot/Case Example: 2025 Scandinavian electric ferry projects delivered nearly 30% fuel reduction using optimized battery-electric systems.

Competitive Landscape: CATL leads with approximately 20% share, followed by BYD, Corvus Energy, Toshiba, Panasonic, and Samsung SDI competing through marine-grade solutions.

Regulatory & ESG Impact: Maritime emission policies are targeting reductions above 40%, accelerating clean propulsion investments and battery deployment.

Investment & Funding: More than USD 5 Billion entered marine electrification projects through partnerships, manufacturing expansion, and maritime technology funding.

Innovation & Future Outlook: Next-generation batteries, recyclable materials, and intelligent charging networks are driving strategic shifts across global shipping operations.

Marine Battery Market demand is accelerating through commercial ferries, offshore vessels, naval applications, and autonomous maritime platforms requiring efficient energy storage solutions. Lithium-ion marine systems now deliver approximately 20% higher operational efficiency than previous battery technologies, while stricter emission rules and port electrification programs are reshaping fleet investment priorities globally.

The Marine Battery Market is becoming strategically important as shipping companies, vessel manufacturers, and energy technology providers compete to reduce operational emissions and improve maritime efficiency. Regulatory pressure from international maritime decarbonization frameworks is accelerating investments in electric propulsion, battery management systems, and integrated charging infrastructure.

The industry is experiencing supply-chain restructuring as manufacturers secure localized lithium resources and establish regional production facilities. Advanced lithium-ion marine batteries provide approximately 30% higher cycle efficiency and significantly lower maintenance requirements compared with conventional marine diesel-electric systems. China focuses on large-scale battery manufacturing, while Norway and Denmark lead commercial vessel electrification through advanced ferry deployments.

Between 2026 and 2028, companies are prioritizing modular battery platforms, digital monitoring systems, and strategic partnerships to improve vessel performance. Electric ferries operating in Northern Europe demonstrate practical deployment advantages through reduced fuel consumption and automated energy optimization. Battery suppliers are expanding manufacturing capacity and collaborating with shipbuilders to capture emerging demand. Competitive advantage will depend on technology reliability, supply-chain control, and the ability to deliver scalable marine energy solutions.

The primary growth driver is accelerating vessel electrification as shipping operators replace conventional propulsion systems with battery-powered alternatives. Battery prices have declined by nearly 20% since 2023, improving commercial feasibility for electric ferries and workboats. Norway’s maritime sector has expanded zero-emission vessel adoption through government-supported infrastructure programs. Companies including battery manufacturers and shipbuilders are increasing investments in high-density lithium systems, automated battery management, and charging networks. The strategic shift is moving beyond emission reduction toward lower operating costs, where electric vessels achieve improved energy utilization and reduced maintenance cycles.

High initial investment and limited charging infrastructure remain major barriers for marine battery adoption. Large marine battery systems can represent 20–35% of vessel electrification costs, affecting project financing decisions. Dependence on lithium, nickel, and graphite supply chains creates pricing volatility, particularly during global mineral market disruptions. Countries such as Japan and South Korea are reducing risks through diversified sourcing agreements and domestic battery technology development. Companies are responding through long-term material contracts, localized manufacturing, and hybrid propulsion solutions that balance performance with cost control.

Opportunities are expanding through solid-state batteries, AI-driven energy optimization, and digital fleet management platforms. Solid-state battery research targets 40% higher energy density compared with current lithium-ion systems, creating potential for longer-range marine operations. India, China, and Southeast Asian shipbuilding markets are exploring electric coastal vessels as port infrastructure modernizes. Companies are increasing R&D spending and forming partnerships with technology providers to develop safer, lighter, and more efficient battery platforms. A key opportunity lies in integrating marine batteries with renewable-powered charging systems to create self-sufficient maritime energy ecosystems.

Marine battery deployment faces challenges related to system integration, safety standards, and long-duration operational reliability. Battery thermal management requirements increase engineering complexity, with marine systems requiring advanced monitoring across thousands of operating cycles. Cybersecurity concerns are rising as digital battery management platforms become connected with vessel automation networks. Countries including Germany and Singapore are strengthening maritime technology standards to support safer deployment. Companies must invest in advanced diagnostics, workforce training, and infrastructure partnerships to ensure consistent performance and maintain competitiveness in future electric shipping markets.

Battery Intelligence Expansion: Marine operators are integrating AI-based battery management systems, improving predictive maintenance accuracy by nearly 25% and reducing unexpected downtime by 15%. Companies are deploying automated monitoring platforms across electric vessels to optimize charging cycles, extend battery life, and improve fleet reliability as maritime operations become increasingly digital.

Localized Supply Chain Shift: Battery manufacturers are restructuring sourcing networks as lithium material volatility affects production planning, with companies increasing regional component procurement by approximately 30%. China, South Korea, and Japan are expanding marine-grade battery manufacturing capacity to strengthen supply security and reduce dependency on fragmented international logistics.

High-Density Battery Adoption: Shipbuilders are moving toward advanced lithium and solid-state technologies, achieving around 20% higher energy density and 15% improved vessel operating efficiency. Companies are redesigning propulsion systems and forming technology partnerships to support longer routes, faster charging, and reduced onboard energy limitations.

Commercial Fleet Modernization: Ferry and coastal vessel operators are accelerating electrification programs, with electric vessel deployments increasing by nearly 35% in targeted maritime segments. Regulatory pressure from emission reduction initiatives is driving companies to combine battery systems, charging infrastructure, and operational automation for lower lifecycle costs.

Lithium-Ion Batteries represent the leading segment in the Marine Battery Market, accounting for approximately 70% market share due to higher energy density, longer lifecycle performance, and compatibility with commercial vessel electrification. Their lightweight structure and scalable configurations make them preferred for ferries, offshore vessels, and hybrid propulsion systems. Companies are expanding lithium battery production and improving thermal management technologies to address marine safety requirements.

Solid-State Batteries are the fastest-growing type, with adoption potential increasing as manufacturers target 40% higher energy density and improved safety compared with conventional systems. Lead-Acid Batteries continue serving smaller vessels due to lower upfront costs, while Nickel-Based Batteries maintain relevance in specialized applications requiring durability. AGM Batteries remain important for auxiliary power systems. Companies are shifting investment toward advanced chemistries while maintaining diversified portfolios to balance cost, reliability, and performance.

Commercial Vessels dominate marine battery adoption with approximately 55% market share, driven by ferry operators, cargo transport companies, and short-route maritime services requiring predictable charging cycles. Electric ferries and hybrid commercial vessels are expanding as operators seek lower fuel expenses and compliance with stricter emission standards. Companies are increasing deployment of modular battery systems and integrated vessel management platforms.

Electric Boats represent the fastest-growing application segment, supported by rising recreational electrification and improved charging accessibility. Adoption is increasing by nearly 30% annually in selected markets as manufacturers introduce compact, efficient propulsion solutions. Naval Vessels, Offshore Support Vessels, and Recreational Boats continue adopting marine batteries for specialized operational requirements. Companies are customizing battery architectures to improve endurance, reduce maintenance complexity, and support diverse vessel designs.

Marine Transportation is the largest end-user segment, contributing approximately 60% market share due to extensive fleet operations, high fuel consumption, and strong demand for efficiency improvements. Shipping companies and ferry operators are investing in battery-electric and hybrid systems to reduce operating expenses and meet environmental compliance requirements. Battery suppliers are developing customized solutions for large-scale fleet integration.

Defense is emerging as the fastest-growing end-user segment, with adoption increasing through naval modernization programs and advanced silent propulsion requirements. Defense-related marine battery demand is expanding by nearly 25% as governments invest in energy-efficient vessels and autonomous maritime technologies. Offshore Energy, Shipbuilders, and Leisure Boating users are adopting specialized battery solutions based on operational needs. Companies are strengthening partnerships with shipyards and technology providers to deliver integrated energy systems.

China accounted for the largest market share at 38% in 2025 however, Norway is expected to register the fastest growth, expanding at a CAGR of 74% between 2026 and 2033.

Electrification of Commercial and Defense Fleets Drives Transformation

North America is strengthening its marine battery position through ferry modernization, naval electrification programs, and offshore vessel upgrades. The region contributes approximately 20% of global marine battery demand, supported by U.S. shipyards and Canadian clean maritime initiatives. Commercial operators are integrating lithium-based propulsion systems, with electric ferry deployments increasing by nearly 25% across selected coastal routes. Battery manufacturers are expanding partnerships with vessel developers to improve charging infrastructure and energy management capabilities. The U.S. focus on domestic battery supply chains is encouraging localized production and reducing dependence on imported components, creating stronger industrial resilience for marine electrification projects.

United States Market Outlook: The United States remains the key North American market due to defense modernization, coastal transportation upgrades, and advanced marine technology investments. More than 100 electric and hybrid vessel projects are under development across commercial and government segments. U.S. companies are prioritizing battery manufacturing partnerships, automated monitoring systems, and scalable charging networks to support long-term fleet conversion.

Regulatory-Led Maritime Decarbonization Accelerates Adoption

Europe maintains a leading position in marine battery deployment due to strict emission regulations, advanced shipbuilding capabilities, and established electric ferry networks. The region represents nearly 30% of global marine battery installations, with Norway, Denmark, and Sweden driving commercial vessel adoption. More than 70% of new ferry projects in Nordic markets incorporate hybrid or electric propulsion planning. Companies are investing in battery recycling systems, charging infrastructure, and integrated vessel energy platforms to meet sustainability targets. The European maritime sector is also restructuring supply chains through local battery partnerships and technology collaborations to strengthen clean transportation capabilities.

Norway Market Outlook: Norway leads Europe’s marine battery adoption through extensive electric ferry operations and strong government support for zero-emission shipping. The country operates more than 60 battery-electric vessels across commercial routes and continues expanding charging infrastructure at major ports. Norwegian companies are focusing on marine battery optimization, vessel automation, and sustainable maritime technology exports.

Manufacturing Scale and Shipbuilding Integration Create Advantage

Asia-Pacific dominates marine battery production through strong shipbuilding ecosystems, lithium supply chains, and large-scale manufacturing capacity. The region contributes approximately 45% of global marine battery manufacturing output, led by China, South Korea, and Japan. Chinese battery producers are expanding marine-grade lithium production, while shipyards integrate battery systems into commercial and offshore vessels. Regional companies are increasing automation in battery assembly and improving supply-chain efficiency, with manufacturing capacity expansion exceeding 30% in major production hubs. Government-backed clean shipping programs are accelerating electric vessel deployment across coastal transportation networks.

China Market Outlook: China represents the strongest Asia-Pacific market due to its battery manufacturing dominance and extensive shipbuilding infrastructure. The country produces more than 60% of global lithium-ion battery cells and is integrating marine battery systems into commercial vessels, ferries, and specialized ships. Chinese enterprises are strengthening export capabilities through advanced energy storage partnerships.

Coastal Electrification Creates Emerging Maritime Opportunities

South America is developing marine battery adoption through coastal transportation upgrades, sustainable port initiatives, and renewable energy integration. The region accounts for a smaller share of global deployment but shows increasing activity in Brazil and Chile. Battery-powered vessel projects are expanding by nearly 20% in selected maritime applications as operators seek lower fuel consumption and cleaner operations. Limited charging infrastructure remains a constraint, encouraging companies to develop hybrid solutions and localized partnerships. Industrial operators are focusing on port-based electrification and efficient vessel systems to improve operational economics in coastal and inland waterways.

Brazil Market Outlook: Brazil holds the strongest position in South America due to extensive coastline operations, commercial shipping activity, and renewable energy potential. The country is exploring electric and hybrid vessels for transportation and industrial applications, with more than 10 pilot projects involving cleaner maritime technologies. Companies are targeting port modernization and battery integration opportunities.

Port Modernization and Energy Transition Reshape Maritime Systems

The Middle East & Africa market is advancing through port modernization, offshore energy projects, and investments in sustainable maritime infrastructure. The region contributes around 5% of global marine battery adoption but is gaining momentum through smart port initiatives and commercial fleet upgrades. Countries are integrating battery systems into offshore support vessels and short-distance maritime operations, with selected port electrification projects improving energy efficiency by nearly 20%. Companies are forming technology partnerships to introduce advanced storage systems while addressing infrastructure limitations. Strategic investments in renewable energy and logistics hubs are creating new opportunities for marine battery deployment.

United Arab Emirates Market Outlook: The United Arab Emirates is emerging as a key regional market due to advanced port infrastructure, maritime logistics investments, and clean energy initiatives. Major ports are adopting digital energy management systems and exploring electric vessel solutions. UAE companies are focusing on smart charging infrastructure, offshore applications, and sustainable maritime operations to strengthen competitiveness.

The Marine Battery Market features competition between global battery manufacturers, maritime technology suppliers, and specialized marine energy innovators. Leading players such as CATL, Corvus Energy, and Samsung SDI compete with regional specialists and vessel integration companies focused on customized propulsion solutions. The top five companies collectively control approximately 55% of the market, creating a moderately concentrated structure. Competition is driven by battery performance, pricing efficiency, supply-chain reliability, and vessel-specific customization, with advanced suppliers improving energy density by 20–30% while reducing lifecycle costs by nearly 15%. Companies are expanding through shipyard partnerships, regional manufacturing facilities, and integrated battery management platforms. The competitive landscape is shifting toward supply-chain control, solid-state innovation, and digital monitoring capabilities. High capital requirements, certification complexity, and marine safety standards create strong entry barriers. Winning companies will combine battery innovation, reliable production capacity, and strategic maritime partnerships to outperform established competitors.

CATL

Corvus Energy

BYD Company

Samsung SDI

Panasonic Energy

Toshiba Energy Systems

LG Energy Solution

Saft Groupe

Echandia

Leclanché

EST-Floattech

Siemens Energy

Wärtsilä

EVE Energy

Marine battery technology is shifting from conventional lead-acid systems toward advanced lithium-ion, solid-state, and intelligent energy management solutions. Lithium-ion batteries provide approximately 30% higher energy efficiency and 40% longer operational cycles compared with traditional marine batteries. AI-based battery management systems are improving predictive maintenance accuracy by nearly 25%, enabling operators to reduce downtime and optimize vessel performance.

Solid-state batteries represent the next disruptive transition, offering around 40% higher energy density potential than current lithium-ion technology. Although commercial marine adoption remains limited, pilot deployments are increasing as shipbuilders evaluate longer-range electric vessels. Companies investing in advanced materials, thermal control systems, and automated charging platforms are gaining competitive advantages through improved safety and reduced maintenance requirements.

Between 2026 and 2028, digital integration will become a critical differentiator as more vessels adopt connected battery monitoring and energy optimization platforms. New-generation systems are expected to improve operational efficiency by 20% compared with older propulsion configurations. Global battery manufacturers and maritime OEMs benefit most from this transition by combining energy storage expertise with vessel integration capabilities, creating stronger positions in future electric shipping ecosystems.

July 2025 CATL launched its marine battery system for China’s first all-electric passenger ship, Yujian 77, achieving 3,918kWh capacity and 140Wh/kg energy density. The deployment validated pure-electric coastal operations and strengthened CATL’s position in zero-emission vessel technology.

August 2025 Wärtsilä expanded its marine battery integration partnership with Wasaline for Aurora Botnia, increasing battery capacity by 10.4MWh to 12.6MWh. The hybrid ferry upgrade improved sustainable operations and reinforced Wärtsilä’s leadership in large-scale maritime energy management solutions. Source: https://www.wartsila.com/

January 2026 International Maritime Organization advanced safety framework development for battery-powered ships, focusing on lithium-ion battery regulations and alternative energy systems. The initiative established future compliance pathways for electric vessels and encouraged manufacturers to prioritize marine battery safety standards. Source: https://www.imo.org/

March 2026 CATL partnered with China Oilfield Services Limited to develop electrified offshore support vessels using LNG-battery hybrid systems. The upgraded vessels achieved 170 tons of fuel savings and reduced engine operation by 34%, improving offshore efficiency and supporting cleaner maritime operations. Source: https://www.catl.com/

The Marine Battery Market Report evaluates industry development across battery types including Lithium-Ion Batteries, Lead-Acid Batteries, Nickel-Based Batteries, Solid-State Batteries, and AGM Batteries. The analysis covers applications such as commercial vessels, naval vessels, recreational boats, offshore support vessels, and electric boats, along with end-users including marine transportation, defense, offshore energy, shipbuilders, and leisure boating sectors.

The report provides regional insights across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa while assessing emerging technologies, battery management systems, charging infrastructure, and advanced energy storage solutions. With more than 50% of market activity concentrated among leading battery and marine technology providers, the study supports investment decisions, expansion planning, competitive benchmarking, and strategic positioning from 2026 to 2033.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2025 | USD 928 Million |

Market Revenue in 2033 | USD 63227.43 Million |

CAGR (2026 - 2033) | 69.5% |

Base Year | 2025 |

Forecast Period | 2026 - 2033 |

Historic Period | 2021 - 2025 |

Segments Covered | By Type

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | CATL, Corvus Energy, BYD Company, Samsung SDI, Panasonic Energy, Toshiba Energy Systems, LG Energy Solution, Saft Groupe, Echandia, Leclanché, EST-Floattech, Siemens Energy, Wärtsilä, EVE Energy |

Customization & Pricing | Available on Request (10% Customization is Free) |