Reports

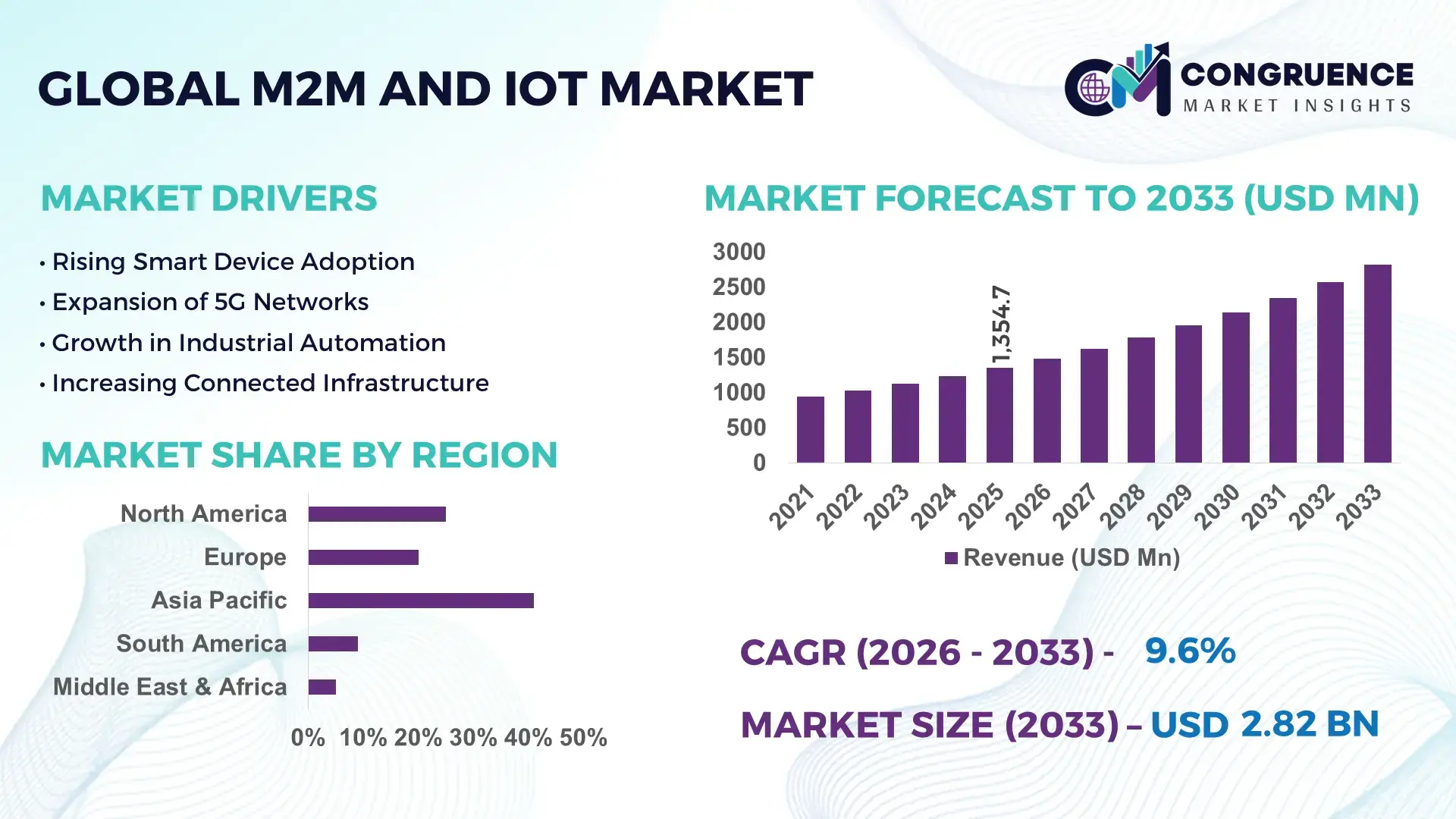

The Global M2M and IoT Market was valued at USD 1354.67 Million in 2025 and is anticipated to reach a value of USD 2824.56 Million by 2033 expanding at a CAGR of 9.62% between 2026 and 2033. Growth is being driven by large-scale industrial IoT deployments, accelerating 5G connectivity, smart utility modernization programs, and real-time asset monitoring across manufacturing, logistics, healthcare, and energy infrastructure.

China remains the dominant country in the global M2M and IoT landscape, accounting for approximately 34% of worldwide IoT connections in 2026, supported by extensive smart manufacturing investments and over 5 million operational 5G base stations. Compared with the United States, which leads in enterprise IoT software integration and cloud-based device management, China maintains a larger connected-device ecosystem across utilities, transportation, and industrial automation. Ongoing digital infrastructure expansion and technology competition between major economies continue to accelerate deployment scale and network intelligence.

Organizations prioritizing scalable connectivity platforms, edge analytics integration, and industrial automation ecosystems are positioned to secure long-term operational advantages.

Market Size & Growth: USD 1354.67 Million in 2025 reaching USD 2824.56 Million by 2033 at 9.62% CAGR, supported by industrial automation, connected assets, and advanced 5G-enabled deployments.

Top Growth Drivers: Industrial IoT adoption contributes 32%, smart city programs 24%, and connected logistics solutions 19% of new deployment activity.

Short-Term Forecast: By 2028, predictive maintenance deployments increase equipment uptime by 25% while reducing maintenance costs by 18%.

Emerging Technologies: Edge AI, digital twins, and private 5G networks improve data-processing efficiency by up to 35% across high-growth industrial environments.

Regional Leaders: Asia-Pacific exceeds USD 980 Million, North America surpasses USD 760 Million, and Europe approaches USD 610 Million, driven by manufacturing, utilities, and mobility digitization.

Consumer/End-User Trends: More than 58% of enterprises prioritize real-time connected-device monitoring to improve operational visibility and asset utilization.

Pilot/Case Example: In 2026, smart factory deployments achieved 22% lower downtime and 17% higher production efficiency through connected sensor networks.

Competitive Landscape: Top providers collectively control nearly 42% market share, with leadership concentrated among major connectivity, cloud, semiconductor, and industrial technology companies.

Regulatory & ESG Impact: Smart energy monitoring solutions reduce facility energy consumption by approximately 14% while supporting emissions reporting requirements.

Investment & Funding: Global investments exceed USD 40 Billion, with partnerships focused on edge computing, industrial connectivity, and regional supply-chain resilience.

Innovation & Future Outlook: Autonomous machine communication, AI-driven orchestration, and satellite IoT connectivity are reshaping next-generation enterprise deployment strategies.

The M2M and IoT Market is experiencing strong momentum from connected manufacturing systems, smart grid modernization, fleet telematics, and remote asset management applications. AI-enabled edge devices now improve data-processing efficiency by approximately 30%, while low-power wide-area networks expand coverage for industrial operations. Growing compliance requirements for infrastructure monitoring and continued supply-chain digitalization are accelerating adoption of intelligent connectivity platforms, setting the stage for broader strategic transformation across industries.

The M2M and IoT Market has become a strategic foundation for industrial competitiveness as enterprises prioritize connected operations, predictive decision-making, and real-time asset visibility. Infrastructure modernization programs, supply-chain restructuring, and digital manufacturing initiatives are accelerating deployment across transportation, utilities, healthcare, and production environments. More than 60% of large industrial organizations now integrate connected-device data into operational workflows, transforming M2M and IoT from a connectivity layer into a core business intelligence platform.

Technology evolution is improving deployment economics and operational performance. AI-enabled edge monitoring systems reduce network bandwidth requirements by nearly 35% compared with legacy centralized architectures while lowering response latency by over 40%. China leads large-scale connected infrastructure deployment through smart manufacturing ecosystems, while Germany emphasizes industrial interoperability and Industry 4.0 integration. In the United States, connected logistics platforms are reducing fleet downtime by approximately 20%, demonstrating measurable operational benefits beyond simple device connectivity.

Over the next two to three years, enterprises are expected to prioritize private network deployments, industrial edge computing, and sector-specific IoT platforms. Companies are increasing investments in ecosystem partnerships, semiconductor supply resilience, and cloud-edge integration strategies. Organizations that successfully combine connectivity, analytics, and automation capabilities will secure stronger operational agility, lower maintenance costs, and a sustainable competitive advantage in increasingly data-driven industries.

The primary growth catalyst is the integration of connected devices into industrial operations, enabling real-time monitoring, predictive maintenance, and automated decision-making. Approximately 58% of manufacturers now deploy IoT-enabled monitoring systems, while connected asset utilization improvements frequently exceed 20%. In China, smart factory investments continue expanding alongside industrial digitalization policies, creating demand for advanced M2M communication infrastructure. The operational impact is significant: predictive maintenance reduces unplanned downtime by nearly 25% and improves equipment productivity. In response, technology providers are expanding edge computing portfolios, forming connectivity partnerships, and investing in sector-specific platforms. A notable strategic shift is the convergence of operational technology and information technology, allowing enterprises to convert machine-generated data into measurable productivity gains and faster operational decision cycles.

A major structural limitation stems from fragmented communication standards and uneven infrastructure readiness across industries. Nearly 45% of enterprises report integration difficulties when connecting legacy equipment with modern IoT platforms, while deployment costs can increase by 15%–20% due to customization requirements. Industrial operators in India and several emerging manufacturing hubs continue facing network reliability and infrastructure consistency challenges. These constraints slow scalability, extend implementation timelines, and reduce return on technology investments. To mitigate exposure, companies are adopting standardized communication protocols, localizing technology ecosystems, and negotiating long-term infrastructure agreements with network providers. A critical operational insight is that interoperability challenges often create larger deployment costs than hardware procurement, making integration architecture a strategic priority rather than a technical afterthought.

Significant opportunities are emerging from edge intelligence, autonomous machine communication, and sector-focused IoT ecosystems. Edge-enabled architectures can reduce data transmission requirements by approximately 30%, while real-time analytics improve operational response rates by more than 25%. Japan and South Korea are accelerating investments in smart infrastructure, advanced manufacturing, and connected mobility platforms, creating high-value deployment environments. The rise of AI-integrated IoT solutions enables companies to monetize operational data through predictive services and outcome-based business models. Organizations are responding through R&D expansion, semiconductor partnerships, and ecosystem development initiatives. A particularly valuable opportunity lies in mid-sized industrial facilities that remain underpenetrated yet can achieve substantial efficiency gains without extensive infrastructure replacement, creating attractive deployment economics and faster implementation cycles.

As connected-device volumes increase, cybersecurity and large-scale system orchestration have become critical execution challenges. More than 70% of enterprise IoT deployments now involve multi-vendor environments, significantly increasing management complexity. Connected infrastructure operators face rising pressure to secure endpoints, communication networks, and operational data against increasingly sophisticated threats. In the United States, industrial organizations continue allocating larger portions of digital transformation budgets toward cybersecurity frameworks and zero-trust architectures. Poorly managed deployments can increase maintenance workloads by nearly 18% and create operational inconsistencies across distributed assets. Companies must address these risks through workforce development, advanced security platforms, and scalable device-management architectures. The long-term competitive differentiator will be the ability to securely manage millions of connected endpoints while maintaining performance, compliance, and operational continuity.

Private Network Deployment Acceleration: Enterprises are increasingly adopting private 5G and dedicated wireless infrastructure to support mission-critical operations. Industrial facilities report up to 30% lower network latency and nearly 25% higher device reliability compared with shared connectivity environments. Germany and the United States are expanding private network deployments across manufacturing and logistics hubs as stricter operational continuity requirements emerge. Companies are responding through telecom partnerships, spectrum investments, and integrated connectivity platforms that improve production visibility and reduce workflow interruptions.

Edge Analytics Becoming Standard: Data processing is moving closer to operational assets, with edge-enabled deployments reducing cloud data transfers by approximately 35% and improving real-time decision speeds by over 40%. Labor shortages and rising data volumes are pushing manufacturers toward autonomous monitoring architectures. Enterprises are restructuring analytics workflows and embedding AI models directly into connected devices. A notable shift is that many organizations now prioritize operational responsiveness over centralized data storage, creating new demand for distributed computing ecosystems.

Satellite IoT Network Expansion: Remote asset monitoring is gaining traction through low-earth-orbit satellite connectivity, increasing coverage availability by nearly 20% across mining, agriculture, and energy operations. Supply-chain resilience initiatives and infrastructure monitoring requirements are accelerating adoption in geographically dispersed locations. Technology providers are forming connectivity alliances and launching hybrid terrestrial-satellite solutions to maintain uninterrupted data transmission where conventional networks remain economically impractical.

Device Lifecycle Optimization Focus: Enterprises are shifting attention from device deployment volumes toward lifecycle management and asset efficiency. Predictive maintenance programs are reducing equipment failures by roughly 22%, while automated device management lowers maintenance workloads by nearly 18%. Large transportation fleets in China and Japan are integrating lifecycle analytics into operational planning. Companies are scaling management platforms, consolidating vendor ecosystems, and standardizing device architectures to improve long-term operational control and reduce support complexity.

Connectivity remains the leading segment due to its foundational role in linking devices, applications, networks, and enterprise systems. More than 40% of large-scale IoT deployments prioritize connectivity investments before expanding software or analytics capabilities, reflecting its critical importance for scalability and performance. Cellular IoT, LPWAN technologies, and private wireless networks continue supporting industrial automation, transportation monitoring, and utility modernization initiatives. Hardware maintains strong relevance through sensor deployment growth, while platform solutions are increasingly adopted to manage data orchestration and device interoperability across multi-vendor environments.

Software is emerging as the fastest-growing type as enterprises seek advanced analytics, automation, and AI-driven operational intelligence. Organizations implementing intelligent software layers report up to 28% faster incident response and nearly 20% higher asset utilization. Services remain strategically important for deployment integration, cybersecurity, and lifecycle management, particularly among enterprises modernizing legacy infrastructure. In response, vendors are expanding cloud-native offerings, investing in interoperability frameworks, and strengthening ecosystem partnerships to capture long-term platform-centric opportunities. Investment priorities are steadily shifting from standalone connectivity toward integrated software-platform ecosystems that generate operational intelligence.

Smart Manufacturing represents the leading application segment due to extensive deployment across production facilities, industrial automation environments, and quality-control operations. Connected manufacturing systems improve equipment effectiveness by approximately 20% while reducing unplanned downtime by nearly 25%. Industrial operators in China, Germany, and the United States continue expanding connected production lines to improve throughput and operational visibility. Smart Cities remain a significant deployment area, while Asset Tracking solutions are becoming increasingly important for inventory optimization and supply-chain transparency.

Connected Vehicles are the fastest-growing application as fleet operators adopt telematics, predictive diagnostics, and real-time routing technologies. Organizations utilizing connected fleet platforms report fuel efficiency improvements exceeding 15% and maintenance cost reductions approaching 18%. Healthcare Monitoring and Smart Energy applications are also gaining momentum as providers prioritize remote monitoring and intelligent grid management capabilities. Companies are accelerating deployment through automation initiatives, integrated platforms, and ecosystem partnerships. Demand is increasingly shifting toward applications capable of delivering measurable operational outcomes rather than simple connectivity expansion.

Manufacturing remains the dominant end-user segment because of its extensive dependence on machine connectivity, predictive maintenance, industrial automation, and operational analytics. Nearly 58% of large manufacturing facilities actively utilize connected asset monitoring systems, reflecting the sector’s scale and infrastructure intensity. Production-focused enterprises prioritize IoT investments to improve equipment uptime, process efficiency, and supply-chain synchronization. Energy & Utilities maintain strong adoption through grid modernization programs, while Government & Public Sector organizations continue deploying connected infrastructure for transportation, public safety, and smart services.

Transportation & Logistics is the fastest-growing end-user segment as organizations seek real-time visibility across increasingly complex supply networks. Connected logistics platforms have improved shipment tracking accuracy by approximately 30% while reducing operational delays by nearly 15%. Healthcare organizations are expanding connected monitoring capabilities, and retailers are integrating IoT-enabled inventory management systems to optimize stock availability. Vendors are responding through customized solutions, industry-specific pricing models, and strategic ecosystem partnerships. Competitive positioning is increasingly determined by the ability to address sector-specific operational requirements rather than offering generic connectivity products.

Asia-Pacific accounted for the largest market share at 41% in 2025 however, Middle East & Africa is expected to register the fastest growth, expanding at a CAGR of 11.4% between 2026 and 2033.

Enterprise Connectivity and Industrial Automation Leadership

North America remains a highly mature M2M and IoT market, supported by extensive enterprise digitization, industrial automation, and advanced network infrastructure. The region represents approximately 27% of global market activity, with deployment concentrated across manufacturing, logistics, utilities, and healthcare sectors. Private wireless networks, edge computing integration, and AI-enabled operational monitoring are becoming standard deployment models. More than 60% of large enterprises utilize connected asset management platforms to improve productivity and maintenance planning. Strategic partnerships between cloud providers, telecom operators, and industrial technology firms continue accelerating deployment scale, while infrastructure modernization programs support broader integration of connected systems into critical operational environments.

United States Market Outlook: The United States leads regional deployment activity through its advanced digital infrastructure, large industrial base, and strong enterprise technology spending. Manufacturing facilities increasingly deploy predictive maintenance systems and intelligent monitoring platforms to improve operational efficiency. More than 70% of large industrial organizations have integrated IoT-enabled operational analytics into core workflows. Strong investment in private networks, edge computing ecosystems, and industrial AI applications continues strengthening the country’s position as a key innovation hub for large-scale connected enterprise operations.

Industry 4.0 and Sustainable Infrastructure Modernization

Europe maintains a strong position through advanced manufacturing capabilities, industrial digitization programs, and regulatory support for connected infrastructure. The region accounts for nearly 24% of global market activity, with Germany, France, and the United Kingdom driving deployment intensity. Smart manufacturing, intelligent energy management, and connected transportation networks remain primary investment areas. Industrial facilities adopting IoT-enabled production systems report efficiency improvements exceeding 20% in many manufacturing segments. Ongoing investments in digital infrastructure and cross-industry interoperability frameworks are strengthening enterprise adoption while supporting long-term operational modernization objectives.

Germany Market Outlook: Germany serves as the region’s strategic industrial technology leader through its strong manufacturing ecosystem and Industry 4.0 initiatives. Connected production facilities, machine-to-machine communication networks, and intelligent factory platforms are widely deployed across automotive and engineering sectors. Approximately 65% of large manufacturers utilize advanced industrial connectivity solutions to optimize production workflows. Strong collaboration among industrial technology providers, manufacturers, and research institutions continues accelerating innovation and deployment sophistication across the country.

Large-Scale Device Deployment and Manufacturing Dominance

Asia-Pacific leads the global M2M and IoT market through its extensive manufacturing base, large connected-device ecosystem, and aggressive digital infrastructure investments. The region contributes approximately 41% of global market activity, supported by smart factory deployment, connected transportation systems, and utility modernization programs. Rapid expansion of 5G infrastructure and industrial automation platforms continues driving adoption. Several countries have significantly expanded machine connectivity across industrial parks and logistics corridors, creating one of the largest operational IoT environments globally. Strong semiconductor production capabilities further reinforce deployment scale and ecosystem development throughout the region.

China Market Outlook: China remains the most influential market due to its manufacturing scale, smart factory investments, and advanced connectivity infrastructure. The country operates millions of connected industrial devices across production facilities, utilities, and transportation networks. Extensive deployment of industrial IoT solutions has enabled measurable productivity improvements in manufacturing operations and logistics management. Government-supported industrial modernization initiatives, strong domestic technology ecosystems, and continuous network expansion continue positioning China at the center of global M2M and IoT deployment activity.

Logistics Modernization and Asset Visibility Expansion

South America is experiencing increasing adoption of connected technologies across transportation, agriculture, mining, and utilities sectors. The region accounts for approximately 5% of global market activity, with deployment priorities focused on asset tracking, fleet management, and operational monitoring. Expanding cellular connectivity and digital transformation initiatives are supporting broader implementation across industrial sectors. Connected logistics platforms have improved fleet visibility by nearly 25% in several large-scale deployments. While infrastructure inconsistencies remain a challenge in some markets, strategic investments and enterprise modernization programs continue strengthening adoption across critical industries.

Brazil Market Outlook: Brazil leads regional demand through its large logistics network, industrial operations, and expanding digital infrastructure. Connected fleet management systems, agricultural monitoring platforms, and industrial automation technologies are increasingly deployed across key economic sectors. More than 50% of large logistics operators have expanded investments in connected asset tracking and operational analytics. The country’s combination of industrial scale, transportation requirements, and technology adoption momentum continues supporting long-term market development.

Smart Infrastructure Investment and Digital Transformation Momentum

Middle East & Africa is emerging as a high-priority deployment market driven by smart city investments, industrial diversification strategies, and critical infrastructure modernization. The region represents approximately 3% of global market activity but demonstrates strong deployment momentum across utilities, transportation, and public-sector infrastructure projects. Large-scale digital transformation initiatives are increasing demand for connected monitoring systems and intelligent operational platforms. Several smart infrastructure projects have achieved over 30% improvement in operational visibility through integrated IoT deployments. Investment-led modernization continues creating new opportunities for technology providers and infrastructure operators.

Saudi Arabia Market Outlook: Saudi Arabia is the region’s most strategically significant market due to extensive smart city development, industrial diversification programs, and digital infrastructure investments. Connected technologies are being integrated into transportation systems, energy infrastructure, industrial facilities, and public services. The country has significantly expanded intelligent infrastructure deployment under national transformation initiatives, supporting broad adoption of machine-to-machine communication systems. Strong public-private collaboration and sustained investment in advanced digital ecosystems continue reinforcing Saudi Arabia’s leadership position within the regional market.

The M2M and IoT market is led by Cisco Systems, Huawei Technologies, Qualcomm, Ericsson, Siemens, and IBM, competing across connectivity infrastructure, industrial platforms, device management, and enterprise analytics. Global technology leaders compete against industrial automation specialists, while telecom infrastructure providers challenge platform-centric software vendors for ecosystem control. The top five participants collectively account for approximately 38% of market activity, creating a moderately concentrated competitive structure. Competition centers on platform interoperability, connectivity performance, cybersecurity capabilities, and deployment speed. Enterprises deploying integrated platforms report up to 25% lower operational management costs and nearly 30% faster device onboarding compared with fragmented architectures. Companies are expanding through strategic partnerships, edge computing investments, industrial AI integration, and vertical-specific solutions. The current competitive shift favors vendors controlling both connectivity and analytics layers. Key barriers include interoperability requirements, large-scale deployment expertise, and cybersecurity compliance. Success increasingly depends on delivering scalable, secure, and outcome-driven connected ecosystems.

Cisco Systems, Inc.

Huawei Technologies Co., Ltd.

Qualcomm Incorporated

Ericsson AB

Nokia Corporation

Siemens AG

IBM Corporation

Oracle Corporation

SAP SE

Schneider Electric SE

Honeywell International Inc.

PTC Inc.

Advantech Co., Ltd.

Telit Cinterion Group SA.

M2M and IoT technology development is increasingly centered on edge computing, AI-enabled analytics, and advanced connectivity platforms. More than 60% of large enterprise deployments now integrate edge processing to reduce data transmission requirements and improve response times. AI-powered monitoring systems improve predictive maintenance accuracy by approximately 25% while reducing unplanned downtime by nearly 20%. Industrial organizations are increasingly combining IoT sensors, cloud platforms, and machine learning models to create real-time operational intelligence. This integration enables faster decision-making, lower operational costs, and improved asset utilization across manufacturing, logistics, and utility environments.

Emerging technologies are shifting market priorities from connectivity alone toward autonomous operations. Private 5G networks improve device reliability by approximately 30% compared with conventional shared networks, while digital twin platforms improve operational planning efficiency by nearly 22%. Edge AI architectures reduce bandwidth consumption by roughly 35% versus legacy centralized processing models. Adoption of satellite-enabled IoT connectivity is also expanding across remote industrial assets, creating new deployment opportunities where terrestrial network coverage remains limited. Companies investing in integrated connectivity and analytics ecosystems are gaining measurable operational advantages over competitors relying on fragmented infrastructures.

Between 2026 and 2028, disruptive technologies including AI agents, industrial digital twins, and non-terrestrial IoT networks will accelerate enterprise transformation. Organizations deploying intelligent edge platforms are expected to achieve 20% faster operational response cycles and stronger infrastructure scalability. Technology leaders that combine connectivity, automation, cybersecurity, and real-time analytics will secure superior competitive positioning as enterprises prioritize intelligent, outcome-driven connected operations.

October 2025 – Ericsson partnered with AT&T to launch the cloud-based AT&T IoT Marketplace, enabling automated provisioning, billing, and service management through a unified digital platform. The scalable architecture supports on-demand service expansion and accelerates enterprise IoT deployment efficiency. Source: ericsson.com

January 2026 – Qualcomm expanded its Industrial and Embedded IoT portfolio through integrated software, processors, and developer tools following multiple strategic acquisitions. The initiative strengthened edge AI deployment capabilities and accelerated commercialization across industrial sectors, supporting broader enterprise adoption. Source: qualcomm.com

March 2026 – Qualcomm introduced the X105 5G Modem-RF platform with up to 30% lower power consumption and a 15% smaller footprint than the previous generation. The launch advances industrial IoT, satellite-enabled connectivity, and next-generation machine communication deployments. Source: qualcomm.com

June 2026 – Cisco unveiled Cisco Cloud Control, an AI-enabled operational platform designed to manage and secure critical infrastructure. The solution reduces operational complexity by unifying infrastructure management and strengthens enterprise readiness for large-scale connected environments. Source: investor.cisco.com

This report provides comprehensive analysis of the M2M and IoT market across key types including Hardware, Connectivity, Platform, Software, and Services. It evaluates demand patterns across Smart Manufacturing, Smart Cities, Connected Vehicles, Asset Tracking, Healthcare Monitoring, and Smart Energy applications while assessing adoption across Manufacturing, Transportation & Logistics, Healthcare, Energy & Utilities, Retail, and Government & Public Sector end-users. The study covers North America, Europe, Asia-Pacific, South America, and Middle East & Africa, representing more than 95% of global deployment activity.

The report examines technology trends including edge computing, private 5G networks, AI-enabled analytics, satellite IoT, and industrial automation platforms. It analyzes enterprise deployment strategies, interoperability developments, cybersecurity priorities, and ecosystem partnerships shaping market evolution between 2026 and 2033. Coverage includes established industrial deployments as well as emerging opportunities in intelligent infrastructure, connected mobility, and remote asset management. Strategic insights support investment evaluation, expansion planning, competitive benchmarking, technology selection, and long-term operational decision-making across the connected enterprise ecosystem.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 1354.67 Million |

|

Market Revenue in 2033 |

USD 2824.56 Million |

|

CAGR (2026 - 2033) |

9.62% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Cisco Systems, Inc., Huawei Technologies Co., Ltd., Qualcomm Incorporated, Ericsson AB, Nokia Corporation, Siemens AG, IBM Corporation, Oracle Corporation, SAP SE, Schneider Electric SE, Honeywell International Inc., PTC Inc., Advantech Co., Ltd., Telit Cinterion Group SA. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |