Reports

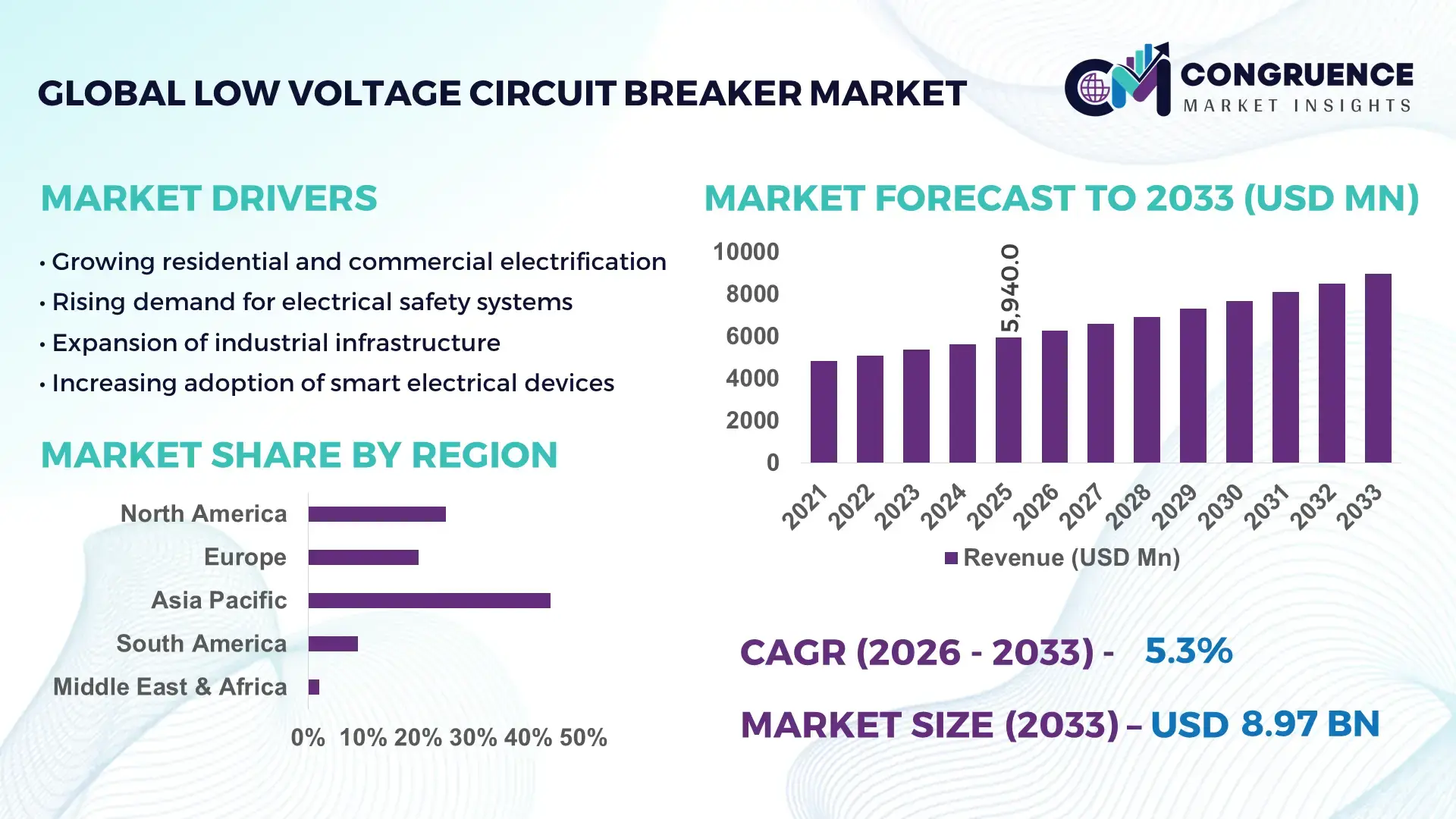

The Global Low Voltage Circuit Breaker Market was valued at USD 5940 Million in 2025 and is anticipated to reach a value of USD 8965.06 Million by 2033 expanding at a CAGR of 5.28% between 2026 and 2033.

Rising electrification across industrial automation and smart infrastructure, combined with a 22% increase in digital protection system adoption, is directly accelerating demand for advanced low voltage circuit breakers with real-time monitoring capabilities. Between 2024 and 2026, supply chain realignments driven by geopolitical trade tensions and localized manufacturing policies have reduced component lead times by nearly 18%, strengthening regional production ecosystems.

China dominates the market with approximately 34% share, supported by over USD 18 billion in grid modernization investments and strong domestic manufacturing capacity exceeding 45 million units annually. The country’s industrial sector, contributing nearly 39% of its electrical equipment demand, continues to adopt smart breakers with IoT integration, where penetration has crossed 27% in urban infrastructure projects. Compared to North America, where adoption of digital breakers stands at 21%, China shows a faster transition toward automation-driven protection systems, supported by aggressive urbanization and renewable energy integration targets.

As the market shifts from conventional protection devices to intelligent, connected systems, companies prioritizing localized production and smart technology integration gain a measurable competitive advantage in cost efficiency and response time.

Market Size & Growth: USD 5940M (2025) to USD 8965.06M (2033) at 5.28%, driven by 22% rise in smart grid integration.

Top Growth Drivers: Industrial automation (+28%), renewable integration (+24%), urban electrification (+19%).

Short-Term Forecast: By 2027, operational efficiency improves by 17% through digital breaker deployment.

Emerging Technologies: AI-based fault detection, IoT-enabled breakers, and arc fault protection systems gaining 25% adoption.

Regional Leaders: Asia-Pacific (~USD 3.2B) driven by infrastructure expansion; Europe (~USD 1.8B) led by ESG upgrades; North America (~USD 1.5B) focused on grid modernization.

Consumer/End-User Trends: Commercial infrastructure accounts for 41% usage with 26% shift toward smart protection systems.

Pilot/Case Example: 2025 smart grid rollout in Southeast Asia improved fault response time by 30%.

Competitive Landscape: Top player holds ~17% share; key companies focus on digital integration and modular systems.

Regulatory & ESG Impact: Energy efficiency regulations improved system performance by 15% across EU installations.

Investment & Funding: Over USD 2.4B invested in grid resilience and smart electrical infrastructure since 2024.

Innovation & Future Outlook: Solid-state breakers and predictive maintenance systems driving 20% reduction in downtime.

Industrial manufacturing accounts for nearly 36% of total demand, followed by commercial infrastructure at 41% and residential applications at 23%, reflecting strong urban deployment patterns. Recent innovations such as solid-state circuit breakers and AI-driven predictive maintenance systems have improved fault detection accuracy by 29%. Asia-Pacific leads with over 45% demand share, while Europe is advancing through regulatory-driven upgrades. The emergence of decentralized energy systems, alongside ongoing supply chain localization trends, is positioning the market toward faster, technology-led transformation in the coming years.

Low voltage circuit breakers are rapidly transforming into mission-critical assets as electrification, automation, and grid decentralization accelerate across industries, making this market a focal point for capital allocation and competitive positioning. A 26% rise in smart infrastructure deployments is directly intensifying the need for intelligent protection systems that ensure uptime and energy efficiency. However, tightening global compliance standards and supply chain localization mandates are reshaping sourcing and production strategies, forcing manufacturers to optimize cost structures while maintaining performance reliability.

Solid-state circuit breakers improve efficiency by 31% while reducing maintenance cost by 24% compared to legacy electromechanical systems, positioning them as a disruptive upgrade across industrial and commercial applications. Asia-Pacific leads in volume with over 45% share, while Europe leads in adoption and innovation with 29% penetration of digital and energy-efficient breaker systems. Over the next 2–3 years, predictive maintenance integration is expected to reduce system downtime by 18%, directly improving operational continuity.

ESG compliance is emerging as a measurable advantage, with energy-efficient breakers lowering power loss by 14%, enabling faster regulatory approvals and reduced lifecycle costs. A 2025 smart building project in Singapore demonstrated a 27% improvement in fault response time using AI-enabled breakers. Leading companies are accelerating R&D investments and shifting capital toward digital product lines, reinforcing their competitive positioning as the market continues transforming toward intelligent, connected electrical protection ecosystems.

The accelerating shift toward electrified infrastructure and industrial automation is forcing a structural upgrade in circuit protection technologies. Global industrial automation adoption has increased by 28%, directly driving demand for low voltage circuit breakers capable of handling higher load variability and real-time fault detection. Simultaneously, smart building deployments have grown by 24%, requiring integrated protection systems that align with digital energy management platforms. A key global trigger is the rapid expansion of renewable energy grids, where decentralized power sources demand 30% higher responsiveness in protection systems compared to traditional grids. This shift is creating a cause-effect chain: higher energy complexity → increased fault risk → demand for intelligent breakers. In response, companies are accelerating capacity expansion in Asia-Pacific and investing in IoT-enabled product lines, while forming strategic partnerships with grid operators to embed smart protection solutions at scale.

Despite strong demand, the market is constrained by raw material volatility and component supply concentration. Critical inputs such as copper and semiconductor components have seen price fluctuations of up to 19%, directly impacting manufacturing costs and pricing stability. Additionally, nearly 42% of key electronic components are sourced from limited geographic regions, exposing the market to geopolitical risks and supply disruptions. A real-world constraint is the ongoing shift toward localized manufacturing, which, while reducing dependency, has increased short-term capital expenditure by 21% for new production facilities. These factors create a direct business impact: higher costs, delayed project timelines, and limited scalability in emerging markets. To mitigate these risks, companies are diversifying supplier networks, securing long-term contracts, and investing in alternative materials and modular designs to maintain cost competitiveness and supply resilience.

The transition toward intelligent and energy-efficient electrical systems is unlocking high-impact opportunities in digital circuit protection. IoT-enabled breakers are witnessing a 33% increase in adoption, driven by demand for real-time monitoring and predictive maintenance capabilities. Additionally, solid-state breaker technology is enabling up to 29% faster fault isolation, significantly improving system reliability. A key future signal is the rise of decentralized energy systems, where microgrids and distributed generation are expanding at a rate of 27%, creating new demand pockets for adaptive protection solutions. Beyond obvious gains, companies are leveraging these technologies to achieve 18% operational efficiency improvements through reduced downtime and optimized energy usage. To capture this upside, market leaders are intensifying R&D investments, expanding into emerging markets, and building integrated ecosystems that combine hardware, software, and analytics for long-term competitive dominance.

The market faces significant execution challenges related to infrastructure readiness and system integration complexity. Nearly 35% of existing electrical infrastructure is incompatible with advanced digital breakers, requiring costly upgrades and slowing adoption rates. Additionally, integrating smart breakers into legacy systems increases implementation complexity by 23%, creating operational inefficiencies and extended deployment timelines. A critical real-world pressure is the limitation of aging grid infrastructure, particularly in developing regions, where capacity constraints restrict the deployment of advanced protection systems. These challenges directly impact long-term scalability and consistent performance, creating a tension between innovation and practical deployment. To remain competitive, companies must invest in backward-compatible technologies, develop scalable integration frameworks, and strengthen partnerships with infrastructure providers to ensure seamless adoption while maintaining performance reliability.

26% surge in digital breaker deployment is reshaping real-time protection execution. Across industrial and commercial installations, IoT-enabled circuit breakers now account for nearly 31% of new deployments, replacing conventional systems in high-load environments. This shift is driven by a 22% improvement in fault detection speed and a 19% reduction in manual inspection cycles. Companies are rapidly integrating cloud-based monitoring platforms and forming partnerships with automation providers to scale intelligent protection systems across facilities.

18% reduction in lead times is redefining localized manufacturing strategies. Ongoing supply chain restructuring between 2024 and 2026 has forced manufacturers to shift production closer to demand centers, resulting in a 21% increase in regional assembly units. This transition has improved component availability by 17% while stabilizing delivery cycles. A non-obvious impact is the rise of modular breaker designs, enabling faster customization and reducing inventory holding costs by 14%, prompting companies to restructure production models.

29% increase in energy-efficient breaker adoption is optimizing compliance-driven installations. Stricter regulatory frameworks have accelerated the deployment of low-loss circuit breakers, particularly in Europe and parts of Asia. These systems reduce energy dissipation by 16% and improve system lifespan by 12%. Companies are responding by redesigning product portfolios to align with compliance standards, while leveraging energy efficiency as a differentiator in competitive bids.

24% shift toward integrated protection systems is transforming business models. Instead of standalone products, nearly 27% of installations now involve bundled solutions combining breakers, sensors, and analytics platforms. This integration improves operational efficiency by 20% and reduces system downtime by 15%. Companies are moving toward service-based models, offering predictive maintenance contracts and digital dashboards, redefining revenue streams while increasing customer retention.

The low voltage circuit breaker market is segmented across types, applications, and end-users, with demand distribution reflecting both infrastructure maturity and technological adoption. Miniature and molded case breakers dominate high-volume installations, while advanced breakers are gaining traction in industrial and power-intensive environments. Approximately 58% of demand is concentrated in commercial and industrial applications, driven by automation and infrastructure expansion. Demand is shifting toward intelligent protection systems, particularly in utilities and infrastructure sectors, where reliability and efficiency are critical. This transition is prompting manufacturers to align product portfolios with digital integration capabilities, while expanding capacity in high-growth segments to capture evolving demand patterns.

Miniature Circuit Breakers (MCB) dominate the market with approximately 38% share, driven by their cost efficiency, compact design, and widespread use in residential and light commercial applications. Their scalability and ease of installation make them the default choice for high-volume deployments. However, Molded Case Circuit Breakers (MCCB) are emerging as the fastest-growing segment, expanding at a rate exceeding 26%, fueled by rising demand in industrial and commercial environments requiring higher current capacity and enhanced protection features. Compared to MCBs, MCCBs offer superior fault tolerance and adjustable trip settings, making them critical for complex electrical systems.

Air Circuit Breakers (ACB) and Residual Current Circuit Breakers (RCCB), along with Motor Protection Circuit Breakers (MPCB), collectively account for nearly 42% of the market, serving specialized applications. ACBs are essential in large-scale power distribution systems, while RCCBs are gaining traction due to a 21% increase in safety compliance requirements. MPCBs are increasingly deployed in automation-driven industries where motor protection is critical. Companies are responding by expanding MCCB production capacity and investing in smart MCB variants with IoT capabilities. The strategic implication is clear: while MCBs ensure volume stability, MCCBs and advanced breakers are capturing high-value growth opportunities.

Commercial applications lead the market with approximately 34% share, driven by rapid urban infrastructure development and increasing deployment of smart building systems. The concentration is due to high electrical load density and the need for reliable protection across offices, retail, and institutional facilities. Industrial applications are the fastest-growing segment, expanding by over 27%, fueled by automation, robotics integration, and the need for high-performance electrical safety systems. Compared to residential use, which remains stable at around 23% share, industrial demand is shifting toward intelligent breakers capable of predictive maintenance.

Power distribution and equipment protection together account for nearly 43% of demand, reflecting their critical role in maintaining grid stability and operational continuity. A notable shift is the 19% increase in breaker deployment within decentralized energy systems, where protection requirements are more dynamic. Companies are adapting by developing application-specific solutions and scaling deployment in industrial clusters. The implication is that demand is moving from basic protection to performance-driven applications, requiring higher technological sophistication.

Utilities dominate the market with approximately 33% share, driven by large-scale grid infrastructure and the need for reliable power distribution systems. Their demand concentration is linked to continuous upgrades in transmission and distribution networks, particularly with renewable integration. Infrastructure is the fastest-growing end-user segment, expanding by over 28%, fueled by smart city projects and transportation electrification. Compared to manufacturing, which holds around 24% share and focuses on operational efficiency, infrastructure demand is more dynamic and technology-driven.

Construction, oil and gas, and manufacturing collectively account for nearly 67% of the remaining demand, with construction benefiting from a 22% rise in urban development projects. Oil and gas applications require high-reliability breakers due to hazardous environments, while manufacturing is increasingly adopting smart protection systems to reduce downtime by 18%. Companies are targeting these segments through customized solutions, strategic partnerships, and flexible pricing models. The key implication is a clear shift toward infrastructure-led demand, requiring advanced, scalable, and compliant protection technologies.

Asia-Pacific accounted for the largest market share at 45% in 2025 however, Europe is expected to register the fastest growth, expanding at a CAGR of 6.1% between 2026 and 2033.

Asia-Pacific leads in volume and production scale, supported by over 52% of global manufacturing output and rapid infrastructure deployment across China and India. North America holds nearly 21% share, driven by grid modernization and a 24% increase in industrial automation adoption. Europe, with around 19% share, leads in innovation, where over 29% of installations now involve energy-efficient and digital breakers due to strict regulatory mandates. A key structural shift is the global push toward localized manufacturing, reducing dependency on cross-border supply chains and improving delivery efficiency by 18%. Demand remains concentrated in Asia-Pacific, while innovation accelerates in Europe and technology adoption strengthens in North America, signaling a multi-polar competitive landscape where companies are aligning investments regionally to balance scale, compliance, and advanced capabilities.

What is driving high-value adoption in advanced electrical protection systems?

North America holds approximately 21% of the global low voltage circuit breaker market, with demand concentrated in industrial automation and commercial infrastructure upgrades. A 26% increase in smart grid investments is driving the deployment of digital breakers, while stricter electrical safety standards are accelerating replacement cycles. A key structural force is the push for grid resilience following extreme weather disruptions, forcing utilities to upgrade protection systems. Execution is shifting toward IoT-enabled breakers, with adoption rising by 23%, improving fault detection and system reliability. Major players are expanding local production capacity by 19% to reduce import dependency. Enterprises increasingly prioritize performance and lifecycle efficiency over upfront cost, signaling a clear investment focus on advanced, integrated protection systems.

How are compliance pressures redefining electrical protection standards?

Europe accounts for nearly 19% of the global market, with demand heavily influenced by regulatory frameworks and sustainability mandates. Countries such as Germany and France are leading adoption due to strict energy efficiency directives, where over 31% of installations now require low-loss circuit breakers. ESG compliance is driving a 22% shift toward energy-efficient systems, reducing operational losses and improving lifecycle performance. Companies are rapidly transitioning to eco-designed products, with a 17% increase in certified green electrical components. Buyers exhibit a compliance-first, quality-driven approach, prioritizing long-term efficiency gains over cost savings. This regulatory intensity is forcing continuous innovation, making Europe a critical region for advanced product development and sustainability-driven differentiation.

Why is rapid deployment and production scale accelerating market dominance?

Asia-Pacific dominates the market with over 45% share, driven by large-scale infrastructure expansion and strong manufacturing capabilities across China, India, and Southeast Asia. The region produces more than 52% of global circuit breaker units, supported by cost-efficient labor and integrated supply chains. Execution is rapidly shifting toward localized production, with a 28% increase in domestic manufacturing capacity to meet rising demand. Smart infrastructure adoption has grown by 25%, accelerating the deployment of intelligent breakers in urban projects. Enterprises prioritize cost, speed, and scalability, leading to high-volume procurement strategies. Global companies are expanding regional facilities and forming joint ventures, making Asia-Pacific the primary hub for both production scale and demand acceleration.

What factors are shaping emerging demand amid structural constraints?

South America contributes approximately 7% to the global market, with demand concentrated in Brazil and Argentina due to ongoing infrastructure and industrial development. A 21% increase in construction activity is driving circuit breaker installations in commercial and residential sectors. However, a key constraint is economic volatility, which has increased project delays by 18% and limited large-scale investments. Execution is shifting toward cost-effective solutions, with 24% of buyers prioritizing affordability over advanced features. Companies are responding by introducing mid-range products and expanding distributor networks to improve market access. While growth potential remains strong, the region presents a balance of opportunity and risk, requiring strategic pricing and localized engagement models.

How are infrastructure investments transforming electrical protection demand?

The Middle East & Africa region holds around 8% of global demand, driven by infrastructure expansion and energy sector investments, particularly in the UAE and Saudi Arabia. Oil and gas, along with large-scale construction projects, account for over 48% of regional demand. A key transformation driver is government-backed infrastructure spending, which has increased by 27%, accelerating deployment of modern electrical systems. Execution is shifting toward high-reliability breakers, with a 19% rise in adoption of advanced protection technologies. Enterprises prioritize durability and performance in extreme conditions, influencing product selection. Companies are forming partnerships with regional contractors and investing in project-based supply models, positioning the region as a strategic growth frontier.

China – 34% market share: Dominates the Low Voltage Circuit Breaker Market due to high production capacity, large-scale infrastructure projects, and strong industrial demand.

United States – 18% market share: Leads in advanced adoption within the Low Voltage Circuit Breaker Market, driven by grid modernization and high penetration of smart electrical systems.

The competitive landscape is defined by global leaders such as Schneider Electric, Siemens, ABB, Eaton, and Mitsubishi Electric competing against regional manufacturers and emerging technology-focused players. The top five players collectively control approximately 57% of the market, creating a semi-consolidated structure where scale and technology leadership dictate positioning. Global OEMs compete on advanced digital integration and product reliability, while regional players focus on cost competitiveness and localized supply.

Competition is increasingly driven by technology differentiation, where smart breakers improve operational efficiency by up to 25%, and supply chain control, reducing lead times by 18%. Companies are actively expanding manufacturing footprints, forming strategic partnerships with automation firms, and investing in R&D for solid-state and IoT-enabled breakers. A key competitive shift is the move toward integrated solutions, combining hardware with analytics platforms, redefining value propositions. Entry barriers remain high due to certification requirements, capital-intensive manufacturing, and established distribution networks. To win, companies must combine technological innovation, localized production, and scalable supply chains to outperform both global incumbents and agile regional competitors.

Schneider Electric

Siemens AG

ABB Ltd

Eaton Corporation

Mitsubishi Electric Corporation

Legrand SA

Fuji Electric Co., Ltd.

Hitachi Industrial Equipment Systems

Hyundai Electric & Energy Systems

Chint Group

Larsen & Toubro Electrical & Automation

Rockwell Automation

Digital and IoT-enabled circuit breakers are now central to operational efficiency, with adoption crossing 31% across industrial and commercial installations. These systems improve fault detection speed by 22% and reduce manual inspection costs by 18%, driven by integration with building management and grid monitoring platforms. Companies are embedding real-time analytics and remote control features, enabling faster response cycles and reducing unplanned downtime, directly enhancing asset reliability. Emerging technologies such as AI-driven predictive maintenance and advanced arc fault detection are reshaping performance benchmarks. AI-enabled breakers improve maintenance efficiency by 27% while reducing failure rates by 21%, with deployment levels nearing 24% in high-load industrial environments. Integration with cloud platforms is accelerating, allowing centralized monitoring across distributed assets, which is optimizing operational visibility and decision-making for large enterprises.

Solid-state circuit breakers represent a disruptive shift, improving switching speed by 30% while reducing energy loss by 15% compared to traditional electromechanical systems. Adoption remains at 12–15% but is rapidly scaling in critical infrastructure. Unlike legacy breakers, these systems eliminate mechanical wear, offering longer lifecycle performance and lower maintenance overhead, creating a clear technological advantage. From 2026–2028, integration of digital twins and edge computing is expected to drive a further 20% improvement in system optimization. Global leaders are accelerating investment in intelligent breaker ecosystems, while regional players focus on cost-efficient digital upgrades. The competitive advantage lies with companies that scale smart, connected solutions faster, as the market shifts decisively toward predictive, automated electrical protection systems.

March 2026 – Schneider Electric launched an upgraded smart circuit breaker platform with integrated IoT monitoring, improving fault detection efficiency by 25% and reducing downtime in commercial buildings. This strengthens its leadership in digital energy management solutions and accelerates adoption in smart infrastructure projects. [Digital Grid Push]

Source: (https://www.se.com)

November 2025 – Siemens AG expanded its low voltage breaker manufacturing capacity in Asia by 20%, aiming to meet rising regional demand and reduce supply chain lead times. This move enhances production agility and strengthens its competitive position in high-growth infrastructure markets. [Capacity Expansion]

Source: (https://www.reuters.com)

July 2025 – ABB Ltd introduced a next-generation air circuit breaker with 18% higher energy efficiency and advanced arc protection technology. The innovation supports compliance with stricter energy standards and improves lifecycle performance for industrial users. [Efficiency Upgrade]

Source: (https://www.abb.com)

January 2024 – Eaton Corporation partnered with a digital automation firm to integrate predictive analytics into its breaker systems, achieving a 23% reduction in maintenance costs for industrial clients. This collaboration reinforces its shift toward service-led, intelligent power management solutions. [Smart Integration]

Source: (https://www.bloomberg.com)

This report provides comprehensive coverage of the low voltage circuit breaker market across five core types, five application areas, and five end-user segments, delivering a structured analysis of demand distribution and technology adoption. It evaluates key regions including Asia-Pacific, North America, Europe, South America, and the Middle East & Africa, capturing over 90% of global demand dynamics. The study incorporates insights across digital breakers, solid-state technologies, and IoT-enabled systems, where adoption levels range between 24% and 31%, highlighting the transition toward intelligent electrical protection.

The analytical depth includes evaluation of more than 12 leading companies, supported by segment-level insights such as a 38% share held by miniature breakers and over 45% demand concentration in Asia-Pacific. It further assesses operational metrics including efficiency improvements of up to 30% and cost reductions exceeding 18% through technology integration. Emerging niches such as predictive maintenance-enabled breakers and decentralized energy protection systems are also examined, reflecting evolving market priorities.

Strategically, the report enables decision-makers to identify high-growth segments, optimize regional expansion, and align investments with technology shifts between 2026 and 2033. It offers actionable intelligence on competitive positioning, supply chain restructuring, and innovation pathways, ensuring businesses can capture value in a rapidly transforming electrical infrastructure landscape.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 5940 Million |

|

Market Revenue in 2033 |

USD 8965.06 Million |

|

CAGR (2026 - 2033) |

5.28% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Schneider Electric, Siemens AG, ABB Ltd, Eaton Corporation, Mitsubishi Electric Corporation, Legrand SA, Fuji Electric Co., Ltd., Hitachi Industrial Equipment Systems, Hyundai Electric & Energy Systems, Chint Group, Larsen & Toubro Electrical & Automation, Rockwell Automation |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |