Reports

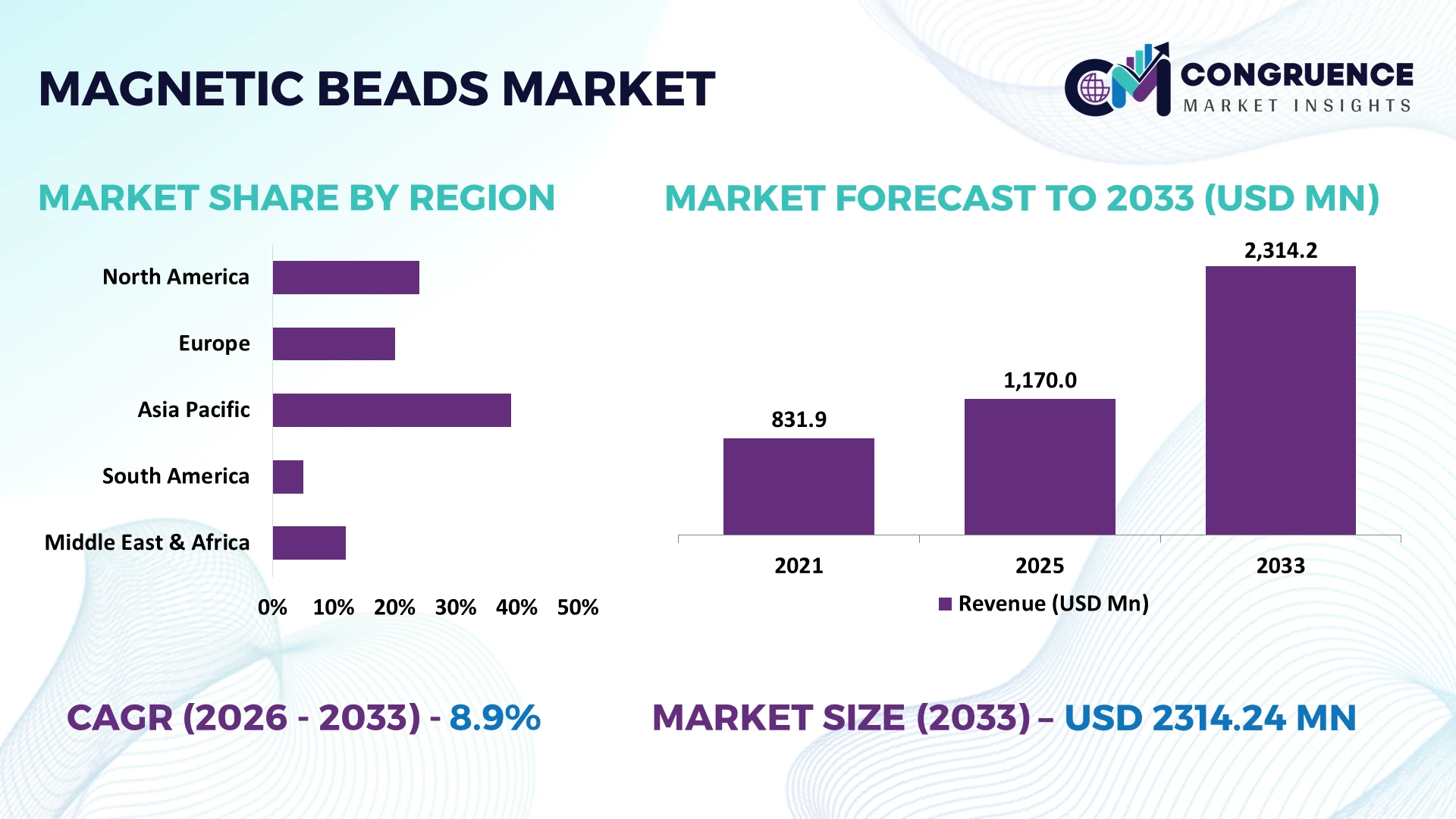

The Global Magnetic Beads Market was valued at USD 1170 Million in 2025 and is anticipated to reach a value of USD 2314.24 Million by 2033 expanding at a CAGR of 8.9% between 2026 and 2033. Growth is primarily driven by expanding molecular diagnostics, automated nucleic acid extraction platforms, and increasing integration of magnetic bead-based workflows in clinical genomics, biopharmaceutical manufacturing, and precision medicine.

The United States accounts for approximately 37% of global magnetic bead demand, supported by multi-billion-dollar investments in biotechnology, advanced clinical diagnostics, and life science research infrastructure, while China contributes nearly 24% through rapid manufacturing expansion and domestic reagent production. Ongoing healthcare supply-chain diversification following geopolitical trade realignments has accelerated localized production capacity and laboratory automation across both markets, strengthening global technology adoption.

Organizations prioritizing scalable manufacturing, automated sample preparation, and resilient regional supply networks are positioned to secure long-term competitive advantage in the global magnetic beads market.

Market Size & Growth: USD 1170 Million in 2025, projected to reach USD 2314.24 Million by 2033 at 8.9% CAGR, driven by automated molecular diagnostics and genomics expansion.

Top Growth Drivers: Clinical diagnostics contribute over 42% demand, genomic research expands by 18%, while laboratory automation adoption exceeds 30% across advanced laboratories.

Short-Term Forecast: By 2027, automated magnetic bead workflows improve sample processing efficiency by 28% while reducing manual handling costs by 20%.

Emerging Technologies: AI-enabled laboratory systems, automated nucleic acid extraction, and high-performance surface-functionalized magnetic beads accelerate workflow accuracy and throughput.

Regional Leaders: North America exceeds USD 820 Million, Asia-Pacific surpasses USD 690 Million, and Europe approaches USD 520 Million, supported by expanding laboratory automation and regional manufacturing.

Consumer & End-User Trends: More than 65% of advanced molecular laboratories increasingly adopt magnetic bead purification for high-throughput clinical and research applications.

Pilot/Case Example: In 2026, automated diagnostic laboratories reported approximately 35% faster sample preparation after deploying integrated magnetic bead extraction systems.

Competitive Landscape: Leading suppliers collectively control nearly 48% market share, with Thermo Fisher Scientific, Merck, Cytiva, Bio-Rad Laboratories, and Takara Bio maintaining strong global positions.

Regulatory & ESG Impact: Sustainable manufacturing initiatives reduce laboratory plastic waste by nearly 15%, while stricter quality standards strengthen product validation across regulated healthcare markets.

Investment & Funding: More than USD 900 Million in strategic investments supports manufacturing expansion, regional partnerships, and supply-chain localization across high-growth biotechnology hubs.

Innovation & Future Outlook: Next-generation functionalized magnetic beads, multiplex diagnostics, and precision bioprocessing platforms accelerate global commercialization and strengthen strategic life science partnerships.

Magnetic beads have become an essential component in molecular diagnostics, cell separation, immunoassays, and biopharmaceutical purification as laboratories prioritize faster, automated sample preparation. More than 55% of newly installed high-throughput genomic platforms incorporate magnetic bead-based extraction technologies, while regional manufacturing expansion and stricter quality compliance continue strengthening supply-chain resilience, creating a solid foundation for the strategic market assessment that follows.

Magnetic beads have become a strategic technology platform as pharmaceutical companies, clinical laboratories, and biotechnology manufacturers prioritize automated sample preparation, higher analytical accuracy, and resilient production networks. The market is increasingly influencing competitive positioning because laboratories require standardized workflows that support high-throughput testing while reducing manual intervention. Ongoing supply-chain restructuring after recent geopolitical trade disruptions has accelerated localized reagent manufacturing and diversified sourcing strategies, strengthening procurement stability across critical life science applications.

Compared with conventional column-based purification, magnetic bead-based extraction improves processing efficiency by approximately 35% while reducing hands-on laboratory time by nearly 40%, enabling scalable automation with consistent recovery rates. The United States continues to lead adoption through advanced genomic research and integrated laboratory automation, whereas China is rapidly expanding domestic manufacturing capacity and lowering production costs through vertically integrated biotechnology ecosystems. Over the next two to three years, automated nucleic acid extraction platforms are expected to account for more than 60% of newly installed molecular diagnostic workflows in advanced laboratories.

A practical example is the deployment of automated magnetic bead extraction systems within hospital diagnostic networks, where laboratories process substantially higher daily sample volumes without proportional workforce expansion. Companies are strengthening competitive positions through localized manufacturing, strategic partnerships with instrument developers, and expanded R&D for application-specific bead chemistries. Organizations that integrate automation, supply resilience, and specialized product innovation will secure stronger operational efficiency and long-term market leadership.

The accelerating adoption of automated molecular diagnostics is reinforcing demand for high-performance magnetic beads across genomics, infectious disease testing, and biopharmaceutical workflows. More than 65% of newly commissioned molecular laboratories now prioritize automated extraction platforms, while workflow efficiency improves by approximately 30% through magnetic separation technologies and sample processing errors decline by nearly 25%. The United States continues expanding precision medicine infrastructure, encouraging suppliers to develop specialized magnetic bead chemistries compatible with next-generation sequencing platforms. In response, companies are increasing manufacturing capacity, forming technology partnerships with diagnostic instrument providers, and investing in application-specific product innovation to strengthen customer retention and improve operational differentiation.

Manufacturers continue facing structural pressure from fluctuating prices of specialty polymers, magnetic nanoparticles, and surface functionalization materials, increasing production costs by nearly 18% during procurement cycles. Approximately 40% of critical raw material inputs remain concentrated within limited supplier networks, creating sourcing vulnerability during logistics disruptions. China remains a significant processing hub, making procurement strategies sensitive to trade policy adjustments and transportation bottlenecks. Companies are reducing operational exposure by diversifying supplier portfolios, establishing localized production facilities, negotiating long-term procurement agreements, and developing alternative coating technologies that improve manufacturing flexibility while protecting product quality and delivery consistency.

Emerging opportunities are centered on functionalized magnetic beads designed for cell therapy, liquid biopsy, and multiplex molecular diagnostics. Automated laboratory platforms improve sample throughput by approximately 45%, while advanced bead chemistries increase target capture efficiency by nearly 20% compared with conventional formulations. Japan continues investing in regenerative medicine and precision diagnostics, creating demand for specialized separation technologies with higher reproducibility. Companies are expanding R&D partnerships with biotechnology firms, integrating AI-supported laboratory workflows, and building innovation ecosystems that accelerate customized product development. These specialized applications provide higher-value market positioning beyond traditional nucleic acid purification.

Maintaining consistent performance across diverse diagnostic instruments, laboratory information systems, and evolving clinical protocols remains a major execution challenge. Cross-platform validation activities can extend product qualification timelines by nearly 30%, while laboratories report integration complexity affecting approximately 22% of new workflow implementations. Germany's highly regulated clinical diagnostics environment highlights the increasing need for standardized validation and interoperability between consumables and automation platforms. Companies must invest in compatibility testing, digital quality management systems, collaborative platform development, and workforce training to ensure deployment consistency, strengthen regulatory compliance, and sustain competitive differentiation in increasingly automated laboratory environments.

Advanced Laboratory Automation Integration Automated magnetic bead workflows now process approximately 38% more samples per shift while reducing manual intervention by nearly 35%. Labor shortages in advanced diagnostic laboratories are accelerating automation deployment, particularly in the United States. Manufacturers are expanding instrument compatibility, strengthening software integration, and partnering with laboratory automation providers to improve throughput and operational consistency.

Localized Manufacturing Network Expansion Companies are restructuring production footprints as supply-chain resilience becomes a procurement priority. More than 30% of leading suppliers have expanded regional manufacturing or secondary sourcing, reducing average delivery times by nearly 20%. China continues strengthening domestic reagent production while European manufacturers increase localized inventory, improving procurement stability and minimizing operational disruption for clinical laboratories.

Application-Specific Bead Engineering Functionalized magnetic beads tailored for cell therapy, liquid biopsy, and multiplex molecular diagnostics are increasing target capture efficiency by approximately 22% while reducing processing variability by nearly 18%. Regulatory emphasis on standardized diagnostic performance is encouraging manufacturers to develop application-focused product portfolios through collaborative R&D, customized surface chemistry, and technology licensing partnerships with biotechnology enterprises.

Digital Workflow Standardization Connected laboratory platforms integrating magnetic bead processing with digital sample tracking have reduced reporting turnaround times by approximately 25% and lowered workflow errors by nearly 17%. A notable operational shift is the growing preference for end-to-end workflow validation instead of standalone reagent qualification. Companies are investing in interoperable software ecosystems, digital quality management, and strategic platform alliances to strengthen long-term customer retention.

Silica-Based magnetic beads remain the leading product category with an estimated 43% market share due to their proven nucleic acid binding efficiency, broad compatibility with automated extraction systems, and cost-effective deployment across clinical laboratories. Their standardized performance and seamless integration with molecular diagnostic instruments continue supporting high-volume testing environments. Agarose-Based beads retain strategic importance in protein purification because of superior biomolecule compatibility, while Polymer-Based products continue expanding through customized surface modifications for specialized research applications.

Functionalized magnetic beads represent the fastest-growing segment as demand increases for cell therapy, liquid biopsy, and precision molecular diagnostics. Adoption of functionalized products has increased by approximately 24%, while enterprise investment in application-specific bead development has expanded by nearly 20%. Manufacturers are prioritizing advanced coating technologies, strategic collaborations with instrument developers, and portfolio expansion to address higher-value laboratory workflows. Investment priorities are steadily shifting toward differentiated products offering greater specificity, reproducibility, and automation compatibility.

Nucleic Acid Isolation accounts for approximately 46% of overall demand, supported by large-scale deployment in molecular diagnostics, genomic sequencing, and infectious disease testing. Standardized extraction protocols and compatibility with automated laboratory platforms continue strengthening its operational importance. Diagnostics is the fastest-growing application as healthcare providers accelerate decentralized testing capabilities and integrated molecular workflows. Diagnostic laboratories increasingly require higher sample throughput, driving broader implementation of automated magnetic bead technologies.

Protein Purification maintains strong demand within biologics manufacturing, while Cell Separation continues expanding across regenerative medicine and immunotherapy research. Immunoassays remain strategically relevant for clinical testing and biomarker analysis, benefiting from improved assay reproducibility. Automated application workflows improve laboratory productivity by nearly 32%, while advanced extraction systems reduce processing variability by approximately 20%. Companies are responding through workflow integration, application-focused product optimization, and collaborative development with clinical instrument manufacturers to strengthen long-term adoption across multiple laboratory environments.

Diagnostic Laboratories represent the largest end-user group with approximately 41% market share, supported by continuous sample processing requirements, automated testing infrastructure, and expanding molecular diagnostic capacity. High operational intensity makes this segment the primary purchaser of standardized magnetic bead consumables. Biotechnology Companies are the fastest-growing buyers as precision medicine, cell therapy, and advanced genomics programs increase demand for customized separation technologies and specialized reagent solutions.

Pharmaceutical Companies continue expanding utilization in biologics development and drug discovery workflows, while Research Institutes remain essential adopters for genomics, proteomics, and translational research projects. Automated laboratory deployment has increased by approximately 29%, and customized reagent demand has expanded by nearly 21% among biotechnology organizations. Companies are strengthening customer engagement through application-specific product customization, strategic research partnerships, flexible pricing models, and integrated workflow support, enabling stronger competitive positioning across diverse scientific and clinical environments.

North America accounted for the largest market share at 39% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 10.2% between 2026 and 2033.

Advanced Molecular Diagnostics Drive Regional Leadership

North America maintains the leading position through extensive deployment of molecular diagnostics, genomics research, and biopharmaceutical manufacturing. The region contributes approximately 39% of global demand, supported by widespread laboratory automation and mature healthcare infrastructure. More than 70% of high-throughput clinical laboratories have integrated magnetic bead-based extraction workflows into routine testing operations, improving processing consistency and turnaround efficiency. Strong collaboration between biotechnology companies, diagnostic platform developers, and pharmaceutical manufacturers continues accelerating commercialization of specialized bead chemistries. Enterprise investment increasingly targets automated sample preparation, precision medicine, and integrated laboratory information systems, enabling higher productivity while strengthening operational resilience across clinical and research environments.

United States Market Outlook: The United States leads regional demand through its advanced biotechnology ecosystem, extensive genomic sequencing capacity, and large concentration of diagnostic laboratories. More than 65% of newly installed automated molecular testing systems utilize magnetic bead-based extraction technologies. Companies continue expanding manufacturing facilities, collaborating with sequencing platform providers, and investing in specialized functionalized bead products that support precision diagnostics, cell therapy development, and scalable laboratory automation.

Regulatory Standardization Strengthens Technology Adoption

Europe benefits from a highly regulated healthcare environment that prioritizes standardized laboratory workflows, product validation, and diagnostic quality assurance. The region represents approximately 28% of global market activity, supported by strong pharmaceutical manufacturing and biomedical research infrastructure. Laboratory modernization initiatives have increased automated sample preparation deployment by nearly 26% across leading healthcare institutions. Sustainability objectives also encourage manufacturers to optimize production efficiency and reduce laboratory waste through improved reagent utilization. Companies continue strengthening regional manufacturing capabilities, expanding technology partnerships, and introducing specialized magnetic bead platforms that comply with evolving quality and clinical performance standards.

Germany Market Outlook: Germany serves as Europe's primary biotechnology and life science manufacturing hub, supported by advanced research institutes, pharmaceutical production, and industrial automation expertise. More than 40% of regional biotechnology equipment investment is concentrated in Germany's leading innovation clusters. Companies continue expanding collaborative research, precision diagnostics development, and automated laboratory infrastructure, reinforcing long-term demand for high-performance magnetic bead technologies.

Manufacturing Expansion Accelerates Market Scale

Asia-Pacific is rapidly strengthening its competitive position through expanding biotechnology manufacturing, growing molecular diagnostics capacity, and large-scale laboratory infrastructure investments. The region accounts for approximately 26% of global demand while serving as a major production center for laboratory consumables. Domestic manufacturing output has expanded by nearly 30% across key biotechnology hubs, improving supply reliability and reducing procurement lead times. Governments continue supporting healthcare modernization and local production capabilities, encouraging enterprises to establish regional manufacturing partnerships. Companies are scaling production, increasing automation, and broadening distribution networks to support rising clinical diagnostics and life science research requirements.

China Market Outlook: China remains the region's largest manufacturing and deployment center for magnetic bead technologies, supported by integrated biotechnology supply chains and expanding domestic diagnostic capacity. Automated molecular testing installations have increased by approximately 35% across major healthcare institutions. Manufacturers continue investing in localized innovation, advanced production facilities, and strategic partnerships to strengthen global competitiveness while reducing dependence on imported laboratory reagents.

Clinical Infrastructure Modernization Supports Adoption

South America continues expanding magnetic bead utilization through improving clinical diagnostics infrastructure, biotechnology research, and public healthcare modernization programs. The region contributes approximately 5% of global market activity, with adoption concentrated in large urban healthcare networks. Laboratory automation deployments have increased by nearly 18% as hospitals improve molecular testing capabilities for infectious disease surveillance and precision diagnostics. Infrastructure limitations and uneven procurement capacity continue influencing implementation speed, encouraging suppliers to strengthen distributor partnerships and localized technical support. Companies increasingly focus on affordable automated solutions that improve laboratory efficiency while supporting long-term operational scalability.

Brazil Market Outlook: Brazil leads regional demand through its extensive healthcare network, expanding biotechnology research ecosystem, and growing pharmaceutical manufacturing sector. More than half of the region's advanced molecular diagnostic laboratories are located within Brazil's major metropolitan centers. Companies continue investing in local distribution partnerships, laboratory training programs, and customized diagnostic solutions that improve accessibility and strengthen nationwide deployment of magnetic bead technologies.

Healthcare Investment Drives Laboratory Transformation

The Middle East & Africa market is progressing through expanding healthcare infrastructure, biotechnology investment, and modernization of clinical laboratory capabilities. The region represents approximately 2% of global demand but continues strengthening its operational foundation through government-supported healthcare initiatives. Automated laboratory installations have increased by nearly 20% across major healthcare facilities, improving molecular diagnostic capacity and workflow efficiency. Strategic investment in biotechnology parks and specialized research centers is encouraging technology transfer and enterprise collaboration. Companies are responding by expanding regional partnerships, establishing technical support capabilities, and introducing validated diagnostic solutions tailored to evolving laboratory requirements.

Saudi Arabia Market Outlook: Saudi Arabia has emerged as the region's most significant market through sustained healthcare modernization, biotechnology investment, and advanced laboratory development. National healthcare transformation initiatives continue expanding molecular diagnostic infrastructure, with automated laboratory capacity increasing by approximately 22% in major medical centers. Companies are strengthening local partnerships, expanding technical training, and supporting domestic laboratory capabilities to improve long-term technology adoption and operational sustainability.

The market is led by Thermo Fisher Scientific, Merck, Cytiva, Bio-Rad Laboratories, and Takara Bio, competing directly against specialized regional manufacturers and cost-focused reagent suppliers. The top five companies collectively control approximately 49% of global market activity through integrated product portfolios, established distribution, and validated laboratory workflows. Competition is increasingly determined by technology performance, workflow compatibility, and supply reliability rather than pricing alone. Functionalized magnetic beads improve target capture efficiency by nearly 22%, while automated extraction platforms reduce processing time by approximately 35%, strengthening premium product positioning. Companies are expanding manufacturing capacity, pursuing instrument partnerships, and vertically integrating reagent production to secure supply resilience and accelerate customized product development. Consolidation is shifting competition toward complete workflow ecosystems instead of standalone consumables. High regulatory validation requirements, application-specific expertise, and automation compatibility create substantial entry barriers for new participants. Winning requires differentiated bead chemistry, dependable supply networks, automation integration, rapid innovation, and strong enterprise partnerships.

Thermo Fisher Scientific

Merck KGaA

Cytiva

Bio-Rad Laboratories

Takara Bio

Promega Corporation

Miltenyi Biotec

Bangs Laboratories

Spherotech

GenScript Biotech

New England Biolabs

Rockland Immunochemicals

Geneaid Biotech Ltd.

BeaverBio

Magnetic bead technology is transitioning from conventional nucleic acid extraction toward integrated, application-specific separation platforms supporting genomics, cell therapy, and precision diagnostics. Functionalized surface chemistries increase target binding efficiency by approximately 22%, while automated magnetic separation reduces manual laboratory intervention by nearly 35%. More than 60% of newly deployed high-throughput molecular diagnostic systems now incorporate magnetic bead workflows, demonstrating strong enterprise adoption. Compared with legacy column-based purification, automated magnetic bead platforms improve sample throughput by approximately 40% while delivering greater reproducibility and simplified workflow standardization.

Emerging technologies combine AI-enabled laboratory automation, digital sample traceability, and multiplex molecular testing within unified processing environments. Laboratories implementing intelligent workflow management report approximately 25% faster reporting cycles and nearly 18% lower operational errors. Biotechnology companies developing customized magnetic bead chemistries gain a competitive advantage by supporting specialized applications including liquid biopsy, regenerative medicine, and advanced biomarker analysis. Instrument manufacturers also benefit through deeper workflow integration, increasing customer retention and expanding long-term platform utilization.

Between 2026 and 2028, innovation will increasingly focus on nanostructured magnetic materials, automated closed-loop processing, and application-specific surface engineering. Deployment of interoperable laboratory platforms is expected to exceed 70% among advanced molecular diagnostic facilities, strengthening operational consistency and reducing validation complexity. Organizations investing now in scalable automation, digital integration, and differentiated bead technologies will achieve stronger laboratory productivity, faster commercialization, and sustainable competitive positioning as precision diagnostics and biopharmaceutical manufacturing continue evolving.

October 2024 MagBio Genomics launched the SFD-10HT Short Fragment Depletor magnetic bead kit for automated long-read sequencing workflows, enabling selective removal of DNA fragments below 10 kb. The innovation improves high-molecular-weight DNA preparation efficiency for advanced genomic research and laboratory automation.

December 2024 Quanterix completed the acquisition of EMISSION's magnetic bead technology assets in a deal valued at approximately USD 10 million, strengthening proprietary bead capabilities for ultra-sensitive Simoa assays and improving diagnostic platform differentiation.

February 2025 Thermo Fisher Scientific announced the acquisition of Solventum's Purification & Filtration business for USD 4.1 billion, expanding bioprocessing capabilities and reinforcing its integrated life science workflow portfolio supporting magnetic bead-based purification applications.

August 2025 Thermo Fisher Scientific introduced the Applied Biosystems MagMAX HMW DNA Kit, a magnetic bead-based solution compatible with KingFisher automation, improving reproducible high-molecular-weight DNA isolation for long-read sequencing and scalable genomic workflows.

This report provides comprehensive analysis across Silica-Based, Agarose-Based, Polymer-Based, and Functionalized magnetic beads while evaluating applications including Nucleic Acid Isolation, Protein Purification, Cell Separation, Immunoassays, and Diagnostics. The assessment covers Biotechnology Companies, Pharmaceutical Companies, Diagnostic Laboratories, and Research Institutes across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa. More than 10 major industry participants and evolving deployment patterns are evaluated to identify competitive positioning, technology adoption, and operational differentiation.

The study examines laboratory automation, functionalized bead technologies, molecular diagnostics, and bioprocessing innovations shaping market evolution between 2026 and 2033. It analyzes segment-level adoption trends, regional manufacturing expansion, supply-chain localization, enterprise partnerships, and workflow integration strategies. The report supports investment prioritization, product portfolio planning, geographic expansion, competitive benchmarking, and long-term strategic decision-making by identifying high-potential application areas, emerging technology opportunities, and operational shifts influencing future market direction.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2025 | USD 1170 Million |

Market Revenue in 2033 | USD 2314.24 Million |

CAGR (2026 - 2033) | 8.9% |

Base Year | 2025 |

Forecast Period | 2026 - 2033 |

Historic Period | 2021 - 2025 |

Segments Covered | By Type

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | Thermo Fisher Scientific, Merck KGaA, Cytiva, Bio-Rad Laboratories, Takara Bio, Promega Corporation, Miltenyi Biotec, Bangs Laboratories, Spherotech, GenScript Biotech, New England Biolabs, Rockland Immunochemicals, Geneaid Biotech Ltd., BeaverBio |

Customization & Pricing | Available on Request (10% Customization is Free) |