Reports

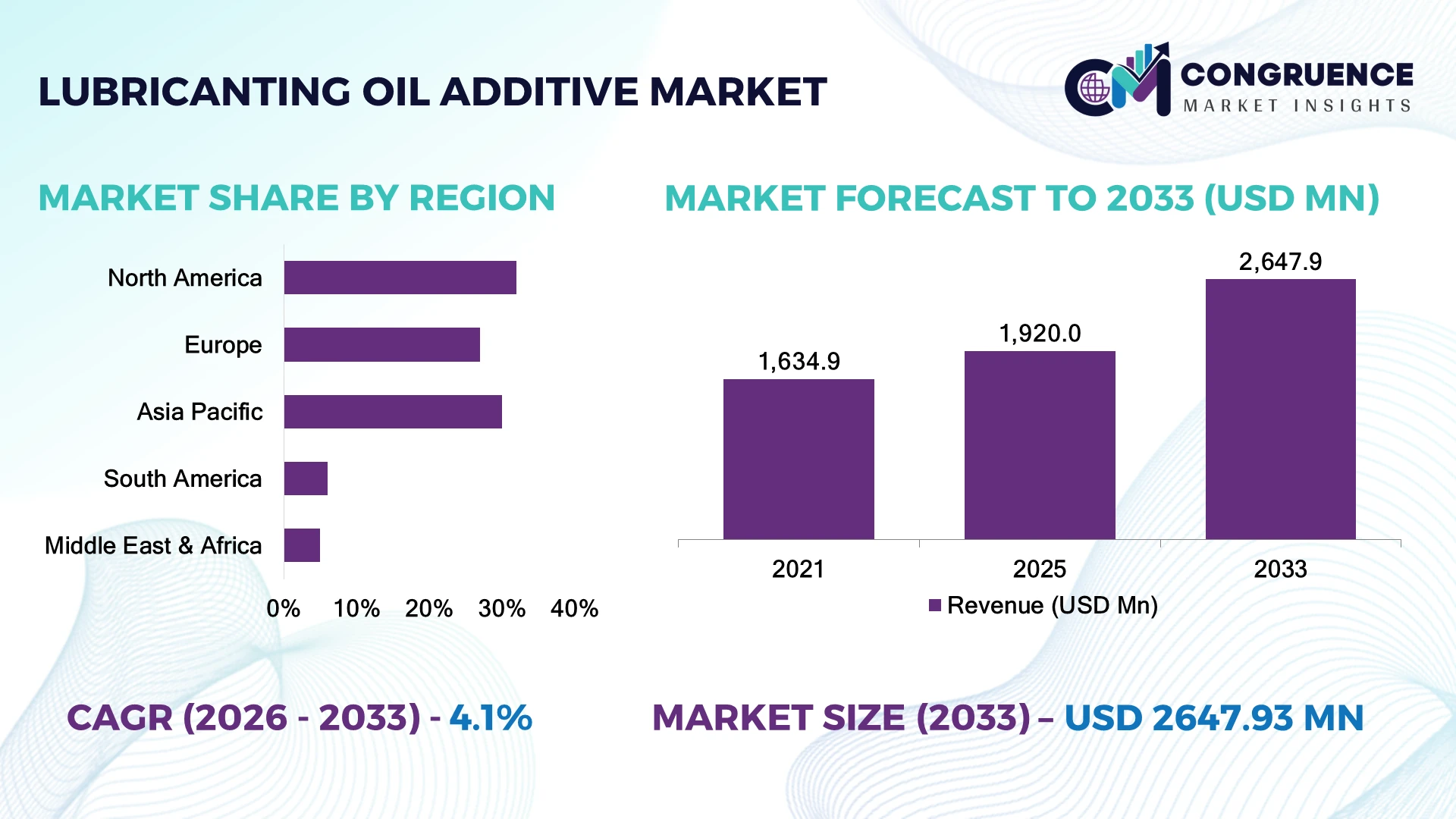

The Global Lubricanting Oil Additive Market was valued at USD 1,920.0 Million in 2025 and is anticipated to reach a value of USD 2,647.9 Million by 2033 expanding at a CAGR of 4.1% between 2026 and 2033. Growth is driven by rising demand for low-emission engine oils, advanced additive packages for fuel efficiency, and stricter vehicle emission standards accelerating lubricant innovation.

The United States leads the market with nearly 28% share, supported by automotive manufacturing, industrial machinery, and refinery investments exceeding USD 50 billion in recent energy infrastructure projects. China follows with over 25% market presence, driven by EV expansion and industrial modernization, while India records faster adoption with lubricant demand increasing across automotive and manufacturing sectors by over 8% annually.

Strategic investments in high-performance additives will strengthen supplier positioning and technology leadership.

Market Size & Growth: Valued at USD 1,920.0 Million in 2025 and reaching USD 2,647.9 Million by 2033 at 4.1% CAGR, driven by advanced engine efficiency requirements.

Top Growth Drivers: Fuel-efficient lubricants 35%, emission compliance 30%, industrial automation 20% shaping market expansion.

Short-Term Forecast: By 2028, additive formulations targeting friction reduction improve lubricant efficiency by 10–15% across automotive applications.

Emerging Technologies: AI-based formulation design, synthetic additive blends, and nanotechnology-enhanced lubricants accelerate product innovation.

Regional Leaders: North America reaches USD 740 Million, Asia Pacific USD 1,050 Million, and Europe USD 620 Million, supported by advanced mobility adoption.

Consumer/End-User Trends: Over 60% of automotive lubricant users prioritize extended drain intervals and improved engine protection.

Pilot/Case Example: 2024 lubricant optimization programs reduced equipment wear by 18% in industrial machinery operations through advanced additive technologies.

Competitive Landscape: Leading suppliers hold significant market influence, with key players including Lubrizol, Infineum, Chevron Oronite, Afton Chemical, and BASF.

Regulatory & ESG Impact: Low-emission lubricant standards support adoption of sustainable formulations, reducing environmental impact by nearly 20% in targeted applications.

Investment & Funding: More than USD 5 billion invested in lubricant technology, refinery upgrades, and specialty chemical expansion projects globally.

Innovation & Future Outlook: Next-generation bio-based additives, EV-compatible lubricants, and digital monitoring solutions are driving strategic industry transformation.

The Lubricanting Oil Additive Market is experiencing stronger demand from automotive electrification, industrial machinery upgrades, and high-performance lubricant applications. Advanced additive technologies are improving thermal stability, wear protection, and fuel economy, with premium lubricant adoption increasing by approximately 15% in developed markets. Supply-chain diversification across Asia and North America is reshaping manufacturing strategies, creating opportunities for specialized additive producers.

The Lubricanting Oil Additive Market is becoming strategically important as industries prioritize equipment efficiency, emission reduction, and longer machinery operating cycles. Automotive manufacturers, energy companies, and industrial operators are restructuring supply chains to secure specialty chemical availability while adapting to stricter environmental regulations and evolving mobility technologies.

Advanced additive formulations are replacing conventional lubricant systems by improving oxidation resistance and reducing maintenance requirements. Modern synthetic additive packages deliver up to 20% better wear protection compared with traditional formulations, enabling longer service intervals and improved operational efficiency. North America emphasizes high-performance automotive and industrial applications, while Asia Pacific leads in production scale and manufacturing expansion.

Companies are increasing investments in research partnerships, localized production facilities, and sustainable formulation development. For example, industrial equipment operators are adopting condition-monitoring systems combined with advanced lubricants to reduce downtime and optimize maintenance schedules. Over the next few years, competitive advantage will depend on technological innovation, supply-chain resilience, and the ability to deliver efficient, environmentally aligned lubricant solutions.

Growing demand for fuel-efficient and low-emission lubricant solutions is accelerating additive innovation across automotive and industrial sectors. Stringent emission regulations in the United States and European Union are pushing manufacturers toward advanced additive packages that improve engine efficiency by 10–15% and reduce friction-related losses by nearly 8%. China’s automotive modernization programs are increasing adoption of high-performance lubricants across commercial vehicles and machinery. Companies are responding through R&D investments, strategic partnerships, and expanded additive production capacity. The shift toward synthetic and hybrid lubricant technologies is creating competitive advantages for suppliers offering customized formulations for next-generation engines and industrial equipment.

Lubricant additive manufacturers face pressure from fluctuating base chemical prices, specialty ingredient dependency, and complex global supply networks. Key raw materials such as dispersants, detergents, and viscosity modifiers experience pricing instability, with chemical input costs fluctuating by 10–20% during supply disruptions. China-based chemical production constraints and geopolitical trade adjustments have affected sourcing strategies for global suppliers. These conditions reduce margin flexibility and increase inventory management challenges for manufacturers. Companies are mitigating risks through supplier diversification, localized production facilities, and long-term procurement agreements to stabilize availability and improve operational resilience.

Rising demand for environmentally optimized lubricants is creating opportunities for bio-based additives, EV-compatible formulations, and smart monitoring technologies. Adoption of sustainable lubricant solutions is increasing, with industrial users targeting 15–25% reductions in maintenance-related waste through improved performance formulations. Japan and Germany are advancing low-emission mobility initiatives, encouraging development of specialized additive technologies. Companies are expanding research collaborations and investing in digital lubricant analysis platforms that enable predictive maintenance. The emerging opportunity lies in integrating additive chemistry with data-driven equipment monitoring, allowing suppliers to move from product sales toward value-based maintenance solutions.

The industry faces execution challenges in developing additives compatible with evolving engine architectures, electric mobility systems, and advanced industrial equipment. More than 30% of new lubricant development efforts require customized testing to meet changing performance standards, increasing formulation complexity and validation costs. Automotive hubs such as Germany, Japan, and the United States are demanding higher-performance solutions for hybrid and specialized machinery applications. Companies must overcome technical barriers through advanced testing facilities, collaborative innovation programs, and skilled workforce development. Long-term competitiveness depends on balancing additive performance, environmental compliance, and scalable manufacturing capabilities across diverse application environments.

Synthetic Additive Transition Accelerates Automotive and industrial users are shifting toward synthetic and semi-synthetic lubricant additives, with adoption increasing by 15–20% in high-performance applications. Manufacturers are optimizing detergent, dispersant, and anti-wear packages to meet tighter engine efficiency requirements. The transition is reducing maintenance cycles by nearly 10% and improving equipment reliability. Companies are expanding specialty additive portfolios and forming technology partnerships to address advanced engine and machinery requirements.

EV Lubricant Development Expands Electric mobility is reshaping additive formulation strategies, with EV-compatible lubricant demand increasing by over 25% across developed automotive markets. Battery thermal management and low-friction component protection are driving new product development. Companies are investing in customized additive chemistries and testing platforms as traditional engine oil demand patterns change. The shift is creating new opportunities for suppliers focused on thermal stability and specialized fluid performance.

Digital Monitoring Integration Grows Industrial operators are adopting smart lubricant monitoring systems, improving maintenance efficiency by 15–30% through predictive analytics and real-time equipment tracking. Manufacturing facilities in countries such as Germany and Japan are integrating sensors with lubricant management workflows to reduce unplanned downtime. Additive producers are collaborating with technology firms to combine chemical performance with digital maintenance solutions.

Sustainable Formulation Demand Rises Environmental compliance and supply-chain restructuring are increasing demand for bio-based and lower-impact additive solutions, with sustainable lubricant adoption rising by approximately 18% among industrial users. Regulatory pressure on emissions and waste reduction is accelerating product redesign. Companies are expanding green chemistry research, localizing production networks, and developing formulations that balance performance with environmental requirements.

Detergents and dispersants represent the leading type segment, accounting for approximately 35% of lubricant additive consumption due to their critical role in engine cleanliness, deposit control, and oxidation management. Their dominance is supported by widespread automotive and industrial applications where reliability and extended equipment life are priorities. Anti-wear additives follow with nearly 25% share, remaining essential for heavy machinery and high-load operating environments. Companies are improving multifunctional additive blends to reduce formulation complexity and enhance performance. Viscosity index improvers are emerging as the fastest-growing type, supported by increasing demand for fuel-efficient lubricants and advanced engine technologies. Adoption is expanding by around 15% as manufacturers focus on products that maintain performance under temperature variations. Friction modifiers and corrosion inhibitors continue supporting specialized applications, particularly in electric mobility and industrial systems. Companies are shifting investment toward customized additive combinations that deliver efficiency gains and meet evolving equipment requirements.

Automotive lubricants represent the leading application segment with approximately 55% market share, supported by increasing vehicle production, stricter emission standards, and demand for improved engine performance. Passenger vehicles, commercial fleets, and hybrid vehicles are driving additive consumption as manufacturers require advanced formulations for fuel efficiency and durability. Industrial lubricants account for nearly 30% share, supported by manufacturing, energy, and heavy equipment operations. The fastest-growing application is electric and hybrid vehicle lubricants, expanding at over 20% adoption growth as mobility systems evolve. These applications require specialized additives for thermal management, component protection, and efficiency optimization. Companies are increasing investment in EV-focused lubricant research and partnering with automotive manufacturers to develop compatible solutions. Aerospace, marine, and specialized machinery applications remain smaller segments but provide opportunities for premium additive formulations and performance-driven products.

Automotive manufacturers and vehicle service providers represent the leading end-user segment, accounting for nearly 50% of demand due to large-scale lubricant consumption across passenger vehicles, commercial fleets, and mobility platforms. Their purchasing decisions are influenced by engine performance requirements, emission regulations, and long-term maintenance optimization. Industrial manufacturers hold around 30% share, driven by machinery-intensive operations requiring reliable lubrication systems.The fastest-growing end-user group is electric vehicle and advanced mobility manufacturers, with adoption increasing by approximately 20% as new drivetrain technologies require specialized lubrication solutions. Energy companies, construction operators, and marine businesses continue expanding usage through equipment modernization programs. Companies are targeting these segments through technical partnerships, application-specific formulations, and integrated lubricant management services. Future competitive positioning depends on supporting diverse end-user requirements with scalable and customized additive solutions.

North America accounted for the largest market share at 32% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 5.2% between 2026 and 2033.

North America held approximately 32% of the global Lubricanting Oil Additive Market in 2025, supported by strong automotive manufacturing, advanced industrial operations, and high adoption of premium lubricant technologies. The United States remains the primary contributor due to its large vehicle fleet, refinery infrastructure, and demand for fuel-efficient lubricant formulations. Industrial users are increasingly deploying synthetic additive packages to improve machinery life and reduce maintenance requirements. More than 60% of lubricant demand in key industrial sectors is linked to automotive, manufacturing, and energy applications. Companies are expanding additive production capacity and investing in specialized formulations for hybrid vehicles, heavy equipment, and advanced machinery systems.

United States Market Outlook: The United States dominates North American demand through its automotive ecosystem, industrial manufacturing base, and advanced chemical production capabilities. The country’s extensive commercial vehicle fleet and manufacturing operations drive consistent additive consumption. Over 250 million registered vehicles support ongoing demand for high-performance lubricants, while companies are increasing investment in low-emission and efficiency-focused additive technologies.

Europe represents nearly 27% of the Lubricanting Oil Additive Market, driven by strict environmental regulations, advanced automotive engineering, and strong industrial modernization programs. Germany, France, and Italy contribute significantly through automotive manufacturing and precision machinery industries. The transition toward lower-emission vehicles is increasing demand for specialized additive formulations designed for hybrid powertrains and advanced engines. European manufacturers are focusing on sustainable chemistry, with nearly 20% growth in demand for environmentally optimized lubricant solutions across selected industrial applications. Companies are strengthening partnerships with automotive manufacturers and chemical innovators to develop next-generation additives aligned with evolving mobility standards.

Germany Market Outlook: Germany leads Europe’s lubricant additive demand due to its automotive engineering strength and industrial manufacturing concentration. The country’s automotive sector produces millions of vehicles annually and requires advanced lubricant technologies for performance optimization. German manufacturers are increasingly adopting digital testing systems and sustainable additive formulations to support efficiency improvements and regulatory compliance.

Asia-Pacific is the fastest-expanding market, supported by large-scale automotive production, industrial development, and increasing lubricant consumption across emerging economies. The region contributes approximately 30% of global demand, with China, India, Japan, and South Korea acting as major consumption and production centers. China’s automotive manufacturing ecosystem and industrial expansion are accelerating demand for advanced additive packages, while India is experiencing increased adoption across transportation and manufacturing sectors. More than 40% of new lubricant formulation investments are concentrated in Asian production hubs. Companies are expanding local manufacturing facilities, strengthening supply chains, and developing cost-efficient additive solutions for high-volume applications.

China Market Outlook: China represents the largest Asia-Pacific market due to its automotive production capacity, chemical manufacturing infrastructure, and industrial equipment demand. The country produces more than 25 million vehicles annually, creating significant demand for advanced lubricant additives. Manufacturers are increasing domestic production capabilities and focusing on efficient formulations for electric vehicles and industrial machinery.

South America accounts for approximately 6% of the Lubricanting Oil Additive Market, supported by automotive activity, mining operations, agriculture, and energy industries. Brazil dominates regional consumption due to its vehicle fleet, industrial base, and agricultural machinery usage. Demand is increasing for additives that improve equipment durability in heavy-duty environments. Mining and infrastructure projects are encouraging adoption of high-performance lubricants, with industrial users targeting maintenance cost reductions of 10–15%. Companies are improving distribution networks and forming regional partnerships to overcome logistics challenges and ensure consistent supply availability across major industrial centers.

Brazil Market Outlook: Brazil is the key South American market due to its automotive manufacturing, agricultural equipment, and mining industries. The country operates one of the largest vehicle markets in Latin America, supporting continuous lubricant demand. Companies are expanding local distribution capabilities and introducing specialized additive solutions for heavy-duty machinery and commercial transportation applications.

Middle East & Africa contributes around 5% of the global Lubricanting Oil Additive Market, with demand concentrated in oil and gas operations, transportation, construction, and industrial infrastructure projects. Gulf countries are investing in refinery expansion, manufacturing diversification, and advanced industrial facilities, creating demand for specialized lubricant technologies. Saudi Arabia and the United Arab Emirates are increasing industrial modernization initiatives, with infrastructure investments exceeding billions of dollars across energy and manufacturing sectors. Companies are strengthening regional supply networks and developing high-temperature resistant additive formulations suited for demanding operating conditions.

Saudi Arabia Market Outlook: Saudi Arabia holds strategic importance due to its energy industry scale, industrial expansion programs, and growing manufacturing base. The country’s large oil and gas operations require advanced lubrication solutions for heavy equipment and processing facilities. Industrial diversification initiatives are encouraging companies to invest in localized chemical production and specialized lubricant technologies.

The Lubricanting Oil Additive Market is led by global suppliers including Lubrizol, Infineum, Chevron Oronite, and Afton Chemical, competing with regional specialty chemical manufacturers and formulation innovators. Competition is based on additive performance, pricing efficiency, supply chain reliability, customization, and OEM qualification capabilities. The top five players collectively account for approximately 45% market share, reflecting a moderately consolidated structure. Advanced additive packages are gaining traction, with premium formulations improving lubricant performance by 10–15% over conventional solutions. Companies are expanding production facilities, strengthening automotive partnerships, and integrating raw material capabilities to secure supply continuity. The competitive landscape is shifting toward sustainable chemistry, EV-compatible lubricants, and digital formulation technologies. High technical expertise, testing infrastructure, and customer approval requirements create entry barriers. Winning requires superior formulation innovation, reliable supply networks, faster product development, and application-specific solutions aligned with evolving industrial and mobility demands.

Infineum International Limited

Chevron Oronite Company LLC

Afton Chemical Corporation

BASF SE

Evonik Industries AG

LANXESS AG

Croda International Plc

Vanderbilt Chemicals LLC

Dover Chemical Corporation

ADEKA Corporation

King Industries Inc.

The Lubricanting Oil Additive Market is evolving through multifunctional additive chemistry, synthetic formulations, digital monitoring systems, and sustainable lubricant technologies. Advanced additive packages improve wear protection by nearly 15% compared with conventional solutions, while digital lubricant monitoring reduces maintenance interruptions by approximately 20%. Automotive manufacturers and industrial operators are adopting these technologies to improve equipment efficiency and operational reliability.

Emerging innovations include AI-assisted formulation development, bio-based additives, nanotechnology-enhanced lubricants, and EV-compatible lubricant systems. AI-driven simulation reduces formulation testing cycles by around 25%, enabling faster product development and customization. Technology-focused suppliers benefit from rapid innovation capabilities, while established manufacturers strengthen competitiveness through scalable production and application-specific solutions.

Between 2026 and 2028, smart lubrication platforms, sustainable additive chemistry, and predictive maintenance integration will influence supplier strategies. Compared with traditional lubricant systems, next-generation formulations provide approximately 10% higher efficiency under demanding operating conditions. Companies investing in advanced testing, digital tools, and collaborative development will gain stronger market positions as industries prioritize performance optimization, sustainability, and operational efficiency.

March 2026 Infineum inaugurated its new blending facility in India to strengthen local additive supply capabilities and support growing mobility and energy demand. The facility expands regional manufacturing presence through a dedicated blending operation, improving supply reliability and customer responsiveness for automotive lubricant applications. Source: www.infineum.com

July 2025 Lubrizol supported the launch of a hybrid-specific engine oil developed with Jiangsu Lopal Tech by providing Lubrizol® PV1710 additive technology. The collaboration targeted China’s hybrid vehicle market and enabled improved lubricant performance through advanced additive chemistry designed for new energy vehicle applications. Source: www.lubrizol.com

September 2025 Afton Chemical launched HiTEC® 12582, the industry’s first commercially available dedicated additive for hydrogen heavy-duty engines. The innovation supports low-emission transportation transition by enabling lubricant performance for hydrogen combustion engines and strengthening Afton’s position in alternative fuel technologies. Source: www.aftonchemical.com

April 2025 Chevron Oronite announced a strategic distribution partnership with ICONIC Base Oil Solutions in Brazil to expand availability of OLOA® lubricant additives and related solutions. The collaboration strengthens customer support, improves market access, and enhances Chevron Oronite’s lubricant additive distribution network in Latin America.

The Lubricanting Oil Additive Market Report analyzes major product categories including detergents, dispersants, viscosity index improvers, anti-wear additives, friction modifiers, and corrosion inhibitors. It evaluates applications across automotive lubricants, industrial lubricants, marine, aerospace, and specialized machinery sectors, covering end-users such as automotive manufacturers, industrial operators, energy companies, and transportation industries.

The report provides regional insights across North America, Europe, Asia-Pacific, South America, and Middle East & Africa, highlighting technology adoption, manufacturing trends, competitive strategies, and emerging opportunities. It examines sustainable formulations, EV-compatible lubricant technologies, digital monitoring systems, and advanced additive innovations. The study supports investment planning, expansion strategies, supplier evaluation, and competitive positioning by identifying market shifts and strategic priorities through 2033.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 1,920.0 Million |

| Market Revenue (2033) | USD 2,647.9 Million |

| CAGR (2026–2033) | 4.1% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Companies Profiled | Lubrizol Corporation; Infineum International Limited; Chevron Oronite Company LLC; Afton Chemical Corporation; BASF SE; Evonik Industries AG; LANXESS AG; Croda International Plc; Vanderbilt Chemicals LLC; Dover Chemical Corporation; ADEKA Corporation; King Industries Inc. |

| Customization & Pricing | Available on Request (10% Customization Free) |