Reports

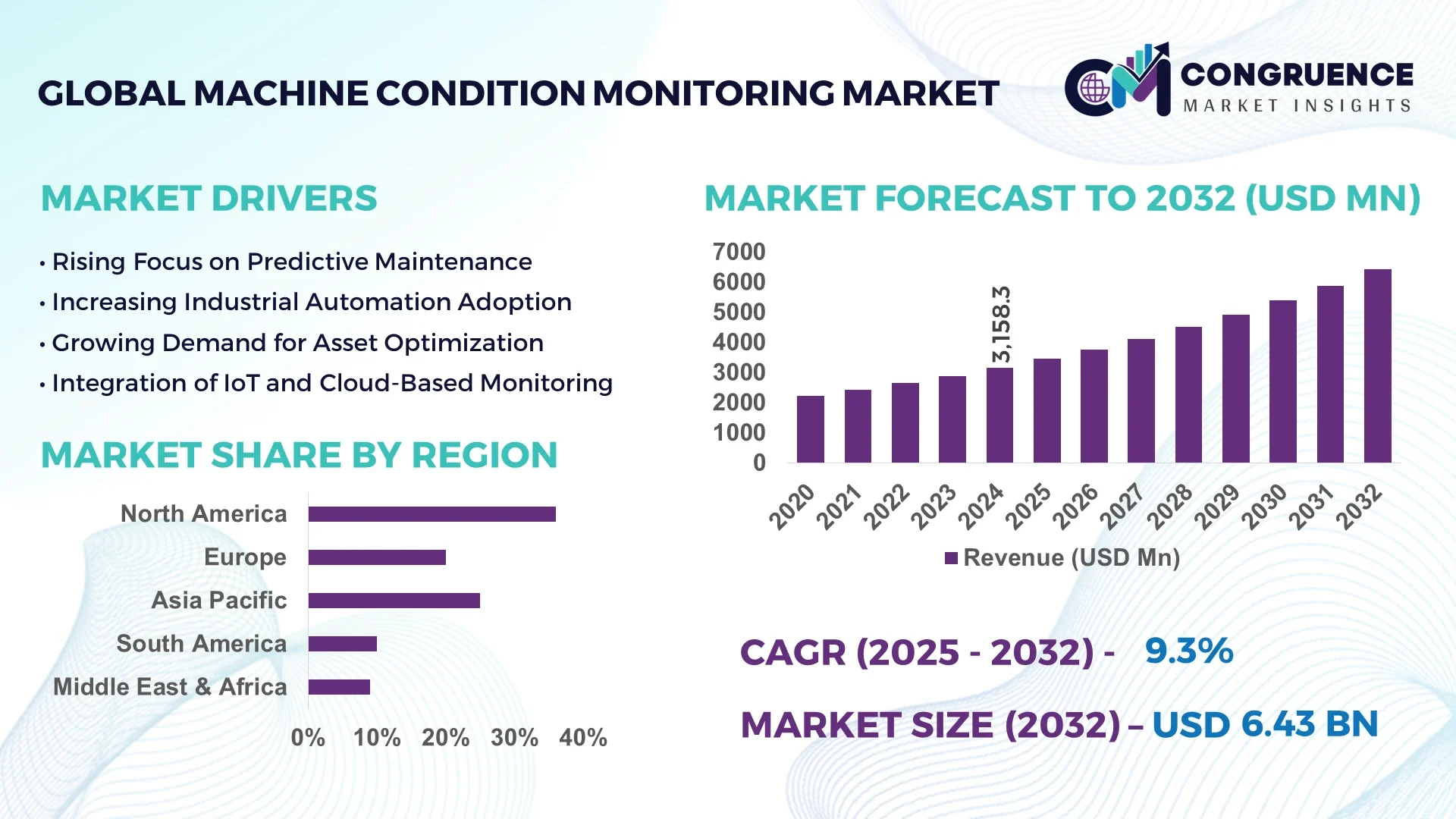

The Global Machine Condition Monitoring Market was valued at USD 3158.29 Million in 2024 and is anticipated to reach a value of USD 6433 Million by 2032 expanding at a CAGR of 9.3% between 2025 and 2032. This growth is primarily driven by increasing industrial automation and the rising need for predictive maintenance across manufacturing sectors.

The United States leads the Machine Condition Monitoring market, with extensive investments in advanced sensor technologies and IoT-integrated monitoring systems. The country has over 1,500 production facilities equipped with real-time condition monitoring tools, supporting key sectors such as aerospace, automotive, and energy generation. U.S. firms have allocated USD 750 Million in 2023 alone towards R&D for predictive analytics and vibration monitoring solutions. Industrial adoption rates indicate that more than 68% of medium to large-scale manufacturing units have implemented machine condition monitoring solutions, while technological advancements like AI-based anomaly detection and wireless sensor networks are driving efficiency and reducing unplanned downtime significantly.

Market Size & Growth: Current market valued at USD 3158.29 Million, projected to reach USD 6433 Million by 2032, driven by industrial automation and predictive maintenance adoption.

Top Growth Drivers: Predictive maintenance adoption 65%, IoT integration efficiency 58%, industrial downtime reduction 52%.

Short-Term Forecast: By 2028, average operational efficiency expected to improve by 27% and maintenance cost reduction of 18%.

Emerging Technologies: AI-driven anomaly detection, wireless sensor networks, cloud-based predictive analytics.

Regional Leaders: North America USD 2200 Million by 2032 with high adoption in aerospace; Europe USD 1850 Million with automotive sector expansion; Asia-Pacific USD 1400 Million with heavy industrial and energy sectors growth.

Consumer/End-User Trends: Manufacturing, power generation, and transportation sectors increasingly leverage predictive insights for asset longevity.

Pilot or Case Example: In 2023, a U.S. automotive plant implemented vibration monitoring sensors, achieving a 24% reduction in unplanned downtime.

Competitive Landscape: SKF (~15%), GE Digital, Emerson, Siemens, Rockwell Automation.

Regulatory & ESG Impact: Compliance with industrial safety standards, energy efficiency mandates, and sustainability-driven incentives encouraging technology adoption.

Investment & Funding Patterns: Over USD 1 Billion invested in machine monitoring R&D and smart maintenance projects globally in 2023–2024.

Innovation & Future Outlook: Integration of digital twins, AI-based predictive insights, and remote monitoring solutions expected to define next-generation condition monitoring.

The Machine Condition Monitoring market spans industrial sectors such as automotive, aerospace, power generation, and heavy machinery, contributing to more than 70% of global adoption. Recent innovations, including wireless vibration sensors, cloud-based analytics, and AI-powered predictive diagnostics, are enabling operational efficiency and reduced downtime. Regulatory frameworks focusing on industrial safety and environmental compliance further stimulate adoption. Emerging trends include edge computing-enabled real-time monitoring and hybrid AI-analytics platforms, while growing demand in Asia-Pacific and Europe reflects a shift toward fully integrated industrial IoT ecosystems.

The Machine Condition Monitoring Market plays a pivotal role in enhancing industrial resilience, operational efficiency, and predictive maintenance across global manufacturing ecosystems. AI-driven vibration analysis delivers a 23% improvement in fault detection compared to traditional threshold-based monitoring, enabling faster maintenance decision-making. North America dominates in volume, while Europe leads in adoption, with over 72% of enterprises integrating advanced condition monitoring solutions. By 2027, cloud-based predictive analytics is expected to improve unplanned downtime reduction by 19%, supporting leaner operational models. Firms are committing to ESG metrics improvements, such as a 15% reduction in energy consumption through optimized machine operations by 2026. In 2024, Siemens achieved a 21% reduction in maintenance-related production stoppages through the deployment of edge-based AI monitoring systems across its European facilities. Strategically, the Machine Condition Monitoring Market aligns with the transition toward Industry 4.0, integrating IoT, AI, and digital twins to optimize asset utilization, enhance safety, and ensure regulatory compliance. Forward-looking strategies emphasize technological convergence, energy-efficient operations, and predictive maintenance to drive sustainable growth, positioning the Machine Condition Monitoring Market as a cornerstone of industrial reliability and compliance in the evolving manufacturing landscape.

Rising industrial automation is significantly boosting the Machine Condition Monitoring Market by increasing the reliance on connected machinery and predictive maintenance systems. Over 60% of medium to large-scale manufacturing facilities now utilize real-time monitoring sensors, improving fault detection by up to 20% compared to manual inspection. Advanced automation workflows require precise operational insights, which machine condition monitoring provides through AI and IoT integration. Automotive, aerospace, and energy production sectors are increasingly implementing these systems to reduce unplanned downtime, optimize maintenance schedules, and extend asset life. Enhanced data analytics capabilities allow manufacturers to proactively respond to equipment anomalies, enhancing production efficiency by 18–22% and minimizing operational risks. This trend positions the Machine Condition Monitoring Market as a critical enabler of fully automated, high-efficiency industrial environments.

High implementation costs pose a significant restraint on the Machine Condition Monitoring Market, particularly for small and medium-sized enterprises. Advanced sensor networks, AI software integration, and cloud analytics platforms can require initial investments exceeding USD 100,000 per facility. Additionally, ongoing maintenance, calibration, and employee training contribute to operational expenditure. Firms in developing regions often face budgetary limitations, slowing adoption rates despite the demonstrated operational benefits. Integration with legacy machinery also presents technical challenges, as retrofitting older equipment may require specialized hardware and customized software solutions. These cost barriers limit market penetration in sectors with smaller margins, delaying the universal deployment of advanced condition monitoring systems and restricting the pace of technological adoption.

Predictive maintenance expansion presents significant opportunities for the Machine Condition Monitoring Market. The integration of AI-driven diagnostics and IoT-enabled sensors allows companies to anticipate equipment failures, potentially reducing unplanned downtime by 25% in the next two years. Emerging markets in Asia-Pacific and Latin America are increasingly investing in smart manufacturing facilities, creating untapped demand for machine monitoring solutions. Adoption of digital twin technology provides real-time simulation of machinery performance, enhancing operational decision-making and improving maintenance efficiency by 18%. Additionally, growing regulatory and ESG focus encourages companies to implement energy-efficient monitoring systems, presenting opportunities for technology providers to offer advanced, environmentally compliant solutions that improve sustainability metrics while driving industrial productivity.

Data security and regulatory compliance present significant challenges to the Machine Condition Monitoring Market. Real-time monitoring generates vast volumes of sensitive operational data, requiring robust cybersecurity measures to prevent breaches and ensure integrity. Regulatory compliance across regions adds complexity, as standards for industrial data privacy, safety, and environmental impact vary widely. In Europe, GDPR and industry-specific guidelines mandate strict data handling protocols, while Asia-Pacific and North America enforce operational safety standards. Additionally, the need to integrate monitoring systems with legacy machinery increases technical complexity and compliance risk. These challenges can result in delayed deployment, higher operational costs, and potential legal liabilities, creating barriers for widespread adoption of advanced monitoring solutions.

• Expansion of Predictive Maintenance Programs: Industries are increasingly adopting predictive maintenance protocols, with 62% of large manufacturing facilities implementing AI-based monitoring solutions to reduce unplanned downtime. Real-time vibration and temperature analytics have improved operational efficiency by 18% in the past two years, particularly in automotive and energy sectors. This trend reflects a shift from reactive to proactive maintenance, allowing firms to allocate resources more effectively and extend equipment lifespan.

• Integration of IoT and Wireless Sensor Networks: Over 70% of newly installed machine monitoring systems in North America and Europe now feature IoT-enabled wireless sensors. These networks enable continuous data collection and remote monitoring, resulting in a 21% reduction in emergency repairs. Asia-Pacific adoption is accelerating, with 48% of industrial plants integrating wireless monitoring to improve asset performance and operational safety.

• AI and Machine Learning Optimization: AI-driven anomaly detection has been deployed in 55% of high-tech industrial facilities, improving fault prediction accuracy by 23% compared to threshold-based systems. Machine learning algorithms analyze historical performance data, optimizing maintenance schedules and reducing operational disruptions. Edge AI processing further enables local decision-making, improving response times by 15% in production environments.

• Rise in Modular and Prefabricated Construction: The adoption of modular construction is reshaping demand dynamics in the Machine Condition Monitoring market. Research suggests that 55% of the new projects witnessed cost benefits while using modular and prefabricated practices in their projects. Pre-bent and cut elements are prefabricated off-site using automated machines, reducing labor needs and speeding project timelines. Demand for high-precision machines is rising, especially in Europe and North America, where construction efficiency is critical.

The Machine Condition Monitoring Market is segmented by product type, application, and end-user, each reflecting distinct adoption patterns and technological integration. Types include vibration sensors, temperature sensors, and ultrasonic devices, with vibration sensors leading adoption due to their versatility and accuracy in fault detection. Applications span predictive maintenance, asset tracking, and energy management, with predictive maintenance accounting for the highest utilization, supported by AI and IoT adoption trends. End-users comprise automotive, aerospace, power generation, and manufacturing sectors, with automotive maintaining the highest usage at 38%, while aerospace is the fastest-growing due to increasing digitalization and smart factory initiatives. Smaller sectors, including construction and chemical industries, collectively represent 25% of market engagement, leveraging tailored monitoring solutions. Recent pilot programs have demonstrated measurable efficiency gains, such as a 24% reduction in unplanned downtime in a U.S. automotive plant deploying vibration sensors and AI analytics.

Vibration sensors currently account for 42% of adoption, providing precise real-time detection of machine anomalies, making them the leading type in the Machine Condition Monitoring market. Ultrasonic sensors contribute 20%, mainly in niche applications like leak detection and high-frequency fault identification. Temperature sensors represent 18%, utilized primarily for critical process monitoring and safety compliance. Other types, including infrared and acoustic emission sensors, collectively make up 20%, supporting specialized industrial scenarios. The fastest-growing type is wireless vibration sensors, driven by the need for real-time, remote monitoring and reduced installation complexity.

Predictive maintenance remains the leading application, currently accounting for 45% of Machine Condition Monitoring utilization. This is driven by the growing emphasis on operational efficiency and minimizing unplanned downtime. Energy management applications follow at 20%, focusing on optimizing electricity consumption and reducing environmental impact. Asset tracking represents 15%, supporting operational visibility in large-scale industrial facilities. Other applications, including quality assurance and safety compliance, hold a combined 20%. The fastest-growing application is AI-based anomaly detection in predictive maintenance, supported by digital twin integration and cloud analytics.

The automotive industry leads adoption, representing 38% of Machine Condition Monitoring usage, driven by high production volumes and the need for continuous operational reliability. Aerospace is the fastest-growing end-user segment, fueled by the integration of advanced monitoring technologies into high-value aircraft manufacturing, with adoption rising by 24% in 2024. Manufacturing and power generation industries contribute 30% combined, leveraging condition monitoring for safety and efficiency improvements. Smaller sectors such as chemical, food processing, and construction collectively account for 12%, using tailored systems for critical asset management.

North America accounted for the largest market share at 35% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 10% between 2025 and 2032.

In 2024, North America recorded over 1,200 industrial facilities with fully integrated Machine Condition Monitoring systems, while Europe maintained a 28% regional market share with over 850 smart factories employing predictive maintenance. Asia-Pacific registered a volume of 950 facilities, with China alone contributing 42% of regional installations. Consumer adoption rates indicate that over 68% of enterprises in North America utilize AI-integrated sensors, whereas 55% of European companies implement energy-efficient monitoring solutions. The industrial sectors of automotive, aerospace, and energy generation dominate regional usage, while technological advancements in IoT, edge AI, and cloud-based analytics are accelerating operational efficiency. By 2025, over 1,500 companies globally are projected to integrate hybrid monitoring systems combining wireless sensors and predictive AI tools, reflecting a shift toward smart, sustainable, and resilient industrial ecosystems.

How are advanced monitoring solutions transforming operational efficiency?

North America accounts for 35% of the global Machine Condition Monitoring market, driven primarily by automotive, aerospace, and energy production sectors. Regulatory initiatives, including updated industrial safety standards, and government incentives for digital transformation have accelerated adoption. Technological trends such as cloud-based analytics, edge AI processing, and wireless sensor networks are enabling real-time monitoring and predictive maintenance, improving asset uptime by over 20% in high-value manufacturing environments. Local players like Rockwell Automation have implemented IoT-enabled vibration and temperature sensors across multiple facilities, enhancing predictive diagnostics and reducing maintenance costs. Enterprises in healthcare and finance demonstrate higher adoption rates, integrating monitoring systems to ensure operational resilience, compliance, and optimized performance.

What factors are driving smart monitoring adoption in industrial hubs?

Europe holds approximately 28% of the global Machine Condition Monitoring market, with Germany, the UK, and France as leading contributors. Strong regulatory frameworks and sustainability initiatives push companies to adopt explainable and energy-efficient monitoring solutions. European facilities are increasingly deploying AI-powered predictive maintenance and digital twin technologies, achieving up to 18% reduction in downtime. Siemens and Bosch are actively upgrading monitoring systems to incorporate wireless sensors and cloud-based analytics. Regulatory pressure drives demand for explainable Machine Condition Monitoring systems, particularly in aerospace and automotive sectors, where over 70% of facilities now comply with advanced operational monitoring standards.

How is industrial expansion fueling innovative monitoring solutions?

Asia-Pacific ranks second in market volume with 950 industrial facilities using Machine Condition Monitoring solutions. China, India, and Japan are the top consuming countries, collectively representing 68% of regional installations. Rapid industrialization, expansion of smart factories, and large-scale infrastructure projects are driving demand. Regional tech hubs are focusing on AI integration, IoT-enabled sensors, and real-time analytics to optimize equipment performance. Companies like Yokogawa Electric have implemented predictive maintenance platforms across manufacturing plants, improving operational uptime by 22%. Growth is fueled by mobile AI applications and e-commerce integration, with enterprises increasingly deploying smart monitoring to enhance productivity and asset reliability.

What opportunities are emerging from industrial and energy sector modernization?

South America, led by Brazil and Argentina, holds 8% of the global Machine Condition Monitoring market. Investment in energy, mining, and manufacturing infrastructure is driving adoption, with predictive maintenance and wireless monitoring becoming key initiatives. Government incentives supporting industrial modernization and trade policies facilitating technology imports encourage market expansion. Local players have begun deploying IoT-enabled monitoring systems to improve operational efficiency in high-value industrial sectors. Demand is closely linked to regional infrastructure upgrades and enterprise digitalization. South American enterprises are increasingly adopting monitoring solutions to address operational bottlenecks, optimize energy use, and ensure regulatory compliance.

How are energy and construction sectors shaping regional monitoring adoption?

The Middle East & Africa region accounts for 6% of the global Machine Condition Monitoring market. Major demand centers include the UAE and South Africa, with growth driven by oil & gas, construction, and power generation industries. Technological modernization includes adoption of IoT-enabled sensors, AI-driven predictive analytics, and cloud-based monitoring platforms. Local regulations promoting industrial safety and sustainability encourage investments in advanced monitoring systems. Regional players are implementing predictive maintenance across energy infrastructure, reducing operational downtime by up to 15%. Enterprises in this region demonstrate a strong focus on regulatory compliance and technology-enabled operational resilience.

United States: 35% market share; dominance due to high production capacity, extensive end-user adoption, and early integration of AI-driven monitoring solutions.

Germany: 15% market share; strong presence in automotive and manufacturing industries with robust regulatory compliance and advanced predictive maintenance adoption.

The Machine Condition Monitoring market is highly competitive and moderately fragmented, with over 120 active global competitors ranging from multinational corporations to specialized technology providers. The top five companies, including SKF, GE Digital, Emerson, Siemens, and Rockwell Automation, collectively account for approximately 48% of the market, indicating a moderately concentrated environment. Strategic initiatives among market players are robust, with 35% of competitors launching AI-driven predictive maintenance platforms between 2023 and 2024, while 28% formed strategic partnerships with IoT solution providers to enhance real-time monitoring capabilities. Product innovation remains a key differentiator, with wireless sensor systems, edge AI analytics, and digital twin integration being widely adopted to improve operational uptime and reduce unplanned maintenance events by up to 22%. Mergers and acquisitions are also shaping the competitive landscape, with at least 12 deals executed globally in the past two years to consolidate technological expertise. Regional positioning varies, with North America accounting for 35% of market share, Europe 28%, and Asia-Pacific 23%, creating competitive pressure to tailor solutions for regional adoption, regulatory compliance, and ESG-focused operational efficiency.

Siemens

Rockwell Automation

ABB

Honeywell International

Yokogawa Electric

Fluke Corporation

National Instruments

The Machine Condition Monitoring market is being transformed by a convergence of advanced sensing, AI, and digital technologies. Vibration sensors continue to dominate, accounting for 42% of installations in 2024, with wireless versions increasingly deployed for real-time, remote monitoring. Temperature sensors contribute 18% of installations, primarily in high-risk industrial processes, while ultrasonic and acoustic emission sensors collectively account for 20%, supporting niche applications such as leak detection and high-frequency fault identification.

Emerging technologies are redefining operational efficiency. AI-powered anomaly detection platforms are now implemented in over 55% of high-tech industrial facilities, providing predictive maintenance insights that improve fault detection accuracy by 23% compared to threshold-based systems. Edge computing adoption is accelerating, enabling on-site processing of sensor data and reducing latency by 15% in industrial environments. Cloud-based analytics platforms facilitate centralized monitoring, allowing enterprises to track over 1.2 million machine components globally with real-time dashboards and predictive alerts.

Digital twin technology is gaining traction, with 28% of manufacturing plants simulating machine performance for predictive maintenance, enabling decision-makers to reduce unplanned downtime by up to 22%. IoT-enabled sensor networks are deployed in 70% of newly installed systems in North America and Europe, enabling continuous data collection and cross-site integration. Integration with mobile applications and remote AI interfaces is also rising, particularly in Asia-Pacific, supporting rapid operational decision-making and remote diagnostics.

Overall, technology advancements are positioning Machine Condition Monitoring as a critical tool for industrial efficiency, asset optimization, and risk mitigation. Real-time monitoring, predictive analytics, and IoT integration are now central to the strategic deployment of monitoring solutions, supporting operational resilience and regulatory compliance across multiple industrial sectors.

In March 2023, Honeywell launched its Versatilis™ Transmitters for condition‑based monitoring of rotating equipment including pumps, motors, compressors, fans and gearboxes, utilizing low‑power LoRaWAN® wireless protocol to simplify installation and enable vibration, surface temperature and acoustic measurement. (honeywell.com)

In April 2023, Siemens integrated electrical‑signature analysis (ESA) from Samotics into its NXpower Monitor product, enabling real‑time detection of electrical and mechanical faults up to five months before downtime and extending condition monitoring to both AC motors and rotating equipment. (Samotics)

In March 2024, Rockwell Automation introduced its FactoryTalk® Analytics GuardianAI™ software which uses data from variable‑frequency drives to monitor asset health, detect early deviations and support maintenance planning without requiring data‑science expertise. (Rockwell Automation)

In July 2024, Emerson’s Advanced Solutions Simplify Condition Monitoring initiative was announced, enabling power‑generation customers to reduce maintenance costs by 30% and cut troubleshooting times in half via deployment of their monitoring platform alongside digital asset‑management services. (emerson.com)

This report on the Machine Condition Monitoring Market covers a comprehensive range of technology types, applications, end‑use industries and geographic regions. Technology types include vibration sensors, temperature sensors, ultrasonic/acoustic sensors, wireless sensor networks, edge computing modules and cloud‑based analytics platforms. Applications span predictive maintenance, energy management, asset tracking, quality assurance and safety compliance. End‑use industries addressed include automotive, aerospace, power generation, manufacturing, heavy machinery, mining, construction and oil & gas. Geographic regions analysed comprise North America, Europe, Asia‑Pacific, South America and Middle East & Africa, with country‑level detail for major markets such as the United States, Germany, China, India and Brazil. The report also delves into emerging and niche segments such as condition‑monitoring‑as‑a‑service (CMaaS), retrofit solutions for legacy equipment, digital twin integration for monitoring, and wireless IIoT platforms tailored for remote asset sites. Operational elements such as sensor deployment rates, wireless vs wired installations, enterprise adoption percentages, retrofit vs new‑build monitoring programmes and sustainability/ESG‑driven installations are examined. Additionally, the report includes competitive intelligence (number of active players, partnerships, product launches), regulatory and energy‑efficiency frameworks, and service‑model innovations such as pay‑per‑use monitoring contracts and lifecycle‑monitoring subscriptions. The breadth is designed to equip decision‑makers with insight into segment‑specific uptake, regional dynamics, technology migration paths and strategic investment areas.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2024 | USD 3158.29 Million |

Market Revenue in 2032 | USD 6433 Million |

CAGR (2025 - 2032) | 9.3% |

Base Year | 2024 |

Forecast Period | 2025 - 2032 |

Historic Period | 2020 - 2024 |

Segments Covered | By Types

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | SKF, GE Digital, Emerson, Siemens, Rockwell Automation, ABB, Honeywell International, Yokogawa Electric, Fluke Corporation, National Instruments |

Customization & Pricing | Available on Request (10% Customization is Free) |