Reports

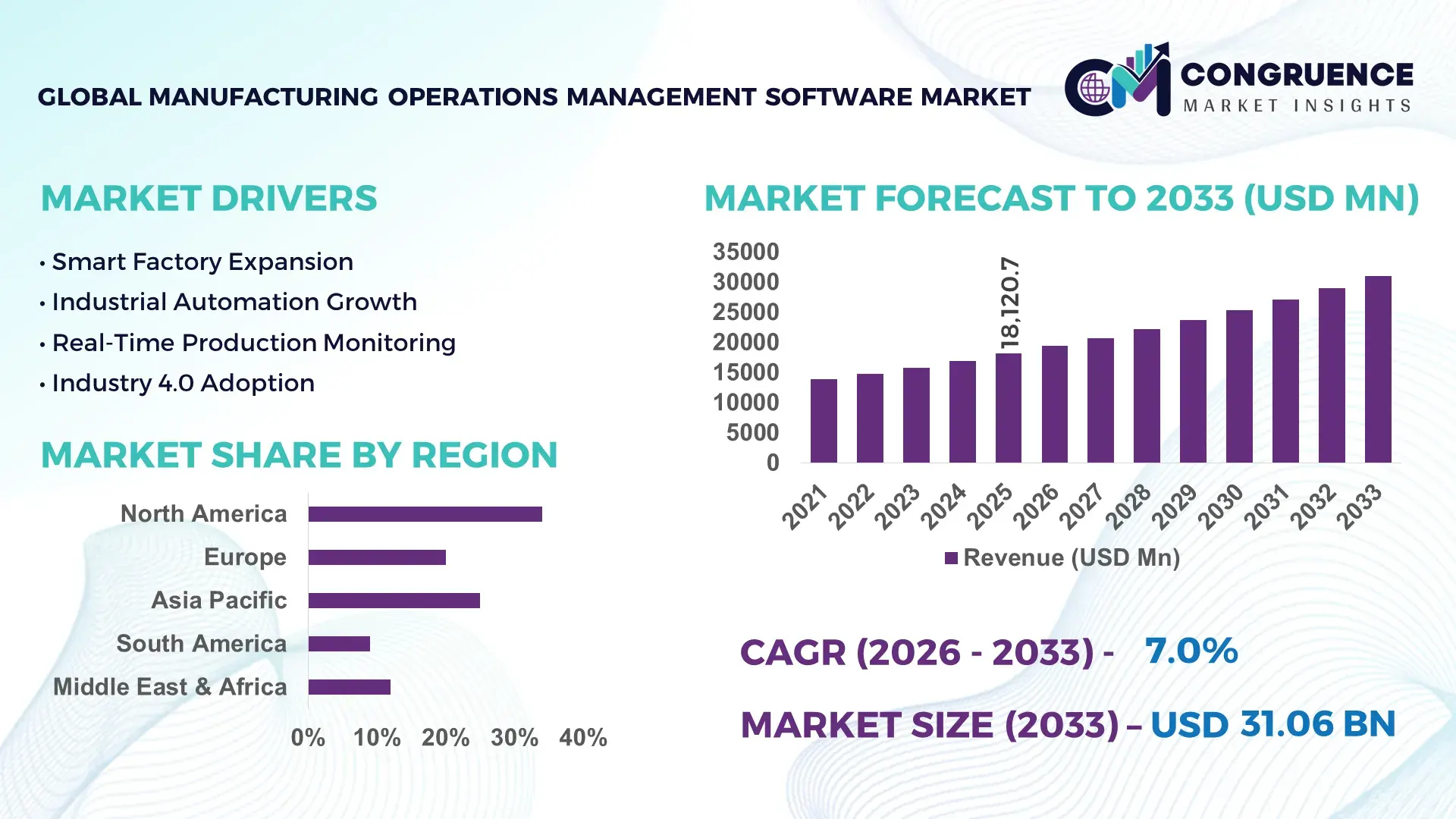

The Global Manufacturing Operations Management Software Market was valued at USD 18120.71 Million in 2025 and is anticipated to reach a value of USD 31065 Million by 2033 expanding at a CAGR of 6.97% between 2026 and 2033.

Rising deployment of AI-enabled production analytics, cloud-based MES integration, and predictive maintenance platforms has reduced unplanned downtime by nearly 18% across large-scale industrial facilities, accelerating enterprise-wide adoption of advanced manufacturing operations management software. Between 2024 and 2026, geopolitical trade realignments, semiconductor supply constraints, and industrial reshoring initiatives across North America and Europe pushed manufacturers to prioritize real-time operational visibility, digital compliance tracking, and multi-site production synchronization.

The United States continues to dominate the global manufacturing operations management software landscape with nearly 34% market contribution, supported by over USD 12 billion in industrial digitalization investments across automotive, aerospace, electronics, and pharmaceutical manufacturing sectors. More than 61% of Tier-1 factories in the country now operate with integrated manufacturing execution and operations intelligence platforms, compared to under 45% in several developing industrial economies. Advanced smart factory deployments across Texas, Michigan, and Ohio improved production scheduling efficiency by approximately 22%, while industrial IoT integration rates exceeded 58% in high-value manufacturing environments.

Companies prioritizing interoperable manufacturing operations platforms, cybersecurity-enabled plant connectivity, and AI-driven production orchestration are securing faster operational scalability and stronger supply chain resilience in the high-growth industrial software ecosystem.

Market Size & Growth: USD 18120.71 Million in 2025 to USD 31065 Million by 2033 at 6.97% CAGR, driven by AI-led factory automation and supply chain digitization.

Top Growth Drivers: Cloud MES adoption rose 41%, predictive maintenance deployments increased 37%, and industrial IoT integration expanded 33% globally.

Short-Term Forecast: By 2027, manufacturers are projected to reduce production downtime by 19% and improve asset utilization by 24%.

Emerging Technologies: AI analytics, digital twins, and edge computing improved production accuracy by 21% across advanced manufacturing environments.

Regional Leaders: North America exceeded USD 6.8 Billion, Europe crossed USD 5.2 Billion, while Asia-Pacific advanced through 46% smart factory adoption.

Consumer/End-User Trends: Automotive and electronics industries represented over 52% of enterprise software deployments due to high-volume precision manufacturing.

Pilot/Case Example: In 2026, a multi-site automotive deployment improved production traceability by 31% and reduced defect rates by 14%.

Competitive Landscape: Top vendors controlled nearly 39% market share, with strong competition across industrial automation and cloud manufacturing ecosystems.

Regulatory & ESG Impact: Energy-monitoring integration lowered industrial power consumption by 16% amid stricter carbon reporting regulations in Europe.

Investment & Funding: Global industrial software investments surpassed USD 9.5 Billion through strategic partnerships, plant modernization, and regional expansion initiatives.

Innovation & Future Outlook: Autonomous production orchestration and AI-driven workflow optimization are reshaping next-generation connected manufacturing infrastructure.

Automotive manufacturing accounted for nearly 29% of enterprise software utilization, followed by electronics at 23% and pharmaceuticals at 17%, reflecting strong demand for traceability and real-time production control. AI-powered digital twins and edge-based analytics improved process accuracy by over 20% in high-volume factories, while Asia-Pacific recorded more than 46% smart manufacturing integration due to accelerated industrial automation investments. Ongoing supply chain diversification and stricter industrial compliance frameworks are pushing manufacturers toward unified operational intelligence platforms, positioning predictive and autonomous manufacturing ecosystems as the next strategic growth frontier.

Manufacturing operations management software is rapidly transforming from a plant-level monitoring tool into a core competitive infrastructure layer for industrial enterprises. Global manufacturers are accelerating investments in connected production ecosystems as labor shortages, volatile raw material cycles, and multi-site operational complexity intensify margin pressure. Real-time production orchestration platforms are now directly influencing throughput, compliance performance, and supply continuity across automotive, semiconductor, pharmaceutical, and industrial machinery sectors. The ongoing restructuring of global supply chains between Asia, North America, and Europe is forcing enterprises to prioritize operational visibility, resilient manufacturing execution, and synchronized factory intelligence.

AI-driven manufacturing operations platforms improve production efficiency by 27% while reducing operational costs by 18% compared to legacy on-premise manufacturing execution systems. Asia-Pacific leads in manufacturing volume, while North America leads in software adoption and industrial AI integration with nearly 58% smart factory penetration. Over the next three years, predictive production analytics and autonomous workflow optimization are expected to reduce equipment downtime by 22% and improve scheduling precision by 19%. ESG-focused production monitoring is also creating measurable competitive advantages by lowering industrial energy waste by 14% and strengthening regulatory compliance readiness.

In 2026, a global electronics manufacturer deploying unified operations management software across six facilities improved production traceability by 33% and reduced quality deviations by 16%. Industrial software providers are shifting capital allocation toward cloud-native architecture, cybersecurity-enabled factory connectivity, and edge intelligence platforms to secure long-term enterprise contracts. Companies optimizing integrated manufacturing ecosystems today are positioning themselves to dominate future autonomous production networks, industrial resilience strategies, and digitally synchronized global manufacturing operations.

Industrial manufacturers are accelerating deployment of manufacturing operations management software as smart factory investments intensify across automotive, electronics, and pharmaceutical production networks. More than 57% of large-scale manufacturers integrated AI-enabled production monitoring platforms in 2025, while cloud-based manufacturing execution deployments increased by 39% globally. Ongoing supply chain restructuring after semiconductor shortages and geopolitical trade shifts forced enterprises to prioritize real-time operational visibility and multi-site coordination. This transformation is directly improving production scheduling accuracy by nearly 21% and reducing unplanned downtime by 18%. In response, industrial technology providers are expanding regional delivery centers, increasing industrial AI investments, and forming strategic automation partnerships to secure long-term enterprise modernization contracts across high-output manufacturing sectors globally.

Complex integration requirements across legacy industrial infrastructure are constraining large-scale manufacturing operations management software deployment, particularly in aging production facilities with fragmented automation environments. Nearly 43% of manufacturers report interoperability limitations between legacy ERP systems and advanced plant-floor intelligence platforms, while cybersecurity incidents targeting industrial networks increased by 28% between 2024 and 2026. Rising compliance obligations surrounding industrial data protection and operational continuity are also increasing implementation costs by approximately 16%. Limited digital infrastructure maturity across emerging manufacturing economies continues delaying full-scale adoption timelines. To mitigate these risks, companies are diversifying software architecture strategies, adopting hybrid cloud deployment models, and increasing long-term cybersecurity investments alongside industrial network partnerships to stabilize enterprise-wide operational transformation initiatives globally.

Rapid expansion of autonomous manufacturing environments is creating high-impact opportunities for advanced manufacturing operations management software providers. Industrial AI adoption across smart factories increased by 44% in 2025, while edge-enabled production analytics improved operational response times by nearly 26%. Southeast Asia, India, and Eastern Europe are emerging as strategic manufacturing hubs due to supply chain diversification and lower operational costs, accelerating demand for scalable digital factory platforms. A major innovation shift toward digital twins and self-optimizing production workflows is redefining plant-level decision-making efficiency. Companies are responding by expanding regional cloud infrastructure, increasing industrial software R&D investments, and building integrated automation ecosystems that combine predictive analytics, industrial IoT, and cybersecurity capabilities to secure future manufacturing dominance and operational scalability.

Scalability limitations across multi-vendor manufacturing ecosystems remain a major challenge for manufacturing operations management software providers. Nearly 38% of industrial enterprises continue experiencing data synchronization delays between production equipment, ERP platforms, and AI-driven analytics systems, reducing operational consistency across global facilities. Rising industrial connectivity demands are also increasing edge computing infrastructure costs by approximately 17%, particularly in high-volume semiconductor and automotive production environments. Regulatory fragmentation across North America, Europe, and Asia is further complicating cross-border industrial data governance and software standardization. Companies seeking long-term competitiveness must strengthen interoperability frameworks, increase investment in industrial cybersecurity resilience, and develop strategic automation partnerships capable of supporting high-speed, real-time manufacturing intelligence across increasingly complex global production networks.

AI-enabled production orchestration adoption increased 42% across large factories in 2026, reshaping execution-level manufacturing control. Manufacturers are integrating real-time analytics with plant-floor automation to reduce scheduling delays by 19% and improve throughput accuracy by 23%. Labor shortages in electronics and automotive production are forcing companies to deploy autonomous workflow management systems faster. Industrial software vendors are responding through AI partnership expansion and edge-computing integration strategies.

Cloud-native manufacturing operations deployments expanded 38%, redefining multi-site operational visibility and scalability. Enterprises are shifting away from isolated plant systems toward centralized operational dashboards capable of synchronizing production across global facilities. Cloud-connected manufacturing environments reduced reporting delays by 27% and accelerated cross-site decision cycles by 18%. Companies are restructuring legacy infrastructure and prioritizing cybersecurity-enabled hybrid deployment frameworks to stabilize industrial connectivity and compliance management.

Asia-Pacific smart factory integration crossed 46%, while North America accelerated industrial AI standardization initiatives. Supply chain diversification and regional manufacturing relocation are shifting deployment intensity toward India, Vietnam, and Mexico. At the same time, U.S. manufacturers increased investment in interoperable manufacturing execution systems to improve traceability by 24%. Industrial software providers are expanding localized implementation services and regional support ecosystems to capture faster deployment demand.

Subscription-based modular software adoption rose 34%, shifting industrial purchasing behavior toward flexible operational models. Manufacturers are prioritizing modular deployment structures that reduce upfront implementation costs by nearly 16% while enabling faster process customization. A non-obvious shift is emerging as mid-sized factories increasingly bypass full-suite installations in favor of targeted operational intelligence modules. Software vendors are optimizing scalable licensing models and vertical-specific configurations to capture fragmented but accelerating industrial digitization demand.

The manufacturing operations management software market is segmented by type, application, and end-user industries, reflecting distinct operational priorities across industrial environments. Cloud-based deployments account for nearly 41% of demand due to scalable plant connectivity and centralized analytics capabilities, while hybrid models are gaining traction among regulated industries requiring secure infrastructure flexibility. Production planning and performance monitoring collectively represent over 36% of application demand as manufacturers prioritize throughput optimization and operational visibility. Automotive and electronics sectors dominate end-user adoption with approximately 52% combined share, driven by high-volume manufacturing complexity. Demand is steadily shifting toward AI-enabled modular platforms and predictive operations tools as enterprises pursue resilient, multi-site industrial execution capabilities.

Cloud-Based deployment dominates the manufacturing operations management software market with nearly 41% share, supported by scalable infrastructure, lower maintenance overhead, and faster multi-site integration capabilities. Large manufacturers are prioritizing cloud-connected production environments to improve operational visibility and reduce deployment timelines by approximately 24%. Hybrid Deployment is emerging as the fastest-growing segment, expanding adoption by nearly 29% as industrial enterprises seek secure interoperability between legacy infrastructure and modern cloud analytics systems. This shift is accelerating across regulated industries requiring localized data control alongside centralized operational intelligence.

Cloud-Based systems currently outperform On-Premises platforms in deployment flexibility and update efficiency, while On-Premises solutions retain strategic relevance in high-security manufacturing environments such as aerospace and defense. Integrated MOM Platforms and Modular MOM Systems collectively account for nearly 37% market demand, serving manufacturers prioritizing customized workflow management and phased implementation strategies. Companies are increasingly restructuring product portfolios toward modular cloud-native architecture, industrial AI integration, and cybersecurity-enabled deployment models. Investment focus is clearly shifting toward scalable hybrid ecosystems, while purely isolated legacy systems are gradually losing competitive relevance in globally connected manufacturing operations.

Production Planning leads the manufacturing operations management software market with approximately 24% share due to its direct influence on throughput optimization, resource utilization, and multi-site manufacturing coordination. Manufacturers are increasingly deploying advanced planning tools integrated with AI-driven forecasting systems to improve scheduling precision by nearly 22% and reduce production bottlenecks across high-volume industrial operations. Performance Monitoring is currently the fastest-growing application segment, expanding adoption by nearly 31% as enterprises prioritize real-time operational intelligence and predictive production management.

Production Planning remains deeply embedded across mature industrial ecosystems, while Performance Monitoring is redefining plant-level decision-making through live analytics and automated process visibility. Quality Management and Inventory Tracking collectively account for nearly 34% of application demand, particularly in electronics and pharmaceutical manufacturing where traceability and compliance pressures remain high. Maintenance Management and Workforce Management are also gaining strategic relevance as labor shortages and equipment reliability challenges intensify globally. Software providers are scaling predictive analytics capabilities, integrating industrial IoT functionality, and repositioning solutions around operational resilience, plant efficiency, and real-time production synchronization to capture accelerating enterprise modernization demand.

Automotive remains the leading end-user segment in the manufacturing operations management software market with nearly 29% share due to extensive dependence on synchronized production scheduling, quality traceability, and high-volume assembly automation. Automotive manufacturers continue prioritizing integrated manufacturing intelligence platforms capable of reducing production downtime by approximately 19% while improving supply chain coordination across global facilities. Pharmaceuticals is emerging as the fastest-growing end-user segment, with adoption increasing by nearly 32% as compliance-intensive production environments accelerate digital batch tracking, validation monitoring, and operational audit automation.

Automotive demand is driven by scale and production complexity, while pharmaceutical companies are reshaping buying behavior around compliance resilience and real-time manufacturing transparency. Electronics, Food and Beverage, Aerospace and Defense, and Chemicals collectively contribute nearly 54% of market demand through increasing deployment of predictive maintenance, inventory synchronization, and operational analytics platforms. Industrial software providers are responding through sector-specific customization, subscription-based deployment models, and strategic automation partnerships tailored to unique manufacturing requirements. Future demand is increasingly shifting toward highly regulated and precision-driven industries where operational traceability and intelligent production control deliver measurable competitive advantage.

North America accounted for the largest market share at 34% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 8.12% between 2026 and 2033.

North America continues leading in enterprise-scale deployments and industrial AI integration, supported by over 58% smart factory penetration across automotive, aerospace, and semiconductor manufacturing. Europe holds nearly 27% market share, driven by compliance-focused digital manufacturing initiatives and energy-efficiency mandates accelerating adoption of integrated operational intelligence platforms. Meanwhile, Asia-Pacific is rapidly reshaping demand dynamics through manufacturing relocation, industrial infrastructure expansion, and localized production digitization across China, India, Vietnam, and South Korea, where factory automation adoption exceeded 46% in 2025. Latin America and the Middle East are also accelerating deployment activity through industrial modernization investments. Global software providers are increasingly prioritizing Asia-Pacific expansion while strengthening North American innovation capabilities and Europe-focused compliance optimization strategies.

North America commands nearly 34% of global manufacturing operations management software demand, driven by advanced adoption across automotive, aerospace, electronics, and pharmaceutical manufacturing. U.S.-based manufacturers continue accelerating digital factory transformation as supply chain reshoring and labor shortages intensify operational pressure. More than 58% of large industrial facilities now operate with AI-enabled production monitoring systems, while cloud-connected manufacturing execution deployments increased by 36% between 2024 and 2026. Enterprises are prioritizing predictive analytics, cybersecurity-enabled plant connectivity, and real-time operational intelligence to improve production efficiency and compliance visibility. Major industrial software vendors expanded regional implementation partnerships and industrial AI investment programs during 2026, reinforcing North America’s position as the primary innovation hub for scalable, enterprise-grade manufacturing operations management ecosystems.

Europe represents approximately 27% of global manufacturing operations management software demand, with Germany, France, and Italy leading industrial deployment intensity across automotive, machinery, and pharmaceutical sectors. Strict carbon accountability frameworks and industrial energy-efficiency regulations are forcing manufacturers to integrate real-time operational monitoring and digital compliance management systems. More than 49% of large European factories adopted advanced energy-optimization analytics platforms in 2025, while production traceability deployments improved regulatory reporting efficiency by nearly 21%. Manufacturers are increasingly favoring interoperable hybrid deployment models that balance cybersecurity, sustainability compliance, and operational flexibility. Industrial software providers are expanding localized compliance-focused solutions and AI-enabled reporting capabilities, making Europe a critical region for manufacturing intelligence innovation shaped by regulatory precision and operational sustainability requirements.

Asia-Pacific ranks as the fastest-expanding regional market due to large-scale manufacturing concentration across China, India, Japan, South Korea, and Southeast Asia. The region accounted for nearly 31% of global deployment demand in 2025, supported by aggressive factory automation programs and expanding industrial infrastructure investment. Smart manufacturing integration exceeded 46% across major export-driven facilities, while localized software deployment timelines improved by approximately 24% due to regional cloud infrastructure expansion. Manufacturers are rapidly digitizing production management systems to strengthen supply chain responsiveness and reduce operational bottlenecks amid global manufacturing relocation trends. Enterprises across Asia-Pacific prioritize scalability, deployment speed, and operational cost efficiency, prompting industrial software providers to expand regional delivery networks, localized analytics capabilities, and industry-specific automation partnerships to secure long-term manufacturing transformation opportunities.

South America contributes nearly 5% of global manufacturing operations management software demand, with Brazil and Argentina leading deployment activity across food processing, automotive, and chemicals manufacturing sectors. Industrial modernization initiatives and export-focused manufacturing expansion are increasing demand for production monitoring and operational synchronization platforms. However, infrastructure limitations, currency volatility, and uneven digital connectivity continue constraining enterprise-wide deployment scalability across several manufacturing corridors. Cloud-based industrial software adoption increased by 19% in 2025 as mid-sized manufacturers pursued lower-cost operational digitization models. Enterprises remain highly price-sensitive and increasingly favor modular deployment structures that reduce upfront implementation complexity. Industrial software providers expanding localized service capabilities and flexible subscription models are better positioned to capture emerging industrial transformation demand while navigating regional operational and economic constraints.

Middle East & Africa accounts for approximately 3% of global manufacturing operations management software demand, with Saudi Arabia, the UAE, and South Africa driving most deployment activity through industrial diversification and infrastructure modernization programs. Oil and gas processing, construction materials, and industrial manufacturing sectors are increasingly adopting operational intelligence platforms to improve production coordination and energy efficiency. Smart industrial facility deployments increased by nearly 22% between 2024 and 2026, while cloud-enabled operational monitoring adoption expanded by 18% across large infrastructure projects. Enterprises are prioritizing scalable digital manufacturing systems that support rapid industrial expansion and centralized operational visibility. Industrial technology providers are strengthening regional partnerships and implementation ecosystems, positioning the region as a strategic long-term opportunity tied to industrial transformation and infrastructure-led economic diversification.

United States – 34% market share: The Manufacturing Operations Management Software Market in the United States is dominated by advanced smart factory deployment, industrial AI integration, and large-scale manufacturing digitalization across automotive, aerospace, and semiconductor sectors.

China – 18% market share: The Manufacturing Operations Management Software Market in China is driven by massive industrial production capacity, export-focused manufacturing expansion, and rapid factory automation adoption supported by localized industrial infrastructure investment.

The manufacturing operations management software market is dominated by competition between global industrial automation leaders, cloud-native software providers, and specialized manufacturing intelligence vendors including Siemens, Rockwell Automation, ABB, Dassault Systèmes, and Emerson Electric. The top five players collectively control nearly 39% market share through integrated automation ecosystems, industrial AI capabilities, and enterprise-scale deployment infrastructure. Competition is increasingly shifting from standalone manufacturing execution systems toward interoperable cloud-connected operational intelligence platforms capable of reducing downtime by 18% and improving production visibility by 24%. Global leaders are aggressively expanding through regional partnerships, AI-driven analytics integration, and vertical-specific product customization, while mid-tier providers compete through lower deployment costs and modular scalability. Industrial cybersecurity, integration complexity, and legacy infrastructure compatibility remain major entry barriers. Companies capable of combining real-time analytics, scalable deployment speed, and sector-specific operational precision are securing the strongest long-term competitive positioning in advanced manufacturing environments.

Siemens

Rockwell Automation

ABB

Dassault Systèmes

Emerson Electric

Honeywell International

Schneider Electric

SAP

AVEVA

General Electric Digital

Oracle

IBM

Plex Systems

Critical Manufacturing

AI-driven manufacturing operations platforms are becoming the operational core of advanced factories between 2026 and 2028. More than 57% of large industrial facilities now deploy AI-enabled production analytics to improve scheduling precision and reduce unplanned downtime by nearly 18%. Integrated digital twin technology is also optimizing production simulation accuracy by 24%, allowing manufacturers to identify bottlenecks before physical deployment. Compared to legacy rule-based manufacturing execution systems, AI-powered autonomous workflow orchestration improves operational efficiency by 27% while lowering process management costs by 16%. Automotive, semiconductor, and pharmaceutical manufacturers are gaining the strongest competitive advantage through faster production synchronization and predictive operational control.

Cloud-native manufacturing operations management platforms are accelerating enterprise-wide integration across multi-site industrial networks. Nearly 49% of manufacturers shifted toward hybrid cloud deployment models in 2026 to improve operational visibility and centralized decision-making. Edge computing integration reduced production response latency by approximately 21%, particularly in high-speed electronics and precision manufacturing environments. Companies are increasingly combining industrial IoT, cloud MES, and real-time analytics platforms to improve traceability, compliance management, and production adaptability amid ongoing global supply chain restructuring.

Disruptive industrial AI agents and autonomous operations copilots are redefining factory execution models. Industrial AI deployments improved workforce productivity by up to 50% in early large-scale implementations, while AI-enabled robotic coordination accelerated material handling efficiency by 20%. Manufacturing software providers are rapidly expanding cybersecurity-enabled edge AI infrastructure and interoperable data ecosystems to support fully connected industrial operations. Enterprises acting now are securing stronger production resilience, faster operational scaling, and long-term leadership in autonomous manufacturing transformation.

April 2024 – AVEVA launched a hybrid cloud Manufacturing Execution System solution integrating AI analytics and enterprise-wide operational visualization across distributed plants. The platform improved multi-site production visibility and accelerated operational synchronization by nearly 24%, strengthening industrial cloud adoption strategies globally. [Hybrid Cloud Shift] Source: AVEVA

June 2024 – AVEVA and AWS entered a strategic collaboration agreement to accelerate industrial AI deployment and cloud-native manufacturing intelligence integration. The partnership focused on reducing industrial data interoperability complexity and improving AI-driven decision workflows across manufacturing environments. [Industrial AI Alliance] Source: AVEVA AWS Collaboration

May 2025 – Siemens introduced advanced AI agents for industrial automation capable of autonomously executing production workflows. The company stated that industrial productivity could improve by up to 50% through AI-enabled operational copilots integrated across manufacturing ecosystems. [Autonomous Factory Push] Source: Siemens Press Release

June 2025 – Siemens expanded autonomous production capabilities by integrating Operations Copilot into automated guided vehicles and mobile robotics systems. The deployment enhanced real-time shop-floor material coordination and accelerated intelligent robotic task execution across advanced manufacturing facilities. [AI Robotics Integration] Source: Siemens Autonomous Production Update

This report delivers a comprehensive assessment of the manufacturing operations management software market across deployment types, operational applications, end-user industries, regional performance, and emerging industrial technologies. The analysis covers Cloud-Based, On-Premises, Hybrid Deployment, Integrated MOM Platforms, and Modular MOM Systems alongside core applications including production planning, quality management, performance monitoring, maintenance management, workforce management, and inventory tracking. End-user evaluation spans automotive, electronics, pharmaceuticals, food and beverage, aerospace and defense, and chemicals manufacturing sectors across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa.

The report analyzes more than 25 strategic market indicators including deployment adoption rates, smart factory integration levels, operational efficiency metrics, and industrial AI implementation trends. Nearly 57% of large-scale manufacturers deploying AI-enabled operational analytics and over 46% smart factory penetration across Asia-Pacific manufacturing hubs are evaluated to identify execution-level demand shifts and technology scaling patterns. The study also profiles leading industrial software providers, competitive positioning strategies, hybrid cloud adoption trends, and edge-enabled manufacturing intelligence systems shaping operational transformation between 2026 and 2033.

The report supports investment prioritization, regional expansion planning, product positioning, partnership strategy, and competitive benchmarking by identifying where industrial software demand is accelerating, which deployment models are scaling fastest, and how enterprises are restructuring manufacturing intelligence ecosystems to secure long-term operational resilience and production optimization advantages.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 18120.71 Million |

|

Market Revenue in 2033 |

USD 31065 Million |

|

CAGR (2026 - 2033) |

6.97% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Siemens, Rockwell Automation, ABB, Dassault Systèmes, Emerson Electric, Honeywell International, Schneider Electric, SAP, AVEVA, General Electric Digital, Oracle, IBM, Plex Systems, Critical Manufacturing |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |