Reports

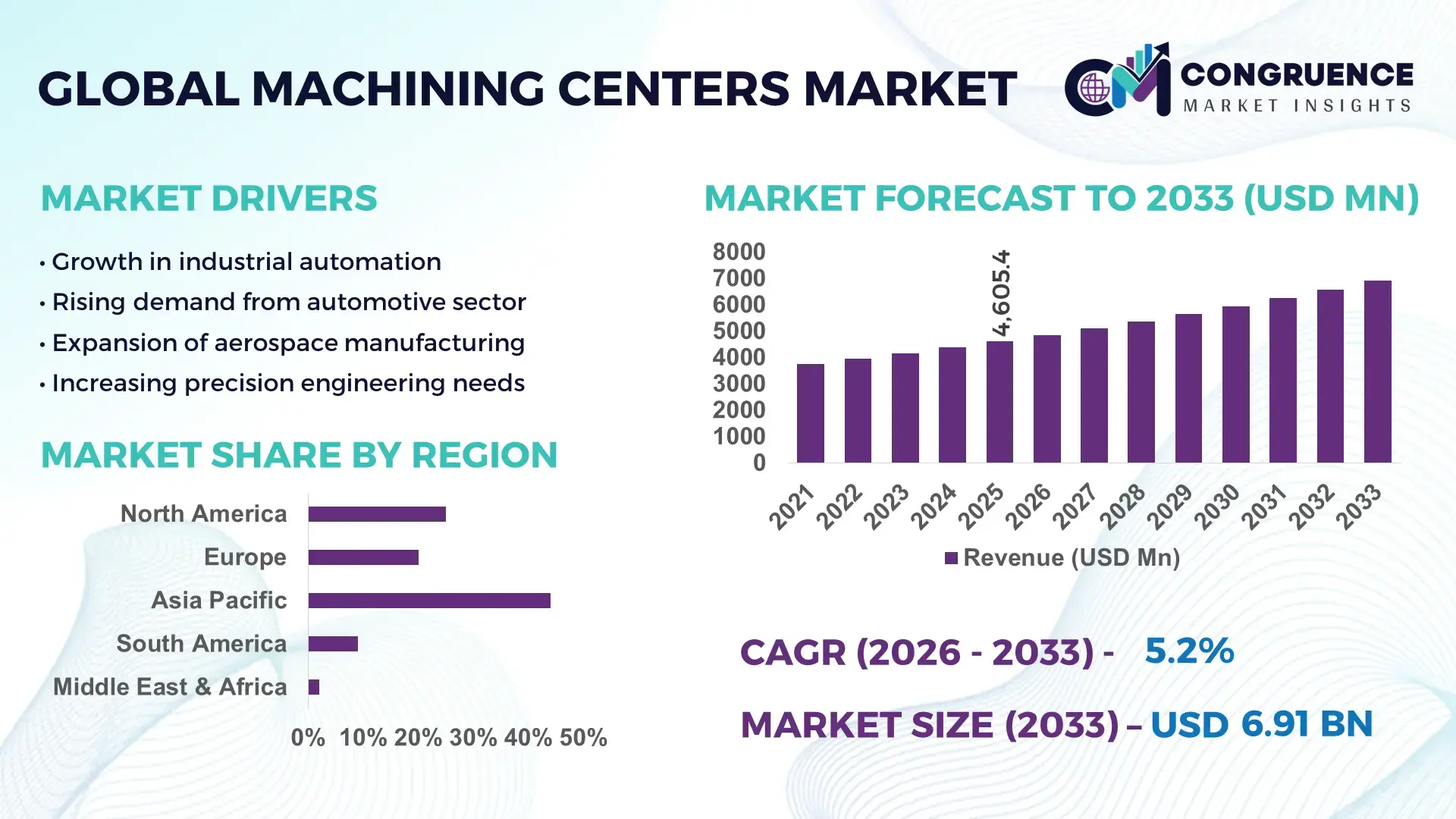

The Global Machining Centers Market was valued at USD 4605.43 Million in 2025 and is anticipated to reach a value of USD 6908.7 Million by 2033 expanding at a CAGR of 5.2% between 2026 and 2033. This growth is primarily driven by increasing automation in precision manufacturing and rising demand for high-efficiency CNC machining solutions.

China continues to dominate the machining centers market in terms of production capacity and industrial deployment. The country produces over 35% of global CNC machine tools annually, supported by strong domestic demand across automotive, aerospace, and electronics manufacturing sectors. Investments exceeding USD 2 billion annually in advanced manufacturing infrastructure and smart factories have accelerated adoption of 5-axis machining centers and automated tool systems. Over 60% of large-scale manufacturing facilities in China have integrated CNC-based machining solutions, while government-backed initiatives in industrial robotics and digital manufacturing have increased operational efficiency by up to 25% across key production clusters.

Market Size & Growth: USD 4605.43 Million in 2025, projected to reach USD 6908.7 Million by 2033 at 5.2% CAGR, driven by rising industrial automation and precision engineering demand.

Top Growth Drivers: Automation adoption increased by 42%, multi-axis machining efficiency improved by 35%, and demand from aerospace manufacturing rose by 28%.

Short-Term Forecast: By 2028, machining centers are expected to reduce production cycle times by 22% through AI-enabled optimization.

Emerging Technologies: Integration of AI-driven predictive maintenance, IoT-enabled smart machining systems, and hybrid additive-subtractive manufacturing technologies.

Regional Leaders: Asia-Pacific projected at USD 3200 Million by 2033 with strong manufacturing expansion; North America at USD 1800 Million driven by aerospace adoption; Europe at USD 1400 Million with focus on precision engineering.

Consumer/End-User Trends: Automotive and aerospace sectors account for over 55% usage, with increasing demand for customized, high-precision components.

Pilot or Case Example: In 2024, a smart factory initiative reduced machining downtime by 30% using real-time analytics integration.

Competitive Landscape: Market leader holds approximately 18% share, followed by key players including global CNC manufacturers and automation specialists.

Regulatory & ESG Impact: Adoption of energy-efficient machining systems reduced industrial energy consumption by 18% under sustainability mandates.

Investment & Funding Patterns: Over USD 3.5 billion invested in smart manufacturing and CNC innovation projects globally.

Innovation & Future Outlook: Increasing adoption of digital twins, cloud-based machining analytics, and autonomous production systems shaping future growth.

The machining centers market is heavily influenced by key industrial sectors such as automotive, aerospace, defense, and electronics, contributing over 70% of total equipment utilization. Recent innovations include high-speed 5-axis machining centers, AI-integrated CNC controllers, and hybrid machines capable of combining milling and additive processes. Regulatory pressures for energy efficiency and emissions reduction are pushing manufacturers to adopt eco-friendly machining technologies, resulting in up to 20% energy savings per unit. Regionally, Asia-Pacific leads in consumption due to large-scale industrialization, while North America and Europe focus on high-precision and customized manufacturing. Emerging trends such as digital manufacturing ecosystems, robotics integration, and smart factory deployment are expected to further transform operational efficiency and production scalability.

The machining centers market holds strong strategic relevance as a foundational pillar in modern manufacturing ecosystems, enabling high-precision production across industries such as aerospace, automotive, and electronics. The integration of AI-enabled CNC machining systems is transforming operational efficiency, where intelligent automation delivers nearly 30% improvement in production throughput compared to conventional CNC machines. Advanced 5-axis machining centers are increasingly replacing 3-axis systems, offering up to 40% reduction in setup time and enhanced geometric accuracy.

Asia-Pacific dominates in production volume due to large-scale manufacturing capabilities, while North America leads in advanced technology adoption, with over 55% of enterprises integrating smart machining solutions into their operations. By 2028, AI-driven predictive maintenance and real-time process optimization are expected to reduce equipment downtime by up to 35%, significantly improving manufacturing reliability.

From an ESG perspective, firms are committing to sustainability targets, including a 25% reduction in energy consumption and material waste by 2030 through adoption of energy-efficient machining technologies and closed-loop manufacturing systems. In 2024, a major industrial manufacturer in Germany achieved a 28% reduction in operational downtime by implementing IoT-enabled CNC monitoring systems combined with AI analytics. Strategically, the machining centers market is evolving toward digital manufacturing ecosystems that combine automation, data analytics, and cloud connectivity. This transformation positions the machining centers market as a critical enabler of resilient supply chains, regulatory compliance, and sustainable industrial growth in the coming decade.

The increasing need for high-precision components across industries such as aerospace, automotive, and electronics is a major driver of the machining centers market. Aerospace manufacturing requires tolerances within microns, pushing demand for advanced 5-axis machining centers capable of achieving up to 50% higher accuracy compared to conventional machines. In the automotive sector, the transition to electric vehicles has increased demand for complex components such as battery housings and motor parts, with machining requirements rising by over 30%. Additionally, electronics manufacturing, particularly semiconductor equipment production, relies heavily on ultra-precision machining processes. The adoption of CNC machining centers has improved production efficiency by nearly 35%, enabling manufacturers to meet stringent quality standards while reducing waste and rework rates.

The high capital expenditure required for advanced machining centers presents a significant restraint, particularly for small and medium-sized enterprises. A modern 5-axis CNC machining center can cost between USD 250,000 and USD 500,000, excluding installation and training expenses. Maintenance costs, including tooling, software upgrades, and skilled labor, further increase operational expenses by approximately 15–20% annually. Additionally, the need for highly trained operators limits adoption in regions with skill shortages. Financial constraints and long return-on-investment periods discourage smaller manufacturers from upgrading their equipment. Economic uncertainties and fluctuating raw material costs also impact purchasing decisions, slowing down market penetration in price-sensitive regions.

The integration of smart manufacturing technologies presents significant growth opportunities for the machining centers market. IoT-enabled machining centers allow real-time monitoring of machine performance, reducing downtime by up to 30% and improving overall equipment effectiveness. The adoption of digital twins enables manufacturers to simulate machining processes, reducing errors and optimizing production efficiency by nearly 25%. Additionally, the rise of Industry 4.0 is driving demand for interconnected production systems, where machining centers operate within fully automated workflows. Emerging markets are increasingly investing in smart factory infrastructure, with industrial automation adoption growing by over 40% in recent years. These advancements are opening new avenues for manufacturers to enhance productivity, reduce operational costs, and deliver customized solutions at scale.

The growing complexity of advanced machining centers, particularly those integrated with AI and IoT systems, has created a significant skills gap in the workforce. Operating modern CNC systems requires expertise in programming, data analysis, and machine maintenance, yet nearly 45% of manufacturers report difficulty in finding qualified personnel. Training costs and time further add to operational burdens, with specialized training programs lasting several months. Additionally, the integration of new technologies into existing production lines can lead to compatibility issues and increased implementation costs. Cybersecurity risks associated with connected machining systems also pose challenges, as manufacturers must invest in secure networks and data protection measures. These factors collectively hinder the seamless adoption of advanced machining technologies across the industry.

• Accelerated Adoption of Smart CNC and AI-Driven Machining Systems: The integration of artificial intelligence and smart CNC technologies is transforming machining operations, with over 48% of manufacturing facilities globally adopting AI-enabled machining centers by 2025. These systems improve predictive maintenance accuracy by nearly 35% and reduce unplanned downtime by up to 30%. Real-time analytics and machine learning algorithms enhance tool life by 20% while increasing machining precision by approximately 15%, particularly in aerospace and automotive component production environments.

• Expansion of 5-Axis and Multi-Tasking Machining Capabilities: Advanced 5-axis machining centers now account for nearly 38% of total installations, reflecting a 25% increase in adoption over the past three years. These machines reduce setup time by up to 40% and enable the machining of complex geometries in a single operation, improving productivity by 28%. Multi-tasking machines combining milling, turning, and drilling functions have enhanced operational efficiency by 32%, particularly in high-precision industries such as medical devices and defense manufacturing.

• Rise in Modular and Prefabricated Construction Demand: The adoption of modular and prefabricated construction is reshaping machining center demand, with approximately 55% of new infrastructure projects reporting cost savings through prefabrication. Automated machining centers are increasingly used for pre-cut and pre-bent structural components, reducing labor requirements by 30% and accelerating project timelines by 25%. Demand for high-precision machining equipment has grown by over 20% in Europe and North America, where construction efficiency and standardization are critical performance metrics.

• Growing Focus on Energy-Efficient and Sustainable Machining Solutions: Sustainability-driven manufacturing is influencing equipment design, with energy-efficient machining centers reducing power consumption by up to 18% compared to traditional systems. Approximately 42% of manufacturers have adopted eco-friendly machining practices, including optimized coolant usage and recyclable tooling materials. Additionally, closed-loop manufacturing systems have reduced material waste by nearly 22%, aligning with regulatory requirements and corporate ESG targets across industrialized regions.

