Reports

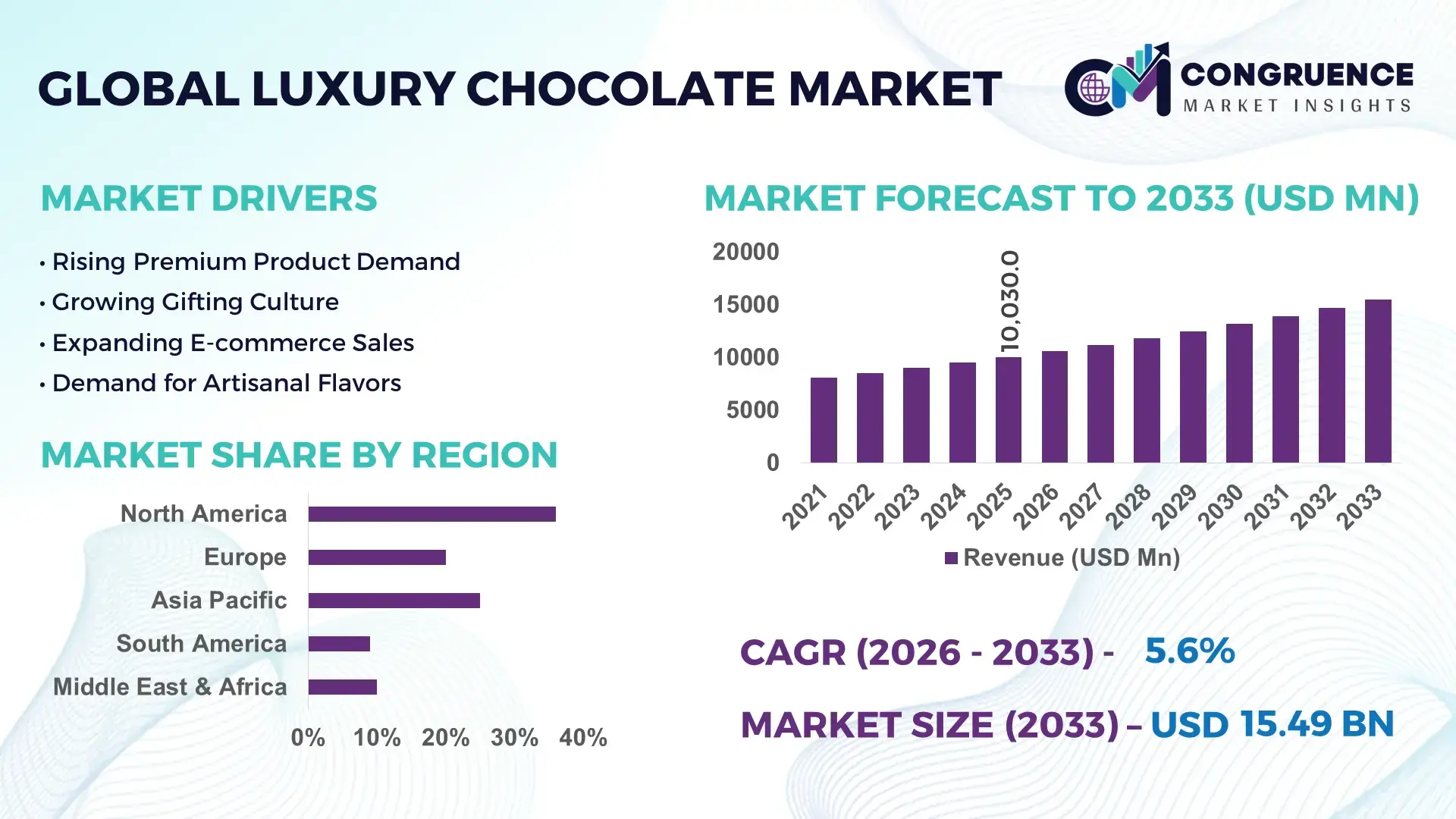

The Global Luxury Chocolate Market was valued at USD 10030 Million in 2025 and is anticipated to reach a value of USD 15486.53 Million by 2033 expanding at a CAGR of 5.58% between 2026 and 2033. Growth is being driven by premium cocoa sourcing programs, single-origin product expansion, artisanal product innovation, sustainable packaging adoption, and increasing penetration of luxury confectionery through digital retail channels.

Switzerland remains the dominant country in the luxury chocolate market, accounting for approximately 18% of global premium chocolate production capacity in 2026, supported by advanced manufacturing technologies and high-value export networks. Compared with Belgium, which contributes nearly 12% of premium production volumes, Swiss manufacturers invest more heavily in precision processing and traceability systems, improving production consistency by over 20%. Ongoing supply-chain adjustments linked to cocoa sourcing challenges in West Africa have accelerated investments in diversified procurement strategies and premium ingredient security.

Companies prioritizing premium sourcing resilience, manufacturing efficiency, and brand differentiation are positioned to strengthen market share in the evolving global luxury chocolate landscape.

Market Size & Growth: USD 10030 Million (2025) to USD 15486.53 Million (2033) at 5.58% CAGR, supported by premiumization, digital luxury retail expansion, and traceable cocoa sourcing initiatives.

Top Growth Drivers: Premium gifting demand (+24%), sustainable cocoa sourcing adoption (+19%), and direct-to-consumer luxury sales growth (+21%).

Short-Term Forecast: By 2028, premium chocolate production efficiency improves by 12% through automation and advanced quality-control systems.

Emerging Technologies: AI-driven demand forecasting, smart packaging, and digital traceability platforms reduce inventory losses by approximately 10%.

Regional Leaders: Europe exceeds USD 6.2 Billion, North America approaches USD 3.8 Billion, and Asia-Pacific surpasses USD 3.1 Billion, driven by premium product adoption.

Consumer/End-User Trends: More than 42% of luxury chocolate buyers prioritize single-origin, ethical, and limited-edition product offerings.

Pilot/Case Example: In 2026, premium manufacturers deploying AI forecasting achieved inventory optimization improvements of nearly 15%.

Competitive Landscape: Leading brands collectively control roughly 35% market share, supported by premium portfolios, innovation, and global distribution networks.

Regulatory & ESG Impact: Sustainable sourcing programs improve certified cocoa procurement rates by approximately 18% across premium supply chains.

Investment & Funding: More than USD 1.4 Billion supports facility expansion, premium product development, and regional manufacturing upgrades.

Innovation & Future Outlook: Advanced personalization, bean-to-bar transparency, and premium wellness formulations are reshaping long-term competitive positioning.

Luxury chocolate demand is increasingly concentrated in premium gifting, gourmet retail, hospitality, and direct-to-consumer channels. Manufacturers are introducing single-origin collections, reduced-sugar premium formulations, and digitally traceable cocoa sourcing systems to strengthen differentiation. Approximately 38% of new premium product launches emphasize sustainability credentials, while cocoa supply-chain diversification initiatives respond to sourcing volatility and regulatory scrutiny, setting the stage for broader strategic market developments.

Luxury chocolate is evolving from a premium confectionery category into a strategic value-added segment shaped by brand differentiation, ethical sourcing, and advanced manufacturing capabilities. Competitive intensity is increasing as manufacturers invest in traceable cocoa networks, personalized product offerings, and premium retail experiences. A notable market shift is the restructuring of cocoa supply chains following sourcing disruptions in West Africa, prompting greater investment in diversified procurement and vertically integrated sourcing models.

Technology adoption is improving operational efficiency across production and distribution. AI-enabled demand forecasting systems reduce inventory imbalances by approximately 12% compared with conventional planning methods, while automated tempering and packaging lines improve production consistency by nearly 18%. Switzerland maintains leadership in premium manufacturing and export quality, whereas Japan is advancing product innovation through functional ingredients and precision flavor development. These differences highlight distinct competitive pathways based on scale, craftsmanship, and innovation intensity.

Over the next two to three years, premium traceability programs are expected to cover more than 40% of luxury chocolate product portfolios. Manufacturers are expanding partnerships with certified cocoa cooperatives and investing in digital supply-chain visibility platforms. Companies that combine sourcing resilience, product innovation, and operational efficiency will secure stronger brand equity and long-term competitive positioning in the global luxury chocolate market.

Premium product premiumization is accelerating demand as consumers increasingly prioritize origin transparency, ingredient quality, and artisanal production standards. More than 45% of luxury chocolate launches now emphasize single-origin cocoa, while certified sustainable cocoa adoption has increased by approximately 20% across premium portfolios. Supply-chain restructuring linked to cocoa availability challenges in Côte d’Ivoire and Ghana has encouraged manufacturers to secure direct sourcing relationships with producer cooperatives. This shift improves ingredient consistency and strengthens brand differentiation. In response, leading companies are expanding bean-to-bar operations, investing in traceability technologies, and forming long-term procurement partnerships. A key operational insight is that direct sourcing models can improve supply visibility by over 15%, creating stronger inventory planning and premium pricing leverage.

Luxury chocolate manufacturers face persistent pressure from cocoa supply concentration and commodity price fluctuations. Nearly 60% of global cocoa production remains concentrated in a limited number of producing countries, increasing exposure to climate variability and crop disruptions. In recent periods, cocoa procurement costs have experienced fluctuations exceeding 30%, affecting premium product margins and pricing strategies. Regulatory requirements related to supply-chain transparency further increase compliance expenditures for exporters and processors. Companies are mitigating these constraints through supplier diversification, multi-year procurement contracts, and expanded sourcing programs in Latin America. A significant operational challenge is maintaining premium quality standards while controlling input costs, requiring greater investment in procurement intelligence and supply-chain risk management capabilities.

Emerging opportunities are being created through functional luxury chocolate formulations, personalized product development, and advanced digital retail models. Approximately 35% of premium consumers actively seek products incorporating wellness-oriented ingredients such as botanicals, high-cocoa-content formulations, and reduced-sugar recipes. AI-driven consumer analytics can improve new product targeting efficiency by nearly 15%, enabling faster commercialization cycles. Japan and South Korea are demonstrating strong adoption of premium functional confectionery concepts, creating attractive expansion pathways. Companies are increasing investments in R&D, direct-to-consumer platforms, and premium subscription models to capture higher-margin demand. A non-obvious opportunity lies in leveraging digital traceability systems as both a compliance tool and a premium branding asset that strengthens customer loyalty and product differentiation.

Maintaining consistent luxury quality standards across expanding international operations remains a critical challenge. Premium chocolate production requires strict control of roasting, conching, tempering, and ingredient sourcing variables, with quality deviations as small as 5% affecting sensory performance and consumer perception. Workforce specialization gaps in emerging manufacturing locations can extend training requirements by 20% or more compared with established production hubs such as Switzerland. Additionally, growing traceability and sustainability requirements increase operational complexity across multi-country supply chains. Companies must invest in digital quality-control systems, workforce development programs, and standardized manufacturing protocols to maintain brand integrity. The strongest strategic performers will be those capable of scaling premium production while preserving craftsmanship, traceability, and operational consistency across global distribution networks.

• Digital Traceability Becoming Standard Premium manufacturers are rapidly expanding digital traceability systems across cocoa procurement networks. More than 40% of newly launched luxury chocolate collections now include origin-verification features, while blockchain-enabled sourcing programs have improved supply-chain visibility by approximately 18%. Regulatory scrutiny on sustainable sourcing and cocoa traceability is accelerating deployment. Companies are responding through direct farmer partnerships, digital certification platforms, and procurement restructuring, reducing verification delays and strengthening premium brand positioning in export-focused markets such as Switzerland and Belgium.

• Functional Indulgence Product Expansion Luxury chocolate portfolios are increasingly incorporating wellness-oriented formulations. Products featuring high-cocoa content, botanical extracts, and reduced-sugar recipes account for nearly 30% of premium product innovation activity. Consumer trial rates for functional luxury confectionery have increased by over 15% in Japan and South Korea. Manufacturers are investing in ingredient science, precision formulation technologies, and specialty supplier partnerships. The operational benefit extends beyond differentiation, as higher-value functional products support stronger margin retention despite ingredient cost pressures.

• Automation Enhancing Craft Production Premium chocolate producers are integrating automated tempering, packaging, and quality-inspection systems without compromising artisanal positioning. Automated quality-control deployment has increased by approximately 20%, reducing batch variability by nearly 12%. Labor availability constraints in European manufacturing hubs are driving this transition. Companies are scaling smart factory investments and integrating AI-assisted production monitoring, improving consistency while preserving handcrafted product characteristics that remain critical for premium category competitiveness.

• Personalized Gifting Driving Demand Advanced customization capabilities are reshaping premium purchasing behavior. Customized packaging and limited-edition product programs have increased conversion rates by approximately 17%, while direct-to-consumer premium orders have expanded by nearly 22%. Enterprise gifting programs and luxury seasonal collections are becoming operational priorities. Companies are strengthening digital commerce platforms, expanding fulfillment partnerships, and adopting data-driven personalization tools. A notable trend is the growing use of consumer preference analytics to optimize premium assortment planning and reduce product development cycle times.

Dark Chocolate remains the leading segment due to its strong premium positioning, higher cocoa content, and alignment with quality-focused consumer preferences. The segment accounts for an estimated 40% of luxury chocolate demand, supported by scalable production capabilities and increasing adoption in wellness-oriented premium offerings. Manufacturers continue expanding single-origin and high-cocoa-content portfolios to strengthen differentiation. Milk Chocolate maintains broad consumer appeal and remains a mature volume contributor, particularly in gifting and family-oriented consumption categories. White Chocolate retains strategic relevance through flavor innovation and seasonal product applications.

Organic Chocolate is the fastest-growing type as sustainability, traceability, and clean-label purchasing behavior reshape premium consumption. Adoption of certified cocoa ingredients has increased by approximately 20%, encouraging manufacturers to expand sourcing partnerships and certification programs. Filled Chocolate is also gaining traction through premium flavor combinations and experiential product formats. Companies are prioritizing product innovation, premium ingredient sourcing, and portfolio diversification to capture evolving demand. Investment is increasingly shifting toward organic and high-cocoa-content products, reflecting changing consumer expectations around authenticity and product transparency.

Gifting remains the leading application segment, accounting for approximately 35% of luxury chocolate demand as premium packaging, personalization, and seasonal purchasing support high-value transactions. Luxury brands continue investing in limited-edition collections and premium presentation formats to strengthen gifting appeal. Personal Consumption remains a significant contributor, supported by increasing preference for premium indulgence and specialty chocolate experiences. Seasonal Products maintain relevance through holiday-driven purchasing cycles, generating concentrated demand peaks that require flexible production planning and inventory management.

Corporate Gifting is emerging as the fastest-growing application, supported by digital ordering platforms and customized branding capabilities. Corporate procurement activity for premium confectionery solutions has increased by nearly 18%, encouraging manufacturers to expand dedicated business-to-business product lines. Premium Desserts are also creating opportunities through hospitality partnerships and gourmet foodservice integration. Companies are responding through automation, personalization technologies, and expanded fulfillment capabilities. Demand is increasingly shifting toward customized and experience-focused applications, making flexible production and rapid product adaptation strategically important.

Retail Stores remain the dominant end-user segment due to extensive distribution infrastructure, premium shelf visibility, and established consumer purchasing patterns. The segment represents approximately 38% of luxury chocolate sales volumes and continues benefiting from premium merchandising strategies. Specialty Stores maintain strong relevance through curated product portfolios and brand storytelling capabilities that reinforce premium positioning. Hotels and Restaurants support demand through gourmet dining experiences and premium dessert offerings, while Duty-Free Shops benefit from international travel recovery and premium impulse purchases.

Online Retailers represent the fastest-growing end-user group, with premium chocolate e-commerce transactions increasing by nearly 22% as consumers seek convenience, personalization, and direct brand engagement. Companies are investing in digital storefronts, subscription programs, and advanced fulfillment networks to support this shift. Corporate Buyers are expanding procurement volumes through customized gifting programs and employee engagement initiatives. Manufacturers are increasingly adopting channel-specific pricing strategies, exclusive product launches, and strategic partnerships to optimize performance across distribution ecosystems. Future demand is steadily migrating toward digitally enabled purchasing environments supported by data-driven customer engagement.

Europe accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 7.1% between 2026 and 2033.

Premium Personalization and Direct-to-Consumer Expansion

North America represents approximately 27% of global luxury chocolate demand, supported by premium gifting culture, advanced retail infrastructure, and strong direct-to-consumer penetration. The United States and Canada continue expanding premium confectionery offerings through digital commerce platforms and customized product formats. More than 30% of premium chocolate launches now incorporate personalization features, while automated packaging investments have improved fulfillment efficiency by nearly 15%. Enterprise gifting programs and subscription-based premium chocolate services are becoming important growth channels. Manufacturers are strengthening logistics partnerships and investing in consumer analytics to optimize product assortment, inventory planning, and customer retention strategies.

United States Market Outlook: The United States remains the region’s most influential market due to its extensive premium retail ecosystem, advanced e-commerce infrastructure, and strong luxury gifting demand. Digital premium confectionery purchases have increased by more than 20% over recent years, encouraging brands to invest in customization technologies and fulfillment networks. Companies are also expanding premium seasonal collections and direct sourcing initiatives to improve product differentiation and supply-chain resilience.

Manufacturing Excellence and Sustainable Sourcing Leadership

Europe maintains the leading position in the luxury chocolate market, accounting for roughly 38% of global consumption and production activity. The region benefits from established premium chocolate heritage, advanced manufacturing capabilities, and strict sustainability standards. Traceable cocoa sourcing programs now cover more than 40% of premium product portfolios across major producers. Regulatory emphasis on supply-chain transparency is accelerating investment in digital traceability systems and supplier monitoring platforms. Manufacturers continue modernizing facilities and strengthening direct cocoa procurement relationships to improve sourcing stability and premium product positioning.

Switzerland Market Outlook: Switzerland remains a global benchmark for luxury chocolate production through precision manufacturing, premium ingredient sourcing, and strong export orientation. The country contributes nearly one-fifth of global premium chocolate production capacity and continues investing in automated quality-control systems. Swiss producers emphasize high-cocoa-content formulations, single-origin offerings, and advanced traceability frameworks, reinforcing their leadership in premium product consistency and international brand value.

Premium Consumption Scaling Across Urban Markets

Asia-Pacific accounts for approximately 22% of global luxury chocolate demand and is experiencing rapid premiumization across urban consumer segments. Rising disposable income, expanding luxury retail infrastructure, and digital commerce adoption are strengthening market penetration. Premium chocolate imports and specialty product launches have increased by nearly 18%, while online premium confectionery transactions continue expanding at double-digit rates. Manufacturers are increasing local packaging capabilities, forming regional distribution partnerships, and introducing products tailored to local flavor preferences. Operational investments increasingly focus on premium retail experiences and digital customer engagement.

Japan Market Outlook: Japan serves as the region’s most strategically significant luxury chocolate market due to advanced product innovation, premium gifting traditions, and sophisticated retail channels. More than 25% of premium product launches incorporate functional ingredients or unique flavor concepts. Companies continue investing in specialty retail formats, precision manufacturing technologies, and seasonal premium collections, enabling strong product differentiation and premium category expansion without relying solely on imported offerings.

Origin-Based Premium Positioning Gains Momentum

South America represents approximately 8% of the global luxury chocolate market and benefits from proximity to major cocoa-producing regions. Premium manufacturers are increasingly leveraging origin-based branding strategies and specialty cocoa varieties to differentiate products. Export-oriented premium chocolate production has expanded by nearly 12%, supported by investments in processing facilities and quality certification programs. However, logistics constraints and infrastructure disparities continue affecting distribution efficiency. Companies are responding through local processing expansion, farmer partnerships, and cocoa traceability initiatives that strengthen premium positioning and export competitiveness.

Brazil Market Outlook: Brazil leads the regional market through its integrated cocoa value chain, growing premium manufacturing capacity, and expanding domestic premium consumption. Investments in specialty cocoa cultivation and premium processing technologies have increased substantially, supporting higher-value product development. Brazilian producers are focusing on single-origin chocolate formats and direct trade relationships, improving product quality while strengthening supply-chain transparency and export opportunities.

Luxury Retail Expansion and Premium Import Investment

The Middle East & Africa region accounts for approximately 5% of global luxury chocolate demand, supported by luxury retail growth, tourism activity, and premium gifting culture. High-end retail formats and duty-free channels are increasing premium product accessibility. Investments in premium food distribution infrastructure have improved product availability by nearly 10% across major urban centers. Companies are expanding partnerships with luxury retailers and hospitality operators to strengthen premium category visibility. While local production remains limited, premium import networks continue supporting category development.

United Arab Emirates Market Outlook: The United Arab Emirates is the region’s leading luxury chocolate market due to its advanced retail infrastructure, international tourism base, and concentration of luxury consumer spending. Premium confectionery distribution through airports, luxury malls, and hospitality venues continues expanding. Companies are utilizing the country as a regional distribution hub, while premium gifting demand and high-end retail penetration support consistent deployment of luxury chocolate brands and exclusive product collections.

The luxury chocolate market is led by premium global brands such as Lindt & Sprüngli, Ferrero, Godiva, Chocoladefabriken Lindt & Sprüngli, and Hotel Chocolat competing against artisanal specialists and regional premium producers. The top five players collectively control approximately 42% of market activity, creating competition between globally integrated manufacturers and niche origin-focused brands. Competitive advantage is increasingly determined by sourcing control, premium product innovation, and personalization capabilities rather than price alone. Companies utilizing direct cocoa procurement models achieve roughly 15% stronger supply visibility, while digital personalization programs improve premium conversion rates by nearly 17%. Vertical integration, sustainable sourcing partnerships, and limited-edition product development are common competitive strategies. A major competitive shift is the growing emphasis on traceability and premium ingredient authentication as supply-chain pressures reshape procurement priorities. The principal entry barrier remains access to premium cocoa networks and established luxury brand equity. Winning requires sourcing resilience, differentiated innovation, and superior premium consumer engagement.

Lindt & Sprüngli

Ferrero

Godiva Chocolatier

Hotel Chocolat

Guylian

Neuhaus

Leonidas

Ghirardelli Chocolate Company

Valrhona

Läderach

Patchi

Amedei

Venchi

Pierre Marcolini Group

Luxury chocolate manufacturers are increasingly deploying AI-driven demand forecasting, automated tempering systems, and digital quality-control platforms to improve operational precision. AI forecasting reduces inventory imbalances by approximately 12%, while automated tempering improves batch consistency by nearly 15% compared with manual processes. More than 35% of premium chocolate facilities now utilize some level of production automation. These technologies help manufacturers reduce waste, optimize premium ingredient utilization, and maintain uniform product quality across expanding global distribution networks.

Emerging technologies are focused on traceability, sustainable sourcing, and personalized product development. Blockchain-enabled cocoa tracking systems improve supply-chain visibility by approximately 18%, while digital product customization platforms increase premium order conversion rates by nearly 17%. Adoption of traceability technologies has surpassed 40% among major premium chocolate producers. Companies benefit through stronger regulatory compliance, improved sourcing transparency, and enhanced consumer trust. Premium brands with direct cocoa procurement networks gain a competitive advantage through greater supply resilience and verified origin credentials.

Disruptive innovation between 2026 and 2028 will center on AI-assisted flavor formulation, smart manufacturing analytics, and advanced sustainable packaging solutions. AI-guided product development shortens formulation cycles by nearly 20% compared with traditional R&D approaches. Early deployment levels remain below 15%, creating a strategic opportunity for innovation leaders. Companies investing now in digital manufacturing ecosystems, ingredient intelligence platforms, and connected supply chains will strengthen premium positioning, accelerate product launches, and improve operational agility as luxury chocolate competition intensifies.

August 2024 – Godiva opened the limited-time GODIVA Laboratory Harajuku innovation concept in Japan, introducing exclusive chef-created chocolate beverages and desserts. The site launched with multiple location-exclusive products, strengthening premium product testing capabilities and accelerating innovation-to-market execution. Source: godiva.co.jp

July 2025 – Lindt & Sprüngli reported 11.2% organic growth in the first half of 2025 while expanding its footprint across India, Saudi Arabia, and Chile. The expansion strengthened premium market penetration and enhanced global retail distribution capabilities in high-potential luxury confectionery markets. Source: lindt-spruengli.com

January 2026 – Hotel Chocolat launched its limited-edition Fire & Ice drinking chocolate featuring 70% dark chocolate, peppermint, and chili, designed for the Velvetiser platform. The innovation expanded premium beverage offerings and reinforced differentiated product positioning within experiential chocolate consumption. Source: foodbev.com

May 2026 – Ferrero Group announced an exclusive global partnership with Netflix alongside the launch of 10 new Wonka seasonal and limited-edition products. The initiative expands premium confectionery engagement opportunities, strengthens brand visibility, and supports multi-category product innovation strategies.

This report provides comprehensive coverage of the luxury chocolate market across product types, applications, end-users, competitive positioning, technology adoption, and regional demand dynamics. The analysis evaluates Dark Chocolate, Milk Chocolate, White Chocolate, Organic Chocolate, and Filled Chocolate while assessing demand across gifting, personal consumption, seasonal products, corporate gifting, and premium desserts. End-user evaluation covers retail stores, specialty stores, hotels and restaurants, online retailers, duty-free shops, and corporate buyers. More than 40% of premium product launches now incorporate traceability, sustainability, or personalization features, highlighting key operational shifts shaping industry priorities.

The study examines North America, Europe, Asia-Pacific, South America, and Middle East & Africa with detailed country-level strategic insights. Coverage includes digital traceability systems, AI-enabled forecasting, manufacturing automation, premium packaging innovation, and sustainable sourcing technologies. The report supports investment planning, expansion strategy, supply-chain optimization, competitive benchmarking, and product portfolio development. It also identifies emerging opportunities in functional luxury chocolate, direct-to-consumer channels, personalized gifting solutions, and premium experiential consumption trends expected to influence market direction between 2026 and 2033.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 10030 Million |

|

Market Revenue in 2033 |

USD 15486.53 Million |

|

CAGR (2026 - 2033) |

5.58% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Lindt & Sprüngli, Ferrero, Godiva Chocolatier, Hotel Chocolat, Guylian, Neuhaus, Leonidas, Ghirardelli Chocolate Company, Valrhona, Läderach, Patchi, Amedei, Venchi, Pierre Marcolini Group |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |