Reports

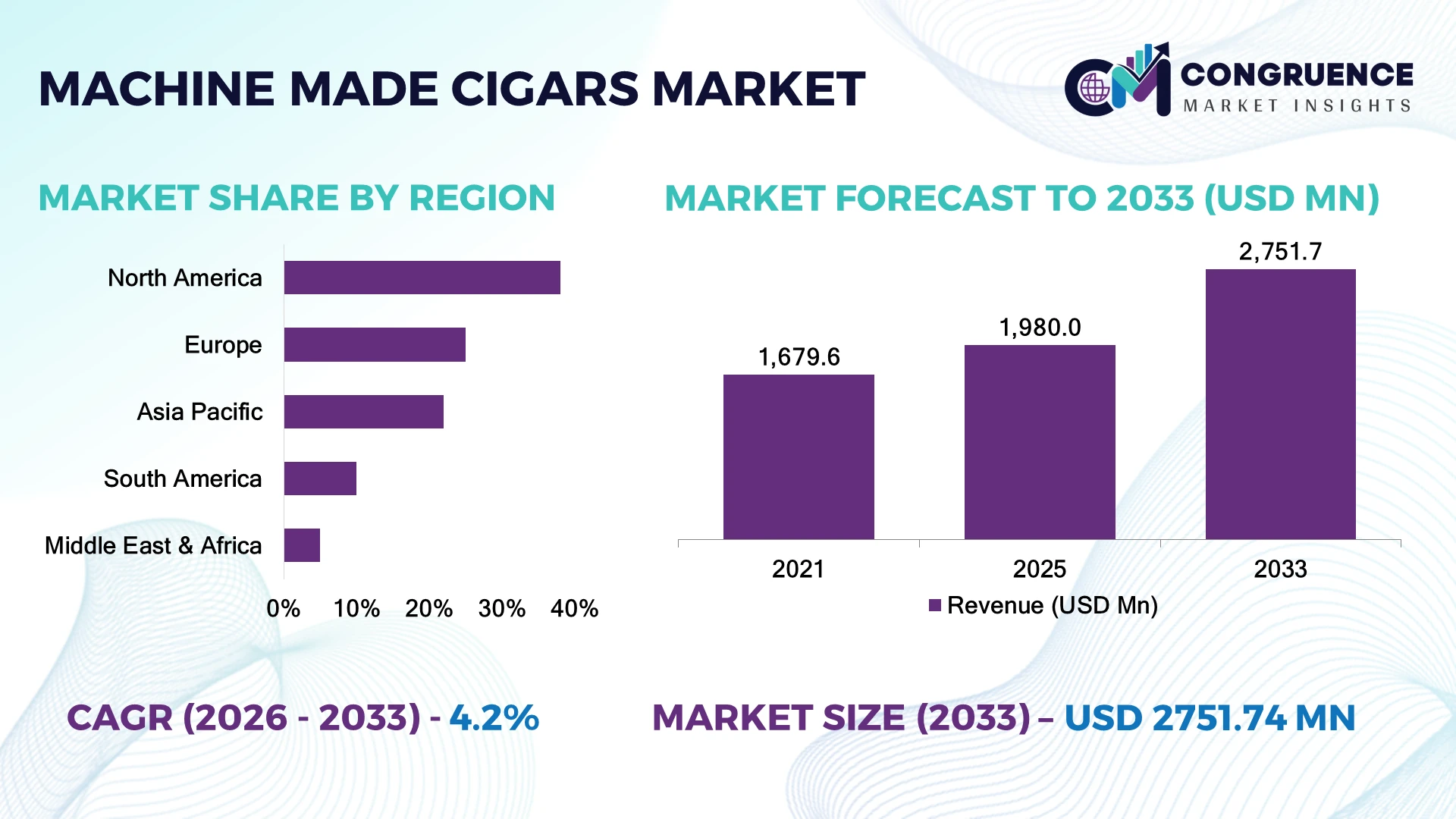

The Global Machine Made Cigars Market was valued at USD 1,980.0 Million in 2025 and is anticipated to reach a value of USD 2,751.7 Million by 2033 expanding at a CAGR of 4.2% between 2026 and 2033. Growth is driven by automated cigar manufacturing lines, rising demand for affordable tobacco formats, premiumized machine-made blends, and advanced packaging innovations improving consistency and shelf stability.

The United States dominates the machine made cigars landscape with approximately 35% market share, supported by large-scale tobacco processing infrastructure, strong domestic distribution networks, and manufacturers investing in automated production facilities. The country processes millions of cigar units annually, while Europe maintains a strong regulatory-driven market with stricter tobacco standards. Compared with emerging Asian markets, North America shows over 60% higher adoption of automated cigar production systems, reflecting mature manufacturing capabilities.

Companies are prioritizing automation, compliance, and regional supply-chain resilience to strengthen long-term competitiveness.

Market Size & Growth: USD 1.98 Billion market in 2025 reaching USD 2.75 Billion by 2033 at 4.2% CAGR, driven by automated manufacturing and cost-efficient production models.

Top Growth Drivers: Automation adoption (35%), premium machine-made blends (28%), and expanding emerging-market consumption (22%) are key growth catalysts.

Short-Term Forecast: By 2028, automated production efficiency improves by 15% with reduced labor dependency and optimized material usage.

Emerging Technologies: AI-based quality inspection, robotic packaging systems, and digital supply-chain tracking are reshaping advanced cigar manufacturing.

Regional Leaders: North America projected at USD 1.0 Billion, Europe at USD 0.8 Billion, and Asia-Pacific at USD 0.6 Billion, supported by automation, premiumization, and expanding distribution channels.

Consumer/End-User Trends: Over 40% of younger adult tobacco consumers prefer convenient packaged cigar formats with consistent quality attributes.

Pilot/Case Example: In 2024, automated tobacco production upgrades reduced manufacturing defects by approximately 20% through precision monitoring systems.

Competitive Landscape: Imperial Brands leads with an estimated 15% share, alongside Scandinavian Tobacco Group, Swedish Match, J.C. Newman, and Altria Group.

Regulatory & ESG Impact: Tobacco manufacturing compliance programs have increased traceability adoption by over 30% across major production facilities.

Investment & Funding: More than USD 500 Million directed toward manufacturing upgrades, automation expansion, and strategic partnerships across tobacco supply chains.

Innovation & Future Outlook: Next-generation production will focus on smart factories, sustainable packaging materials, and data-driven manufacturing optimization.

Machine made cigars are gaining strategic importance as manufacturers focus on production efficiency, product consistency, and diversified consumer preferences. Demand is expanding across convenience retail, duty-free channels, and emerging markets where affordable cigar formats remain attractive. Recent innovations include precision rolling technology, improved filtration systems, and recyclable packaging solutions, with approximately 30% of large producers adopting upgraded manufacturing processes. Global supply-chain adjustments following geopolitical disruptions have encouraged regional sourcing strategies and localized production investments, creating a stronger foundation for future industry transformation.

The Machine Made Cigars Market is becoming strategically important as manufacturers compete through automation, production scalability, and differentiated product development. Companies are restructuring supply chains, expanding regional manufacturing hubs, and adopting digital monitoring systems to improve operational control amid evolving tobacco regulations and shifting consumer preferences.

Advanced automated cigar production lines deliver measurable advantages compared with traditional manufacturing methods, improving production consistency by nearly 20% while reducing manual handling requirements. North America continues to lead through mature tobacco infrastructure and established distribution networks, whereas Asia-Pacific markets are gaining attention through expanding retail penetration and increasing manufacturing investments.

Manufacturers are deploying smart inspection systems, automated wrapping equipment, and integrated inventory platforms to strengthen efficiency. For example, large producers are upgrading facilities with robotics-based packaging operations to reduce downtime and improve throughput. Over the next few years, companies are prioritizing partnerships, technology upgrades, and compliance-focused investments to maintain market positioning. The strongest competitive advantage will come from balancing manufacturing efficiency, regulatory readiness, and product innovation across global markets.

The shift toward automated cigar production is accelerating as manufacturers prioritize consistency, speed, and cost control. Modern machine-based manufacturing lines improve output efficiency by nearly 20–30% compared with traditional manual processes, while automated quality inspection reduces production defects by approximately 15%. In the United States and Dominican Republic, producers are investing in high-speed rolling, wrapping, and packaging systems to address labor constraints and maintain product uniformity. Rising adoption of digital monitoring technologies is enabling real-time production optimization. Companies are responding through facility upgrades, equipment partnerships, and process innovation, creating a more scalable manufacturing ecosystem with stronger operational margins.

Strict tobacco regulations and raw material dependency continue to limit operational flexibility for machine made cigar producers. Compliance requirements in markets such as the United States and European Union have increased documentation and testing processes by nearly 25%, raising administrative costs. Tobacco leaf price volatility, driven by weather disruptions and agricultural constraints, affects production planning, with raw material costs fluctuating by approximately 10–15% annually. Packaging restrictions and evolving sustainability standards further pressure manufacturers. Companies are reducing exposure through supplier diversification, localized sourcing agreements, and long-term contracts with tobacco growers to stabilize procurement and protect profitability.

Machine made cigar manufacturers are finding new opportunities through smart factory adoption, premium product innovation, and expanding distribution channels in developing markets. Advanced automation platforms can improve production efficiency by 25%, while digital inventory systems reduce material waste by nearly 15%. Countries such as India, Vietnam, and Brazil are attracting attention due to expanding retail networks and growing demand for affordable cigar formats. Manufacturers are exploring recyclable packaging, AI-based quality control, and customized product lines to capture evolving consumer preferences. Strategic partnerships with technology providers and regional distributors are becoming a key pathway for improving market penetration and operational agility.

Long-term competitiveness depends on overcoming manufacturing complexity, workforce transitions, and evolving regulatory expectations. Around 30% of tobacco manufacturers globally are upgrading production systems, but integration of advanced machinery requires skilled technical personnel and significant process adjustments. Automation maintenance requirements and cybersecurity concerns are increasing as factories adopt connected equipment and digital controls. In countries such as Germany and the United States, compliance-driven production changes require continuous system upgrades and workforce training. Companies must strengthen technology capabilities, invest in employee expertise, and develop resilient production networks to maintain consistent output quality and competitive positioning.

Smart Factory Adoption Accelerates Manufacturers are integrating automated rolling, wrapping, and inspection systems to improve production consistency, with advanced facilities reporting 15–25% efficiency gains after equipment upgrades. U.S. and European producers are replacing fragmented workflows with connected manufacturing platforms to reduce downtime and improve quality control. Labor availability pressures and rising operational costs are accelerating robotics adoption, while companies are expanding automation partnerships to strengthen production reliability.

Premiumization Through Process Innovation Machine made cigar producers are investing in improved tobacco blends, flavor consistency, and upgraded packaging formats as premium segments capture increasing consumer attention. Approximately 30% of product launches now emphasize enhanced presentation or differentiated formulations. Companies are using precision manufacturing technologies to replicate premium characteristics at scale, creating new value opportunities without significantly increasing production complexity.

Supply Chain Localization Expands Global supply disruptions and stricter compliance requirements are encouraging manufacturers to diversify tobacco sourcing and strengthen regional supplier networks. More than 20% of large producers have increased supplier diversification efforts to reduce dependency risks. Companies are developing closer relationships with growers and packaging suppliers to improve inventory stability and respond faster to market fluctuations.

Digital Quality Control Integration AI-assisted inspection and data analytics are becoming important tools for reducing defects and improving traceability. Automated monitoring systems can lower quality-related losses by around 15%, helping manufacturers meet stricter production standards. Companies are scaling digital infrastructure to support predictive maintenance, regulatory reporting, and more efficient factory operations.

Machine made cigars are primarily segmented into filtered cigars, little cigars, and cigarillos, with cigarillos representing the leading type segment with approximately 45% market share due to their balance of affordability, convenience, and mass-market availability. Their compact format, faster consumption time, and compatibility with automated production systems have strengthened adoption across the United States and European markets. Filtered cigars account for nearly 30% of demand, supported by consumer preference for standardized formats and improved packaging designs, while little cigars maintain relevance through value-focused consumption patterns. Cigarillos are also emerging as the fastest-growing type segment, supported by premium flavor innovation and expanded retail availability, with adoption increasing by around 8–10% in selected developed markets. Manufacturers are investing in advanced blending technologies, packaging improvements, and product diversification to capture shifting consumer preferences. The strategic focus is moving toward scalable formats that combine production efficiency with differentiated consumer experiences.

The retail application segment dominates the machine made cigars market, accounting for approximately 60% share, driven by strong availability through convenience stores, specialty tobacco outlets, supermarkets, and duty-free channels. The segment benefits from established distribution networks in countries such as the United States, Germany, and Spain, where packaged cigar products maintain broad consumer accessibility. Online and specialty tobacco platforms represent around 20% of application demand and are expanding as digital commerce improves product discovery and purchasing convenience. Hospitality and premium entertainment applications are emerging growth areas as lounges, clubs, and tourism-linked businesses increasingly include cigar products within customer experiences. Adoption in these channels is rising by approximately 10%, supported by premium packaging and curated product offerings. Companies are strengthening partnerships with distributors, expanding retail presence, and improving digital engagement strategies to capture evolving purchasing behavior.

Individual consumers represent the largest end-user segment with approximately 70% market share, supported by widespread availability, affordable pricing, and established consumption habits in countries such as the United States, Brazil, and the Dominican Republic. Consumer-focused machine made cigars benefit from automated production advantages that enable consistent quality and competitive pricing. Commercial hospitality businesses account for nearly 20% of demand, with cigar lounges, resorts, and entertainment venues adopting diversified product portfolios to attract premium customers. The fastest-growing end-user segment is hospitality and specialty establishments, expanding at an estimated 8–12% pace as experiential tobacco consumption gains importance. Manufacturers are responding through customized product ranges, distributor partnerships, and premium packaging strategies designed for specific customer groups. Institutional and specialty buyers are also increasing interest in reliable supply agreements, creating opportunities for producers to develop stronger business-to-business relationships.

North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 5.1% between 2026 and 2033.

North America remains the dominant machine made cigars market, supported by large-scale manufacturing capacity, established tobacco distribution channels, and strong consumer accessibility. The region contributes approximately 38% of global demand, with the United States representing the largest production and consumption base. Manufacturers are increasingly adopting automated rolling, packaging, and quality inspection systems, with advanced facilities achieving around 20% improvement in production efficiency. Regulatory compliance requirements and labor cost pressures are encouraging companies to modernize operations. Strategic partnerships between manufacturers and distributors are strengthening retail penetration, while premium machine-made formats continue gaining traction across convenience and specialty tobacco channels.

United States Market Outlook: The United States is the key market contributor due to its mature tobacco manufacturing ecosystem and extensive retail infrastructure. The country accounts for nearly 35% of global machine made cigar consumption, supported by thousands of convenience retail outlets and advanced production facilities. U.S. manufacturers are investing in automation, traceability systems, and product diversification to maintain operational efficiency and regulatory readiness.

Europe represents a mature machine made cigars market characterized by strict regulatory frameworks, established tobacco traditions, and increasing focus on product quality management. The region contributes approximately 25% of global market demand, with Germany, Spain, and Italy acting as important consumption and distribution centers. Manufacturers are upgrading packaging technologies and production monitoring systems to comply with evolving tobacco control requirements. Sustainability initiatives and supply-chain transparency programs are influencing operational strategies, with more than 25% of major producers strengthening traceability processes. Companies are focusing on premium blends, efficient manufacturing workflows, and compliant product innovation to maintain competitiveness.

Germany Market Outlook: Germany remains one of Europe’s most strategically important markets due to its strong retail network, industrial capabilities, and regulatory influence. The country represents nearly 8% of European machine made cigar demand, supported by specialty tobacco retailers and efficient distribution infrastructure. Manufacturers are prioritizing automated production systems and compliance-focused investments to improve operational resilience.

Asia-Pacific is becoming a high-growth market for machine made cigars due to expanding tobacco processing capabilities, rising urban consumption, and improving retail infrastructure. The region contributes around 22% of global demand, with China, Japan, and India emerging as important markets. Manufacturers are increasing investments in automated production lines and regional supply networks to improve cost efficiency. Production facilities in developing markets are adopting digital quality monitoring systems, improving manufacturing accuracy by approximately 15%. Companies are also exploring partnerships with local distributors to strengthen market access and respond to changing consumer preferences across emerging economies.

China Market Outlook: China holds the strongest position in Asia-Pacific due to its large-scale tobacco manufacturing infrastructure and extensive domestic distribution network. The country accounts for more than 40% of regional machine made cigar consumption. Manufacturers are focusing on production modernization, automated packaging solutions, and supply-chain integration to improve efficiency and support expanding premium product categories.

South America benefits from strong tobacco cultivation expertise, established processing infrastructure, and export-oriented manufacturing capabilities. The region contributes approximately 10% of global machine made cigar demand, with Brazil playing a central role in production and supply-chain activity. Manufacturers are improving processing efficiency through upgraded equipment and quality-control systems, with some facilities achieving 15% higher operational productivity after modernization. However, infrastructure differences and logistics complexity continue influencing expansion strategies. Companies are strengthening farmer partnerships, improving local processing capabilities, and developing export-focused production models to enhance competitiveness.

Brazil Market Outlook: Brazil is the leading South American market due to its extensive tobacco agriculture base and established processing industry. The country contributes nearly 60% of regional tobacco production capacity and supports machine made cigar manufacturing through integrated supply networks. Producers are investing in advanced processing technologies and export partnerships to improve efficiency and strengthen global positioning.

The Middle East & Africa market is evolving through expanding hospitality channels, premium tobacco consumption, and improved import distribution systems. The region accounts for approximately 5% of global machine made cigar demand, with the United Arab Emirates and South Africa acting as key commercial hubs. Duty-free retail expansion and luxury hospitality growth are supporting product availability, while companies are developing targeted distribution partnerships. Approximately 20% of regional tobacco product growth initiatives involve premium retail and hospitality-focused strategies. Manufacturers are improving supply reliability through regional partnerships and flexible inventory management systems.

United Arab Emirates Market Outlook: The United Arab Emirates represents the most strategically significant market due to its duty-free ecosystem, luxury hospitality sector, and international consumer base. Dubai’s aviation and tourism infrastructure supports strong premium tobacco distribution, with duty-free channels accounting for a significant portion of cigar sales. Companies are expanding partnerships with hospitality operators and specialized retailers to capture high-value consumer segments.

The Machine Made Cigars Market features competition between global tobacco manufacturers, regional cigar specialists, and vertically integrated producers. Key players include Scandinavian Tobacco Group, Imperial Brands, Altria, J.C. Newman, and Swedish Match, competing through scale, product innovation, and distribution strength. The top five companies collectively account for approximately 45% of market share, creating a moderately consolidated structure. Competition is driven by pricing efficiency, automated manufacturing, supply-chain control, and premium product customization, with automation improving production efficiency by 20–30% and packaging innovation reducing operational waste by nearly 15%. Leading companies are expanding through manufacturing upgrades, distributor partnerships, and portfolio diversification. Regional producers compete through cost advantages and localized sourcing, while global firms leverage technology and brand equity. Rising compliance requirements and capital-intensive production systems create entry barriers. Winning companies will require manufacturing agility, supply reliability, and continuous product innovation.

Imperial Brands PLC

Altria Group

Swedish Match

J.C. Newman Cigar Company

Arnold André GmbH & Co. KG

Dannemann

Agio Cigars

Habanos S.A.

Oettinger Davidoff AG

Gurkha Cigar Group

Villiger Group

Machine made cigar manufacturing is increasingly adopting automated rolling, wrapping, and packaging technologies to improve production consistency and reduce dependence on manual labor. Advanced automation systems deliver approximately 20% higher operational efficiency compared with conventional processes, while AI-based inspection tools reduce quality defects by nearly 15%. Large manufacturers benefit most by integrating smart factory platforms across production facilities.

Digital supply-chain monitoring and predictive maintenance are becoming important technologies for improving inventory visibility and reducing downtime. Connected manufacturing systems enable around 10–20% faster workflow optimization by identifying production bottlenecks. Companies with integrated data platforms gain competitive advantages through improved traceability, faster response cycles, and stronger regulatory compliance.

Between 2026 and 2028, robotics, AI quality control, and sustainable packaging technologies will reshape competitive positioning. New-generation production lines are expected to outperform older equipment through improved speed, precision, and resource utilization. Technology leaders will benefit through scalable manufacturing, while cost-focused producers will face pressure to modernize operations and maintain efficiency.

February 2025 Altria Group Investor Relations announced continued strategic investment across its tobacco portfolio, highlighting the performance of its smokeable products segment and John Middleton cigar business. Reported cigar shipment volume remained resilient, supporting portfolio optimization and strengthening U.S. cigar market positioning. Source: www.investor.altria.com

September 2025 Altria Group Investor Relations entered a memorandum of understanding with KT&G to pursue long-term growth opportunities, combining operational capabilities and product expertise. The partnership expands collaboration potential across tobacco innovation and efficiency initiatives, improving strategic flexibility. Source: www.investor.altria.com

October 2025 Imperial Brands PLC announced plans to withdraw from its Langenhagen manufacturing site in Germany as part of a global production network review. The decision affected 640 employees and reflected manufacturing consolidation efforts to improve capacity utilization. Source: www.imperialbrandsplc.com

March 2026 Scandinavian Tobacco Group continued implementing its strategic manufacturing approach focused on production efficiency and portfolio strength. The company emphasized investments in production and distribution capabilities to support value and premium cigar segments through improved availability and operational flexibility.

The Machine Made Cigars Market Report covers comprehensive analysis across product types, applications, end-users, and major geographic markets including North America, Europe, Asia-Pacific, South America, and Middle East & Africa. The study evaluates machine-made cigar categories, retail and hospitality applications, consumer segments, manufacturing structures, and evolving distribution channels shaping industry performance.

The report examines automation technologies, smart manufacturing systems, packaging innovations, supply-chain strategies, and competitive positioning among key industry participants. Coverage includes adoption trends, production modernization, regional expansion patterns, and emerging opportunities in premium and value-focused segments. The analysis supports investment planning, market entry decisions, partnership strategies, and long-term competitive positioning by identifying operational shifts and business priorities influencing the market through 2033.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 1,980.0 Million |

| Market Revenue (2033) | USD 2,751.7 Million |

| CAGR (2026–2033) | 4.2% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Companies Profiled | Scandinavian Tobacco Group; Imperial Brands PLC; Altria Group; Swedish Match; J.C. Newman Cigar Company; Arnold André GmbH & Co. KG; Dannemann; Agio Cigars; Habanos S.A.; Oettinger Davidoff AG; Gurkha Cigar Group; Villiger Group |

| Customization & Pricing | Available on Request (10% Customization Free) |