The machining centers market is segmented based on type, application, and end-user industries, each contributing distinctively to overall market dynamics. By type, vertical machining centers dominate due to their versatility and cost efficiency, while horizontal and multi-axis machining centers are gaining traction in high-precision applications. In terms of application, automotive manufacturing accounts for over 35% of total usage, followed by aerospace and defense at approximately 22%, driven by increasing demand for complex components. End-user segmentation highlights large-scale manufacturing enterprises as primary adopters, representing nearly 60% of installations, while small and medium enterprises are gradually increasing adoption due to improved accessibility of advanced CNC technologies. The segmentation reflects a shift toward automation, customization, and precision-driven manufacturing across global industries.

Vertical machining centers (VMCs) currently account for approximately 46% of total market adoption due to their cost-effectiveness, ease of operation, and suitability for a wide range of applications such as milling and drilling. In comparison, horizontal machining centers (HMCs) hold around 28% share, offering better chip evacuation and higher efficiency for large-scale production. However, 5-axis machining centers are emerging as the fastest-growing segment, expanding at an estimated CAGR of 7.1%, driven by demand for complex component manufacturing and reduced setup times. These advanced systems are increasingly used in aerospace and medical industries, where precision and multi-angle machining are critical. Other types, including gantry and universal machining centers, collectively contribute nearly 26% of the market, catering to niche industrial requirements such as heavy-duty machining and large component fabrication.

The automotive sector leads the machining centers market with an estimated 37% share, driven by high-volume production requirements and increasing demand for electric vehicle components. Aerospace and defense applications follow with approximately 24% adoption, benefiting from the need for high-precision machining and lightweight component manufacturing. However, the medical device sector is emerging as the fastest-growing application segment, expanding at a CAGR of 6.8%, supported by rising demand for customized implants and surgical instruments. Electronics manufacturing also contributes significantly, accounting for nearly 18% of usage, particularly in semiconductor equipment production. Other applications, including energy and heavy machinery, collectively represent around 21% of the market.

Large-scale manufacturing enterprises dominate the machining centers market, accounting for nearly 62% of total adoption due to their capacity for high capital investment and need for large-scale production efficiency. Small and medium enterprises (SMEs) represent around 25% of the market, increasingly adopting compact and cost-efficient machining solutions. However, contract manufacturing and precision engineering firms are the fastest-growing end-user segment, expanding at a CAGR of 6.5%, driven by outsourcing trends and demand for specialized machining services. Industries such as aerospace, automotive, and electronics collectively account for over 70% of end-user demand, reflecting strong reliance on precision machining capabilities.

Region Asia-Pacific accounted for the largest market share at 48% in 2025 however, Region North America is expected to register the fastest growth, expanding at a CAGR of 6.1% between 2026 and 2033.

Asia-Pacific’s dominance is supported by high-volume manufacturing output, with China, Japan, and India collectively contributing over 65% of regional machining center installations. The region also accounts for nearly 52% of global CNC machine production capacity, driven by large-scale industrial clusters and export-oriented manufacturing. Europe holds approximately 27% of the market, led by Germany, Italy, and France, where precision engineering accounts for over 40% of machining center usage. North America represents around 18%, with strong demand from aerospace and defense sectors contributing over 35% of regional consumption. South America and the Middle East & Africa together account for nearly 7%, with growing investments in energy, infrastructure, and industrial automation projects increasing machining center deployment by 15–20% across emerging economies.

How are advanced manufacturing investments accelerating precision machining adoption?

North America holds approximately 18% of the global machining centers market, driven by strong demand from aerospace, automotive, and defense industries. Aerospace manufacturing alone contributes over 38% of machining center usage in the region due to high precision requirements. Government-backed initiatives promoting domestic manufacturing and supply chain resilience have increased capital investment in advanced machining technologies by nearly 20% since 2023. The adoption of smart manufacturing solutions, including AI-integrated CNC systems, has improved production efficiency by up to 30%. A key industry participant, Haas Automation, has expanded its production capacity by over 15% through investments in automated machining systems and digital manufacturing processes. Consumer behavior in this region reflects high enterprise adoption, with over 60% of large manufacturers integrating connected machining systems for real-time monitoring and predictive maintenance.

What factors are driving high-precision engineering and sustainable machining innovation?

Europe accounts for approximately 27% of the machining centers market, with Germany, the UK, and France leading in industrial adoption. Germany alone contributes nearly 35% of regional demand due to its strong automotive and industrial machinery sectors. Strict regulatory frameworks focused on energy efficiency and emissions reduction have driven adoption of eco-friendly machining technologies, reducing energy consumption by up to 18%. The region has seen over 45% adoption of advanced CNC systems integrated with IoT and digital twins for process optimization. A notable example includes DMG Mori, which has implemented smart factory solutions improving operational efficiency by 25% across its European facilities. Consumer behavior in Europe is influenced by regulatory pressure, leading to increased demand for precision, traceability, and sustainable machining solutions across industries.

Why is large-scale industrial expansion fueling machining center demand?

Asia-Pacific leads the global machining centers market with nearly 48% share, supported by strong manufacturing output in China, Japan, and India. China alone contributes over 35% of global CNC machine production, while Japan accounts for approximately 20% of high-precision machining equipment exports. Rapid industrialization and infrastructure development have increased machining center installations by over 25% in the past five years. The region is also a hub for technological innovation, with over 50% of manufacturers adopting automation and robotics in machining operations. Fanuc Corporation has enhanced its production capabilities by integrating AI-driven CNC systems, resulting in a 28% increase in machining efficiency. Consumer behavior reflects high adoption rates in electronics and automotive sectors, with over 65% of manufacturers prioritizing cost-efficient, high-volume production solutions.

How are industrial diversification and policy support shaping machining demand?

South America represents approximately 5% of the global machining centers market, with Brazil and Argentina as key contributors. Brazil accounts for nearly 60% of regional demand, driven by automotive manufacturing and energy sector investments. Infrastructure development projects have increased demand for machining centers by approximately 18% over recent years. Government incentives aimed at promoting local manufacturing and reducing import dependency have supported equipment adoption. Local manufacturers have increased production output by 12–15% through modernization initiatives and automation integration. Consumer behavior in the region shows demand closely tied to industrial expansion, with over 40% of machining center usage concentrated in automotive and heavy machinery sectors.

What role do industrial modernization and energy projects play in equipment adoption?

The Middle East & Africa region holds around 2% of the machining centers market, with demand primarily driven by oil & gas, construction, and infrastructure projects. The UAE and South Africa are key markets, contributing over 55% of regional demand. Industrial diversification strategies and investments in smart manufacturing have increased machining center adoption by approximately 20% in recent years. Trade partnerships and government-led industrialization programs have facilitated technology transfer and equipment imports. A regional industrial firm has implemented automated machining systems, improving production efficiency by 22% in energy-related component manufacturing. Consumer behavior reflects growing interest in modernization, with increasing adoption of advanced machining technologies to support large-scale infrastructure and industrial projects.

China – 35% market share in Machining Centers market, driven by massive production capacity and strong domestic manufacturing demand.

Germany – 14% market share in Machining Centers market, supported by advanced engineering expertise and high adoption in automotive and industrial machinery sectors.

The machining centers market is moderately fragmented, with over 120 active global and regional competitors operating across different segments of CNC and advanced machining technologies. The top five companies collectively account for approximately 42% of the global market, indicating a competitive yet innovation-driven landscape. Leading players focus heavily on product differentiation through advanced features such as AI-enabled controls, multi-axis machining capabilities, and IoT integration. Strategic initiatives including mergers, partnerships, and facility expansions have increased by nearly 25% over the past three years, reflecting aggressive competition for market share.

Product innovation remains a key competitive factor, with more than 60% of manufacturers investing in smart machining technologies and digital manufacturing ecosystems. Companies are also prioritizing energy-efficient designs, reducing machine energy consumption by up to 20% to align with sustainability requirements. Additionally, after-sales services, including predictive maintenance and remote monitoring, have become critical differentiators, with service-based revenue streams contributing to nearly 15% of overall business operations. The competitive landscape is further shaped by regional players focusing on cost-effective solutions, while global leaders emphasize high-precision and technologically advanced machining systems.

DMG Mori

Mazak Corporation

Haas Automation

Okuma Corporation

Makino Milling Machine Co., Ltd.

Fanuc Corporation

Doosan Machine Tools

Hurco Companies Inc.

Hyundai WIA

GF Machining Solutions

Hermle AG

Starrag Group

Technological advancements in the machining centers market are increasingly centered on automation, precision engineering, and digital integration. One of the most significant developments is the widespread adoption of AI-enabled CNC systems, with over 50% of newly installed machining centers incorporating intelligent control features for real-time optimization. These systems improve machining accuracy by up to 20% and reduce tool wear by approximately 18%, enabling longer operational cycles and lower maintenance frequency. The integration of Industrial Internet of Things (IIoT) technologies is also transforming machining operations. Nearly 45% of manufacturers have implemented connected machining solutions that allow real-time monitoring of spindle performance, vibration levels, and thermal stability. This connectivity has reduced unplanned downtime by 30% and improved overall equipment effectiveness by 25%. Digital twin technology is gaining traction, allowing manufacturers to simulate machining processes and reduce production errors by up to 28%, particularly in high-precision industries such as aerospace and medical devices.

Advanced multi-axis machining technologies, especially 5-axis and hybrid machining centers, are becoming standard in complex component manufacturing. These machines reduce setup time by up to 40% and enable single-pass machining of intricate geometries, improving throughput by 30%. Additionally, hybrid systems combining additive and subtractive manufacturing are expanding capabilities, allowing material deposition and machining within a single platform, reducing material waste by nearly 22%. Energy-efficient machining solutions are also emerging as a critical innovation area, with modern systems consuming up to 18% less energy through optimized spindle drives and regenerative braking technologies. Automation through robotic integration has further enhanced productivity, with robotic loading and unloading systems increasing production output by 35% while minimizing human intervention. These advancements collectively position machining centers as core components in smart manufacturing ecosystems.

• In March 2025, DMG MORI introduced its next-generation 5-axis machining center equipped with integrated digital twin technology and AI-based process optimization, enabling up to 30% reduction in setup time and significantly improving machining accuracy in aerospace component manufacturing.

• In September 2024, Mazak Corporation expanded its Smart Factory initiative by deploying advanced IoT-enabled machining centers across its production facilities, achieving a 25% increase in operational efficiency and enabling real-time monitoring of over 10,000 machine parameters.

• In January 2025, FANUC Corporation enhanced its CNC control systems with AI-driven predictive maintenance features, reducing machine downtime by approximately 32% and extending tool life through advanced analytics and automated diagnostics.

• In July 2024, Haas Automation launched an upgraded line of vertical machining centers with improved spindle speed and energy-efficient drives, delivering up to 15% higher productivity and reducing power consumption by nearly 12% in high-volume manufacturing environments.

The machining centers market report provides a comprehensive analysis of the global industry, covering a wide range of segments, technologies, and end-user industries. The scope includes detailed segmentation by type, such as vertical, horizontal, and multi-axis machining centers, with vertical systems accounting for nearly 46% of installations and multi-axis systems showing rapid adoption in high-precision sectors. Application coverage spans key industries including automotive, aerospace, medical devices, electronics, and heavy machinery, which together contribute over 75% of total machining center utilization. Geographically, the report evaluates major regions including Asia-Pacific, North America, Europe, South America, and the Middle East & Africa, with Asia-Pacific leading in production volume at approximately 48% of global output. The scope also incorporates analysis of emerging markets where industrialization and infrastructure investments are increasing machining center adoption by 15–20%.

From a technology perspective, the report examines advancements such as AI-integrated CNC systems, IoT-enabled smart machining, digital twin simulations, and hybrid additive-subtractive manufacturing solutions. These technologies have improved operational efficiency by up to 35% and reduced material waste by over 20% across multiple industries. Additionally, the report covers industry-specific trends, including automation adoption rates exceeding 50% in large manufacturing enterprises and increasing penetration among small and medium-sized businesses. It also highlights niche segments such as micro-machining for electronics and high-speed machining for aerospace, providing a holistic view of current capabilities and future opportunities within the machining centers market.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

5.2% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

DMG Mori, Mazak Corporation, Haas Automation, Okuma Corporation, Makino Milling Machine Co., Ltd., Fanuc Corporation, Doosan Machine Tools, Hurco Companies Inc., Hyundai WIA, GF Machining Solutions, Hermle AG, Starrag Group |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |