Reports

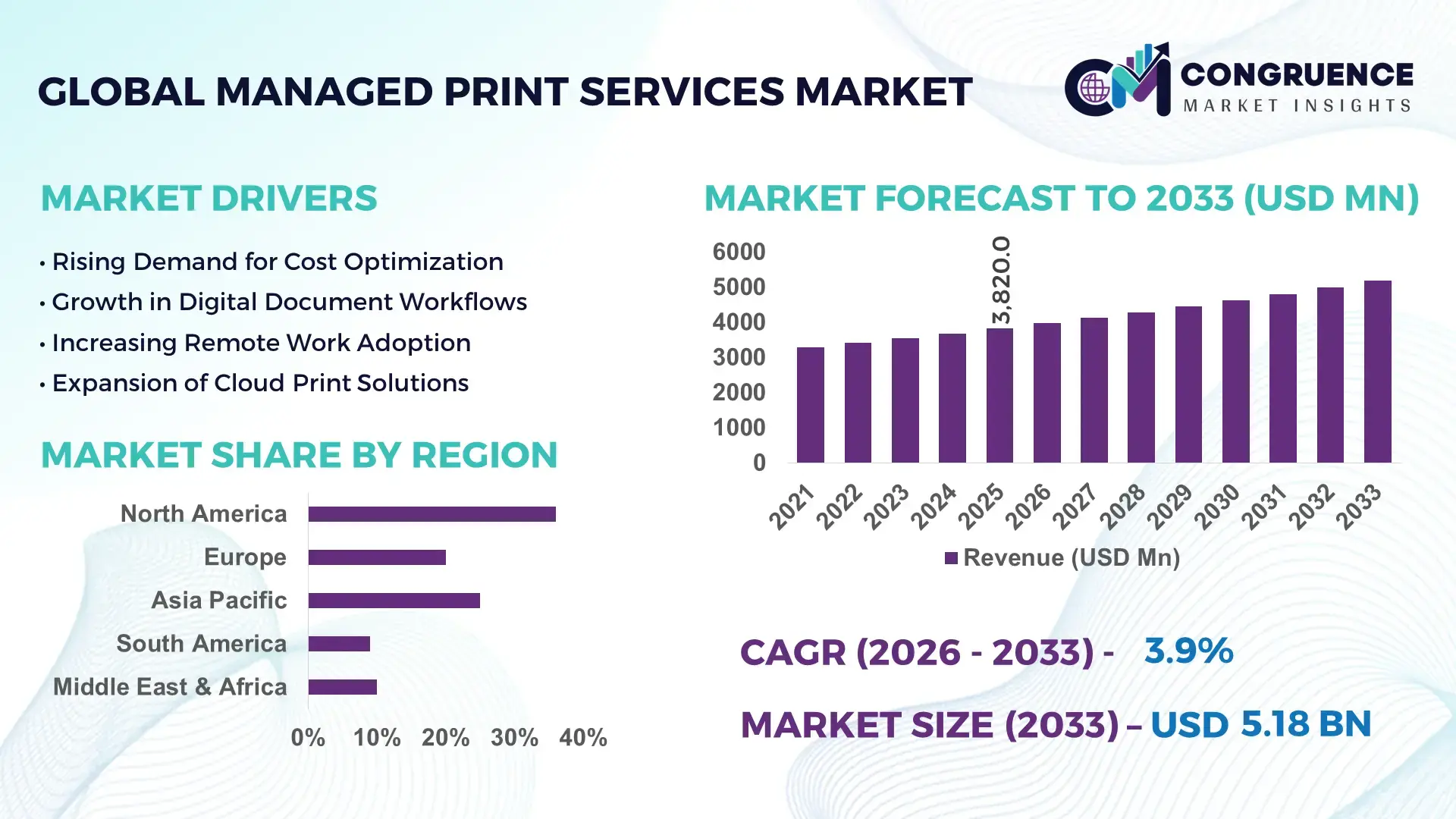

The Global Managed Print Services Market was valued at USD 3820 Million in 2025 and is anticipated to reach a value of USD 5179.87 Million by 2033 expanding at a CAGR of 3.88% between 2026 and 2033. Enterprise-wide migration toward AI-enabled print analytics and cloud-based document workflow optimization reduced unmanaged printing costs by nearly 28% across large corporate environments in 2026, accelerating long-term managed print service contracts in banking, healthcare, manufacturing, and government sectors.

