Reports

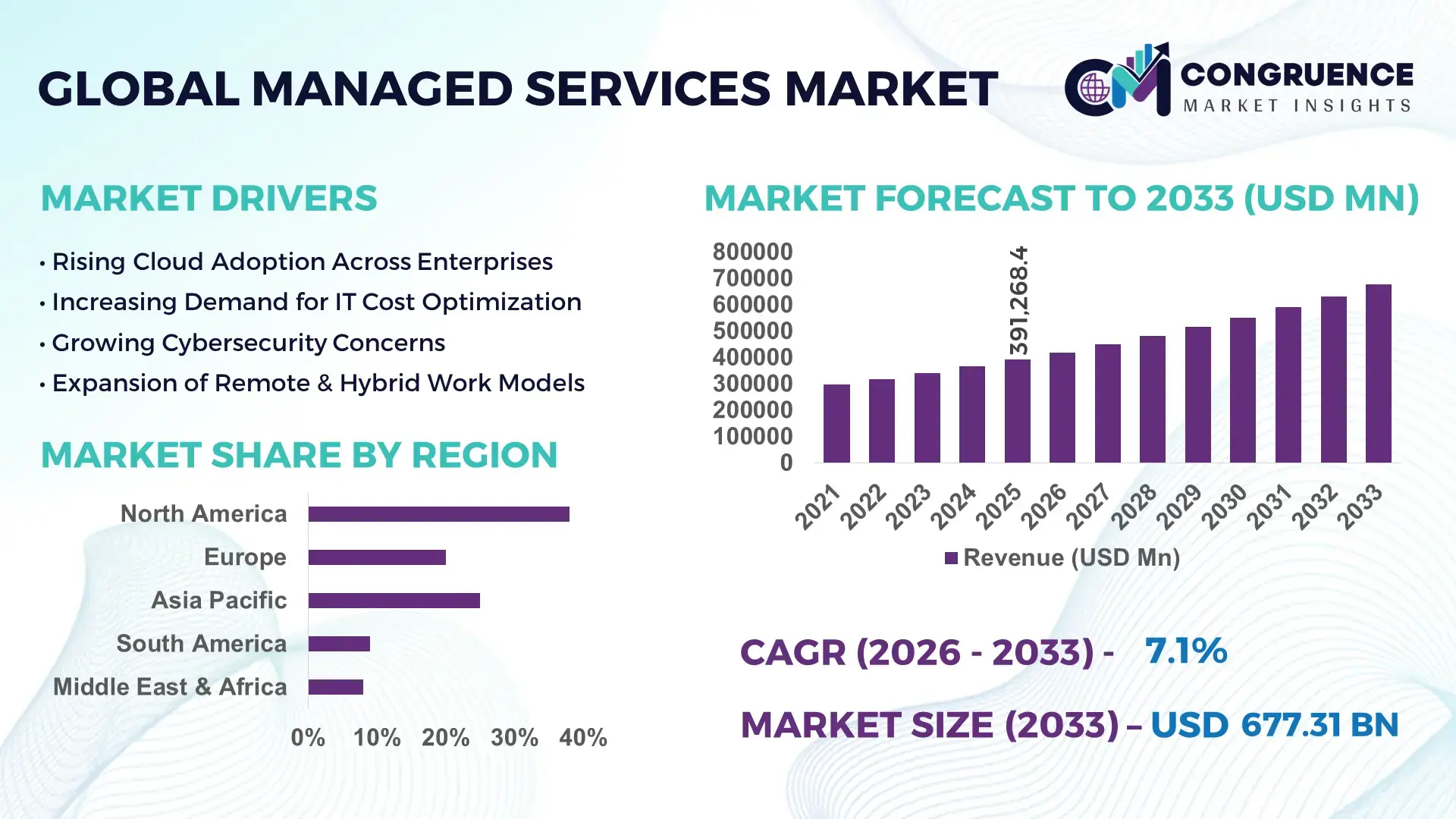

The Global Managed Services Market was valued at USD 391268.43 Million in 2025 and is anticipated to reach a value of USD 677314.81 Million by 2033 expanding at a CAGR of 7.1% between 2026 and 2033. This growth is primarily driven by increasing enterprise demand for scalable IT infrastructure and cost-efficient operational models.

The United States continues to lead the managed services market with extensive enterprise IT outsourcing capabilities and advanced digital infrastructure investments. Over 68% of large enterprises in the country rely on managed IT services for cloud, cybersecurity, and network management functions. The U.S. hosts more than 5,000 managed service providers, with annual enterprise IT spending exceeding USD 2 trillion. Cloud adoption rates surpass 90% among Fortune 500 companies, significantly boosting demand for managed cloud services. Key sectors such as BFSI, healthcare, and retail contribute heavily to adoption, with healthcare alone reporting over 40% reliance on managed security services due to regulatory requirements.

Market Size & Growth: Valued at USD 391268.43 million in 2025, projected to reach USD 677314.81 million by 2033 at a CAGR of 7.1%, driven by rapid cloud adoption and IT outsourcing demand.

Top Growth Drivers: Cloud adoption (78%), cybersecurity demand increase (65%), IT cost optimization (52%).

Short-Term Forecast: By 2028, managed services are expected to reduce enterprise IT operational costs by up to 30% while improving system uptime by 25%.

Emerging Technologies: AI-driven IT operations (AIOps), edge computing integration, and zero-trust cybersecurity frameworks.

Regional Leaders: North America projected at USD 245 billion by 2033 with strong cloud penetration; Europe at USD 180 billion driven by compliance needs; Asia-Pacific at USD 160 billion with rapid SME adoption.

Consumer/End-User Trends: BFSI and healthcare sectors dominate usage, with over 60% enterprises outsourcing security and infrastructure management.

Pilot or Case Example: In 2024, a global retail firm achieved 35% downtime reduction through AI-powered managed network services.

Competitive Landscape: Market leader holds approximately 12% share, followed by key players including IBM, Accenture, Cisco, TCS, and Infosys.

Regulatory & ESG Impact: Data protection regulations and carbon-neutral IT initiatives are pushing adoption of energy-efficient managed data centers.

Investment & Funding Patterns: Over USD 25 billion invested in managed services innovation and cloud partnerships in recent years.

Innovation & Future Outlook: Integration of AI automation, hybrid cloud ecosystems, and predictive analytics is shaping future service delivery models.

The managed services market is supported by diverse industry sectors, with BFSI contributing approximately 28% of demand, followed by IT and telecom at 22%, and healthcare at 18%. Recent innovations such as AI-powered monitoring tools and automated incident response systems are improving service efficiency by over 40%. Regulatory frameworks like GDPR and evolving data sovereignty laws are influencing service deployment strategies globally. Asia-Pacific shows strong consumption growth due to digital transformation in SMEs, while Europe emphasizes compliance-driven adoption. Future trends indicate increased demand for hybrid cloud management and integrated cybersecurity services, positioning managed services as a core component of enterprise IT strategy.

The strategic relevance of the managed services market lies in its ability to deliver operational efficiency, scalability, and risk mitigation for enterprises navigating complex digital ecosystems. Organizations are increasingly outsourcing IT infrastructure and security operations to reduce capital expenditure while maintaining high service quality. Advanced technologies such as AI-driven IT operations deliver 40% faster incident resolution compared to traditional manual IT management systems, enabling proactive service delivery and minimizing downtime.

North America dominates in volume due to mature IT infrastructure, while Asia-Pacific leads in adoption with over 62% of enterprises embracing managed cloud and network services. The growing reliance on hybrid and multi-cloud environments is further driving demand for specialized managed services providers capable of integrating diverse platforms seamlessly. By 2028, AI-powered automation in managed services is expected to improve operational efficiency by 35% and reduce system downtime by nearly 30%.

From an ESG perspective, firms are committing to sustainable IT operations, including a 25% reduction in data center energy consumption by 2030 through managed green cloud solutions. In 2024, a European telecom provider achieved a 28% reduction in operational costs by implementing AI-based managed network services, demonstrating the tangible benefits of technological integration. The evolving regulatory landscape, including stricter data privacy and cybersecurity mandates, is compelling organizations to rely on managed services for compliance assurance. As digital transformation accelerates, the managed services market is emerging as a critical pillar for enterprise resilience, regulatory compliance, and long-term sustainable growth.

The widespread adoption of cloud computing is a primary driver of the managed services market, as enterprises seek expert support for managing complex cloud environments. Over 85% of global enterprises have adopted multi-cloud strategies, creating a need for specialized managed services to ensure seamless integration, monitoring, and security. Managed cloud services improve operational efficiency by up to 45% through automation and centralized management. Additionally, businesses are increasingly migrating legacy systems to cloud platforms, which requires ongoing maintenance, optimization, and compliance management. The demand is particularly strong in sectors such as banking and healthcare, where secure and reliable data handling is essential. As organizations prioritize agility and scalability, managed services providers play a critical role in enabling efficient cloud adoption and long-term infrastructure optimization.

Despite its advantages, the managed services market faces restraints related to data security risks and dependency on third-party providers. Approximately 48% of enterprises express concerns about potential data breaches when outsourcing IT operations. Vendor lock-in is another challenge, as organizations may face difficulties in switching providers due to proprietary systems and long-term contracts. Additionally, compliance with region-specific data protection regulations adds complexity, particularly for multinational companies. Limited transparency in service delivery and performance metrics can also impact trust between clients and providers. Small and medium enterprises may hesitate to adopt managed services due to perceived risks and lack of control over critical IT functions. These factors collectively slow adoption rates in certain sectors and regions.

AI-driven automation presents significant growth opportunities in the managed services market by enhancing operational efficiency and service quality. Automated monitoring systems can detect and resolve issues up to 60% faster than traditional methods, reducing downtime and improving customer satisfaction. The integration of predictive analytics allows service providers to anticipate system failures and optimize performance proactively. Emerging markets, particularly in Asia-Pacific, offer substantial opportunities as SMEs increasingly adopt digital technologies and require cost-effective IT management solutions. Furthermore, the rise of edge computing and IoT ecosystems is creating demand for specialized managed services capable of handling decentralized networks. These advancements are enabling providers to expand their service portfolios and deliver higher-value solutions to clients.

The managed services market faces challenges related to increasing operational complexity and a shortage of skilled professionals. As enterprises adopt multi-cloud and hybrid environments, managing diverse platforms and ensuring seamless integration becomes more difficult. Approximately 54% of service providers report a shortage of skilled IT professionals, particularly in areas such as cybersecurity and cloud architecture. This talent gap limits the ability of providers to scale services and meet growing demand. Additionally, maintaining high service quality while managing multiple clients with varying requirements adds to operational challenges. The need for continuous training and upskilling further increases costs for service providers. These factors create barriers to efficient service delivery and may impact overall market growth.

• AI-Driven Automation Enhancing Operational Efficiency: The integration of AI-driven automation in managed services is transforming service delivery models, with over 67% of enterprises implementing AIOps platforms to streamline IT operations. Automated incident management systems are reducing mean time to resolution by nearly 45%, while predictive maintenance tools are lowering system downtime by up to 38%. Organizations leveraging AI-enabled monitoring report a 30% improvement in service-level agreement compliance, particularly in network and infrastructure management. This trend is particularly strong in sectors such as BFSI and telecom, where real-time analytics and rapid issue resolution are critical for maintaining uninterrupted operations.

• Rapid Expansion of Hybrid and Multi-Cloud Environments: Hybrid and multi-cloud strategies are gaining traction, with approximately 82% of enterprises adopting multi-cloud architectures to enhance flexibility and avoid vendor lock-in. Managed service providers are increasingly offering integrated solutions that support seamless workload migration and cross-platform management. Enterprises utilizing hybrid cloud-managed services report a 28% improvement in resource utilization and a 35% reduction in operational complexity. This trend is accelerating in Asia-Pacific, where over 60% of SMEs are transitioning to hybrid cloud models to support digital transformation initiatives and improve scalability.

• Rising Demand for Cybersecurity Managed Services: Cybersecurity remains a critical focus area, with 72% of organizations outsourcing security operations to managed service providers due to increasing cyber threats. Managed detection and response services have improved threat detection accuracy by 50% and reduced breach response times by 40%. The adoption of zero-trust security frameworks has increased by 55%, particularly in regulated industries such as healthcare and finance. Additionally, organizations implementing managed security services report a 25% reduction in compliance-related risks, driven by stricter global data protection regulations.

• Growth in Industry-Specific and Verticalized Services: The demand for industry-specific managed services is increasing, with over 58% of enterprises opting for customized solutions tailored to their operational needs. Vertical-specific offerings in healthcare, manufacturing, and retail are improving process efficiency by up to 33% through specialized analytics and automation tools. For instance, managed services in manufacturing are enabling predictive maintenance, reducing equipment downtime by 27%. Similarly, retail enterprises leveraging managed analytics services are experiencing a 20% improvement in customer engagement metrics, highlighting the growing importance of sector-focused service models.

The managed services market segmentation reflects a diverse and evolving landscape driven by enterprise IT modernization and digital transformation strategies. By type, the market includes managed infrastructure, managed security, managed network, and managed cloud services, each addressing specific operational needs. Applications span across IT and telecom, BFSI, healthcare, retail, and manufacturing sectors, where service adoption varies based on regulatory requirements and operational complexity. End-user insights reveal strong adoption among large enterprises, while small and medium enterprises are increasingly leveraging managed services for cost efficiency and scalability. Approximately 65% of demand originates from organizations undergoing cloud migration and cybersecurity enhancement initiatives. Regional variations further shape segmentation, with North America focusing on advanced security services, while Asia-Pacific demonstrates strong growth in cloud and network management services.

Managed services by type encompass managed infrastructure services, managed network services, managed security services, and managed cloud services. Managed cloud services currently lead the segment, accounting for approximately 36% of total adoption, driven by widespread enterprise migration to cloud-based platforms and the need for continuous optimization. Managed security services follow with around 28% adoption, reflecting the growing importance of cybersecurity in enterprise IT strategies. However, managed security services are the fastest-growing segment, expanding at an estimated rate of 9.2% annually due to increasing cyber threats and regulatory compliance requirements.

Managed network services and managed infrastructure services collectively contribute nearly 36% of the market, supporting connectivity, system performance, and legacy system management. These services remain critical for organizations maintaining hybrid IT environments. The rise of edge computing and IoT integration is further enhancing the relevance of network management solutions, particularly in industrial and manufacturing applications.

The application landscape of the managed services market is dominated by the IT and telecom sector, which accounts for approximately 34% of total adoption due to its reliance on continuous network monitoring and infrastructure management. The BFSI sector follows with a 26% share, driven by stringent data security requirements and the need for real-time transaction processing. Healthcare represents around 18% of the market, leveraging managed services for secure data handling and regulatory compliance. Among these, healthcare is the fastest-growing application segment, expanding at an estimated rate of 10.1% annually, supported by increasing adoption of digital health records and telemedicine platforms. Retail and manufacturing sectors collectively contribute about 22%, utilizing managed services for supply chain optimization and customer analytics.

End-user segmentation highlights large enterprises as the dominant segment, accounting for approximately 61% of total managed services adoption due to their extensive IT infrastructure and higher investment capacity. Small and medium enterprises (SMEs) represent around 39% of the market, increasingly adopting managed services to reduce operational costs and access advanced technologies without significant capital expenditure. SMEs are the fastest-growing end-user segment, with an estimated growth rate of 9.8% annually, driven by digital transformation initiatives and the need for scalable IT solutions. Adoption among SMEs has increased by over 25% in the past three years, particularly in emerging economies where cloud-based managed services offer cost-effective alternatives to in-house IT management.

Other end-users, including government agencies and educational institutions, contribute significantly to the market by adopting managed services for secure data management and infrastructure modernization. These segments collectively account for a notable share of enterprise IT outsourcing activities.

Region North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 9.4% between 2026 and 2033.

North America’s dominance is supported by over 70% enterprise cloud adoption and more than 65% of organizations outsourcing IT infrastructure management. Europe follows with approximately 27% market share, driven by strict regulatory compliance and data protection frameworks impacting over 80% of enterprises. Asia-Pacific holds nearly 23% share, with over 60% of SMEs adopting managed services for digital transformation. South America contributes around 7%, while Middle East & Africa collectively account for about 5%, supported by increasing investments in smart infrastructure and IT modernization. Across all regions, more than 75% of large enterprises rely on managed cybersecurity services, while hybrid cloud deployments exceed 68% adoption globally, reinforcing strong regional demand variations.

How are enterprise cloud strategies accelerating advanced service adoption?

North America holds approximately 38% of the managed services market share, driven by high enterprise IT spending and early adoption of digital transformation strategies. Key industries such as BFSI, healthcare, and IT & telecom collectively account for over 60% of regional demand, with healthcare alone reporting more than 45% reliance on managed security services. Regulatory frameworks such as data privacy mandates and cybersecurity compliance policies influence over 70% of service contracts. Technological advancements including AI-driven automation and hybrid cloud integration are widely adopted, with over 80% of enterprises using multi-cloud environments. A leading regional player has expanded AI-based managed network solutions, improving client system uptime by 32%. Consumer behavior in this region shows strong preference for outsourced IT services, particularly among large enterprises seeking scalability, operational efficiency, and enhanced cybersecurity resilience.

How are regulatory compliance demands reshaping enterprise outsourcing strategies?

Europe accounts for nearly 27% of the managed services market, with key markets including Germany, the UK, and France contributing over 65% of regional demand. Strict regulatory frameworks such as GDPR influence more than 85% of enterprises to adopt managed security and compliance services. Sustainability initiatives and green IT policies are also driving adoption, with over 40% of data centers transitioning to energy-efficient models. Emerging technologies such as edge computing and AI-driven monitoring tools are being implemented by more than 55% of enterprises to improve operational efficiency. A prominent regional provider has introduced carbon-neutral managed cloud services, reducing data center emissions by 22%. Consumer behavior reflects a strong emphasis on compliance and transparency, with over 60% of organizations prioritizing explainable and auditable managed service solutions.

What factors are driving rapid digital transformation across enterprise ecosystems?

Asia-Pacific ranks as the fastest-growing region and holds approximately 23% of the managed services market, with China, India, and Japan accounting for over 70% of regional consumption. Rapid infrastructure development and increasing digitalization have led to over 62% of SMEs adopting managed cloud and network services. The region is witnessing strong growth in e-commerce and mobile-based platforms, with digital transactions increasing by over 50% in recent years. Technology hubs are expanding, particularly in India and Southeast Asia, where over 45% of startups rely on managed IT services. A regional provider has deployed AI-powered managed services across manufacturing clusters, improving operational efficiency by 29%. Consumer behavior highlights strong demand for cost-effective, scalable solutions, with SMEs prioritizing cloud-based managed services to support rapid business expansion.

How are infrastructure modernization and digital adoption influencing service demand?

South America contributes approximately 7% to the global managed services market, with Brazil and Argentina accounting for over 65% of regional demand. Infrastructure modernization initiatives and increasing digital adoption are key growth drivers, with over 48% of enterprises transitioning to cloud-based systems. The energy and telecommunications sectors represent more than 50% of managed service usage, driven by the need for efficient network management and system optimization. Government incentives promoting digital transformation have led to a 20% increase in IT outsourcing projects. A local service provider has implemented managed network solutions for telecom operators, improving network reliability by 26%. Consumer behavior in the region is influenced by demand for localized content and language-specific services, particularly in media and digital communication platforms.

How are smart infrastructure investments shaping enterprise IT outsourcing trends?

The Middle East & Africa region accounts for nearly 5% of the managed services market, with major growth in countries such as the UAE and South Africa. Demand is largely driven by oil & gas, construction, and financial services sectors, which together contribute over 55% of regional adoption. Technological modernization initiatives, including smart city projects, have increased managed service adoption by 30% in urban areas. Regulatory frameworks and trade partnerships are encouraging digital transformation, with over 40% of enterprises investing in cloud-based solutions. A regional provider has deployed managed cybersecurity services for financial institutions, reducing security incidents by 24%. Consumer behavior reflects growing interest in digital services, with enterprises prioritizing secure, scalable IT infrastructure to support economic diversification efforts.

United States – 34% Managed Services market share: High enterprise IT spending, advanced cloud infrastructure, and over 68% enterprise outsourcing adoption drive dominance in the Managed Services market.

China – 16% Managed Services market share: Strong digital transformation initiatives, expanding SME adoption exceeding 60%, and rapid cloud infrastructure development support growth in the Managed Services market.

The managed services market is moderately fragmented, with over 300 active global and regional service providers competing across diverse service categories such as cloud, network, and cybersecurity management. The top five companies collectively account for approximately 42% of the total market share, indicating a competitive yet consolidated structure among leading players. Market leaders focus on expanding service portfolios through strategic partnerships, mergers, and acquisitions, with over 120 major deals recorded in the past three years. Innovation remains a key differentiator, with more than 65% of providers investing in AI-driven automation and predictive analytics to enhance service delivery. Additionally, around 58% of companies are integrating hybrid cloud management capabilities to address evolving enterprise needs. Competitive positioning is further influenced by industry-specific solutions, with over 40% of providers offering customized services for sectors such as healthcare, finance, and manufacturing. Pricing strategies and service-level agreements also play a critical role, as enterprises increasingly demand measurable performance improvements and cost optimization.

IBM

Accenture

Cisco Systems

Tata Consultancy Services (TCS)

Infosys

Wipro

HCL Technologies

Fujitsu

NTT Data

DXC Technology

Cognizant

Capgemini

Atos

Tech Mahindra

Verizon Communications

The managed services market is undergoing rapid technological transformation driven by the integration of advanced digital tools, automation frameworks, and intelligent analytics platforms. Artificial Intelligence for IT Operations (AIOps) is now deployed by over 65% of large enterprises, enabling predictive incident detection and reducing unplanned downtime by up to 40%. Machine learning algorithms are increasingly used to analyze system logs and network patterns, improving threat detection accuracy by nearly 50% and enhancing proactive maintenance capabilities across hybrid IT environments.

Cloud-native technologies are also reshaping service delivery models, with more than 70% of organizations leveraging containerization and microservices architectures. Kubernetes-based orchestration platforms are enabling managed service providers to automate deployment and scaling processes, improving infrastructure efficiency by approximately 35%. Edge computing is another critical innovation, with over 45% of enterprises implementing edge-managed services to support low-latency applications such as IoT, autonomous systems, and real-time analytics.

Cybersecurity technologies, including zero-trust architectures and Secure Access Service Edge (SASE), are gaining widespread adoption, with nearly 60% of enterprises integrating these frameworks into their managed security services. Automation in cybersecurity operations has reduced incident response times by over 30%, while enhancing compliance monitoring across multiple regulatory environments. Additionally, robotic process automation (RPA) is being used to streamline repetitive IT tasks, improving operational productivity by 25%.

The integration of advanced analytics and real-time dashboards is further empowering decision-makers with actionable insights, enabling data-driven service optimization. These technologies collectively position managed services as a critical enabler of digital transformation, operational resilience, and enterprise scalability.

• In March 2025, Accenture expanded its managed services portfolio by launching an AI-powered platform for enterprise IT operations, integrating predictive analytics and automation capabilities. The solution improved incident resolution efficiency by over 35% across pilot enterprise deployments. Source: www.accenture.com

• In October 2024, IBM introduced enhancements to its managed cloud services by integrating generative AI tools into hybrid cloud environments. This development enabled enterprises to automate workload management and improve infrastructure performance by approximately 30%. Source: www.ibm.com

• In January 2025, Cisco announced advancements in its managed security services, incorporating zero-trust architecture and AI-driven threat detection. The update significantly reduced security breach response times by nearly 40% for enterprise clients. Source: www.cisco.com

• In July 2024, Tata Consultancy Services (TCS) launched a next-generation managed services framework focused on cloud modernization and automation. The initiative enabled clients to achieve up to 28% improvement in operational efficiency and faster deployment cycles. Source: www.tcs.com

The Managed Services Market Report provides a comprehensive analysis of service types, applications, end-user industries, and regional dynamics shaping the global market landscape. The report covers core service segments including managed infrastructure, managed network, managed cloud, and managed security services, which collectively account for over 90% of enterprise outsourcing activities. It also examines emerging segments such as edge-managed services and AI-driven operations, which are gaining traction among organizations adopting advanced digital ecosystems.

Geographically, the report spans key regions including North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, representing 100% of global market activity. It highlights regional variations in adoption patterns, with over 70% enterprise penetration in developed markets and rapidly increasing SME adoption exceeding 60% in emerging economies. The report further analyzes application-specific demand across industries such as BFSI, healthcare, IT & telecom, retail, and manufacturing, which together contribute more than 85% of total managed services utilization.

From a technological perspective, the report evaluates the impact of AI, cloud computing, cybersecurity frameworks, and automation tools, which are being adopted by over 65% of enterprises globally. It also includes insights into regulatory environments, compliance requirements, and ESG considerations influencing service deployment strategies. Additionally, the report addresses evolving customer preferences, including demand for scalable, cost-efficient, and secure IT solutions. This structured scope ensures a holistic understanding of market trends, competitive positioning, and future growth opportunities for business decision-makers.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

7.1% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

IBM, Accenture, Cisco Systems, Tata Consultancy Services (TCS), Infosys, Wipro, HCL Technologies, Fujitsu, NTT Data, DXC Technology, Cognizant, Capgemini, Atos, Tech Mahindra, Verizon Communications |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |