Reports

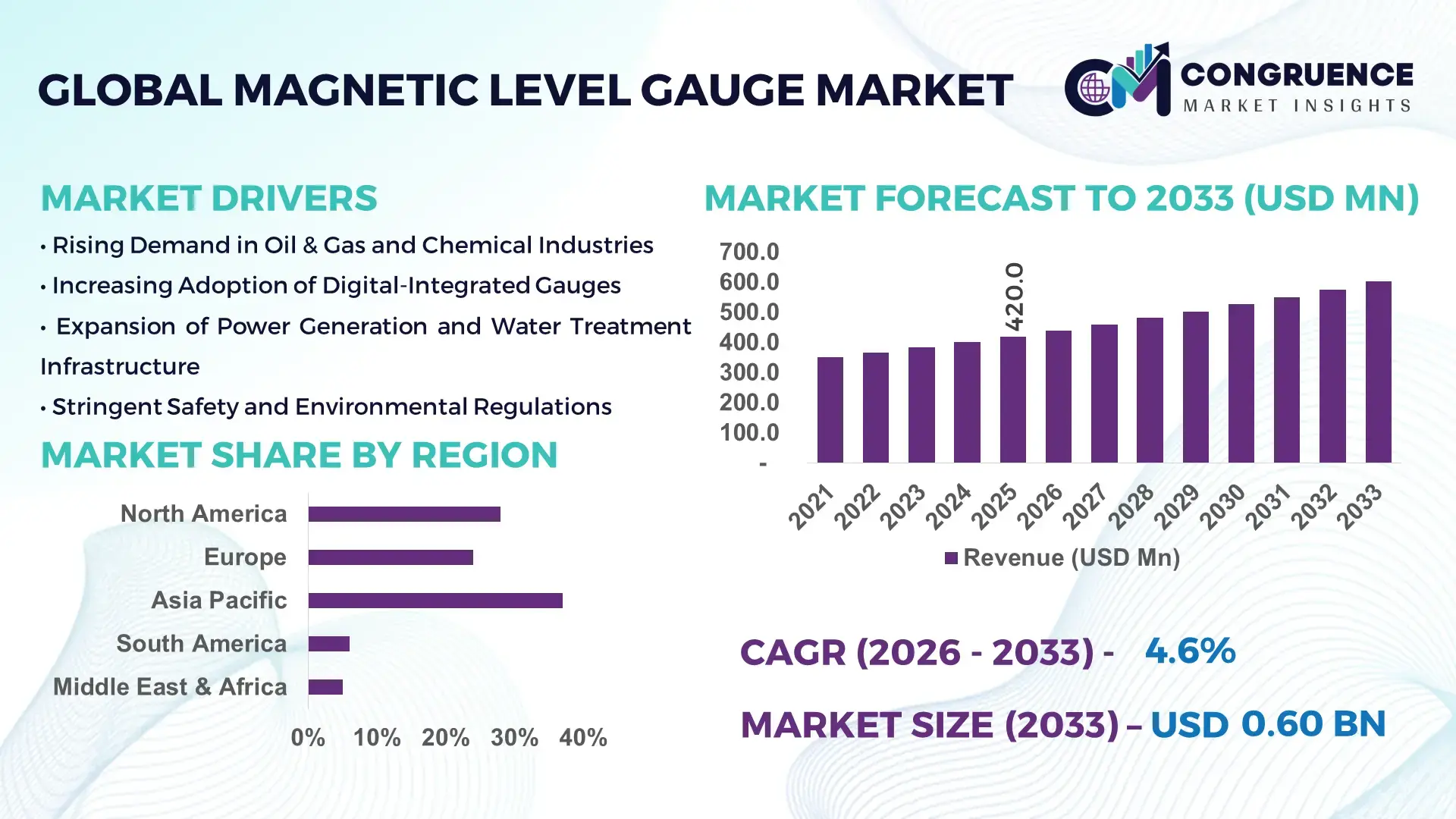

The Global Magnetic Level Gauge Market was valued at USD 420 Million in 2025 and is anticipated to reach a value of USD 601.9 Million by 2033 expanding at a CAGR of 4.6% between 2026 and 2033, according to an analysis by Congruence Market Insights. This growth is primarily supported by rising deployment of high-reliability level measurement systems in oil & gas, chemicals, and power generation where safety and accuracy are critical.