The United States dominated the global managed print services market with nearly 34% share in 2026, supported by large-scale hybrid workplace infrastructure, federal cybersecurity modernization programs, and over USD 2.4 billion in enterprise print fleet transformation investments. Healthcare and financial institutions accounted for more than 41% of enterprise managed print deployments due to strict compliance-led document tracking requirements and secure print authentication mandates. Compared with traditional print environments, AI-driven fleet monitoring platforms improved device uptime by 32% while lowering toner waste by 21%. Rising trade restrictions on semiconductor and imaging component imports following U.S.-China technology tensions also accelerated localized print hardware sourcing and regional service partnerships across North America.

Organizations integrating advanced managed print services into digital workplace strategies achieved document workflow processing speeds nearly 26% faster than legacy decentralized print ecosystems, strengthening vendor positioning in high-volume enterprise contracts and multi-site operational environments.

Market Size & Growth: USD 3820 Million in 2025 reaching USD 5179.87 Million by 2033, driven by AI-based print automation and hybrid workplace document security demand.

Top Growth Drivers: Cloud print adoption increased 31%, workflow automation deployment rose 27%, and secure print management integration expanded 24% in enterprise environments.

Short-Term Forecast: By 2028, enterprises are projected to reduce print infrastructure operating costs by 22% through centralized fleet optimization and predictive maintenance systems.

Emerging Technologies: AI analytics, IoT-enabled printers, and zero-trust print security platforms improved fleet efficiency by nearly 30% across advanced enterprise deployments.

Regional Leaders: North America exceeded USD 1.5 Billion with cybersecurity-led adoption, Europe crossed USD 1.1 Billion through ESG compliance programs, and Asia-Pacific advanced rapidly with 29% cloud print expansion.

Consumer/End-User Trends: Nearly 58% of large enterprises shifted toward subscription-based print management contracts supporting hybrid workforce operations and remote device monitoring.

Pilot/Case Example: In 2026, a multinational banking deployment reduced paper waste by 35% and improved print asset utilization by 26% after AI-based workflow integration.

Competitive Landscape: Top five providers controlled nearly 49% market share, with HP, Xerox, Canon, Ricoh, and Konica Minolta competing through automation and analytics capabilities.

Regulatory & ESG Impact: ESG-driven print reduction policies lowered enterprise paper consumption by 18% while secure compliance frameworks accelerated government-sector adoption.

Investment & Funding: More than USD 1.3 Billion was allocated toward cloud print infrastructure, regional service expansion, and intelligent workflow platforms amid supply chain restructuring.

Innovation & Future Outlook: AI-powered predictive servicing, decentralized print orchestration, and edge-connected document ecosystems are reshaping advanced global managed print operations.

Banking, healthcare, and manufacturing collectively contributed more than 61% of global managed print services adoption due to high-volume document processing, compliance-intensive workflows, and secure print authentication requirements. AI-enabled print analytics, predictive servicing platforms, and cloud-connected fleet orchestration emerged as key technology innovations improving asset utilization and reducing downtime across enterprise environments. North America maintained strong demand leadership, while Asia-Pacific experienced accelerated deployment growth through digital workplace modernization initiatives. Enterprises increasingly prioritized low-waste print ecosystems and automated workflow governance following stricter sustainability regulations and regional supply chain realignments. Intelligent document lifecycle management and subscription-based print ecosystems are expected to define the next phase of strategic enterprise transformation discussions.

Managed print services are becoming strategically critical as enterprises shift from fragmented print infrastructure toward centralized digital workflow ecosystems integrated with cybersecurity, cloud governance, and AI-based device analytics. Large organizations reduced document handling inefficiencies by nearly 24% in 2026 after integrating managed print systems with enterprise resource planning and identity-access platforms. The market is also benefiting from infrastructure modernization initiatives and supply-chain restructuring across North America and East Asia, where enterprises are prioritizing localized servicing models and secure device lifecycle management to reduce operational disruptions.

AI-enabled print fleet monitoring platforms now deliver nearly 31% faster issue resolution compared with legacy reactive maintenance systems while lowering consumable waste by 19%. Japan and Germany continue leading in automated workflow deployment within manufacturing and industrial sectors, whereas India and Brazil are expanding adoption through cost-focused cloud print contracts for banking and public administration networks. In 2026, a multinational healthcare provider consolidated over 12,000 print assets into a unified managed ecosystem, reducing downtime by 27% and improving regulatory document traceability.

Over the next two to three years, enterprises are expected to prioritize predictive servicing, zero-trust print architecture, and subscription-based fleet management partnerships to strengthen operational resilience and compliance efficiency. Vendors investing in AI integration, localized service networks, and advanced workflow automation are securing stronger competitive positioning in enterprise digital transformation programs.

Rapid enterprise migration toward automated document ecosystems remains the primary driver accelerating managed print services deployment across banking, healthcare, logistics, and government sectors. In 2026, enterprises implementing AI-enabled print orchestration reduced unmanaged print volumes by 29% while improving workflow processing speed by 23%. U.S.-based financial institutions increasingly integrated zero-trust print authentication following stricter cybersecurity mandates, accelerating demand for centralized print governance platforms. Hybrid workplace expansion also pushed cloud-connected print deployments above 46% across large corporate environments. Service providers responded through regional expansion, predictive maintenance partnerships, and AI-powered analytics integration to secure long-term enterprise contracts. A key operational shift emerged as companies increasingly bundled managed print services with broader workplace digitization and compliance management solutions, improving recurring service retention and reducing infrastructure fragmentation.

Persistent dependency on imported imaging components, semiconductors, and proprietary print hardware continues limiting operational flexibility across the managed print services ecosystem. In 2026, average enterprise device replacement costs increased by 18% due to supply-chain instability and logistics disruptions affecting East Asian component manufacturing hubs. Nearly 37% of mid-sized enterprises also reported interoperability limitations between legacy printers and cloud-native workflow platforms, delaying modernization programs. Germany and the United Kingdom experienced extended procurement timelines following stricter electronic waste and energy-efficiency compliance requirements for enterprise printing equipment. Service providers are mitigating these pressures through localized inventory sourcing, multi-vendor hardware strategies, and long-term consumables contracts. A critical business impact remains margin compression for providers managing fixed-cost enterprise agreements during periods of volatile hardware procurement costs.

Advanced AI-driven print intelligence platforms are creating new monetization opportunities beyond traditional device management contracts. Enterprises deploying predictive analytics and automated consumable tracking achieved nearly 26% lower maintenance intervention rates and 21% higher device utilization efficiency during 2026. India and Southeast Asian business hubs are witnessing accelerated demand for subscription-based cloud print ecosystems supporting distributed workforces and multi-location operations. Emerging integration between managed print systems and robotic process automation platforms is enabling automated document classification, compliance tracking, and workflow routing. Providers are expanding R&D investments into edge-connected print analytics, remote diagnostics, and sustainability-focused optimization software to strengthen service differentiation. A non-obvious strategic advantage is emerging in regulated industries where AI-enhanced document governance reduces audit preparation workloads and improves enterprise compliance visibility.

Rising cybersecurity exposure linked to connected print infrastructure represents a major long-term execution challenge for managed print service providers. In 2026, nearly 43% of enterprise IT leaders identified network-connected printers as vulnerable endpoints within hybrid workplace environments, while unauthorized print access incidents increased by 17% across large distributed enterprises. U.S. healthcare and government institutions face mounting pressure to secure sensitive document workflows under stricter digital compliance frameworks. Simultaneously, managing multi-vendor print ecosystems across cloud, on-premise, and edge environments is increasing deployment complexity and technical support costs. Companies are responding through zero-trust architecture investment, encrypted print authentication, and cybersecurity partnerships with enterprise software vendors. Long-term competitiveness will depend on providers building scalable security frameworks capable of supporting increasingly decentralized and AI-integrated workplace ecosystems.

AI-Based Fleet Optimization Expansion Enterprises increased deployment of AI-enabled print analytics platforms by 33% during 2026 to reduce device downtime and automate consumable management across distributed workplaces. Large banking and insurance networks in the United States integrated predictive maintenance tools that lowered emergency service interventions by 24% and improved print asset utilization by 19%. Vendors responded through analytics partnerships and remote diagnostics integration to strengthen recurring enterprise contracts.

Cloud Print Migration Acceleration Hybrid workplace restructuring pushed cloud print service adoption above 48% across multinational enterprises, particularly within India’s IT services and public-sector operations. Organizations replacing legacy server-based print infrastructure reduced print administration workloads by 27% while improving remote accessibility and workflow continuity. Companies increasingly shifted toward subscription-based deployment models and localized cloud hosting partnerships following rising concerns around cross-border data governance and infrastructure resilience.

Security-Centric Print Architecture Adoption Zero-trust print security implementation expanded by 29% in healthcare and government environments after stricter enterprise cybersecurity regulations increased scrutiny around unsecured network-connected printers. Japanese manufacturers and German healthcare providers accelerated encrypted authentication deployment to reduce unauthorized print access incidents by nearly 21%. Managed print vendors expanded cybersecurity alliances and embedded compliance-monitoring capabilities directly into enterprise workflow platforms to strengthen operational trust.

Sustainability-Led Workflow Restructuring Enterprises reduced office paper consumption by approximately 18% through automated digital document routing, print quota enforcement, and intelligent duplex printing systems. European corporate campuses increasingly linked managed print contracts with ESG reporting targets and energy-efficiency mandates, while manufacturing companies adopted low-energy multifunction devices that lowered operational power consumption by 16%. Providers responded through carbon-monitoring dashboards, circular consumables programs, and device refurbishment initiatives supporting long-term enterprise sustainability strategies.

Print Management remained the leading segment in 2026, accounting for nearly 32% of managed print services deployments due to its strong integration with enterprise workflow governance, centralized device orchestration, and operational cost visibility. Large enterprises prioritized print management platforms to reduce unmanaged output volumes and improve fleet efficiency across multi-site operations. Cloud Print Services emerged as the fastest-growing segment, with adoption increasing by 28% as hybrid work environments accelerated demand for location-independent printing and remote infrastructure control. Compared with traditional on-premise systems, cloud-based print orchestration reduced administrative workload by 26% and improved deployment scalability across distributed enterprises. Device Management maintained strong relevance within manufacturing and logistics sectors requiring predictive servicing and uptime optimization, while Security Management Services gained traction in healthcare and government environments following stricter cybersecurity mandates. Companies are expanding investments into AI-enabled print analytics, encrypted print authentication, and subscription-based cloud deployment models to strengthen recurring enterprise service contracts and long-term infrastructure flexibility.

Office Printing remained the dominant application segment due to sustained enterprise dependency on centralized document processing across banking, legal, healthcare, and public administration environments. In 2026, nearly 44% of managed print contracts were still linked directly to high-volume office printing infrastructure requiring secure device governance and consumable optimization. Workflow Automation emerged as the fastest-growing application as enterprises accelerated digital transformation initiatives and integrated AI-driven document routing systems that improved processing efficiency by 31%. Companies deploying automated print workflows reduced manual document handling errors by approximately 22% while improving operational turnaround speed. Document Security and Fleet Monitoring also gained strategic relevance as organizations strengthened cybersecurity frameworks and predictive servicing capabilities across decentralized workplaces. Remote Printing adoption expanded rapidly within multinational IT and consulting firms managing distributed workforces. Providers are increasingly integrating workflow orchestration, analytics dashboards, and cloud-based monitoring platforms into unified enterprise service offerings to strengthen operational continuity and long-term client retention.

BFSI remained the leading end-user segment in 2026 due to high-volume transactional printing, regulatory document retention requirements, and strict data security protocols across banking and insurance institutions. Financial organizations accounted for nearly 29% of enterprise managed print deployments, particularly within the United States, Japan, and the United Kingdom where secure document governance remains operationally critical. Healthcare emerged as the fastest-growing end-user segment as hospitals and diagnostic networks expanded digital patient record integration and encrypted print authentication systems, increasing managed print adoption by nearly 25%. Government agencies continued prioritizing centralized print governance for compliance and cost management, while manufacturing companies adopted predictive device monitoring to reduce operational downtime across production facilities. Education and retail sectors increasingly shifted toward subscription-based cloud print ecosystems supporting decentralized campuses and multi-store operations. Service providers are responding through sector-specific workflow customization, cybersecurity partnerships, and scalable cloud infrastructure packages tailored to compliance-intensive enterprise environments.

North America accounted for the largest market share at 36% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 5.41% between 2026 and 2033.

North America maintained the leading position in the managed print services market due to strong enterprise digital infrastructure, high cloud integration maturity, and accelerated workflow automation adoption across banking, healthcare, and government sectors. The region represented nearly 36% of global deployment activity in 2025, while cloud-connected print management implementation increased by approximately 31% across multi-site enterprises. Organizations integrating AI-enabled print analytics reduced infrastructure management costs by 24% and improved fleet utilization efficiency by 19%. Enterprises across the United States and Canada increasingly consolidated fragmented print environments into centralized workflow ecosystems supporting cybersecurity compliance and remote workforce operations. Major providers expanded strategic partnerships with enterprise software vendors and cybersecurity firms to strengthen long-term contract retention and operational scalability.

United States Market Outlook: The United States dominates the regional market through strong enterprise IT infrastructure, large-scale hybrid workplace deployment, and extensive adoption of AI-driven workflow automation platforms. In 2026, more than 48% of Fortune 500 enterprises integrated centralized print governance systems supporting predictive maintenance, encrypted authentication, and remote print orchestration. Federal cybersecurity modernization initiatives and rising enterprise compliance requirements continue accelerating long-term managed print service expansion across financial institutions, healthcare networks, and government agencies.

Europe continues strengthening managed print service adoption through enterprise sustainability mandates, digital workflow modernization, and strict regulatory compliance requirements. The region accounted for nearly 28% of global deployment concentration in 2025, supported by strong adoption across Germany, the United Kingdom, and France. Enterprises implementing centralized print governance systems reduced paper consumption by approximately 18% while improving compliance tracking efficiency across distributed office environments. Low-energy multifunction devices and automated document workflows gained traction as organizations aligned infrastructure modernization with ESG performance objectives. Service providers increasingly focused on circular equipment refurbishment, lifecycle optimization programs, and secure cloud print integration to improve enterprise operational efficiency and reduce environmental impact across corporate and public-sector environments.

Germany Market Outlook: Germany remains strategically significant due to its industrial manufacturing strength, advanced enterprise automation ecosystem, and strict operational sustainability standards. In 2026, nearly 42% of large enterprises implemented encrypted workflow management and energy-efficient print infrastructure to strengthen regulatory compliance and reduce operational waste. Manufacturing, automotive, and engineering sectors continue driving demand for predictive print servicing and centralized document governance integrated with broader industrial digital transformation initiatives.

Asia-Pacific is emerging as the fastest-growing managed print services market due to accelerated enterprise digitization, rising cloud infrastructure investment, and expanding hybrid workplace adoption across large business hubs. The region accounted for approximately 24% of global deployment activity in 2025, while cloud print adoption increased by nearly 34% across enterprise environments. Manufacturing, IT services, and public administration sectors increasingly adopted centralized workflow automation platforms to improve operational efficiency and remote print accessibility. Organizations replacing decentralized print environments achieved approximately 26% faster workflow processing and improved device utilization efficiency. Global vendors expanded localized servicing operations, subscription-based deployment models, and AI-enabled analytics integration to strengthen enterprise scalability and long-term customer retention across rapidly digitizing markets.

China Market Outlook: China remains a critical market due to large-scale enterprise digitization programs, extensive manufacturing infrastructure, and expanding cloud ecosystem development. In 2026, enterprise organizations operating across industrial clusters improved print fleet efficiency by nearly 27% through centralized workflow orchestration and predictive servicing integration. Domestic providers are strengthening localized print analytics capabilities and workflow automation platforms to reduce software dependency risks and improve operational flexibility for large enterprise deployments.

South America is witnessing steady managed print services expansion through enterprise infrastructure modernization and rising cloud-based workflow deployment across banking, education, and government operations. Brazil and Chile accounted for the majority of regional deployment activity in 2025 as organizations increasingly prioritized centralized print governance and subscription-based infrastructure models. Enterprises implementing managed print optimization reduced consumable waste by approximately 16% while improving multi-location fleet visibility and operational consistency. Infrastructure limitations and dependency on imported print hardware continue creating deployment challenges across certain markets, particularly during periods of supply-chain volatility. Service providers are responding through regional partnerships, localized technical support expansion, and scalable remote print management solutions tailored for cost-sensitive enterprise environments.

Brazil Market Outlook: Brazil leads the regional market due to strong banking infrastructure, expanding enterprise cloud adoption, and increasing demand for centralized workflow governance. In 2026, enterprise cloud print deployment activity increased by approximately 22% as organizations modernized legacy print environments and strengthened remote workforce support capabilities. Financial institutions and public administration networks continue driving demand for secure document management platforms integrated with predictive maintenance and compliance-focused print governance systems.

Middle East & Africa is experiencing rising managed print services adoption through government-led digitization programs, enterprise modernization strategies, and expanding cloud connectivity infrastructure. Gulf countries represented the largest regional deployment concentration in 2025, supported by smart workplace transformation initiatives across healthcare, banking, and public administration sectors. Enterprises implementing automated document workflow systems improved operational processing efficiency by approximately 21% while reducing dependency on manual print administration. Service providers expanded cybersecurity integration partnerships and cloud-hosted print governance platforms to strengthen deployment scalability and compliance management capabilities. Increasing investment in smart office infrastructure and digital government transformation continues supporting long-term enterprise managed print ecosystem development across the region.

United Arab Emirates Market Outlook: The United Arab Emirates remains strategically important due to advanced enterprise connectivity infrastructure, strong digital government initiatives, and rapid smart workplace adoption across Dubai and Abu Dhabi. In 2026, nearly 39% of large corporate offices integrated cloud-connected print governance systems with enterprise cybersecurity frameworks to improve operational security and workflow visibility. Organizations across banking, healthcare, and logistics sectors continue prioritizing AI-enabled document automation and subscription-based managed print ecosystems to strengthen long-term operational efficiency.

HP, Xerox, Canon, Ricoh, and Konica Minolta collectively controlled nearly 49% of the managed print services market in 2026, competing through enterprise workflow automation, AI-enabled analytics, cybersecurity integration, and global service infrastructure. HP and Xerox are aggressively targeting multinational enterprise contracts through cloud-based print orchestration and predictive servicing platforms, while Canon and Ricoh compete strongly within compliance-intensive healthcare, government, and financial sectors through secure document governance capabilities. Regional providers across India and Latin America are competing primarily through pricing flexibility, localized servicing, and rapid deployment execution. AI-driven fleet optimization reduced servicing costs by approximately 22%, while automated consumable management improved operational efficiency by nearly 19%, intensifying technology-led competition. Companies are expanding through cybersecurity partnerships, workflow software integration, and subscription-based enterprise contracts. Strong cloud infrastructure, secure workflow ecosystems, and scalable enterprise integration capabilities remain critical competitive differentiators.

HP Inc.

Xerox Holdings Corporation

Canon Inc.

Ricoh Company Ltd.

Konica Minolta Inc.

Lexmark International Inc.

Kyocera Document Solutions Inc.

Sharp Corporation

Toshiba Tec Corporation

Seiko Epson Corporation

Brother Industries Ltd.

ARC Document Solutions Inc.

Pitney Bowes Inc.

FUJIFILM Business Innovation Corporation

AI-enabled print analytics, predictive maintenance platforms, and cloud-native fleet orchestration systems are becoming core technologies transforming managed print environments across enterprise sectors. In 2026, nearly 48% of large organizations integrated centralized print analytics platforms to improve device monitoring, automate consumable replenishment, and reduce unplanned downtime. AI-driven servicing workflows lowered infrastructure management intervention by approximately 24% while improving fleet utilization efficiency by 19%. Compared with traditional reactive maintenance systems, predictive print intelligence platforms resolved operational issues nearly 31% faster and reduced consumable waste by 21%, strengthening enterprise workflow continuity and lowering long-term servicing costs.

Emerging technologies between 2026 and 2028 include zero-trust print architecture, edge-connected print management, and AI-assisted document workflow automation integrated with enterprise cloud ecosystems. Organizations deploying encrypted pull-print authentication and cloud governance frameworks reduced unauthorized print exposure by approximately 18%. Hybrid workplace expansion accelerated cloud print deployment above 52% across multinational enterprises, particularly within banking, healthcare, and government environments managing distributed operations and compliance-sensitive workflows.

Disruptive innovation is increasingly centered on generative AI integration, autonomous workflow orchestration, and quantum-resistant print security infrastructure. Global vendors are competing aggressively through AI-powered workflow ecosystems, remote diagnostics, and cybersecurity partnerships benefiting enterprises with complex multi-site operations. Organizations delaying infrastructure modernization risk higher support costs, slower workflow processing, and weaker enterprise security resilience as intelligent document ecosystems become operationally standard by 2028.

May 2025 – Xerox secured leadership positioning in Quocirca’s Cloud Print Services Landscape for the fourth consecutive year, strengthening AI-enabled cloud print deployment capabilities supporting distributed enterprises across global operations.

November 2025 – Xerox completed strategic Lexmark integration, expanding combined managed print operations across more than 170 countries and strengthening AI, analytics, workflow automation, and IoT-enabled enterprise servicing capabilities.

January 2026 – HP launched Microsoft 365 Copilot integration directly into enterprise multifunction print devices, enabling AI-assisted workflow automation while supporting organizations already saving 10–15 employee productivity hours monthly.

March 2026 – HP expanded AI-powered Workforce Experience Platform capabilities, helping enterprises reduce device downtime by 30% and save nearly 50 operational hours per employee annually through automated remediation tools.

The managed print services market report delivers detailed analysis across core segments including Print Management, Device Management, Document Management, Cloud Print Services, and Security Management Services. The study evaluates operational deployment trends across applications such as workflow automation, office printing, document security, remote printing, cost management, and fleet monitoring. Coverage extends across BFSI, healthcare, manufacturing, government, education, and retail sectors, with enterprise cloud print adoption exceeding 50% across large distributed workplaces by 2026. The report also analyzes deployment concentration, workflow modernization patterns, and enterprise transition toward AI-enabled print governance systems.

Regional assessment covers North America, Europe, Asia-Pacific, South America, and Middle East & Africa with strategic evaluation of infrastructure modernization, cybersecurity integration, hybrid workplace expansion, and cloud-based workflow transformation between 2026 and 2033. The report further examines competitive positioning, technology partnerships, predictive servicing deployment, ESG-focused print optimization, and emerging intelligent document ecosystem strategies supporting investment planning, enterprise expansion, operational benchmarking, and long-term market positioning decisions.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 3820 Million |

|

Market Revenue in 2033 |

USD 5179.87 Million |

|

CAGR (2026 - 2033) |

3.88% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

HP Inc., Xerox Holdings Corporation, Canon Inc., Ricoh Company Ltd., Konica Minolta Inc., Lexmark International Inc., Kyocera Document Solutions Inc., Sharp Corporation, Toshiba Tec Corporation, Seiko Epson Corporation, Brother Industries Ltd., ARC Document Solutions Inc., Pitney Bowes Inc., FUJIFILM Business Innovation Corporation |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |