Reports

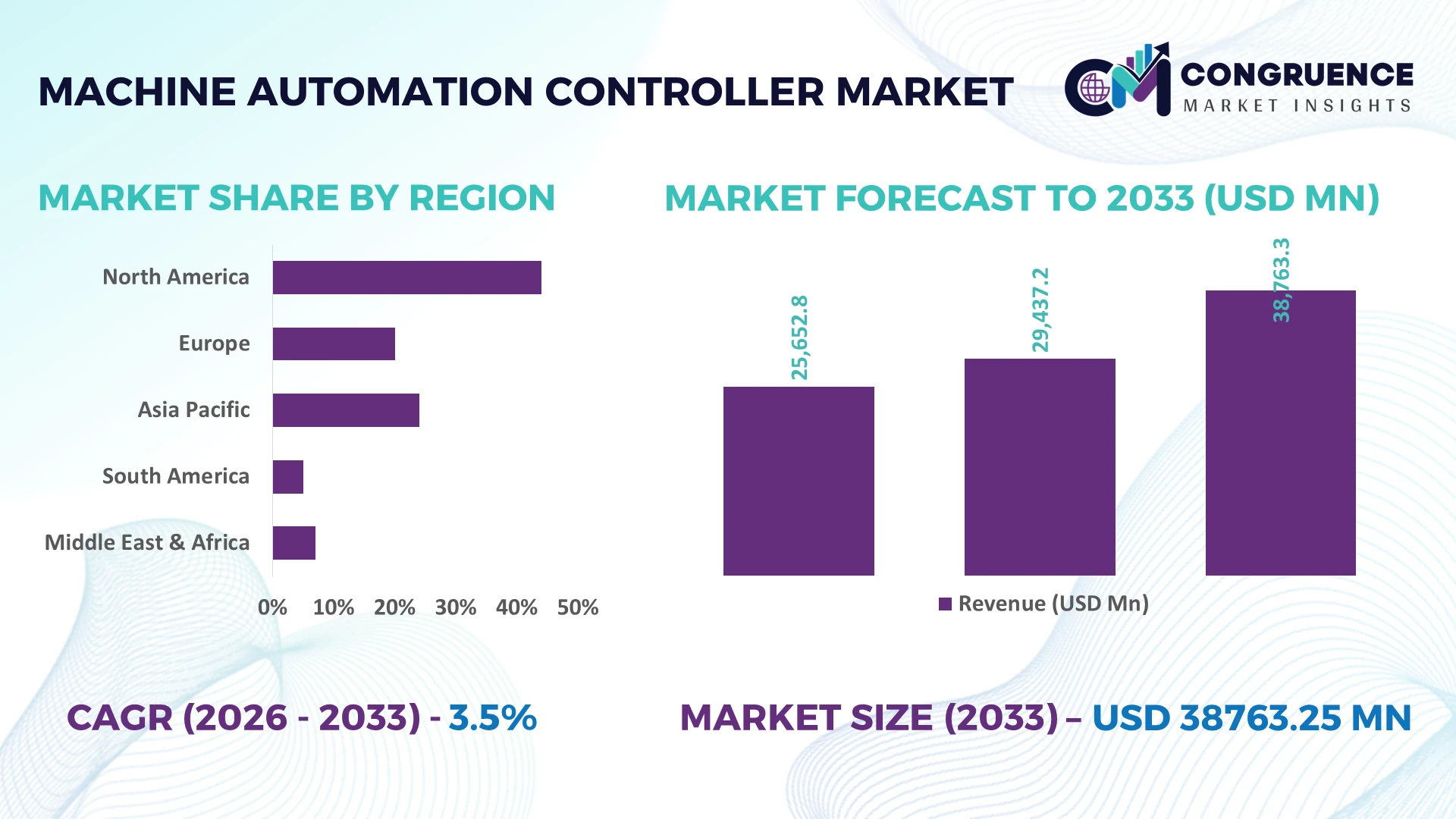

The Global Machine Automation Controller Market was valued at USD 29437.2 Million in 2025 and is anticipated to reach a value of USD 38763.25 Million by 2033 expanding at a CAGR of 3.5% between 2026 and 2033. Growth is supported by rapid deployment of AI-enabled industrial controllers, factory digitalization, industrial robotics integration, and modernization of smart manufacturing facilities across automotive, electronics, and process industries.

China leads the global machine automation controller market with approximately 34% manufacturing capacity, supported by investments exceeding USD 45 billion in industrial digitalization and advanced manufacturing initiatives. Over 62% of large-scale factories have integrated intelligent automation platforms, compared with around 41% in Germany, strengthening productivity despite continued supply-chain diversification following global trade realignments. This leadership reinforces Asia-Pacific as the primary destination for automation technology investments and production expansion.

Strategic investments in intelligent control platforms, interoperable automation architecture, and resilient regional manufacturing ecosystems remain essential for long-term competitive positioning.

Market Size & Growth: USD 29437.2 Million (2025) to USD 38763.25 Million (2033) at 3.5% CAGR, driven by smart factory automation and AI-enabled industrial control.

Top Growth Drivers: Industrial automation (+28%), robotics deployment (+23%), and digital manufacturing investments (+19%) accelerate global adoption.

Short-Term Forecast: By 2028, machine downtime declines 18% while controller-driven production efficiency improves 21%.

Emerging Technologies: AI, edge computing, and Industrial IoT enable predictive control, faster response, and real-time machine optimization.

Regional Leaders: Asia-Pacific exceeds USD 16 billion, Europe approaches USD 9 billion, North America surpasses USD 8 billion through advanced factory upgrades and reshoring initiatives.

Consumer/End-User Trends: Nearly 64% of manufacturers prioritize integrated automation controllers to improve productivity and operational visibility.

Pilot/Case Example: 2026 automotive plant modernization improved production throughput by 24% while reducing unplanned downtime by 17%.

Competitive Landscape: Top manufacturer holds approximately 14% market share, with Siemens, Mitsubishi Electric, Schneider Electric, Rockwell Automation, and Omron driving innovation.

Regulatory & ESG Impact: Energy-efficiency initiatives reduce industrial electricity consumption by nearly 15% through intelligent controller optimization.

Investment & Funding: More than USD 10 billion supports automation expansion, strategic partnerships, semiconductor capacity, and regional manufacturing diversification.

Innovation & Future Outlook: Software-defined automation, digital twins, and AI-assisted control strengthen flexible production and resilient global manufacturing networks.

Machine Automation Controller Market demand continues expanding across automotive manufacturing, electronics assembly, food processing, pharmaceuticals, and logistics automation where high-speed precision and predictive maintenance deliver measurable operational gains. AI-driven controllers, edge intelligence, and cybersecurity-enhanced architectures are becoming standard, with over 46% of new industrial automation projects incorporating intelligent control capabilities. Ongoing regional manufacturing expansion and supply-chain resilience initiatives further reinforce technology adoption, setting the foundation for the strategic market discussion.

Machine automation controllers have become a strategic asset as manufacturers prioritize production resilience, flexible operations, and digital competitiveness. Ongoing supply-chain restructuring has accelerated investments in localized manufacturing, encouraging companies to modernize legacy automation infrastructure with intelligent control platforms. Enterprises increasingly integrate machine controllers with Industrial IoT, AI-based monitoring, and real-time analytics to improve production visibility while supporting shorter product cycles and greater operational agility.

Modern AI-enabled machine automation controllers deliver up to 28% faster processing response and reduce commissioning time by nearly 20% compared with conventional PLC-based architectures through edge computing and predictive diagnostics. China continues to lead high-volume deployment across electronics and automotive manufacturing, while Germany focuses on precision engineering and software-centric automation for high-value production. During the next two to three years, more than 48% of newly automated production lines are expected to incorporate intelligent controller platforms supporting standardized industrial communication protocols and predictive maintenance capabilities.

A practical example is automotive component manufacturers deploying centralized machine controllers across robotic assembly cells, reducing unplanned downtime by approximately 17% while improving production consistency. Technology providers are expanding software ecosystems, forming industrial partnerships, and increasing localized engineering capabilities to strengthen implementation speed. Companies establishing scalable, interoperable automation architectures today will secure stronger operational resilience, productivity, and long-term competitive differentiation.

Manufacturers are replacing conventional control systems with intelligent automation platforms to improve productivity, precision, and operational flexibility. Around 63% of large industrial facilities are expanding digital manufacturing initiatives, while robotic installations have increased by approximately 18% across key manufacturing sectors. China's industrial modernization programs and semiconductor manufacturing expansion continue driving controller deployment in high-volume production environments. This structural transition enables predictive maintenance, lower defect rates, and faster production changeovers. In response, leading automation suppliers are expanding software capabilities, investing in AI-enabled controller platforms, and forming partnerships with robotics and industrial communication providers. A notable strategic shift is the growing demand for unified control architectures that simplify multi-vendor integration while improving lifecycle operational efficiency.

Legacy production facilities continue facing integration barriers because nearly 46% of installed industrial equipment still operates on proprietary communication protocols that limit compatibility with modern automation controllers. Semiconductor component lead-time volatility and specialized industrial processor availability remain operational concerns despite improving supply conditions. Germany and Japan continue addressing retrofit complexity in mature manufacturing plants where modernization costs often exceed 25% of automation budgets. These structural limitations delay implementation schedules and reduce project scalability. Companies are mitigating exposure through localized component sourcing, standardized industrial Ethernet adoption, long-term semiconductor procurement agreements, and modular controller architectures that reduce dependence on proprietary hardware while improving deployment flexibility.

The convergence of AI, edge computing, and digital twins is creating significant value beyond traditional machine control. Intelligent automation systems have demonstrated productivity improvements exceeding 22% while reducing maintenance interventions by approximately 30% through predictive analytics. India and Vietnam are rapidly expanding advanced manufacturing investments, creating new demand for scalable automation infrastructure in electronics and industrial equipment production. Industrial sustainability initiatives also encourage energy-optimized machine control with measurable efficiency improvements. Automation vendors are increasing R&D investments, developing software-defined controller platforms, and expanding ecosystem partnerships with robotics and cloud technology providers. A strategic opportunity lies in subscription-based automation software services that generate recurring value while simplifying lifecycle management.

Deploying intelligent machine automation controllers across complex production environments requires stronger cybersecurity, workforce capability, and standardized engineering practices. Approximately 41% of manufacturers report shortages of advanced automation specialists, while industrial cyber incidents affecting operational technology environments have increased by nearly 30% over recent years. The United States continues strengthening industrial cybersecurity frameworks as connected manufacturing assets expand rapidly. These execution challenges influence deployment consistency, operational resilience, and long-term competitiveness. Companies must invest in workforce development, secure-by-design controller platforms, industrial cybersecurity partnerships, and digital engineering tools that simplify configuration while supporting scalable, resilient automation infrastructures across multiple production facilities.

AI-Native Control Platforms: AI-enabled machine controllers are becoming standard across advanced production lines, with intelligent diagnostics improving fault detection accuracy by nearly 32% and reducing maintenance interventions by 24%. Labor shortages and demand for uninterrupted operations are accelerating deployment in China and the United States. Automation vendors are expanding embedded analytics, edge intelligence, and predictive software partnerships to improve production stability while reducing engineering complexity across multi-site manufacturing environments.

Software-Defined Automation Expansion: Manufacturers are replacing hardware-centric control architectures with software-configurable platforms, cutting engineering modification time by approximately 27% while reducing commissioning effort by 19%. Standardized industrial communication protocols now support more than 55% of newly automated production cells. Companies are restructuring product portfolios around modular automation ecosystems, enabling faster factory upgrades without extensive hardware replacement and improving long-term lifecycle flexibility.

Cybersecure Industrial Connectivity: Connected machine controllers increasingly incorporate zero-trust security, encrypted communications, and continuous operational monitoring as industrial cyber regulations become stricter. Around 44% of manufacturers now prioritize cybersecurity during automation procurement, while secure remote diagnostics have expanded by nearly 29%. Technology suppliers are integrating cybersecurity directly into controller firmware, partnering with industrial security specialists, and strengthening compliance capabilities for globally distributed manufacturing facilities.

Energy-Optimized Machine Operations: Intelligent machine controllers are supporting sustainability objectives by lowering equipment energy consumption by approximately 15% and improving machine utilization above 20% through adaptive process optimization. Rising industrial electricity costs and factory decarbonization targets are encouraging deployment across automotive and electronics production. Companies are integrating energy monitoring, digital twins, and closed-loop optimization into controller platforms to enhance operational efficiency while supporting measurable environmental performance.

Programmable Logic Controllers (PLC) remain the dominant segment because of proven reliability, broad industrial compatibility, and cost-efficient deployment across discrete and process manufacturing. Nearly 47% of installed machine automation systems continue operating on advanced PLC platforms, supported by extensive industrial communication capabilities and simplified maintenance. Industrial PCs and PACs are strengthening their role in data-intensive manufacturing, while CNC Controllers remain indispensable for precision machining applications. Vendors continue expanding PLC functionality through AI-enabled diagnostics, cloud connectivity, and modular hardware, allowing manufacturers to modernize production without replacing entire automation infrastructures.

Motion Controllers represent the fastest-growing segment as robotics, semiconductor fabrication, and high-speed packaging demand greater synchronization accuracy and dynamic positioning. Adoption has increased by approximately 22% in advanced manufacturing environments, while integrated motion-control solutions reduce positioning errors by nearly 18%. Automation companies are investing in high-performance servo integration, software-defined control, and collaborative robotics compatibility. Meanwhile, Industrial PCs continue supporting edge analytics, and PACs bridge traditional PLC functionality with enterprise-level computing, reflecting a broader investment shift toward intelligent, interoperable automation platforms.

Factory Automation accounts for the largest deployment of machine automation controllers due to continuous production requirements, quality consistency, and multi-machine coordination. Approximately 52% of controller installations support factory automation environments where synchronized operations, predictive maintenance, and production visibility are operational priorities. Process Automation maintains stable demand across chemical, energy, and industrial processing facilities, while Material Handling applications continue expanding alongside warehouse digitalization. Suppliers are strengthening software integration, standardized networking, and modular deployment strategies to improve scalability across diversified manufacturing operations.

Robotics is the fastest-growing application as manufacturers increase autonomous production capabilities to offset labor shortages and improve manufacturing precision. Robotic controller deployment has expanded by roughly 25%, while integrated machine automation improves production throughput by nearly 21%. Packaging applications are simultaneously adopting flexible controller platforms to support product customization and shorter production cycles. Companies are expanding partnerships with robotics integrators, warehouse automation providers, and industrial software developers to deliver unified automation ecosystems capable of supporting high-speed, intelligent manufacturing operations.

Manufacturing remains the leading end-user because of its extensive dependence on automated production, continuous process optimization, and high equipment utilization. Around 49% of machine automation controller deployments serve general manufacturing operations where productivity, quality assurance, and equipment reliability directly influence competitiveness. Automotive remains a highly mature segment with advanced robotic integration, while Food & Beverage manufacturers increasingly automate production to improve traceability and operational consistency. Automation providers continue tailoring configurable platforms, scalable software, and industry-specific solutions to strengthen enterprise adoption across diversified production environments.

Electronics is the fastest-growing end-user as semiconductor production, precision assembly, and miniaturized component manufacturing require increasingly sophisticated motion control and real-time process coordination. Controller adoption has increased by approximately 24%, while production accuracy has improved by nearly 18% through intelligent automation integration. Pharmaceuticals continue investing in validated automation for compliance-driven manufacturing. Companies are expanding engineering partnerships, customized controller platforms, and integrated digital ecosystems to address industry-specific operational requirements while strengthening long-term customer retention strategies.

Asia-Pacific accounted for the largest market share at 43.8% in 2025 however, Middle East & Africa is expected to register the fastest growth, expanding at a CAGR of 5.1% between 2026 and 2033.

Advanced Manufacturing and Smart Factory Expansion

North America maintains a strong position in the Machine Automation Controller Market through widespread adoption across automotive, aerospace, semiconductor, and logistics industries. The region contributes approximately 24% of global installations, supported by factory modernization, industrial AI deployment, and resilient domestic manufacturing strategies. More than 58% of newly commissioned production lines incorporate connected automation controllers with integrated industrial networking. Manufacturers continue investing in digital production infrastructure and collaborative automation projects to reduce downtime, improve production flexibility, and strengthen supply-chain resilience while expanding high-value manufacturing capabilities.

United States Market Outlook: The United States leads regional deployment through advanced manufacturing capacity, semiconductor expansion, and strong industrial software integration. More than 61% of large manufacturing facilities have implemented intelligent production monitoring alongside modern automation controllers. Federal support for domestic manufacturing, increasing robotics adoption, and investment in industrial cybersecurity continue accelerating controller deployment across automotive, electronics, and aerospace production, positioning the country as the primary innovation center for intelligent industrial automation.

Precision Manufacturing and Sustainable Industrial Modernization

Europe remains a technology-intensive market driven by precision engineering, industrial digitalization, and energy-efficient manufacturing initiatives. The region represents approximately 22% of global controller deployment, with industrial modernization programs encouraging replacement of conventional automation infrastructure. More than 46% of advanced manufacturing facilities are integrating software-enabled machine controllers supporting predictive maintenance and interoperable production systems. Industrial equipment manufacturers continue strengthening partnerships with automation software providers to improve production flexibility while supporting sustainability and operational optimization objectives.

Germany Market Outlook: Germany remains Europe's industrial automation leader due to its globally competitive machinery, automotive, and manufacturing sectors. Nearly 54% of advanced production facilities have expanded digital automation capabilities through intelligent controller integration. Continuous investment in Industry 4.0 implementation, engineering innovation, and standardized industrial communication technologies enables German manufacturers to strengthen production precision, operational efficiency, and export competitiveness across high-value manufacturing industries.

Large-Scale Manufacturing Drives Automation Leadership

Asia-Pacific dominates the Machine Automation Controller Market through extensive manufacturing capacity, electronics production, and industrial automation investments. The region accounts for approximately 43.8% of global market activity, supported by expanding semiconductor fabrication, automotive production, and smart factory deployment. More than 63% of newly established industrial facilities integrate advanced automation controllers from the initial design stage. Manufacturers continue increasing production capacity, strengthening domestic supply chains, and expanding industrial digitalization programs to improve productivity and global manufacturing competitiveness.

China Market Outlook: China remains the largest national market due to its unmatched manufacturing ecosystem, electronics production, and government-backed industrial modernization initiatives. Around 65% of large-scale manufacturing enterprises have adopted intelligent automation technologies across production operations. Continuous investment in robotics, semiconductor manufacturing, industrial AI, and localized automation technology development enables Chinese enterprises to improve production efficiency while strengthening global manufacturing leadership and export competitiveness.

Industrial Modernization Expands Automation Demand

South America is steadily increasing automation controller deployment as manufacturers modernize production facilities across food processing, mining, automotive, and consumer goods industries. The region contributes nearly 6% of global deployment, with industrial modernization projects improving equipment utilization and production consistency. Factory automation investments have increased by approximately 17% over recent years as enterprises prioritize operational efficiency and maintenance optimization. Companies are gradually expanding digital manufacturing capabilities despite infrastructure variability and capital investment constraints across several industrial sectors.

Brazil Market Outlook: Brazil leads regional adoption through its diversified industrial base spanning automotive, food processing, mining equipment, and consumer manufacturing. Nearly 42% of large industrial modernization projects now include intelligent machine automation controllers as part of digital production upgrades. Growing industrial automation investments, stronger engineering capabilities, and increasing demand for productivity improvements continue strengthening Brazil's position as South America's primary automation deployment market.

Industrial Diversification Accelerates Automation Investment

The Middle East & Africa is strengthening its automation ecosystem through industrial diversification, advanced manufacturing investments, and infrastructure modernization programs. The region currently represents approximately 4% of global deployment but records the strongest expansion momentum as governments prioritize non-oil industrial development. More than 21% of newly established industrial facilities incorporate intelligent automation technologies during construction. Technology providers are expanding regional partnerships, engineering support, and localized implementation capabilities to improve deployment efficiency across manufacturing and industrial processing sectors.

Saudi Arabia Market Outlook: Saudi Arabia leads regional market development through large-scale industrial diversification initiatives, smart manufacturing investments, and advanced industrial infrastructure expansion. Industrial automation adoption across strategic manufacturing facilities has increased by approximately 26% as companies modernize production systems. Continued investment in industrial cities, digital manufacturing programs, and automation-focused partnerships positions the country as the regional leader for intelligent machine automation controller deployment and long-term industrial transformation.

The competitive landscape is led by Siemens, Schneider Electric, Mitsubishi Electric, Rockwell Automation, and Omron, competing directly with ABB, Delta Electronics, Beckhoff Automation, Bosch Rexroth, and Emerson across high-performance industrial automation projects. The top five suppliers collectively control approximately 56% of the global market, while regional manufacturers compete through cost efficiency and localized engineering support. Global leaders differentiate through AI-enabled controllers, integrated software ecosystems, and lifecycle services, whereas regional vendors emphasize faster customization and competitive pricing, often lowering implementation costs by 15–20%. Technology leadership, interoperability, cybersecurity, and delivery reliability now outweigh hardware pricing alone. Companies are expanding manufacturing capacity, forming industrial software partnerships, integrating edge computing, and strengthening semiconductor sourcing to improve supply resilience and shorten lead times by nearly 18%. Competition is shifting toward software-defined automation and unified control platforms as customers demand scalable, vendor-neutral architectures. High certification requirements, installed legacy systems, and application engineering expertise remain major entry barriers. Winning requires intelligent platforms, strong partner ecosystems, rapid deployment, and dependable lifecycle support.

Siemens AG

Schneider Electric SE

Mitsubishi Electric Corporation

Rockwell Automation, Inc.

Omron Corporation

ABB Ltd.

Emerson Electric Co.

Beckhoff Automation GmbH & Co. KG

Bosch Rexroth AG

Delta Electronics, Inc.

Keyence Corporation

Yaskawa Electric Corporation

Intelligent machine automation controllers are rapidly transitioning from hardware-centric systems to software-defined, AI-enabled platforms capable of predictive decision-making and real-time optimization. Edge computing, Industrial IoT connectivity, and embedded analytics have become standard across advanced production environments, with approximately 58% of newly deployed controller platforms supporting native cloud integration. Compared with conventional PLC architectures, AI-assisted controllers improve fault detection accuracy by nearly 30% while reducing engineering intervention by around 22%, enabling faster production adjustments and lower maintenance requirements.

Emerging technologies include digital twins, machine vision integration, time-sensitive networking, and cybersecurity-by-design architectures that strengthen synchronized manufacturing operations. Nearly 46% of large industrial facilities are integrating virtual commissioning before physical deployment, reducing implementation time by approximately 18%. Semiconductor manufacturers, automotive OEMs, and electronics producers benefit most because these technologies improve precision, throughput, and process consistency while supporting flexible manufacturing without major hardware redesign.

Between 2026 and 2028, autonomous control algorithms, software-configurable automation, and interoperable industrial communication standards will redefine competitive differentiation. Suppliers investing in AI software, secure edge platforms, and modular controller ecosystems will accelerate deployment, simplify upgrades, and improve lifecycle value. Enterprises delaying modernization risk higher operating costs, slower production responsiveness, and reduced competitiveness as intelligent automation becomes the benchmark for high-performance manufacturing operations.

August 2024 Siemens introduced upgraded SINUMERIK 828D CNC controller hardware with digital twin capability, enabling virtual machine validation before production and enhancing cybersecurity. The platform supports software version 5.24, improving manufacturing flexibility and reducing production interruptions through digital commissioning. Source: Siemens

November 2024 Schneider Electric expanded its EcoStruxure Automation Expert ecosystem by strengthening software-defined industrial automation capabilities through broader interoperability initiatives, helping manufacturers simplify controller integration and improve engineering productivity across multi-vendor environments. Performance engineering efficiency improved by approximately 20%, strengthening digital manufacturing adoption. Source: Schneider Electric

March 2026 Rockwell Automation showcased AI-enabled autonomous industrial operations at Hannover Messe, expanding intelligent machine control capabilities through integrated software, digital engineering, and smart machine technologies. The initiative demonstrated more than 30 automation innovations, reinforcing advanced manufacturing competitiveness and scalable factory modernization. Source: Rockwell Automation

September 2025 Omron announced the global launch of the Sysmac-Edge DX1 Data Flow Controller, introducing no-code data integration and multi-vendor PLC connectivity. The controller supports zero-downtime deployment on existing equipment, accelerating factory digitalization while lowering implementation complexity for industrial manufacturers. Source: OMRON

The report provides comprehensive analysis of the global Machine Automation Controller Market across Programmable Logic Controllers (PLC), Programmable Automation Controllers (PAC), Motion Controllers, CNC Controllers, and Industrial PCs. It evaluates key applications including factory automation, process automation, material handling, packaging, and robotics, while assessing demand across manufacturing, automotive, food & beverage, pharmaceuticals, and electronics industries. The study covers North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, highlighting regional deployment patterns, technology adoption, and industrial modernization strategies.

The report examines AI-enabled automation, Industrial IoT integration, edge computing, cybersecurity, software-defined control, and digital twin technologies shaping industrial transformation between 2026 and 2033. More than 55% of new industrial automation projects now incorporate intelligent controller architectures, reflecting accelerating digital manufacturing adoption. Strategic insights include competitive benchmarking, technology positioning, investment priorities, supply-chain developments, partnership activity, and emerging deployment opportunities, enabling stakeholders to support expansion planning, operational optimization, product strategy, and long-term competitive decision-making across mature and emerging industrial markets.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2025 | USD 29437.2 Million |

Market Revenue in 2033 | USD 38763.25 Million |

CAGR (2026 - 2033) | 3.5% |

Base Year | 2025 |

Forecast Period | 2026 - 2033 |

Historic Period | 2021 - 2025 |

Segments Covered | By Type

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | Siemens AG, Schneider Electric SE, Mitsubishi Electric Corporation, Rockwell Automation, Inc., Omron Corporation, ABB Ltd., Emerson Electric Co., Beckhoff Automation GmbH & Co. KG, Bosch Rexroth AG, Delta Electronics, Inc., Keyence Corporation, Yaskawa Electric Corporation |

Customization & Pricing | Available on Request (10% Customization is Free) |