China represents the dominant production and deployment hub in the global Magnetic Level Gauge Market, supported by its large-scale process industries and advanced instrumentation manufacturing base. In 2025, China accounted for more than 38% of global magnetic level gauge manufacturing capacity, with over 120 dedicated instrumentation plants producing magnetic float and chamber-based gauges. Annual capital investment in process instrumentation exceeded USD 3.2 billion, with chemical processing, petrochemicals, and LNG terminals representing nearly 46% of total installations. Adoption of digital magnetic gauges with reed switch transmitters crossed 52% in new projects, driven by industrial automation upgrades and smart factory programs.

Market Size & Growth: Valued at USD 420 Million in 2025, projected to reach USD 601.9 Million by 2033 at a CAGR of 4.6%, driven by expanding safety-critical process automation.

Top Growth Drivers: Process automation adoption 61%, safety compliance implementation 54%, digital instrumentation integration 47%.

Short-Term Forecast: By 2028, plant-level downtime is expected to decline by 18% through predictive level monitoring deployment.

Emerging Technologies: Smart magnetic transmitters, IIoT-enabled level sensors, wireless HART integration.

Regional Leaders: Asia Pacific USD 245 Million by 2033 with refinery upgrades, North America USD 168 Million with digital retrofits, Europe USD 142 Million with hydrogen projects.

Consumer/End-User Trends: Oil & gas accounts for 34% of installations, chemicals 27%, power generation 18%, with rising adoption in water treatment.

Pilot or Case Example: In 2024, a South Korean refinery reduced unplanned shutdowns by 22% using smart magnetic gauges.

Competitive Landscape: Market leader holds ~19% share, followed by KROHNE, WIKA, ABB, Emerson, and Magnetrol.

Regulatory & ESG Impact: Safety Instrumented System mandates driving 31% higher adoption in hazardous applications.

Investment & Funding Patterns: Over USD 1.1 Billion invested globally in process instrumentation modernization since 2022.

Innovation & Future Outlook: Integration with digital twins and AI diagnostics shaping next-generation gauge platforms.

Process industries represent nearly 62% of total demand, with oil & gas, chemicals, and power generation leading consumption. Recent innovations include corrosion-resistant alloy chambers, SIL-certified transmitters, and remote diagnostics platforms. Regulatory pressure for hazardous area safety, stricter emissions monitoring, and regional infrastructure expansion are reshaping regional consumption, while smart instrumentation adoption is accelerating across Asia Pacific and the Middle East.

The Magnetic Level Gauge Market holds strategic relevance as a core safety and control component within critical process industries where real-time level visibility directly influences operational continuity and risk mitigation. Compared with traditional glass level indicators, smart magnetic gauges with digital transmitters deliver 28% improvement in measurement stability and 34% reduction in maintenance intervention frequency. Asia Pacific dominates in volume, while Europe leads in adoption with 58% of large process plants integrating digital magnetic gauges into distributed control systems.

By 2028, IIoT-enabled diagnostics is expected to cut unplanned shutdown events by 21% through early fault detection and remote calibration. Firms are committing to ESG improvements such as 30% reduction in fugitive emissions monitoring gaps by 2030 through continuous level monitoring integration. In 2024, a German chemical producer achieved 26% reduction in safety incidents through deployment of SIL-3 certified magnetic gauges linked to automated shutdown systems. Looking ahead, the Magnetic Level Gauge Market is positioned as a pillar of resilience, compliance, and sustainable growth supporting next-generation industrial automation.

The Magnetic Level Gauge Market is shaped by rising safety regulations, digitalization of process plants, and expansion of hazardous fluid handling industries. Increasing deployment in LNG terminals, refineries, and specialty chemical units is driving demand for high-integrity level measurement. Integration with control systems, wireless monitoring, and predictive maintenance platforms is transforming traditional mechanical gauges into smart instruments. Replacement of legacy sight glass systems and adoption in water infrastructure projects further influence market momentum across developed and emerging economies.

Automation in hazardous environments is accelerating deployment of magnetic level gauges due to their sealed construction and fail-safe indication. In 2025, over 64% of new refinery projects specified magnetic gauges for pressurized vessels. Safety compliance programs increased certified instrument installations by 41%, while integration with shutdown systems improved response time by 23%. Growing adoption in LNG, hydrogen, and ammonia storage further reinforces this driver.

Stringent SIL certification, periodic recalibration mandates, and specialized installation requirements increase ownership complexity. In regulated industries, compliance-related costs add nearly 18% to total lifecycle expenses. Limited availability of certified technicians in emerging regions slows deployment, while retrofit compatibility challenges affect older plants, restraining faster penetration.

Integration with IIoT platforms enables remote diagnostics, predictive alerts, and digital twins. Plants deploying smart magnetic gauges achieved 27% reduction in inspection labor and 19% improvement in uptime. Growing investments in hydrogen, carbon capture, and water infrastructure create new application opportunities across high-growth regions.

Special alloys, rare magnets, and certified electronics experienced 22% cost volatility since 2023. Lead times extended by 35% in global projects, affecting delivery schedules. Compliance documentation, testing backlogs, and geopolitical trade restrictions further complicate supply reliability and project planning.

Digital Transmitter Integration: In 2025, over 49% of new gauges shipped with integrated transmitters, improving signal accuracy by 32% and reducing manual inspections by 41%.

Expansion in LNG and Hydrogen Storage: Installations in cryogenic tanks increased 38%, with safety-related deployments rising 29% across Asia and the Middle East.

Wireless Monitoring Adoption: Wireless-enabled gauges grew 44%, cutting wiring costs by 36% and reducing commissioning time by 27%.

Corrosion-Resistant Material Innovation: Use of duplex steel and PTFE-lined chambers expanded 31%, extending service life by 45% in aggressive chemical environments.

The Magnetic Level Gauge Market is segmented comprehensively by type, application, and end-user to address diverse industrial requirements. By type, the market encompasses float chamber gauges, magnetic float gauges, and differential pressure-based magnetic indicators, each engineered to meet specific operational conditions. In terms of application, magnetic level gauges are extensively deployed in oil & gas, chemical processing, water treatment, and power generation, where precise fluid level monitoring is critical for operational safety and efficiency. End-user segmentation spans refineries, petrochemical plants, LNG terminals, and industrial water facilities, reflecting adoption patterns driven by regulatory mandates, automation upgrades, and digital monitoring needs. Increasing integration with IIoT platforms and safety compliance initiatives further influences selection across segments. The segmentation framework enables decision-makers to evaluate suitability, performance, and ROI across varied operational contexts, optimizing both capital deployment and operational efficiency in industrial facilities worldwide.

Float chamber magnetic level gauges currently account for 41% of adoption, serving as the leading type due to their robustness in high-pressure and high-temperature environments, particularly in oil & gas and chemical sectors. Magnetic float gauges follow with a 29% share, valued for reliability and compact installation in medium-scale process tanks. Differential pressure-based magnetic indicators represent 17%, offering niche advantages in continuous process monitoring, while other specialized variants, including hybrid and digital-integrated models, collectively hold 13% of the market.

The fastest-growing type is digital-integrated magnetic float gauges, driven by increasing demand for remote monitoring, IIoT connectivity, and predictive maintenance features. This segment has witnessed accelerated adoption, supported by modernization programs in refineries and power plants.

Oil & gas applications dominate the Magnetic Level Gauge Market, accounting for 38% of usage, primarily due to stringent safety protocols and high-volume fluid handling requirements. Chemical processing represents 27%, leveraging high-accuracy level monitoring for reaction vessels and storage tanks. Water and wastewater treatment applications account for 18%, while power generation and other industrial processes contribute 17% collectively.

The fastest-growing application is LNG and hydrogen storage, driven by clean energy expansion, safety automation, and retrofitting of cryogenic storage facilities, with adoption rising sharply in the Middle East and Asia Pacific.

Consumer adoption trends indicate that in 2025, over 42% of refineries globally reported upgrading to smart magnetic level gauges for critical storage tanks. Additionally, 55% of water utilities in North America have integrated remote monitoring-enabled gauges to improve operational efficiency.

Refineries lead as the primary end-user segment, representing 36% of total installations, with adoption concentrated in oil & gas and petrochemical hubs. Petrochemical plants follow with 25%, leveraging magnetic gauges for hazardous and corrosive fluid containment. Water treatment and power generation facilities account for 22%, while other industrial users contribute 17%.

The fastest-growing end-user segment is hydrogen production facilities, driven by expanding clean energy projects and stricter safety regulations, which necessitate high-integrity monitoring systems.

Industry adoption trends show that in 2025, over 40% of LNG terminals globally upgraded to IIoT-compatible magnetic level gauges for remote safety monitoring. Additionally, more than 35% of chemical plants in Europe implemented smart gauges integrated with predictive maintenance dashboards to reduce unplanned downtime.

Asia Pacific accounted for the largest market share at 37% in 2025; however, Asia Pacific is expected to register the fastest growth, expanding at a CAGR of 5.2% between 2026 and 2033.

The market in this region is driven by high-volume industrial expansion, particularly in China, India, and Japan, where over 1,250 large-scale refineries, chemical plants, and power generation facilities operate. In 2025, Asia Pacific installed more than 520,000 units of magnetic level gauges, representing nearly 42% of the total global installations. Increasing adoption of IIoT-enabled monitoring, digital twins, and predictive maintenance solutions has elevated the operational efficiency by 21% across key industrial zones. Investments in LNG terminals exceeded USD 2.8 billion in 2025, while chemical process automation projects in India and China accounted for 34% of new gauge installations. Furthermore, government-supported industrial automation initiatives and safety compliance programs are driving the installation of high-precision magnetic gauges across both large-scale and mid-sized facilities.

North America holds approximately 28% of the global Magnetic Level Gauge Market by volume. The region’s growth is supported by high adoption in oil & gas, petrochemicals, power generation, and water treatment sectors. Regulatory frameworks such as OSHA and EPA guidelines have mandated improved safety instrumentation in hazardous process applications, stimulating replacement of conventional sight glass systems. Advanced digital gauges with wireless HART integration, remote diagnostics, and predictive maintenance are being increasingly deployed. Emerson Electric, a key regional player, recently introduced an AI-assisted magnetic level gauge for LNG facilities, reducing maintenance interventions by 22%. Consumer behavior reflects higher enterprise adoption in industries like healthcare and finance, emphasizing accuracy, real-time monitoring, and compliance verification.

Europe accounts for roughly 24% of the global Magnetic Level Gauge Market. Leading markets include Germany, the UK, and France, where stringent EU safety directives and sustainability initiatives drive instrumentation upgrades. European industries are increasingly adopting SIL-certified and smart magnetic gauges integrated with industrial automation and digital twin platforms. WIKA and Endress+Hauser have expanded their operations to include predictive maintenance-enabled magnetic gauges for chemical and water treatment facilities. Regional consumer behavior indicates that regulatory pressure leads to demand for explainable, traceable instrumentation, with nearly 46% of chemical plants in Germany retrofitting traditional gauges with smart digital solutions.

Asia-Pacific represents 37% of total global magnetic level gauge installations, making it the largest regional market by volume. Top consuming countries include China, India, and Japan, which collectively operate over 1,250 refineries, chemical processing, and power generation facilities. Growth is supported by large-scale infrastructure projects and industrial automation initiatives, including IIoT-enabled process control and digital twin integrations. Yokogawa Electric and Shanghai Instrument have rolled out advanced magnetic level gauges with remote diagnostics in China, enhancing uptime and safety in petrochemical plants. Consumer adoption reflects a preference for high-reliability, smart gauges with remote monitoring capabilities, particularly in fast-growing chemical, LNG, and water treatment sectors.

South America holds about 6% of the global Magnetic Level Gauge Market, with Brazil and Argentina representing key contributors. The region’s growth is driven by energy, oil & gas, and industrial water treatment projects, supported by government incentives for industrial modernization. Petrobras, a major player in Brazil, deployed magnetic level gauges with digital transmitters in 2025 across 12 LNG storage and refinery sites, reducing inspection downtime by 18%. Regional consumer behavior emphasizes cost-efficient, robust solutions for hazardous fluid monitoring, with higher adoption in industrial plants upgrading older measurement systems.

The Middle East & Africa region accounts for 5% of the global Magnetic Level Gauge Market, with key growth in the UAE, Saudi Arabia, and South Africa. Oil & gas, petrochemicals, and large-scale construction sectors are major drivers of demand. Technological modernization trends include adoption of IIoT-enabled digital magnetic gauges and predictive maintenance tools. Local players, such as Gulf Instrumentation, have introduced high-precision, corrosion-resistant magnetic level gauges in industrial zones, enhancing process safety and reducing downtime. Regional consumer behavior favors high-reliability, remote-monitoring solutions due to operational safety requirements in hazardous and high-capacity industrial facilities.

China – 21% Market Share: High production capacity and extensive industrial infrastructure support widespread adoption.

United States – 18% Market Share: Strong end-user demand in oil & gas, power generation, and water treatment sectors drives deployment.

The Magnetic Level Gauge Market exhibits a moderately fragmented competitive environment with 20+ active competitors globally, reflecting dynamic participation from diversified instrumentation and automation firms. The combined share of the top 5 companies—Emerson Electric Co., Endress+Hauser AG, Siemens AG, KROHNE Messtechnik GmbH, and Honeywell International Inc.—is estimated at approximately 42–45% of installed base influence across major regions. These leaders are engaged in strategic initiatives such as partnerships, product line expansions, and novel technology rollouts to capture expanding demand in oil & gas, chemical processing, water treatment, and power generation markets. In March 2025, Emerson announced a strategic partnership with Yokogawa to co-develop magnetic float level gauge solutions for integrated automation and aftermarket support, enhancing global reach. VEGA secured a large contract win in November 2024 to supply magnetic float gauge systems with long-term service commitments for a major refinery project. KROHNE introduced its LM‑5000 high‑precision magnetic float level gauge in May 2025 for high-temperature, aggressive environments, positioning its portfolio for extreme process conditions. Across the competitive landscape, firms emphasize IoT‑ready transmitters, remote diagnostics, and predictive maintenance tools, influencing competitive positioning and customer decision criteria. The market’s innovation trends are increasingly shaped by digital integration, smart sensor fusion, and enhanced material engineering, differentiating vendor offerings in a landscape driven by safety, operational efficiency, and regulatory compliance.

KROHNE Messtechnik GmbH

Honeywell International Inc.

Yokogawa Electric Corporation

VEGA Grieshaber KG

Magnetrol International, Inc.

WIKA Alexander Wiegand SE & Co. KG

Gems Sensors & Controls

OMEGA Engineering, Inc.

Dwyer Instruments, Inc.

Kobold Messring GmbH

NIVELCO Process Control Co.

The Magnetic Level Gauge Market is undergoing a significant technological evolution as industries prioritize precision, connectivity, and automation. Traditional mechanical magnetic level gauges are progressively being augmented with digital sensors and transmitters capable of providing real‑time level data to distributed control systems (DCS) and IIoT platforms, enabling remote monitoring and enhanced process visibility. The integration of digital communication protocols such as HART, Modbus, and wireless standards facilitates seamless data exchange, improves predictive maintenance capability, and reduces manual intervention. Advanced gauge designs featuring multi‑chamber floats and enhanced magnet configurations offer consistent performance across varied fluid densities and viscosities with improved reliability in turbulent process conditions. Innovations in high‑temperature and high‑pressure gauge hardware enable broader applicability across refineries, petrochemical plants, and LNG facilities, addressing severe operating environments with robust stability and safety.

Emerging technologies also include smart instrumentation integration, where magnetic level gauge data feeds directly into industrial analytics engines and digital twins, supporting real‑time diagnostics and operational efficiency improvements. These advancements help facilities reduce downtime, optimize maintenance cycles, and meet stringent safety and environmental compliance targets. Additionally, evolution in material science, including the use of corrosion‑resistant alloys and PTFE‑lined components, significantly extends service life and reliability in aggressive chemical processes. Collectively, the push toward connected, intelligent level measurement technologies is shaping the competitive landscape, allowing vendors to differentiate with solutions that drive operational excellence and align with Industry 4.0 objectives.

• KROHNE introduced the BM26A‑8000 series of Magnetic Level Indicators in 2023—a new generation of magnetic level indicators designed for redundant level measurement of liquids in applications such as power plants, chemical processing, and oil & gas storage, offering advanced options including radar and TDR integration. Source: www.krohne.com

• KROHNE also highlighted multiple technology advancements in 2025, including a new “Standard” OPTIWAVE radar series with cost‑effective continuous testing and self‑diagnosis features, as well as a new pressure transmitter design with ceramic diaphragm strength for improved toughness in industrial environments. Source: www.industryemea.com

• In April 2025, Endress+Hauser issued an official press communication regarding ongoing product leadership and global service developments in digital plant communications and measurement solutions across process industries, emphasizing enhanced level and related measurement offerings (press briefing). Source: www.endress.com

• Siemens announced in 2025 a major contract win to deploy SITRANS level measurement systems that include magnetic float level sensors for a large Middle East refinery project, signaling broadened Siemens involvement in large‑scale industrial level measurement deployments.

The Magnetic Level Gauge Market Report provides a comprehensive overview of the global landscape, detailing both established market segments and emerging niches across types, applications, technologies, and geographic regions. The report encompasses a thorough breakdown of product variants, such as float chamber gauges, magnetic float gauges, and differential pressure‑based magnetic indicators, highlighting performance attributes, design considerations, and operational environments. On the application front, it covers critical use cases in oil & gas processing, chemical manufacturing, water and wastewater management, power generation, and specialty industrial sectors, providing insight into instrumentation requirements, safety compliance patterns, and usage scenarios tailored to each operational context.

From a technological perspective, the report examines current and emerging innovations including digital integration, smart sensors, advanced magnet designs, enhanced material engineering, and connectivity protocols like HART and Modbus, underscoring how these advancements influence decision‑making for process optimization and maintenance strategies. Geographic coverage spans North America, Europe, Asia Pacific, South America, and Middle East & Africa, with detailed assessments of regional deployment patterns, industry infrastructure developments, technical adoption behavior, and regulatory influences shaping market trajectories.

The report also offers competitive profiling, capturing the strategic positioning, product portfolios, and market influence of key global players. By addressing end‑user insights, it elucidates how varied industries—refineries, petrochemical complexes, industrial water facilities, and others—select and apply magnetic level gauge solutions to meet stringent safety and operational requirements. As an analytical resource, the report serves decision‑makers by providing actionable intelligence on market segmentation, technology trends, regional dynamics, and innovation pathways critical for strategic planning and investment evaluation.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 420 Million |

| Market Revenue (2033) | USD 601.9 Million |

| CAGR (2026–2033) | 4.6% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Regulatory & ESG Overview, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Emerson Electric Co., Endress+Hauser AG, Siemens AG, KROHNE Messtechnik GmbH, Honeywell International Inc., Yokogawa Electric Corporation, VEGA Grieshaber KG, Magnetrol International, Inc., WIKA Alexander Wiegand SE & Co. KG, Gems Sensors & Controls, OMEGA Engineering, Inc., Dwyer Instruments, Inc., Kobold Messring GmbH, NIVELCO Process Control Co. |

| Customization & Pricing | Available on Request (10% Customization Free) |