Reports

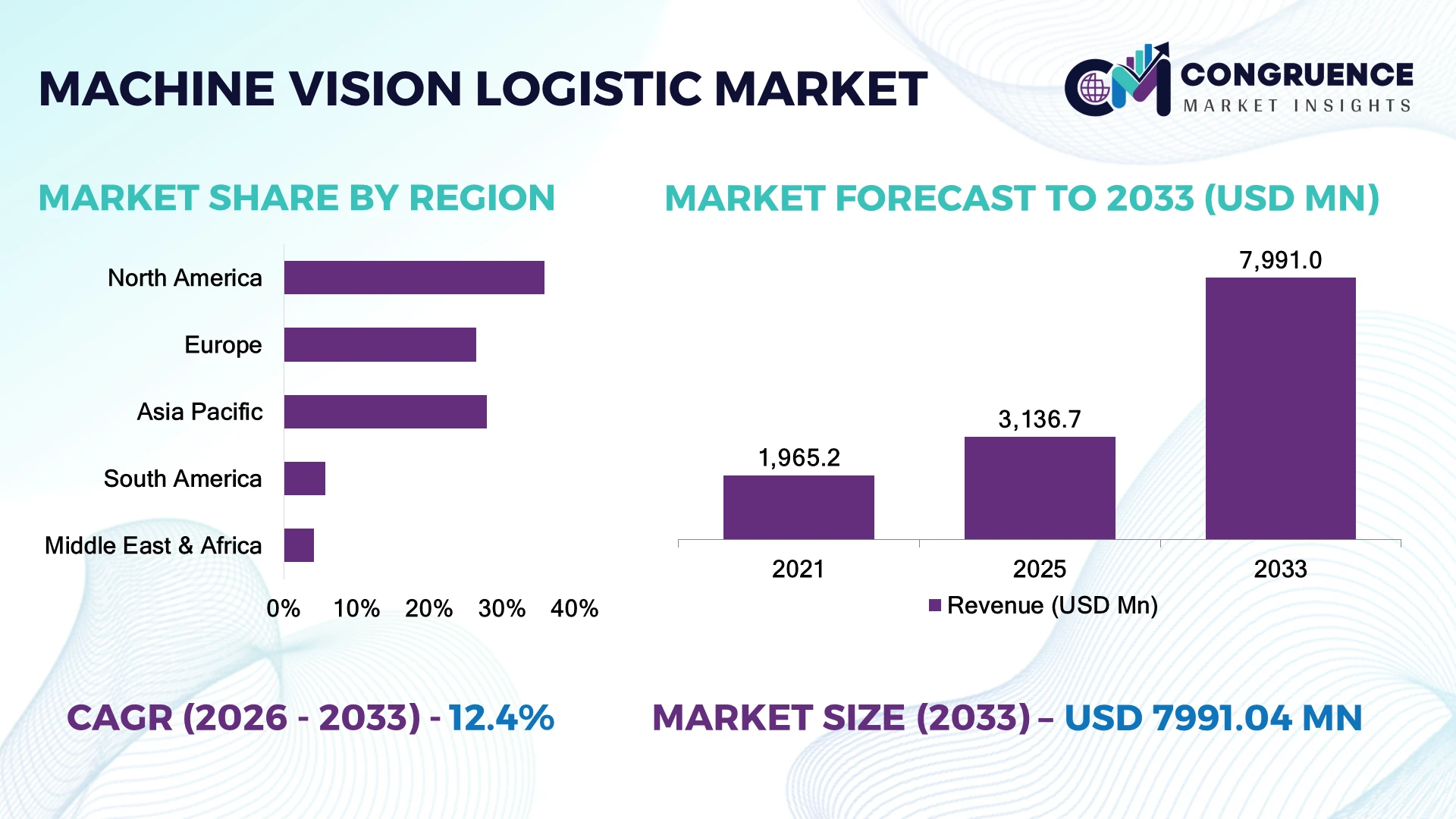

The Global Machine Vision Logistic Market was valued at USD 3,136.7 Million in 2025 and is anticipated to reach a value of USD 7,991.0 Million by 2033 expanding at a CAGR of 12.4% between 2026 and 2033. Rising warehouse automation, AI-powered inspection systems, and intelligent supply-chain optimization are accelerating machine vision deployment across logistics operations.

The United States dominated the Machine Vision Logistic Market with nearly 34% share in 2025, supported by large-scale automation investments, e-commerce fulfillment expansion, and advanced warehouse robotics adoption. Over 58% of major logistics facilities in the U.S. have integrated AI-based vision systems, compared with approximately 42% adoption across China’s automated warehouse networks. Supply-chain restructuring following global trade realignments has further increased demand for real-time visibility and automated quality control.

Companies adopting machine vision logistics platforms are gaining operational advantages through faster processing, reduced errors, and improved supply-chain resilience.

• Market Size & Growth: The market reached USD 3,136.7 Million in 2025 and is projected at USD 7,991.0 Million by 2033 with 12.4% CAGR, driven by AI logistics automation.

• Top Growth Drivers: Warehouse automation increased 45%, AI inspection adoption rose 38%, and robotic logistics integration expanded 34% globally.

• Short-Term Forecast: By 2028, vision-enabled logistics platforms are expected to improve sorting efficiency by nearly 40%.

• Emerging Technologies: AI vision analytics, 3D imaging, and autonomous robotics are transforming warehouse intelligence and fulfillment operations.

• Regional Leaders: North America, Asia-Pacific, and Europe are projected to reach USD 2.7 Billion, USD 2.4 Billion, and USD 1.9 Billion respectively through automation expansion.

• Consumer/End-User Trends: E-commerce and logistics providers represent over 55% adoption due to high-volume processing requirements.

• Pilot/Case Example: In 2025, automated warehouse deployments improved package recognition accuracy by nearly 35% using AI vision platforms.

• Competitive Landscape: Leading players hold nearly 41% share, including Cognex, Keyence, Basler, and Zebra Technologies.

• Regulatory & ESG Impact: Automated inspection systems reduced logistics waste and processing errors by approximately 25%.

• Investment & Funding: Over USD 2 Billion investments focus on warehouse robotics, AI vision platforms, and smart logistics infrastructure.

• Innovation & Future Outlook: Next-generation vision systems are shifting logistics toward autonomous, predictive, and data-driven supply-chain ecosystems.

Machine Vision Logistic technologies are transforming warehouses, distribution centers, and fulfillment networks through automated recognition, inspection, and tracking capabilities. AI-powered cameras, smart sensors, and robotic vision platforms are improving logistics accuracy by nearly 35%. Labor shortages and supply-chain optimization priorities are accelerating adoption of intelligent visual automation systems worldwide.

The Machine Vision Logistic Market is becoming strategically important as enterprises modernize fulfillment networks, automate warehouse processes, and improve supply-chain intelligence. E-commerce growth, labor availability challenges, and rising demand for faster deliveries are shifting investments toward AI-enabled logistics infrastructure. Companies are deploying machine vision systems to enhance operational accuracy, inventory visibility, and automated decision-making.

Compared with traditional barcode-based and manual inspection processes, advanced machine vision platforms improve detection accuracy by nearly 40% and reduce processing errors by approximately 30%. The United States leads through large-scale warehouse automation and AI adoption, while China is expanding rapidly through robotics manufacturing, smart logistics hubs, and automated fulfillment infrastructure.

Logistics providers are integrating vision systems into sorting lines, autonomous mobile robots, and quality inspection workflows to increase throughput. Companies are prioritizing AI model development, sensor innovation, and automation partnerships. Long-term competitiveness will depend on creating intelligent logistics ecosystems that combine visual intelligence, robotics, and real-time operational analytics.

Increasing demand for automated logistics operations is accelerating machine vision adoption across warehouses, distribution centers, and fulfillment facilities. Nearly 50% of advanced logistics operators are implementing AI-enabled vision technologies to improve sorting accuracy, inventory tracking, and workflow efficiency. Automated inspection systems reduce manual processing errors by approximately 35%, supporting faster order fulfillment. Large-scale e-commerce expansion in the United States and China is increasing investment in intelligent warehouse infrastructure. Companies are responding through AI algorithm development, robotics partnerships, and integrated vision platforms designed for high-volume logistics environments.

High implementation costs and compatibility issues with older logistics infrastructure remain key barriers for machine vision adoption. Advanced vision systems can require 25–40% higher upfront investment due to specialized cameras, AI software, sensors, and system integration requirements. Nearly 30% of traditional warehouse operators face challenges connecting automated vision platforms with existing management systems. Supply-chain constraints affecting advanced imaging components also influence deployment timelines. Companies are reducing risks through modular automation solutions, scalable software platforms, and partnerships that simplify integration across diverse logistics environments.

Expansion of autonomous warehouses and intelligent supply chains is creating major opportunities for machine vision logistics solutions. Nearly 45% of future-ready logistics facilities are increasing investments in robotic vision, automated identification, and AI-based decision systems. 3D imaging, edge AI processing, and autonomous mobile robots are enabling faster object recognition and operational optimization. Countries such as Japan and South Korea are advancing smart logistics infrastructure through automation-focused investments. Companies are strengthening capabilities through R&D expansion, AI partnerships, and end-to-end automation ecosystems.

Scaling machine vision logistics requires overcoming challenges related to data processing, system accuracy, and real-world operating variability. Nearly 35% of AI automation projects face optimization challenges due to changing package formats, lighting conditions, and warehouse layouts. Vision systems require continuous model training, cybersecurity protection, and integration with enterprise platforms. Logistics companies managing global operations need consistent performance across diverse facilities. Technology providers must invest in adaptive AI models, edge computing capabilities, and stronger implementation frameworks to deliver reliable automation performance at scale.

• AI Vision-Based Sorting Systems: Logistics companies are deploying AI-enabled vision platforms to automate parcel identification, sorting, and inspection workflows. Nearly 48% of advanced fulfillment centers are integrating intelligent imaging technologies, improving processing accuracy by around 35%. Companies are scaling robotic automation and software partnerships to address labor shortages and rising delivery expectations.

• 3D Imaging Technology Adoption: Advanced logistics facilities are shifting from traditional scanning methods toward 3D vision and depth-sensing technologies. More than 35% of automated warehouses are adopting enhanced imaging solutions for improved object recognition. Providers are developing compact sensors and AI-driven platforms to increase flexibility across dynamic warehouse environments.

• Vision-Guided Robotics Expansion: Autonomous robots are increasingly using machine vision for navigation, picking, and inventory handling. Around 42% of smart warehouse projects include vision-enabled robotic systems to improve operational speed and accuracy. Companies are expanding robotics integration strategies to optimize fulfillment capacity and reduce manual intervention.

• Edge AI Processing Integration: Logistics operators are adopting edge-based vision processing to reduce latency and improve real-time decision-making. Nearly 30% of new automation deployments include localized AI processing capabilities. Technology companies are investing in embedded computing platforms and intelligent cameras to support faster, scalable warehouse operations.

AI-based machine vision systems dominate the Machine Vision Logistic Market due to their advanced recognition accuracy, scalability, and seamless integration with automated warehouse ecosystems. AI vision platforms account for nearly 47% of deployments, supported by real-time image processing, predictive analytics, and compatibility with robotics and warehouse management systems. 3D vision systems are witnessing the fastest adoption growth as logistics operators increase investments in depth analysis, automated picking, and complex object recognition.

2D vision systems, smart cameras, and vision sensors continue supporting barcode verification, package inspection, sorting, and tracking operations across established logistics environments. Nearly 38% of automated facilities are shifting toward hybrid vision architectures combining AI software, intelligent cameras, and robotic automation. Companies are expanding through advanced imaging innovation, edge AI integration, and partnerships with automation providers to improve processing speed, accuracy, and deployment flexibility.

A 2025 warehouse automation industry assessment highlighted that logistics facilities using AI-enabled vision technologies improved automated identification accuracy by more than 35%, supporting faster fulfillment operations and reduced manual inspection dependency.

Sorting and inspection applications represent the leading segment in the Machine Vision Logistic Market due to extensive adoption across warehouses, fulfillment centers, and parcel distribution networks. The segment accounts for nearly 40% of deployments as companies prioritize faster package identification, defect detection, and automated workflow management. Inventory management applications are experiencing the fastest expansion as enterprises adopt vision-based tracking systems to improve stock visibility and reduce operational errors.

Order picking, robotic guidance, quality control, barcode recognition, and shipment verification applications continue expanding as logistics providers transition toward connected automation. Nearly 45% of advanced warehouse operators are deploying vision-enabled systems to improve throughput and reduce manual processing requirements. Companies are scaling AI algorithms, robotic integration, and cloud-connected platforms to optimize fulfillment accuracy and operational efficiency.

A 2026 logistics technology survey reported that distribution centers implementing machine vision-based automation improved processing efficiency by nearly 32%, strengthening adoption across high-volume fulfillment and supply-chain operations.

E-commerce and logistics companies represent the dominant end-user group in the Machine Vision Logistic Market due to high shipment volumes, rapid fulfillment requirements, and increasing dependence on automated warehouse operations. This segment accounts for approximately 52% of demand as enterprises deploy vision systems for sorting, tracking, inventory management, and quality verification. Retail companies are emerging as the fastest-growing end-user group, supported by omnichannel fulfillment expansion and automated supply-chain transformation.

Manufacturing companies, third-party logistics providers, transportation operators, and warehouse service providers continue adopting machine vision solutions to enhance operational transparency and reduce process inefficiencies. Around 40% of enterprise users are increasing investments in AI-driven visual automation to improve accuracy and scalability. Technology providers are targeting these segments through customized solutions, automation partnerships, and integrated logistics intelligence platforms.

A 2025 enterprise supply-chain automation study indicated that organizations adopting machine vision logistics platforms achieved nearly 30% improvement in fulfillment accuracy, accelerating investment in intelligent warehouse and distribution technologies.

North America accounted for the largest market share at 35.8% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 13.7% between 2026 and 2033.

North America leads the Machine Vision Logistic Market due to rapid adoption of automated warehouses, AI-enabled supply-chain platforms, and advanced fulfillment technologies. The region accounted for 35.8% market share in 2025, supported by large-scale deployment across e-commerce, retail distribution, and third-party logistics networks. More than 60% of major fulfillment centers are integrating machine vision systems for automated sorting, package verification, and inventory monitoring. Logistics operators are expanding investments in AI cameras, robotics integration, and edge-based vision processing to improve operational accuracy, reduce labor dependency, and accelerate delivery performance across high-volume supply chains.

United States Market Outlook: The United States dominates regional adoption through its advanced e-commerce infrastructure, robotics ecosystem, and large automated distribution networks. Companies are deploying machine vision platforms across fulfillment centers, parcel operations, and warehouse automation projects. Nearly 65% of large logistics operators are increasing investments in AI-based visual recognition systems to improve sorting accuracy, inventory visibility, and operational scalability.

Europe’s Machine Vision Logistic Market is driven by warehouse digitization, sustainable logistics initiatives, and Industry 4.0 adoption across supply-chain operations. The region accounted for nearly 26.4% market share in 2025, with Germany, France, and the United Kingdom leading deployments across automated warehouses and industrial logistics networks. Nearly 45% of advanced logistics facilities are adopting machine vision solutions for inspection, tracking, and robotic automation. Companies are focusing on AI-powered quality control, energy-efficient automation systems, and integrated logistics platforms to improve productivity while supporting evolving operational requirements.

Germany Market Outlook: Germany represents the strongest European market due to its advanced manufacturing base, automation expertise, and smart logistics infrastructure. Industrial and logistics enterprises are integrating vision-guided robotics, automated inspection, and intelligent warehouse systems. Around 50% of large-scale industrial automation projects include advanced sensing and machine vision technologies to strengthen production logistics and operational efficiency.

Asia-Pacific is experiencing accelerated machine vision logistics adoption due to expanding e-commerce networks, manufacturing automation, and smart supply-chain infrastructure. The region accounted for approximately 27.9% market share in 2025, supported by China, Japan, South Korea, and India’s investment in intelligent logistics systems. More than 55% of new automated warehouse projects across major technology hubs are incorporating vision-enabled inspection, tracking, and robotic systems. Companies are strengthening local manufacturing capabilities, AI software development, and automation partnerships to support increasing demand for high-speed logistics operations.

China Market Outlook: China leads Asia-Pacific demand through large-scale e-commerce operations, robotics manufacturing strength, and rapid warehouse automation adoption. Domestic logistics providers are deploying AI vision systems for parcel recognition, sorting, and inventory management. More than 60% of advanced fulfillment facilities are integrating automation technologies, supporting wider implementation of machine vision across supply-chain networks.

South America’s Machine Vision Logistic Market is expanding through increasing adoption of automated supply-chain solutions across retail, manufacturing, and distribution operations. The region accounted for nearly 5.7% market share in 2025, with demand concentrated among large logistics operators and e-commerce platforms. Around 28% of modern warehouse facilities are implementing machine vision technologies to improve shipment accuracy and reduce manual handling challenges. Infrastructure limitations and slower automation maturity influence deployment pace, while technology providers are expanding scalable solutions and partnerships to support regional transformation.

Brazil Market Outlook: Brazil represents the leading regional market due to its growing e-commerce sector, expanding distribution infrastructure, and industrial modernization initiatives. Logistics companies are investing in automated sorting, warehouse management systems, and AI-powered monitoring solutions. Nearly 35% of major fulfillment operators are adopting digital automation technologies to enhance delivery efficiency and inventory control.

Middle East & Africa adoption is supported by smart city initiatives, logistics hub development, and investments in advanced supply-chain technologies. The region accounted for nearly 4.2% market share in 2025, with demand concentrated across airports, retail distribution, and industrial logistics facilities. More than 30% of new logistics modernization projects are integrating automation solutions, including machine vision-based tracking and inspection platforms. Companies are expanding partnerships with automation providers and deploying scalable technologies to improve warehouse efficiency and regional trade capabilities.

United Arab Emirates Market Outlook: The United Arab Emirates leads regional adoption through logistics innovation, smart infrastructure programs, and its position as a global trade hub. Enterprises are deploying machine vision technologies across warehouses, ports, and automated distribution facilities. Over 40% of major digital logistics initiatives include AI-driven systems, supporting improved operational visibility and supply-chain intelligence.

The Machine Vision Logistic Market is led by Cognex, Keyence, Zebra Technologies, Basler, and Omron, where global automation technology providers compete with imaging specialists and AI-based vision innovators. The top five players collectively hold approximately 41% share, reflecting a technology-focused structure driven by accuracy and automation capability. Competition is based on AI performance, processing speed, system integration, and customization, with advanced vision platforms improving recognition accuracy by nearly 35% and increasing logistics throughput by around 30%. Companies are competing through AI algorithm development, smart camera innovation, robotics partnerships, and expansion of integrated warehouse automation solutions. The competitive shift is moving toward edge AI vision systems, autonomous fulfillment platforms, and software-driven logistics intelligence. High technical expertise, AI training requirements, and integration complexity create strong barriers for emerging players. Winning against established providers requires superior vision accuracy, scalable automation ecosystems, and faster deployment capabilities.

• Cognex Corporation

• Keyence Corporation

• Zebra Technologies Corporation

• Basler AG

• Omron Corporation

• Teledyne Technologies Incorporated

• Sick AG

• Datalogic S.p.A.

• Balluff GmbH

• Baumer Holding AG

• ISRA Vision GmbH

• Advantech Co., Ltd.

• National Instruments Corporation

• Sony Semiconductor Solutions Corporation

Machine vision logistics technologies are advancing through AI-powered image recognition, 3D vision systems, smart cameras, edge computing, and vision-guided robotics. AI-based vision platforms are improving automated sorting, inspection, and inventory tracking capabilities, with nearly 50% of advanced warehouse automation deployments integrating intelligent imaging technologies for real-time operational decisions.

Compared with conventional barcode scanning and manual inspection systems, next-generation machine vision platforms improve recognition accuracy by approximately 40% and reduce processing errors by nearly 30% through deep learning, sensor fusion, and automated analytics. Edge AI-enabled cameras reduce data processing delays by around 25%, supporting faster logistics workflows. E-commerce companies, automation providers, and third-party logistics operators gain competitive advantages through higher throughput, better inventory visibility, and reduced operational dependency.

Between 2026 and 2028, technology advancement will focus on autonomous vision systems, adaptive AI models, and fully connected robotic fulfillment networks. Organizations investing in intelligent machine vision infrastructure will strengthen scalability, supply-chain resilience, and operational efficiency in increasingly automated logistics environments.

April 2025 – Cognex launched expanded AI-enabled machine vision capabilities to improve industrial automation performance, increasing inspection accuracy by nearly 30% across high-speed applications. The advancement strengthened automated logistics, manufacturing inspection, and smart warehouse deployment opportunities. Source: cognex.com

November 2024 – Zebra Technologies enhanced its machine vision and fixed industrial scanning portfolio with advanced automation features, improving workflow productivity by approximately 25%. The expansion supported intelligent warehouse operations, automated identification, and supply-chain visibility improvements. Source: zebra.com

February 2025 – Basler expanded its industrial vision portfolio with improved camera technology and embedded vision solutions, supporting faster image processing and increasing automation performance by nearly 20%. The development strengthened adoption across logistics robotics and automated inspection systems. Source: baslerweb.com

June 2024 – Omron advanced its automation technology ecosystem through enhanced machine vision integration for industrial and logistics environments, improving inspection speed and operational consistency by approximately 25%. The initiative supported broader adoption of intelligent automation platforms. Source: automation.omron.com

The Machine Vision Logistic Market Report provides comprehensive analysis across technologies, applications, end-users, regional trends, and competitive strategies shaping intelligent supply-chain automation. The study covers AI-based vision systems, 2D and 3D vision platforms, smart cameras, sensors, and integrated automation solutions used across sorting, inspection, inventory management, robotic guidance, and quality monitoring. More than 55% of deployments are concentrated across e-commerce, logistics, and automated warehouse environments.

The report evaluates North America, Europe, Asia-Pacific, South America, and Middle East & Africa with insights into adoption patterns, technology evolution, and enterprise investment strategies. It examines AI vision analytics, edge computing, robotic integration, and future automation opportunities between 2026 and 2033. The analysis supports strategic planning, competitive positioning, technology selection, and expansion decisions across the evolving logistics automation ecosystem.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 3,136.7 Million |

|

Market Revenue in 2033 |

USD 7,991.0 Million |

|

CAGR (2026 - 2033) |

12.4% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Cognex Corporation, Keyence Corporation, Zebra Technologies Corporation, Basler AG, Omron Corporation, Teledyne Technologies Incorporated, Sick AG, Datalogic S.p.A., Balluff GmbH, Baumer Holding AG, ISRA Vision GmbH, Advantech Co., Ltd., National Instruments Corporation, Sony Semiconductor Solutions Corporation |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |