Reports

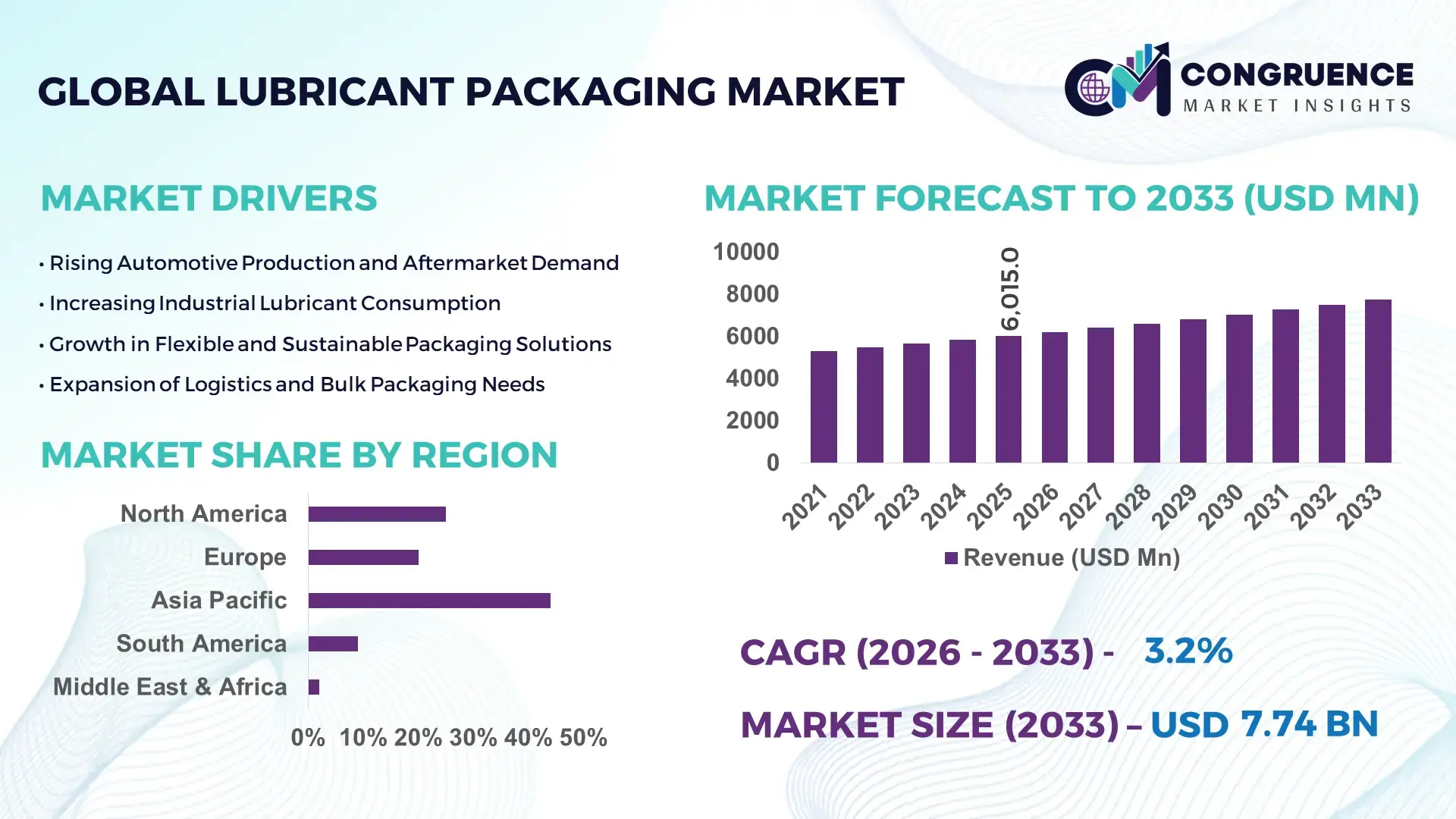

The Global Lubricant Packaging Market was valued at USD 6015 Million in 2025 and is anticipated to reach a value of USD 7738.79 Million by 2033 expanding at a CAGR of 3.2% between 2026 and 2033. This growth is primarily driven by increasing automotive production and industrial lubrication demand across emerging economies.

China continues to exhibit a strong industrial footprint in the lubricant packaging landscape, supported by annual lubricant consumption exceeding 7 million metric tons. The country operates more than 200 large-scale lubricant blending plants, with packaging demand heavily concentrated in HDPE bottles, metal drums, and flexible pouches. Over 60% of packaging formats are utilized in automotive and heavy machinery applications, while industrial lubricants account for nearly 35% of packaging consumption. Significant investments in automated filling lines and smart labeling technologies have improved packaging efficiency by approximately 20% over the last five years. Additionally, China’s transition toward recyclable plastic packaging has resulted in over 45% of lubricant containers being manufactured from recyclable polymers, reflecting ongoing advancements in sustainable packaging solutions.

Market Size & Growth: USD 6015 Million in 2025 projected to reach USD 7738.79 Million by 2033 at 3.2% CAGR, driven by rising automotive fleet expansion and industrial maintenance demand.

Top Growth Drivers: Automotive lubricant consumption growth at 28%, industrial equipment maintenance demand at 22%, and shift toward sustainable packaging adoption at 18%.

Short-Term Forecast: By 2028, automated packaging systems are expected to reduce operational costs by 15% and improve filling efficiency by 20%.

Emerging Technologies: Smart packaging with QR-based traceability, lightweight polymer containers, and advanced barrier coatings for extended shelf life.

Regional Leaders: Asia-Pacific projected at USD 3200 Million by 2033 with strong manufacturing demand; North America at USD 1900 Million driven by aftermarket automotive services; Europe at USD 1600 Million with high sustainability compliance adoption.

Consumer/End-User Trends: Automotive workshops and industrial plants dominate usage, with increasing preference for eco-friendly and easy-dispense packaging formats.

Pilot or Case Example: In 2024, a leading manufacturer implemented AI-enabled filling systems achieving 18% reduction in material wastage and 12% faster throughput.

Competitive Landscape: Market leader holds approximately 17% share, followed by key players including major global packaging and lubricant container manufacturers.

Regulatory & ESG Impact: Increasing mandates for recyclable materials and reduced plastic waste are pushing adoption of reusable and biodegradable packaging formats.

Investment & Funding Patterns: Over USD 900 Million invested in packaging innovation and automation projects, with rising focus on sustainable materials.

Innovation & Future Outlook: Integration of IoT-enabled packaging, refillable container systems, and lightweight composite materials shaping next-generation lubricant packaging solutions.

The lubricant packaging market is strongly influenced by automotive, marine, and industrial machinery sectors, which collectively contribute over 70% of packaging demand. Plastic containers, particularly HDPE bottles, account for more than 55% of total usage due to durability and cost efficiency, while metal drums contribute significantly in bulk industrial applications. Recent innovations include multi-layer barrier packaging that extends lubricant shelf life by up to 25% and reduces contamination risks. Regulatory frameworks encouraging recyclable and reusable materials have accelerated the transition toward eco-friendly packaging solutions, with over 40% of manufacturers adopting sustainable alternatives. Regionally, Asia-Pacific leads consumption due to high industrial output, while Europe shows strong growth in green packaging adoption. Increasing demand for compact, user-friendly designs and refillable systems is expected to redefine packaging strategies in the coming years.

The lubricant packaging market holds strategic importance within the broader automotive and industrial supply chain, serving as a critical interface between manufacturers and end-users. Efficient packaging solutions directly influence product safety, transportation costs, and shelf life, making them essential for operational optimization. Advanced packaging technologies such as multi-layer polymer containers deliver up to 30% improved barrier protection compared to conventional single-layer plastic packaging, significantly reducing oxidation and contamination risks.

Asia-Pacific dominates in volume due to large-scale automotive production and industrial activities, while Europe leads in sustainable packaging adoption, with over 55% of enterprises integrating recyclable or reusable materials into their packaging systems. The increasing focus on automation is reshaping the market, as automated filling and sealing systems enhance production efficiency by nearly 25% compared to manual processes. By 2028, AI-enabled packaging lines are expected to improve operational efficiency by 20% while reducing material waste by approximately 15%. Environmental compliance is also becoming a key priority, with firms committing to sustainability goals such as achieving 50% recyclable packaging materials by 2030. Governments across major economies are enforcing stricter regulations on plastic usage, further accelerating the transition to eco-friendly alternatives.

In a notable micro-scenario, in 2024, a European packaging manufacturer achieved a 22% reduction in carbon emissions by adopting lightweight container designs and integrating recycled polymers into production. These developments highlight how technological innovation and sustainability initiatives are shaping future pathways. As industries continue to demand cost-efficient, durable, and environmentally compliant solutions, the lubricant packaging market is positioned as a pillar of resilience, regulatory alignment, and sustainable industrial growth.

The expansion of the global automotive fleet, which surpassed 1.5 billion vehicles, has significantly increased the demand for lubricants and, consequently, packaging solutions. Industrial sectors such as manufacturing, mining, and construction also require consistent lubrication, driving bulk packaging needs such as drums and intermediate bulk containers. Approximately 65% of lubricant packaging demand originates from automotive applications, while industrial usage contributes around 30%. The rise in vehicle servicing frequency and preventive maintenance practices has further boosted demand for small and medium-sized packaging formats. Additionally, the growing adoption of electric vehicles, despite lower lubrication requirements, still necessitates specialized lubricants, contributing to niche packaging demand. These factors collectively drive the need for innovative, durable, and efficient packaging solutions across multiple industries.

Stringent environmental regulations targeting single-use plastics have created significant challenges for lubricant packaging manufacturers. Governments across Europe and North America have introduced mandates requiring up to 50% recyclable content in plastic packaging, increasing compliance costs and necessitating material redesign. Traditional HDPE containers, which account for over half of the market, face scrutiny due to their environmental impact. Additionally, recycling infrastructure limitations in developing regions hinder the effective reuse of packaging materials, leading to increased waste management costs. The transition to biodegradable or alternative materials often results in higher production expenses, with eco-friendly packaging solutions costing approximately 20–30% more than conventional options. These factors create financial and operational constraints, limiting rapid adoption and affecting overall market expansion.

The shift toward sustainable packaging presents substantial opportunities for innovation and market differentiation. The adoption of recyclable plastics, biodegradable materials, and refillable container systems is gaining momentum, with over 40% of manufacturers investing in eco-friendly solutions. Smart packaging technologies, including QR codes and IoT-enabled tracking systems, are enhancing supply chain visibility and product authentication. These solutions can improve inventory management efficiency by up to 18% and reduce counterfeiting risks. Additionally, lightweight packaging designs reduce transportation costs by approximately 12%, offering economic and environmental benefits. Emerging markets in Asia, Africa, and Latin America also present growth opportunities due to increasing industrialization and automotive expansion, creating demand for cost-effective and scalable packaging solutions.

Fluctuations in raw material prices, particularly for plastics and metals, pose a significant challenge for the lubricant packaging industry. Polymer prices have experienced volatility of up to 25% due to supply chain disruptions and geopolitical factors, directly impacting production costs. Additionally, logistics challenges, including container shortages and increased transportation costs, have disrupted supply chains, delaying product delivery and increasing operational expenses. The reliance on petrochemical-based materials further exposes the market to oil price fluctuations, adding another layer of uncertainty. Compliance with evolving environmental regulations also requires continuous investment in research and development, increasing financial pressure on manufacturers. These challenges necessitate strategic sourcing, cost optimization, and innovation to maintain competitiveness in a rapidly changing market environment.

• Rapid shift toward lightweight plastic packaging reducing material usage by 18%: Manufacturers are increasingly adopting lightweight HDPE and PET containers to optimize logistics and sustainability. Studies indicate that lightweight packaging designs reduce overall material consumption by nearly 18% while improving transportation efficiency by up to 12%. Over 60% of lubricant packaging manufacturers have transitioned to thinner-walled containers without compromising durability. This trend is particularly strong in Asia-Pacific, where high-volume production demands cost-efficient solutions. Additionally, lightweight containers contribute to a 10–15% reduction in carbon emissions during transportation, making them a preferred choice for large-scale automotive lubricant suppliers.

• Increasing adoption of smart packaging technologies improving traceability by 25%: Digital integration in lubricant packaging is gaining traction, with QR codes, RFID tags, and IoT-enabled tracking systems being implemented across supply chains. These technologies have enhanced traceability and inventory management efficiency by approximately 25%, allowing real-time monitoring of lubricant distribution. Nearly 35% of global packaging firms have integrated smart labeling systems to combat counterfeit products and ensure regulatory compliance. In North America and Europe, adoption rates exceed 45%, driven by strict quality assurance requirements. Smart packaging also enables predictive maintenance insights, improving product lifecycle management for industrial users.

• Growth in sustainable and recyclable packaging materials exceeding 40% adoption: Environmental regulations and corporate ESG commitments are accelerating the use of recyclable and biodegradable materials in lubricant packaging. Over 40% of manufacturers now utilize recyclable polymers, with some companies achieving up to 50% recycled content in their containers. Metal drums and reusable intermediate bulk containers are also gaining traction, particularly in industrial applications where reuse cycles can exceed 20 times. Europe leads in sustainability initiatives, with nearly 55% of lubricant packaging firms adopting eco-friendly solutions, while Asia-Pacific is rapidly catching up with a 30% adoption rate driven by regulatory reforms.

• Expansion of automated filling and packaging systems increasing efficiency by 22%: Automation is transforming lubricant packaging operations, with advanced filling lines and robotic handling systems improving productivity and accuracy. Automated systems have demonstrated efficiency gains of up to 22% while reducing human error by nearly 30%. More than 50% of large-scale lubricant manufacturers have implemented automated packaging solutions to meet high production demands. These systems also optimize material usage, reducing wastage by approximately 15%. In regions with high labor costs, such as Europe and North America, automation adoption exceeds 60%, highlighting its importance in maintaining competitive operational efficiency.

The lubricant packaging market is segmented based on type, application, and end-user, each contributing uniquely to overall demand patterns. Packaging types range from plastic containers and metal drums to flexible pouches, with varying adoption depending on cost efficiency and application requirements. Plastic-based packaging dominates due to its lightweight properties and versatility, accounting for more than half of total usage. Applications are primarily concentrated in automotive and industrial sectors, which together contribute over 70% of total demand, reflecting the critical role of lubricants in machinery performance and maintenance. End-user segmentation highlights automotive service providers, manufacturing industries, and energy sectors as key consumers, each requiring specific packaging formats tailored to volume, storage, and transportation needs. The growing emphasis on sustainability and operational efficiency is influencing segmentation trends, with increasing adoption of recyclable materials and smart packaging solutions across all categories.

The lubricant packaging market by type includes plastic containers, metal drums, intermediate bulk containers, and flexible packaging solutions. Plastic containers currently account for approximately 55% of total adoption, driven by their lightweight structure, cost efficiency, and ease of handling in automotive and retail lubricant distribution. In comparison, metal drums hold around 25% share, primarily used for bulk industrial lubricant storage, while intermediate bulk containers contribute nearly 12% due to their reusability and durability in large-scale operations. Flexible packaging solutions, including pouches, represent the remaining 8%, serving niche applications where portability and space efficiency are critical.

Flexible packaging is emerging as the fastest-growing segment, expanding at an estimated rate of 5.8% annually, supported by increasing demand for compact, user-friendly, and environmentally sustainable packaging formats. These solutions reduce storage space requirements by up to 30% and transportation costs by nearly 15%, making them attractive for emerging markets.

The lubricant packaging market by application is segmented into automotive, industrial machinery, marine, and aerospace sectors. Automotive applications dominate the segment, accounting for nearly 65% of total demand, as passenger vehicles, commercial fleets, and two-wheelers require frequent lubricant replacement and maintenance. Industrial machinery follows with approximately 25% share, driven by continuous lubrication needs in manufacturing, mining, and construction equipment. Marine and aerospace applications collectively contribute around 10%, focusing on specialized lubricant packaging designed for extreme operating conditions.

Industrial machinery applications are witnessing the fastest growth, with an estimated expansion rate of 5.2%, fueled by increasing automation and global industrial output. The demand for bulk packaging solutions, such as drums and intermediate containers, is rising due to high-volume lubricant consumption in factories and heavy industries.

End-user segmentation in the lubricant packaging market includes automotive service centers, manufacturing industries, oil and gas companies, and power generation sectors. Automotive service centers lead with approximately 48% of total usage, driven by high vehicle servicing frequency and demand for small and medium-sized packaging formats. Manufacturing industries account for nearly 30% of demand, utilizing bulk packaging solutions for machinery maintenance and operational efficiency. Oil and gas and power generation sectors together contribute around 22%, requiring specialized, high-durability packaging for large-scale lubricant storage and transportation.

Manufacturing industries represent the fastest-growing end-user segment, expanding at an estimated rate of 5.5%, supported by increasing industrial automation and global production activities. Adoption rates in advanced manufacturing facilities exceed 60%, reflecting the need for efficient lubrication systems to maintain equipment performance.

Region Asia-Pacific accounted for the largest market share at 42% in 2025 however, North America is expected to register the fastest growth, expanding at a CAGR of 4.1% between 2026 and 2033.

Asia-Pacific’s dominance is supported by lubricant consumption exceeding 45 million metric tons annually, with China and India together contributing over 60% of regional packaging demand. North America follows with approximately 26% market share, driven by high automotive servicing rates and advanced packaging technologies, while Europe holds around 21% supported by strong sustainability regulations. South America and the Middle East & Africa collectively account for nearly 11%, with growing industrial and energy sector activities. Across regions, plastic containers represent over 55% of packaging formats, while metal drums contribute close to 28% in industrial applications. Increasing adoption of recyclable materials has reached 48% in developed markets, compared to 32% in emerging economies, reflecting varied regulatory pressures and technological readiness.

How are automation and sustainability initiatives transforming advanced packaging demand?

North America accounts for approximately 26% of the global lubricant packaging market, driven primarily by automotive aftermarket services and industrial machinery sectors. The region processes over 9 million metric tons of lubricants annually, creating substantial demand for durable and efficient packaging solutions. Regulatory frameworks such as plastic reduction mandates and recycling targets have pushed manufacturers to incorporate up to 45% recycled content in packaging materials. Technological advancements, including AI-enabled filling systems and automated packaging lines, have improved operational efficiency by nearly 20%. A notable example includes a leading packaging manufacturer implementing robotic filling solutions, reducing production errors by 18%. Consumer behavior in this region reflects a strong preference for premium, eco-friendly packaging, with over 50% of enterprises prioritizing sustainability compliance and traceability features.

What role do sustainability regulations play in shaping advanced packaging solutions?

Europe holds nearly 21% of the lubricant packaging market, with key countries such as Germany, the United Kingdom, and France driving regional demand. The region is characterized by strict environmental policies requiring up to 50% recyclable content in plastic packaging, significantly influencing product design and material selection. Industrial lubricant consumption exceeds 8 million metric tons annually, supporting demand for bulk packaging formats such as metal drums and intermediate containers. Emerging technologies, including biodegradable polymers and multi-layer barrier packaging, have improved product shelf life by 25%. A prominent regional packaging company has introduced fully recyclable lubricant containers, achieving a 30% reduction in plastic usage. Consumer behavior reflects strong regulatory compliance, with over 55% of businesses adopting sustainable packaging solutions to meet environmental standards and corporate ESG commitments.

Why is rapid industrial expansion driving large-scale packaging demand?

Asia-Pacific leads the lubricant packaging market in both volume and consumption, accounting for over 42% of global demand. China, India, and Japan are the top consuming countries, collectively processing more than 25 million metric tons of lubricants annually. Rapid industrialization, expanding automotive production, and infrastructure development have significantly increased packaging requirements. The region hosts over 300 lubricant blending plants, supporting large-scale packaging operations. Technological advancements, including automated filling systems and lightweight packaging materials, have improved production efficiency by approximately 18%. A regional packaging manufacturer recently expanded its production capacity by 25% to meet rising demand from automotive and construction sectors. Consumer behavior in this region is influenced by cost efficiency and convenience, with increasing adoption of flexible packaging solutions growing by nearly 20% annually.

How are industrial growth and trade policies influencing packaging demand patterns?

South America accounts for around 6% of the global lubricant packaging market, with Brazil and Argentina serving as key contributors. The region consumes approximately 3 million metric tons of lubricants annually, largely driven by automotive and agricultural sectors. Infrastructure development and energy projects have increased demand for bulk packaging formats such as metal drums and intermediate containers. Government policies promoting local manufacturing and import substitution have encouraged domestic production of packaging materials, reducing dependency on imports by nearly 15%. A regional packaging firm has expanded its manufacturing capacity by 20% to meet growing demand in agricultural machinery lubrication. Consumer behavior varies significantly, with demand closely tied to industrial and agricultural cycles, and increasing preference for cost-effective and durable packaging solutions.

What factors are accelerating packaging demand in energy-driven economies?

The Middle East & Africa region represents approximately 5% of the global lubricant packaging market, with demand primarily driven by oil and gas, construction, and mining industries. Countries such as the UAE and South Africa are key growth markets, collectively consuming over 2.5 million metric tons of lubricants annually. Technological modernization initiatives, including automated packaging systems and improved logistics infrastructure, have enhanced efficiency by nearly 15%. Trade partnerships and regional agreements have facilitated easier access to raw materials, reducing production costs by approximately 10%. A local packaging manufacturer has introduced reusable bulk containers, extending lifecycle usage by over 20 cycles. Consumer behavior reflects a strong focus on durability and large-volume packaging, with over 60% of demand concentrated in industrial applications.

China – 28% market share: Lubricant Packaging market growth is supported by high production capacity, with over 200 blending plants and strong automotive and industrial demand.

United States – 22% market share: Lubricant Packaging market expansion is driven by advanced packaging technologies, high vehicle servicing rates, and strong regulatory compliance for sustainable materials.

The lubricant packaging market exhibits a moderately fragmented structure, with over 150 active global and regional players competing across various product segments. The top five companies collectively account for approximately 35% of the total market share, indicating significant competition alongside opportunities for niche and regional manufacturers. Leading players are focusing on strategic initiatives such as mergers, acquisitions, and partnerships to strengthen their market presence and expand product portfolios. Over 25 major product launches were recorded in the past two years, primarily centered on sustainable packaging solutions and lightweight materials.

Innovation remains a key competitive factor, with more than 40% of companies investing in research and development to enhance packaging durability, recyclability, and efficiency. Automation and digital transformation are also reshaping competition, as nearly 50% of large manufacturers have adopted automated filling and packaging systems to improve productivity and reduce operational costs by up to 20%. Additionally, collaborations between packaging manufacturers and lubricant producers are increasing, enabling customized solutions tailored to specific industrial requirements.

The market is also witnessing increased competition from regional players offering cost-effective solutions, particularly in Asia-Pacific and South America. Sustainability-driven differentiation is becoming critical, with over 45% of companies introducing eco-friendly packaging alternatives to comply with evolving environmental regulations and meet customer expectations.

Greif Inc.

Mauser Packaging Solutions

SCHÜTZ GmbH & Co. KGaA

Time Technoplast Ltd.

Berry Global Inc.

Amcor plc

Mold-Tek Packaging Ltd.

Balmer Lawrie & Co. Ltd.

Scholle IPN Corporation

RPC Group Plc

TPL Plastech Ltd.

Parekhplast India Limited

Technological advancements in the lubricant packaging market are reshaping production efficiency, product safety, and sustainability performance. One of the most significant developments is the adoption of multi-layer barrier packaging, which enhances oxygen and moisture resistance by up to 30%, thereby extending lubricant shelf life and reducing contamination risks. These advanced materials are increasingly used in high-performance automotive and industrial lubricants where product integrity is critical.

Automation technologies are also transforming packaging operations. Fully automated filling and capping systems now achieve throughput rates exceeding 120 containers per minute, improving operational efficiency by approximately 20% while reducing human error by nearly 25%. Robotics integrated with vision inspection systems are capable of detecting defects with over 98% accuracy, ensuring consistent quality across large production volumes.

Smart packaging is gaining traction with the integration of QR codes, RFID tags, and IoT-enabled sensors. These technologies enable real-time tracking and authentication, improving supply chain visibility by nearly 25% and significantly reducing counterfeit risks. Around 35% of large lubricant manufacturers have already implemented digital tracking systems in their packaging lines.

Sustainability-focused innovations are also accelerating. The use of post-consumer recycled (PCR) plastics has increased to nearly 40% in certain markets, while biodegradable polymers are being tested for performance under extreme conditions. Lightweight packaging designs reduce material usage by approximately 15% and transportation emissions by up to 12%. Additionally, refillable and reusable packaging systems are gaining adoption, with some industrial containers achieving reuse cycles of more than 20 times, supporting circular economy objectives.

• In March 2025, Amcor plc announced the expansion of its recyclable packaging portfolio for industrial applications, introducing high-barrier lubricant containers with up to 50% recycled content, designed to meet stricter European sustainability regulations. Source: www.amcor.com

• In October 2024, Greif Inc. launched a new line of eco-friendly intermediate bulk containers (IBCs) featuring enhanced durability and reusability, achieving up to 25 reuse cycles and reducing packaging waste by approximately 30%. Source: www.greif.com

• In July 2025, Mauser Packaging Solutions introduced advanced closed-loop recycling systems for plastic lubricant containers, enabling recovery and reuse of over 60% of packaging materials within industrial supply chains. Source: www.mauserpackaging.com

• In January 2024, Berry Global Inc. developed lightweight HDPE lubricant bottles incorporating post-consumer recycled material, reducing overall plastic usage by nearly 20% while maintaining structural integrity for automotive lubricant applications. Source: www.berryglobal.com

The scope of the lubricant packaging market report encompasses a comprehensive evaluation of product types, applications, end-user industries, regional markets, and technological advancements shaping the industry landscape. The report covers key packaging formats including plastic containers, metal drums, intermediate bulk containers, and flexible packaging solutions, which collectively account for over 95% of total market utilization. It also analyzes application segments such as automotive, industrial machinery, marine, and aerospace, with automotive and industrial sectors contributing more than 70% of total demand. Geographically, the report provides detailed insights across five major regions, including Asia-Pacific, North America, Europe, South America, and the Middle East & Africa. Asia-Pacific leads in volume consumption with over 40% share, while developed regions demonstrate higher adoption of advanced and sustainable packaging technologies. The report further evaluates regional production capacities, consumption patterns, and trade dynamics influencing packaging demand.

In terms of technology, the scope includes analysis of automation systems, smart packaging solutions, and sustainable material innovations. Over 50% of large manufacturers are adopting automated filling lines, while approximately 40% are integrating recyclable materials into their packaging processes. The report also highlights emerging trends such as IoT-enabled tracking, lightweight packaging designs, and reusable container systems, which are expected to redefine operational efficiency and environmental performance. Additionally, the report examines industry-specific requirements, regulatory frameworks, and environmental standards influencing packaging design and material selection. It provides a structured assessment of competitive dynamics, innovation strategies, and investment trends, offering decision-makers a holistic view of current opportunities and future growth areas within the lubricant packaging market.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

3.2% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Greif Inc., Mauser Packaging Solutions, SCHÜTZ GmbH & Co. KGaA, Time Technoplast Ltd., Berry Global Inc., Amcor plc, Mold-Tek Packaging Ltd., Balmer Lawrie & Co. Ltd., Scholle IPN Corporation, RPC Group Plc, TPL Plastech Ltd., Parekhplast India Limited |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |