Reports

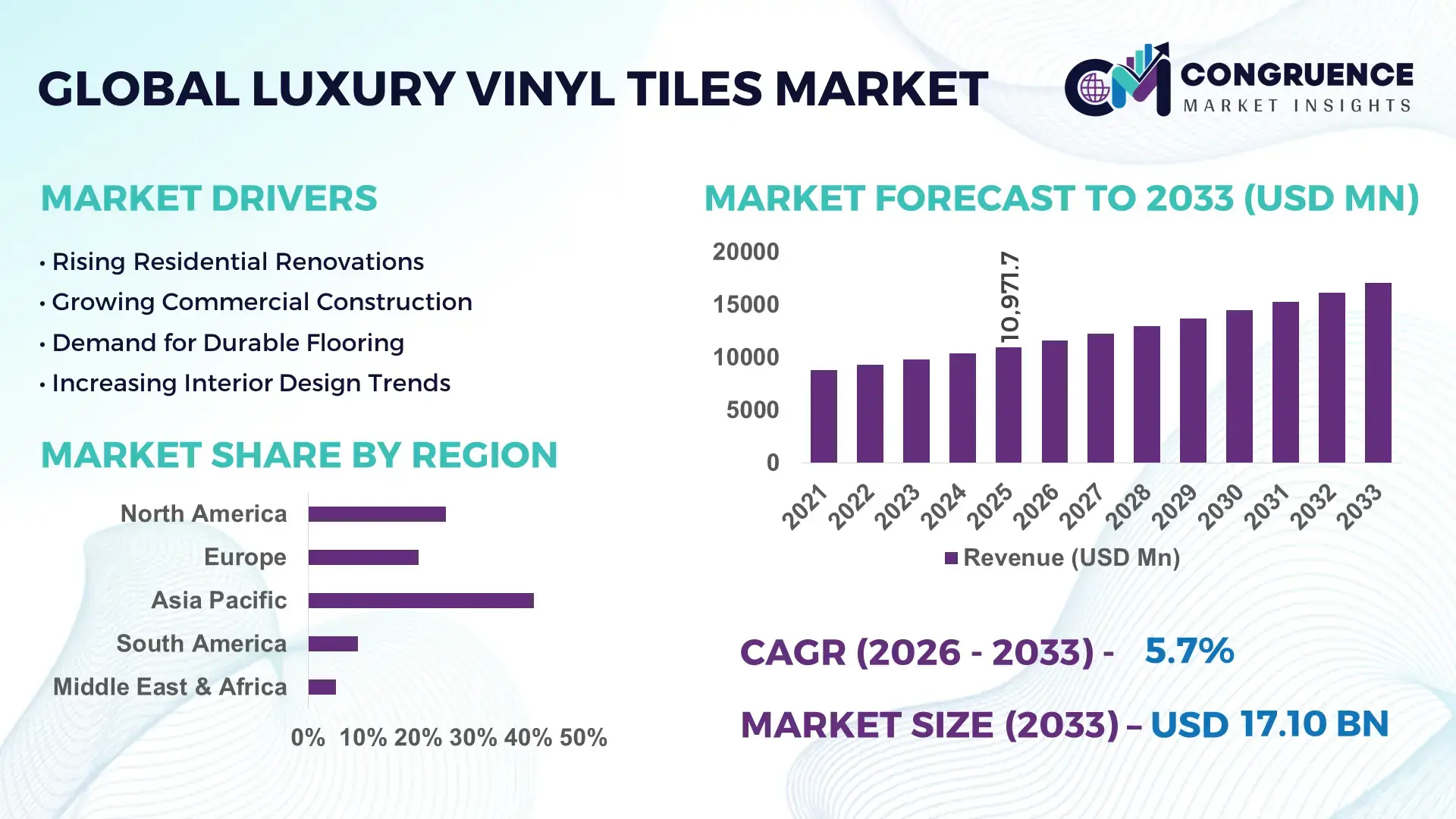

The Global Luxury Vinyl Tiles Market was valued at USD 10971.66 Million in 2025 and is anticipated to reach a value of USD 17095.12 Million by 2033 expanding at a CAGR of 5.7% between 2026 and 2033. Advanced rigid-core flooring systems, digital wood-stone texture printing, and low-maintenance installation formats are accelerating replacement demand across commercial construction, multifamily housing, and healthcare interiors, with click-lock luxury vinyl tiles reducing installation time by nearly 28% compared to traditional ceramic flooring systems.

China maintains the dominant position in the global luxury vinyl tiles market with nearly 34% manufacturing share, supported by large-scale PVC processing capacity, automated flooring plants, and over USD 1.8 billion in recent flooring modernization investments concentrated in Guangdong and Zhejiang. The country supplies high-volume residential and commercial flooring products to North America and Europe while expanding advanced SPC and WPC production lines with 22% higher output efficiency than conventional vinyl flooring systems. Compared with several Southeast Asian exporters, China retains stronger logistics integration and lower unit production costs, enabling faster delivery cycles for hospitality, retail, and healthcare construction projects. Domestic adoption of digitally printed, phthalate-free flooring solutions surpassed 41% across new commercial interior installations during 2025–2026.

The market is increasingly rewarding manufacturers that combine localized production, ESG-compliant materials, and high-speed modular flooring technologies to secure long-term contracts across institutional and renovation-driven construction segments.

Market Size & Growth: USD 10.97 billion in 2025 advancing toward USD 17.09 billion by 2033, driven by high-durability SPC flooring adoption and renovation-focused construction demand.

Top Growth Drivers: Commercial renovation activity rose 19%, waterproof flooring demand expanded 24%, and rapid-installation systems improved contractor productivity by 27%.

Short-Term Forecast: By 2028, automated cutting and digital printing systems will reduce production waste by 16% and installation turnaround time by 21%.

Emerging Technologies: AI-based texture mapping, rigid-core SPC engineering, and recycled polymer blending increased manufacturing precision by 18% across advanced flooring facilities.

Regional Leaders: Asia-Pacific exceeds USD 6.4 billion through manufacturing scale, North America crosses USD 4.1 billion via remodeling demand, and Europe advances through low-emission flooring adoption.

Consumer/End-User Trends: More than 46% of commercial buyers prioritize waterproof and scratch-resistant flooring for healthcare, retail, and hospitality projects.

Pilot/Case Example: In 2025, a large mixed-use renovation project reduced flooring replacement cycles by 31% after deploying premium rigid-core luxury vinyl tiles.

Competitive Landscape: The top five players control nearly 38% market share, while global manufacturers accelerate premium product launches and regional expansion strategies.

Regulatory & ESG Impact: Low-VOC flooring standards and recycled material mandates lowered compliance-related rejection rates by 14% across institutional procurement contracts.

Investment & Funding: Over USD 2 billion has been allocated toward automated flooring plants, regional supply chain diversification, and sustainable material integration since 2024.

Innovation & Future Outlook: Bio-based polymers, smart acoustic flooring layers, and digitally customized surface finishes are transforming high-growth commercial flooring competition.

Commercial construction contributes nearly 39% of total luxury vinyl tiles consumption, followed by residential remodeling at 34% and healthcare-retail infrastructure at 18%, reflecting strong replacement-driven demand. Advanced SPC flooring, antimicrobial coatings, and digitally embossed textures improved durability performance by over 20% across premium product lines during 2025–2026. Asia-Pacific remains the largest production hub, while North America records stronger renovation-led installation growth amid regional supply chain restructuring and stricter indoor emission regulations. Manufacturers are increasingly prioritizing recyclable composite flooring and localized production ecosystems, positioning the market for a more technology-intensive and compliance-driven competitive phase.

Luxury vinyl tiles have become a strategic flooring category for construction, renovation, and institutional infrastructure projects because developers now prioritize installation speed, lifecycle durability, and maintenance efficiency over traditional flooring materials. Global procurement strategies are rapidly shifting toward modular and rigid-core flooring systems that reduce operational downtime by nearly 25% across retail, hospitality, and healthcare projects. Rising raw material localization and regional manufacturing expansion are accelerating competitive positioning, particularly as supply chain disruptions and energy volatility continue transforming procurement economics between Asia, Europe, and North America.

Advanced SPC flooring technology improves installation efficiency by 32% while reducing lifecycle maintenance cost by 21% compared to legacy ceramic and laminate systems. Asia-Pacific leads in production volume, while Europe leads in sustainable flooring adoption with more than 36% of new institutional projects integrating low-VOC and recyclable flooring standards. Over the next three years, automated flooring plants are expected to increase production throughput by 18%, while digital printing systems reduce material wastage by 15%. ESG-focused flooring portfolios are delivering measurable compliance advantages and helping suppliers secure premium public infrastructure contracts.

In 2025, a large healthcare renovation program in North America achieved 29% faster project completion after deploying click-lock luxury vinyl tile systems across high-traffic facilities. Major manufacturers are accelerating capital allocation toward recycled polymer integration, regional warehousing, and premium acoustic flooring technologies to optimize margins and strengthen long-term contract visibility. Companies that combine sustainable materials, localized production, and advanced flooring engineering are redefining competitive advantage across the global luxury vinyl tiles market.

Commercial renovation activity and modular construction expansion are accelerating luxury vinyl tile deployment across retail, healthcare, and multifamily projects due to faster installation and lower maintenance requirements. Click-lock and rigid-core flooring systems reduce installation time by nearly 28% while improving durability performance by 22% compared with conventional laminate products. Rising urban redevelopment in Asia-Pacific and North America, combined with post-2024 supply chain restructuring, is forcing contractors to prioritize regionally available flooring materials with shorter lead times. Large manufacturers are responding through automated SPC production lines, strategic distributor partnerships, and localized warehousing expansion. Premium waterproof flooring adoption surpassed 44% across commercial renovation projects during 2025, strengthening replacement-driven demand and increasing competitive differentiation for technology-focused suppliers globally.

The luxury vinyl tiles market remains heavily exposed to PVC resin price volatility, petrochemical supply concentration, and tightening environmental compliance standards across Europe and North America. Raw material cost fluctuations exceeded 17% during recent procurement cycles, while freight disruptions increased logistics expenses by nearly 13% for export-focused flooring manufacturers. Stricter low-VOC certification requirements and recycling mandates are forcing producers to redesign product formulations and invest in higher-cost sustainable materials. These constraints directly impact pricing stability, production planning, and margin consistency across mid-sized suppliers. Companies are mitigating exposure through long-term resin procurement contracts, regional supplier diversification, and accelerated investment in recycled polymer technologies. Several manufacturers are also expanding localized production to reduce transportation dependency and compliance-related delays.

Sustainable flooring innovation and infrastructure expansion across emerging economies are unlocking high-margin opportunities for luxury vinyl tile manufacturers. Recycled-content SPC flooring improved material efficiency by 19%, while advanced digital embossing technologies enhanced premium product customization by over 24% during 2025. Rapid urban housing development across Southeast Asia, the Middle East, and Latin America is accelerating demand for cost-efficient, waterproof, and low-maintenance flooring systems. Smart acoustic flooring and antimicrobial surface coatings are creating non-obvious upside in healthcare and hospitality construction segments where performance standards continue tightening. Companies are positioning for long-term dominance through R&D partnerships, regional manufacturing investments, and vertically integrated supply ecosystems. The shift toward phthalate-free and recyclable flooring portfolios is also strengthening access to institutional procurement programs globally.

Maintaining product consistency, recycling scalability, and installation performance across high-volume projects remains a major challenge for luxury vinyl tile manufacturers. Quality deviations in rigid-core flooring production can increase material rejection rates by 11%, while inconsistent subfloor preparation contributes to installation failure risks exceeding 14% in large commercial projects. Rising energy costs and stricter emissions regulations are also constraining manufacturing efficiency, particularly across export-dependent production hubs. These pressures threaten long-term pricing competitiveness and supply reliability as buyers increasingly demand certified sustainable flooring products. To remain competitive, companies must accelerate automation investment, strengthen installer training ecosystems, and expand recycling infrastructure partnerships. Advanced quality-control systems and regional production diversification are becoming essential for sustaining operational resilience and long-term market credibility.

32% Faster Installation Cycles Reshaping Commercial Flooring Deployment Click-lock luxury vinyl tile systems are reducing installation timelines by 32% across office renovation and hospitality retrofit projects, while labor dependency declined nearly 18% during 2025. Contractors are shifting toward pre-attached underlayment formats to optimize turnaround speed amid skilled labor shortages in North America and Europe. Manufacturers are expanding modular flooring inventories and regional warehousing networks to secure faster project fulfillment and reduce installation disruption for high-traffic commercial facilities.

27% Increase in Recycled Material Integration Redefining Product Portfolios Flooring manufacturers increased recycled polymer usage by 27% across premium luxury vinyl tile lines as low-emission regulations and procurement standards tightened globally. Phthalate-free flooring adoption exceeded 38% in institutional construction projects, forcing suppliers to redesign formulations and restructure sourcing partnerships. A non-obvious shift is emerging where recycled-content products are now positioned as premium offerings rather than low-cost alternatives, improving supplier margins while strengthening compliance positioning across healthcare and education projects.

21% Expansion in Regional Manufacturing Shifting Global Supply Chains Companies accelerated regional production deployment by 21% following Red Sea shipping disruptions and volatile freight costs. North American and European flooring suppliers are reducing dependency on long-distance imports through localized SPC manufacturing and automated cutting facilities. Production lead times improved by 16%, while inventory variability dropped nearly 14%. This operational restructuring is optimizing contractor reliability but simultaneously increasing competitive pressure on low-cost export-focused manufacturers across Asia.

35% Growth in Digital Surface Customization Transforming Buyer Preferences Advanced digital embossing and AI-assisted texture mapping expanded by 35% across premium flooring production lines during 2025–2026. Commercial buyers increasingly demand customized wood-stone visuals with enhanced scratch resistance and acoustic performance, particularly in retail and hospitality interiors. Flooring producers are responding through rapid-batch manufacturing, strategic design partnerships, and digitally controlled printing systems that reduce sample development time by 24%, reshaping product differentiation and accelerating premium flooring conversion rates.

The luxury vinyl tiles market is segmented by type, application, and end-user, with rigid core and click-lock tiles collectively accounting for over 52% of total product demand due to durability and rapid installation efficiency. Commercial flooring and residential flooring dominate application usage, representing nearly 61% combined demand as renovation activity accelerates across urban infrastructure projects. Demand is increasingly shifting toward healthcare facilities, hospitality interiors, and office renovation segments where waterproof, low-maintenance flooring delivers measurable operational benefits. Commercial buildings and residential sectors remain the largest end-users, while educational institutions and healthcare facilities are expanding adoption through low-VOC compliance requirements and faster replacement cycles, reshaping supplier product positioning and regional manufacturing priorities globally.

Rigid Core tiles dominate the luxury vinyl tiles market with nearly 34% share due to superior dimensional stability, waterproof performance, and scalability across high-traffic commercial environments. Their structural durability and compatibility with automated installation systems are accelerating deployment across healthcare, retail, and multifamily renovation projects. Click-Lock Tiles represent the fastest-growing segment, expanding by approximately 18% during 2025 as contractors prioritize faster installation cycles and lower labor dependency. Compared with Flexible Vinyl Tiles, click-lock systems reduce installation time by nearly 30%, redefining project execution economics in commercial renovation markets. Glue-Down Tiles continue maintaining relevance in large-format retail and office renovation projects where permanent adhesion and long lifecycle performance remain critical. Loose Lay Tiles and Flexible Vinyl Tiles collectively contribute around 29% market share, serving cost-sensitive residential remodeling and temporary commercial interior applications. Manufacturers are increasingly prioritizing rigid-core SPC expansion, digital embossing upgrades, and modular installation technologies to capture premium commercial demand while gradually reducing focus on lower-margin conventional flexible formats. Strategic investment is shifting toward high-durability and rapid-installation product categories where replacement cycles are accelerating globally.

Commercial Flooring leads the luxury vinyl tiles market with approximately 33% share as businesses prioritize durable, waterproof, and low-maintenance flooring solutions for high-traffic environments. Usage concentration remains strongest across retail chains, healthcare facilities, and office renovation projects where lifecycle cost optimization and rapid installation directly affect operational continuity. Hospitality Interiors represent the fastest-growing application segment, recording nearly 17% deployment growth during 2025 due to accelerated hotel refurbishment programs and rising demand for premium acoustic flooring systems. Compared with Residential Flooring, commercial applications increasingly favor rigid-core and click-lock formats because they reduce replacement downtime by nearly 24%. Retail Spaces, Healthcare Facilities, and Office Renovation collectively contribute over 41% of application demand as institutional buyers tighten low-VOC procurement standards and prioritize modular installation efficiency. Companies are responding by scaling antimicrobial flooring portfolios, strengthening regional distribution partnerships, and launching digitally customized surface designs tailored for commercial interior projects. Demand is clearly shifting toward specialized, performance-driven flooring applications where durability, installation speed, and compliance standards now determine supplier competitiveness.

Commercial Buildings remain the dominant end-user segment with nearly 36% share due to continuous renovation activity, high flooring replacement frequency, and growing demand for durable modular flooring systems. Large office complexes, mixed-use developments, and retail infrastructure projects rely heavily on luxury vinyl tiles because they reduce maintenance costs while supporting faster installation schedules. Healthcare Facilities represent the fastest-growing end-user category, expanding by approximately 19% during 2025 as hospitals and outpatient centers prioritize antimicrobial, waterproof, and low-VOC flooring environments. Compared with the Residential Sector, healthcare and hospitality buyers increasingly favor premium rigid-core products that improve acoustic control and operational durability under intensive daily usage. The Hospitality Industry, Retail Industry, and Educational Institutions collectively account for nearly 39% of end-user demand, supported by renovation-driven procurement and stricter indoor environmental standards. Manufacturers are targeting these segments through customized pricing programs, design-focused product differentiation, and strategic contractor partnerships. Demand is shifting toward institutional buyers requiring certified sustainable flooring systems, forcing suppliers to optimize compliance-driven production and localized distribution capabilities.

Asia-Pacific accounted for the largest market share at 41% in 2025 however, North America is expected to register the fastest growth, expanding at a CAGR of 6.3% between 2026 and 2033.

Asia-Pacific leads global luxury vinyl tiles production and consumption through large-scale manufacturing capacity, cost-efficient SPC flooring exports, and accelerating urban infrastructure projects across China, India, and Southeast Asia. North America represents nearly 29% market share, driven by renovation-focused commercial flooring demand and rapid adoption of click-lock installation systems reducing project timelines by 30%. Europe contributes approximately 22% demand share while leading in recyclable flooring adoption and low-VOC compliance integration across institutional construction. Supply chain restructuring following Red Sea freight disruptions has accelerated regional manufacturing diversification and localized inventory expansion globally. Companies are increasingly prioritizing Asia-Pacific for scale, North America for premium renovation demand, and Europe for compliance-driven product innovation and sustainable flooring differentiation.

North America holds nearly 29% of global luxury vinyl tiles demand, supported by aggressive commercial renovation activity and rising replacement cycles across healthcare, retail, and office interiors. Waterproof rigid-core flooring adoption exceeded 46% in institutional renovation projects during 2025 as contractors prioritized faster installation and lower maintenance costs. Supply chain regionalization and freight cost volatility are accelerating localized SPC flooring production across the United States and Mexico. Manufacturers expanded automated flooring capacity by approximately 18% to reduce lead times and improve inventory reliability. Enterprise buyers increasingly prefer click-lock systems that shorten installation timelines by nearly 30% while minimizing labor dependency. Companies are prioritizing this region because premium renovation demand, operational efficiency requirements, and localized manufacturing incentives continue strengthening long-term competitive positioning.

Europe accounts for nearly 22% of global luxury vinyl tiles demand, led by Germany, France, and the United Kingdom where institutional construction increasingly prioritizes recyclable and low-VOC flooring systems. More than 39% of commercial procurement contracts now include sustainability-linked flooring specifications, forcing manufacturers to redesign material formulations and expand recycled polymer integration. Compliance-driven production upgrades improved manufacturing efficiency by 14% across several advanced flooring facilities during 2025. Enterprise buyers increasingly favor certified acoustic and phthalate-free flooring products to align with environmental performance standards and indoor air quality requirements. Flooring suppliers are accelerating regional partnerships and localized warehousing strategies to strengthen compliance responsiveness. This region is forcing global manufacturers to innovate faster in sustainable flooring engineering and premium product differentiation.

Asia-Pacific dominates the luxury vinyl tiles market with approximately 41% share, driven by large-scale manufacturing operations and rapid urban infrastructure development across China, India, Vietnam, and South Korea. China alone contributes over one-third of global SPC flooring exports due to integrated PVC processing ecosystems and lower production costs. Automated flooring plants increased production throughput by nearly 23% during 2025, enabling faster delivery cycles for residential and commercial construction projects. Contractors and distributors increasingly prioritize scale, pricing efficiency, and rapid inventory availability over customized premium specifications. Several manufacturers expanded regional production capacity by more than 16% to capture accelerating demand from commercial renovation and multifamily housing sectors. Asia-Pacific remains strategically critical because it combines manufacturing scale, export strength, and expanding domestic flooring consumption simultaneously.

South America represents nearly 6% of global luxury vinyl tiles demand, with Brazil and Argentina leading regional consumption through retail renovation, hospitality upgrades, and urban housing projects. Commercial flooring demand increased by approximately 13% during 2025 as developers shifted toward lower-maintenance interior materials with faster installation capabilities. However, import dependency and currency volatility continue constraining large-scale flooring procurement and pricing stability across several regional markets. Companies are responding by strengthening localized distribution partnerships and expanding mid-range product portfolios optimized for cost-sensitive buyers. Click-lock flooring adoption rose nearly 17% in commercial renovation projects because contractors seek reduced labor intensity and shorter installation timelines. The region offers strong replacement-driven opportunity, but operational success depends on pricing flexibility, supply reliability, and localized market execution strategies.

The Middle East & Africa region contributes nearly 8% of global luxury vinyl tiles demand, supported by expanding hospitality infrastructure, commercial construction, and mixed-use urban development projects across the UAE, Saudi Arabia, and South Africa. Large-scale infrastructure modernization programs increased premium flooring deployment by approximately 15% during 2025, particularly in hotels, airports, and healthcare facilities. Governments and private developers are accelerating investments in rapid-construction interior solutions that reduce project completion timelines and long-term maintenance costs. Waterproof SPC flooring adoption expanded by nearly 19% as contractors prioritized durability under high-traffic commercial usage conditions. Regional buyers increasingly favor modular flooring systems offering faster installation and lower operational disruption. This region is emerging strategically because infrastructure diversification and premium construction activity continue reshaping institutional flooring demand patterns.

China – Holds approximately 34% share of the global Luxury Vinyl Tiles market due to large-scale SPC flooring production capacity, integrated supply chains, and strong export-driven manufacturing ecosystems.

United States – Accounts for nearly 21% share of the Luxury Vinyl Tiles market driven by high commercial renovation demand, rapid click-lock flooring adoption, and strong institutional replacement activity.

The luxury vinyl tiles market is dominated by competition between global flooring leaders such as Shaw Industries, Mohawk Industries, Tarkett, Interface, and Gerflor against regional manufacturers focused on low-cost SPC and click-lock flooring production. The top five players collectively control nearly 38% market share, leveraging scale, distribution reach, and vertically integrated supply chains. Competition is increasingly centered on installation speed, recycled material integration, and premium surface customization, with advanced digital printing technologies improving production efficiency by 18% and reducing material wastage by 15%. Leading companies are accelerating regional manufacturing expansion, contractor partnerships, and automated flooring investments to strengthen inventory responsiveness and pricing control. Consolidation and supply chain localization are reshaping competitive dynamics as freight volatility pressures import-dependent suppliers. High capital requirements, compliance-driven product redesign, and distribution network complexity remain major entry barriers. Winning requires localized production, sustainable flooring innovation, rapid delivery capability, and strong commercial contractor relationships.

Shaw Industries Group, Inc.

Mohawk Industries, Inc.

Tarkett S.A.

Interface, Inc.

Gerflor Group

Mannington Mills, Inc.

Forbo Holding AG

Armstrong Flooring Inc.

NOX Corporation

LG Hausys

Beaulieu International Group

Milliken & Company

Polyflor Ltd.

Responsive Industries Ltd.

Advanced rigid-core SPC technology currently dominates premium luxury vinyl tile manufacturing due to higher dimensional stability, waterproof performance, and installation efficiency across commercial renovation projects. SPC flooring systems improve impact resistance by nearly 26% while reducing maintenance interventions by 19% compared with conventional flexible vinyl flooring. More than 48% of newly deployed commercial luxury vinyl tile installations now integrate click-lock SPC structures, particularly across healthcare and retail projects. Manufacturers are increasingly combining automated embossing, digital printing, and modular installation technologies to optimize production speed and reduce material waste, strengthening contractor preference for rapid-installation flooring systems.

Emerging technologies are reshaping product differentiation through AI-assisted texture mapping, phthalate-free polymer engineering, and recycled-content integration. Digital surface customization reduced product development timelines by approximately 24% during 2025–2026 while increasing premium flooring conversion rates across hospitality interiors. Recycled-content luxury vinyl tiles now exceed 35% adoption in several institutional procurement programs as compliance-driven buyers prioritize low-emission flooring systems. Compared with legacy laminate flooring, digitally engineered luxury vinyl tiles improve acoustic insulation by 21% and reduce replacement frequency through enhanced scratch resistance and structural durability.

Disruptive innovation between 2026 and 2028 is centered on PVC-free resilient flooring, closed-loop recycling systems, and smart acoustic flooring layers integrated with modular construction ecosystems. Premium manufacturers deploying recyclable flooring technologies are securing faster institutional approvals and reducing lifecycle disposal costs by nearly 18%. Global leaders with localized automated production and sustainable flooring portfolios are gaining competitive advantage, while low-cost manufacturers dependent on traditional vinyl formats face rising compliance pressure and shrinking premium-market access.

October 2024 – Shaw Industries announced a USD 90 million expansion of its Ringgold resilient flooring facility, more than doubling SPC and LVT production capacity by 2026 while adding advanced embossing and loose-lay product capabilities. The investment strengthens domestic supply reliability and reduces lead-time exposure across North American commercial flooring projects. [Capacity Scale-Up] Source: Shaw Industries

November 2024 – Shaw Industries launched EcoWorx Resilient, a fully recyclable and PVC-free resilient flooring platform for commercial interiors, improving sustainability positioning across institutional procurement markets. The product line supports circular flooring recovery programs and addresses rising low-emission compliance demand in healthcare and office renovation sectors. [Circular Flooring Push] Source: Shaw Industries Press Release

October 2024 – PPG and Shaw Industries entered a strategic agreement to distribute PPG FLOORING resinous flooring solutions through Shaw’s Patcraft commercial network, expanding product reach across industrial and workplace environments. The partnership strengthens portfolio diversification and accelerates access to high-durability flooring applications requiring enhanced chemical and wear resistance. [Strategic Channel Alliance] Source: PPG Investor Relations

April 2025 – Shaw Industries reported that nearly 90% of its flooring portfolio achieved Cradle to Cradle certification benchmarks while operational carbon emissions declined by 64% versus 2010 levels. The company also expanded recyclable flooring integration, reinforcing sustainability-led differentiation across commercial luxury vinyl tile procurement programs. [ESG Manufacturing Shift] Source: Floor Covering News

This report delivers comprehensive coverage of the global luxury vinyl tiles market across product types, applications, end-user industries, regional demand structures, and technology deployment trends. The analysis includes rigid core, flexible vinyl tiles, glue-down, click-lock, and loose lay formats while evaluating demand across residential flooring, commercial flooring, healthcare facilities, retail spaces, hospitality interiors, and office renovation projects. Geographic assessment spans North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, with focused evaluation of production concentration, procurement shifts, and regional manufacturing expansion. Key technologies covered include SPC flooring systems, AI-driven digital embossing, recyclable polymers, PVC-free resilient flooring, and modular installation platforms.

The report analyzes more than 15 strategic market indicators, including adoption intensity, installation efficiency gains, regional production concentration, and sustainability integration trends. Rigid-core flooring systems currently account for over 34% of product deployment, while commercial applications contribute nearly one-third of total demand. Institutional procurement programs integrating recyclable or low-VOC flooring standards exceeded 39% across developed construction markets during 2025. The study also profiles major global manufacturers, competitive positioning strategies, supply chain restructuring patterns, and operational shifts shaping 2026–2033 market direction. The report supports investment planning, product portfolio optimization, regional expansion decisions, and long-term competitive positioning for manufacturers, distributors, contractors, and institutional flooring buyers.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 10971.66 Million |

|

Market Revenue in 2033 |

USD 17095.12 Million |

|

CAGR (2026 - 2033) |

5.7% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Shaw Industries Group, Inc., Mohawk Industries, Inc., Tarkett S.A., Interface, Inc., Gerflor Group, Mannington Mills, Inc., Forbo Holding AG, Armstrong Flooring Inc., NOX Corporation, LG Hausys, Beaulieu International Group, Milliken & Company, Polyflor Ltd., Responsive Industries Ltd. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |