Reports

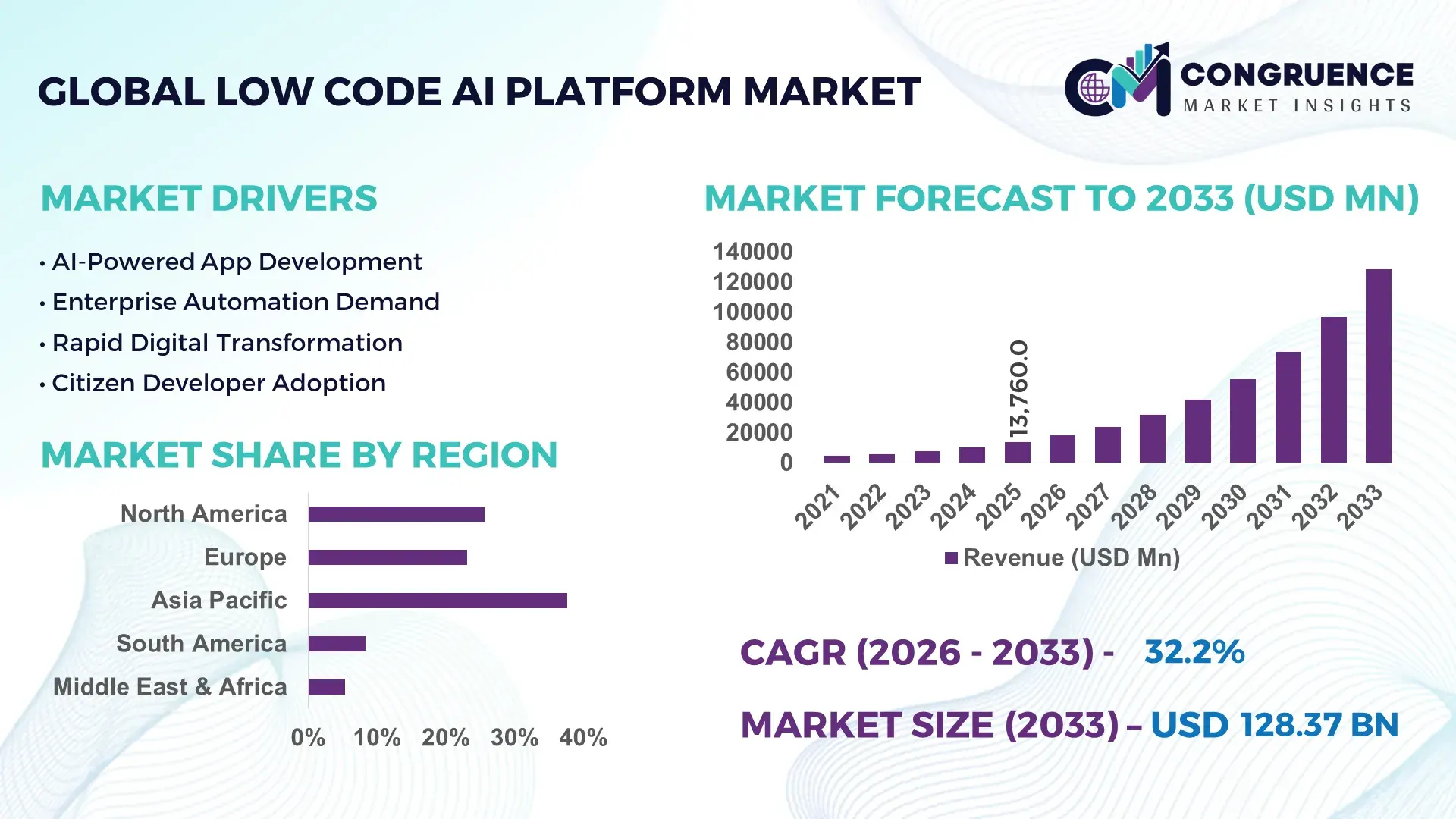

The Global Low Code AI Platform Market was valued at USD 13760 Million in 2025 and is anticipated to reach a value of USD 128371.93 Million by 2033 expanding at a CAGR of 32.2% between 2026 and 2033.

Enterprise demand for accelerated AI deployment, combined with a 40%–60% reduction in application development time through low code automation frameworks, continues to reshape digital transformation budgets across banking, healthcare, retail, and manufacturing sectors. Between 2024 and 2026, stricter AI governance frameworks in the European Union and large-scale generative AI investments across North America and Asia-Pacific pushed organizations toward secure, scalable, and compliance-ready low code AI ecosystems capable of supporting rapid workflow modernization.

The United States maintained market leadership with approximately 38% global platform adoption in 2025, supported by over USD 18 billion in enterprise AI modernization investments and strong deployment across financial services, telecom, and healthcare infrastructure. More than 62% of Fortune 500 enterprises integrated low code AI tools into workflow orchestration and predictive analytics environments, compared with below 35% adoption across several developing economies. China followed with accelerated industrial AI deployment, particularly in smart manufacturing and logistics automation, while India recorded over 45% growth in citizen developer programs across IT services and retail operations. Compared with traditional software engineering models, advanced low code AI platforms improved deployment cycles by nearly 55% while lowering operational integration costs by over 30%.

Organizations prioritizing secure automation, faster AI deployment cycles, and cross-functional application scalability are positioned to capture stronger operational efficiency and long-term competitive resilience in the global low code AI platform market.

Market Size & Growth: USD 13760 Million in 2025 reaching USD 128371.93 Million by 2033, driven by enterprise AI automation and 55% faster application deployment cycles.

Top Growth Drivers: Cloud-native AI adoption exceeded 68%, workflow automation demand rose 52%, and citizen developer participation expanded by 47% globally.

Short-Term Forecast: By 2028, enterprises are projected to reduce software development costs by 35% while improving operational productivity by 41%.

Emerging Technologies: Generative AI copilots, no-code predictive analytics, and API-driven automation platforms increased enterprise integration efficiency by over 44%.

Regional Leaders: North America is projected above USD 46 billion, Asia-Pacific above USD 38 billion, and Europe above USD 24 billion with strong compliance-focused AI adoption.

Consumer/End-User Trends: Nearly 61% of enterprises now allow non-technical departments to build AI-enabled workflows using low code platforms.

Pilot/Case Example: In 2025, a global banking automation project reduced customer onboarding time by 48% using AI-driven low code process orchestration.

Competitive Landscape: Top vendors collectively controlled nearly 49% market share, with competition intensifying across enterprise AI integration and automation ecosystems.

Regulatory & ESG Impact: AI governance mandates improved enterprise compliance monitoring efficiency by 33% across regulated financial and healthcare sectors.

Investment & Funding: Global investments exceeded USD 24 billion between 2024 and 2026, supported by strategic partnerships and regional cloud expansion initiatives.

Innovation & Future Outlook: Autonomous AI agents, embedded analytics, and hybrid deployment models are redefining enterprise software modernization strategies globally.

Banking, healthcare, retail, and manufacturing collectively contributed more than 64% of global low code AI platform deployments in 2025, driven by demand for workflow automation and faster analytics integration. Generative AI-enabled visual development tools improved application configuration efficiency by nearly 43%, while Asia-Pacific recorded over 36% enterprise adoption growth due to expanding digital infrastructure investments. North America continued leading advanced deployments, whereas Europe accelerated compliance-oriented implementations amid evolving AI governance regulations. Increasing integration of autonomous AI assistants and cross-platform orchestration tools is positioning the market toward highly scalable enterprise automation ecosystems, setting the foundation for deeper strategic transformation initiatives.

The low code AI platform market is rapidly transforming into a core competitive infrastructure layer as enterprises prioritize accelerated software delivery, operational automation, and AI-driven decision-making. Organizations deploying low code AI frameworks are reducing application rollout timelines by nearly 55% while optimizing IT operating costs by over 34%, creating measurable advantages in banking, logistics, healthcare, and telecom sectors. Rising pressure from stricter AI governance rules, cybersecurity mandates, and digital workforce shortages is forcing enterprises to replace fragmented legacy environments with scalable automation ecosystems. Generative AI-assisted low code development improves workflow efficiency by 48% while reducing integration expenditure by 31% compared to conventional software engineering systems.

North America leads in deployment volume due to enterprise cloud maturity, while Asia-Pacific leads in adoption acceleration with more than 42% annual expansion in citizen developer programs and AI workflow automation initiatives. Over the next three years, enterprises are projected to automate nearly 60% of repetitive operational workflows using integrated low code AI platforms, significantly improving customer response times and reducing manual processing errors. ESG-focused AI infrastructure strategies are also delivering nearly 22% lower energy utilization through optimized cloud orchestration and resource-efficient automation environments.

In 2025, a multinational healthcare provider improved patient data processing efficiency by 46% after integrating AI-enabled low code analytics across decentralized operations. Simultaneously, major technology vendors are shifting capital allocation toward embedded AI copilots, vertical-specific automation suites, and regional cloud expansion strategies to strengthen enterprise retention. Companies capable of optimizing compliance, deployment speed, and scalable AI orchestration are securing long-term strategic dominance as the competitive landscape rapidly consolidates around intelligent automation leadership.

Enterprise pressure to accelerate digital transformation and reduce software dependency is forcing rapid adoption of low code AI platforms across core industries. Organizations using AI-enabled low code frameworks are cutting application deployment cycles by nearly 55% and reducing operational development costs by over 30%, accelerating enterprise-wide automation strategies. Global shortages of advanced software engineers, combined with rising demand for workflow intelligence, pushed more than 61% of large enterprises toward citizen development programs during 2025. Expanding generative AI integration and cloud modernization initiatives across North America and Asia-Pacific further intensified deployment momentum. In response, technology vendors are accelerating infrastructure expansion, forming strategic hyperscaler partnerships, and increasing investment in industry-specific automation ecosystems to secure long-term enterprise transformation leadership globally.

Despite rapid adoption momentum, integration complexity and governance fragmentation are constraining scalable deployment across enterprise environments. Nearly 43% of organizations continue facing interoperability limitations between legacy infrastructure and AI-enabled low code platforms, increasing implementation delays and workflow inefficiencies. Rising cybersecurity compliance costs and stricter AI governance regulations across Europe and North America have elevated enterprise deployment expenditures by approximately 28% since 2024. Data residency mandates and fragmented cloud architectures are further restricting seamless cross-border AI workflow orchestration. In response, enterprises are diversifying cloud partnerships, adopting hybrid deployment architectures, and negotiating long-term cybersecurity integration contracts. Platform providers are also prioritizing standardized APIs, compliance automation, and modular infrastructure strategies to reduce operational risk and strengthen deployment scalability.

Autonomous AI workflows and embedded analytics are redefining competitive differentiation opportunities across the low code AI platform market. Enterprises integrating AI copilots into workflow automation environments are improving operational productivity by nearly 47% while lowering manual process dependency by over 38%. Emerging economies across Southeast Asia, Latin America, and the Middle East are witnessing accelerated enterprise digitization, creating new demand pockets for scalable low code infrastructure. By 2028, more than 58% of enterprise applications are expected to incorporate AI-assisted development capabilities. Companies are aggressively expanding R&D investment toward autonomous orchestration engines, industry-trained language models, and cross-platform integration ecosystems. Early movers optimizing vertical-specific automation and decentralized AI governance frameworks are positioning themselves for long-term infrastructure dominance and enterprise retention advantages globally.

Scaling enterprise-grade low code AI ecosystems remains challenging due to infrastructure complexity, governance inconsistency, and performance reliability pressures. Nearly 39% of enterprises report workflow instability when integrating advanced AI automation across fragmented multi-cloud environments, while model governance overhead has increased operational management costs by approximately 24%. Growing energy consumption from large-scale AI processing and regional cloud infrastructure constraints are also pressuring long-term deployment sustainability. Organizations expanding automation too rapidly often face process redundancy, shadow IT expansion, and inconsistent security controls across decentralized business units. To remain competitive, platform providers are increasing investment in AI observability tools, scalable orchestration layers, and zero-trust security architectures. Strategic partnerships with cloud operators and cybersecurity firms are becoming critical for sustaining enterprise confidence and operational consistency globally.

58% of Enterprises Are Embedding Generative AI Into Low Code Workflows as organizations shift from rule-based automation toward AI-assisted execution environments. More than 46% of enterprise platforms now include embedded AI copilots for workflow generation, reducing configuration time by nearly 40%. Companies are restructuring development operations around reusable automation templates and centralized AI governance layers to accelerate deployment consistency while managing rising compliance pressure across regulated industries.

44% Faster Deployment Cycles Are Reshaping Enterprise Operations Models as businesses replace fragmented application development with unified low code orchestration environments. Nearly 52% of large enterprises consolidated multiple automation tools into integrated platforms during 2025, improving cross-department workflow visibility and reducing software maintenance overhead by 27%. Labor shortages in advanced software engineering are forcing companies to expand citizen developer programs and scale internal low code certification initiatives.

36% Growth in Asia-Pacific Deployments Is Redefining Regional Demand Patterns as enterprises across India, Southeast Asia, and China accelerate cloud-native AI adoption. North America continues dominating enterprise-scale integrations, while Asia-Pacific leads operational expansion through telecom and manufacturing digitization programs. Companies are increasing regional cloud partnerships and localized compliance infrastructure investments to optimize deployment speed amid evolving data sovereignty regulations.

31% Increase in Subscription-Based Platform Consumption Is Transforming Vendor Business Models as enterprises prioritize scalable consumption pricing over fixed infrastructure commitments. More than 49% of vendors now bundle predictive analytics, workflow monitoring, and AI governance tools into modular subscription ecosystems. A non-obvious shift is emerging where mid-sized enterprises are demanding industry-trained AI workflows instead of generic automation stacks, forcing providers to redesign vertical-specific platform architectures and partnership strategies.

The low code AI platform market is segmented by type, application, and end-user, reflecting shifting enterprise priorities toward scalable automation and AI-driven operational efficiency. Cloud-Based platforms account for nearly 48% of deployments due to flexibility and lower infrastructure dependency, while AI-Assisted Development Tools are experiencing accelerated adoption across enterprise modernization initiatives. Workflow Automation and Application Development collectively contribute over 52% of platform usage as organizations prioritize faster execution and reduced manual processes. BFSI and IT & Telecom remain dominant end-users because of high workflow complexity and compliance requirements, while healthcare and manufacturing are rapidly expanding adoption through predictive analytics and process optimization initiatives, reshaping long-term enterprise automation investment strategies globally.

Cloud-Based platforms dominate the low code AI platform market with nearly 48% share due to faster deployment capabilities, scalable infrastructure integration, and lower operational maintenance requirements. Enterprises increasingly prefer cloud-native environments because they improve application deployment efficiency by over 42% while reducing infrastructure dependency across distributed operations. Hybrid Development Platforms are emerging as the fastest-growing segment, recording adoption growth above 39% as organizations seek greater control over sensitive workloads while maintaining scalable AI orchestration flexibility. Compared with traditional On-Premises systems, hybrid architectures improve integration agility by nearly 33%, particularly across regulated industries managing complex data governance requirements.

No-Code Platforms continue expanding across non-technical business teams, accounting for approximately 18% of market demand as enterprises accelerate citizen developer strategies to offset software talent shortages. Meanwhile, AI-Assisted Development Tools and On-Premises deployments collectively represent nearly 29% share, maintaining strategic relevance in industries requiring advanced customization, internal governance, and legacy system continuity. Companies are increasingly prioritizing AI-enabled automation ecosystems, expanding cloud infrastructure partnerships, and integrating vertical-specific development capabilities. Investment momentum is shifting toward scalable hybrid and AI-assisted environments, while purely legacy on-premises deployments are gradually declining in strategic importance due to operational rigidity and higher maintenance complexity.

“According to a 2025 report by the International Data Corporation (IDC), cloud-based AI development platforms were adopted by over 64% of enterprise software teams, resulting in nearly 41% faster deployment efficiency and significant infrastructure optimization, reinforcing their growing strategic importance.”

Workflow Automation leads the low code AI platform market with approximately 32% share as enterprises prioritize operational streamlining, repetitive task reduction, and real-time process orchestration. High deployment concentration exists because organizations are increasingly integrating AI-driven automation into finance, customer operations, and supply chain management environments to improve execution speed and reduce dependency on manual workflows. Predictive Modeling is the fastest-growing application segment, expanding above 37% due to rising enterprise demand for forecasting intelligence, anomaly detection, and AI-supported decision automation. Compared with mature Workflow Automation deployments, Predictive Modeling reflects a strategic shift toward proactive business optimization and intelligent operational forecasting.

Application Development and Customer Service Automation collectively contribute nearly 34% of market demand as organizations accelerate omnichannel engagement and rapid software modernization initiatives. Data Analytics and Process Optimization maintain growing relevance across manufacturing, healthcare, and telecom industries where enterprises require scalable performance visibility and operational precision. Companies are responding by embedding AI copilots, expanding process orchestration capabilities, and restructuring platform offerings around industry-specific workflows. Demand is shifting toward integrated automation ecosystems capable of combining analytics, prediction, and workflow execution within unified interfaces, redefining how enterprises manage operational scalability and digital transformation priorities.

“According to a 2025 report by the World Economic Forum, workflow automation solutions were deployed across over 72,000 organizations globally, improving operational processing efficiency by 44%, highlighting their rapid operational adoption.”

BFSI dominates the low code AI platform market with nearly 29% share due to high transaction volumes, strict compliance requirements, and growing reliance on AI-enabled workflow automation. Financial institutions increasingly deploy low code AI platforms to optimize fraud detection, automate onboarding, and accelerate customer service operations, improving processing efficiency by more than 38%. Healthcare represents the fastest-growing end-user segment with adoption expansion exceeding 41%, driven by decentralized patient management, predictive diagnostics integration, and increasing regulatory pressure for digital health modernization. Compared with BFSI’s process-centric deployments, healthcare demand is shifting toward intelligent analytics and real-time operational coordination.

IT and Telecom, along with Retail and E-commerce, collectively account for approximately 36% of market demand as companies prioritize scalable application development, omnichannel automation, and customer engagement optimization. Manufacturing and Government sectors are accelerating adoption through process optimization and compliance-oriented digital infrastructure modernization initiatives. Vendors are responding with industry-specific pricing models, AI governance features, and strategic cloud partnerships to strengthen enterprise retention across high-value sectors. Future demand is increasingly concentrating around industries requiring continuous workflow orchestration, predictive intelligence, and secure decentralized operations, forcing providers to redesign platform architectures for sector-specific scalability and operational resilience.

“According to a 2025 report by the International Telecommunication Union (ITU), adoption among healthcare organizations increased by 43%, with over 18,000 institutions implementing AI-enabled low code automation solutions, leading to nearly 36% improvement in administrative efficiency, indicating a strong shift in demand dynamics.”

North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 35.8% between 2026 and 2033.

North America maintains demand concentration through large-scale enterprise AI modernization and advanced cloud infrastructure adoption, while Europe captures nearly 24% share through compliance-driven automation deployment across financial and healthcare sectors. Asia-Pacific is rapidly accelerating enterprise adoption, supported by over 42% expansion in citizen developer programs and aggressive telecom and manufacturing digitization initiatives across China, India, and Southeast Asia. Europe leads in governance-focused AI integration, whereas Asia-Pacific dominates operational scaling speed and deployment expansion. Rising global data localization requirements and regional cloud infrastructure investments are reshaping deployment strategies worldwide. Companies are increasingly prioritizing North America for enterprise-scale monetization, Europe for regulatory-grade innovation, and Asia-Pacific for scalable automation expansion and long-term user acquisition.

North America commands nearly 38% of global low code AI platform demand, driven by large-scale deployment across BFSI, healthcare, telecom, and retail sectors. More than 64% of Fortune 500 enterprises now integrate AI-enabled low code workflows into operational automation environments to reduce deployment complexity and optimize decision-making speed. Tightening AI governance frameworks and cybersecurity regulations are forcing enterprises to shift toward centralized, compliance-ready automation ecosystems. Organizations adopting AI-assisted development tools improved workflow execution efficiency by approximately 44% during 2025. Major vendors are expanding cloud infrastructure partnerships and embedding generative AI copilots into enterprise platforms. Enterprises increasingly prioritize scalable, secure, and vertically integrated automation ecosystems, making North America the primary region for high-value enterprise deployment and platform monetization strategies.

Europe contributes nearly 24% of the global low code AI platform market, with Germany, the United Kingdom, and France leading enterprise adoption across financial services, manufacturing, and public administration sectors. Expanding AI governance mandates and strict data sovereignty regulations are redefining enterprise software deployment strategies, forcing organizations to prioritize compliant and auditable automation ecosystems. More than 51% of large enterprises now demand embedded governance controls and localized cloud infrastructure within low code AI environments. Companies implementing compliance-oriented workflow automation improved operational transparency by nearly 36% while reducing regulatory reporting delays. Vendors are responding through sovereign cloud partnerships, ESG-focused infrastructure optimization, and secure AI orchestration capabilities. Europe continues forcing innovation around trustworthy, regulation-ready automation frameworks that increasingly shape global enterprise deployment standards.

Asia-Pacific ranks as the fastest-expanding low code AI platform market, supported by aggressive enterprise digitization across China, India, Japan, and Southeast Asia. The region accounts for nearly 31% of global deployment activity, with telecom, manufacturing, and e-commerce sectors accelerating large-scale AI workflow adoption. More than 42% growth in citizen developer programs and cloud-native enterprise applications is reshaping operational scaling strategies. Regional advantages in digital infrastructure expansion, technology outsourcing ecosystems, and lower deployment costs continue strengthening enterprise platform penetration. Major providers are increasing localized cloud capacity and AI integration partnerships to support rising enterprise workloads. Organizations across Asia-Pacific prioritize deployment speed, scalability, and operational cost efficiency, positioning the region as a critical expansion hub for long-term enterprise automation and platform ecosystem growth.

South America represents approximately 5% of the global low code AI platform market, with Brazil and Argentina leading enterprise adoption across banking, retail, and public sector modernization initiatives. Growing pressure to improve operational efficiency and customer service automation is accelerating demand for cloud-enabled AI workflows. However, infrastructure limitations, uneven cloud penetration, and technology budget constraints continue restricting large-scale deployment consistency across several economies. Nearly 34% of enterprises shifted toward subscription-based low code environments during 2025 to reduce upfront technology expenditure and deployment risk. Vendors are increasingly targeting localized partnerships and industry-specific automation models to address regional operational requirements. The region presents strong long-term expansion potential, although scalability and infrastructure readiness remain critical competitive barriers for sustained adoption momentum.

The Middle East & Africa accounts for nearly 7% of global low code AI platform demand, led by the United Arab Emirates, Saudi Arabia, and South Africa through large-scale smart infrastructure and digital government initiatives. Oil and gas, construction, banking, and public sector transformation programs are accelerating adoption of AI-enabled workflow orchestration and process automation platforms. More than 39% of regional enterprises increased cloud automation deployment during 2025 as governments intensified investments in digital infrastructure modernization. Strategic partnerships between cloud providers and regional telecom operators are expanding enterprise-grade AI deployment capacity. Organizations increasingly prioritize scalable automation tools that reduce operational complexity and improve service responsiveness. The region is emerging as a strategic growth corridor for infrastructure-led enterprise AI transformation and long-term cloud ecosystem expansion.

United States – 38% market share in the Low Code AI Platform market due to advanced enterprise cloud infrastructure, high AI workflow adoption, and strong demand from BFSI, healthcare, and telecom sectors.

China – 19% market share in the Low Code AI Platform market driven by large-scale manufacturing digitization, aggressive enterprise AI deployment, and expanding government-backed automation initiatives.

The low code AI platform market is dominated by competition between global enterprise software leaders, cloud-native automation providers, and AI-focused workflow innovators including Microsoft, Salesforce, ServiceNow, OutSystems, and Mendix. The top five players collectively control nearly 49% of market activity through integrated AI ecosystems, enterprise cloud reach, and large-scale workflow orchestration capabilities. Competition is increasingly centered on deployment speed, AI-assisted automation depth, customization flexibility, and governance integration, with enterprises demanding nearly 44% faster workflow execution and over 31% lower operational development costs. Vendors are aggressively expanding through hyperscaler partnerships, vertical-specific automation suites, and embedded generative AI copilots. Market dynamics are shifting from standalone low code platforms toward fully integrated enterprise automation ecosystems, accelerating consolidation pressure. High infrastructure investment requirements, compliance complexity, and enterprise integration demands remain major entry barriers. Winning requires scalable AI orchestration, trusted governance capabilities, and deep industry-specific workflow intelligence.

Microsoft Corporation

Salesforce Inc.

ServiceNow Inc.

OutSystems

Mendix

Appian Corporation

Pegasystems Inc.

Oracle Corporation

SAP SE

Zoho Corporation

Creatio

Kissflow

Quickbase

IBM Corporation

Generative AI copilots, visual workflow orchestration, and AI-assisted development engines are currently reshaping the low code AI platform market. More than 62% of enterprise platforms now integrate embedded AI copilots to automate application logic generation, reducing workflow configuration time by nearly 41%. Compared with legacy rule-based automation systems, AI-assisted low code environments improve deployment efficiency by over 48% while lowering integration costs by approximately 29%. Enterprises across BFSI and healthcare sectors are increasingly adopting centralized AI governance layers and API-driven orchestration frameworks to improve compliance visibility and operational scalability. Vendors prioritizing unified workflow ecosystems are gaining stronger enterprise retention advantages through faster deployment execution and lower customization dependency.

Emerging technologies between 2026 and 2028 are centered on multi-agent orchestration, autonomous workflow execution, and hybrid cloud AI integration. Nearly 46% of large enterprises are deploying cross-platform AI agents capable of coordinating customer service, analytics, and operational automation within a single environment. AI fabric architectures and low code orchestration engines are improving process execution accuracy by more than 35%, especially across telecom and manufacturing operations. Companies are responding by restructuring platform architectures around modular AI agents, embedded analytics, and real-time governance controls to optimize operational continuity and enterprise-scale automation management.

Disruptive innovation is accelerating around autonomous enterprise AI systems, multimodal automation interfaces, and intelligent process simulation tools. Advanced AI workflow platforms are now capable of resolving up to 91% of repetitive enterprise service tasks without human intervention, significantly reducing operational bottlenecks and labor dependency. Organizations deploying intelligent orchestration layers are improving service resolution speed by nearly 50% while optimizing infrastructure utilization. Global technology providers are aggressively expanding AI partnership ecosystems, vertical-specific automation libraries, and low code developer environments, positioning intelligent workflow orchestration as a decisive competitive advantage through 2028.

March 2024 – Salesforce launched Einstein 1 Studio, introducing low-code AI tools for customizing Einstein Copilot and embedding generative AI into CRM workflows. The platform supported over 6 million Trailhead users with integrated AI development capabilities, accelerating enterprise workflow automation and AI deployment scalability. [AI Workflow Expansion] Source: salesforce.com (Salesforce Investor Relations)

May 2025 – ServiceNow unveiled its new AI Platform integrating orchestration across Microsoft, NVIDIA, Google, and Oracle ecosystems. The platform strengthened enterprise-wide workflow automation while supporting unified AI governance and multi-model integration, accelerating deployment efficiency across global enterprise operations. [Enterprise AI Orchestration] Source: newsroom.servicenow.com (ServiceNow Newsroom)

March 2025 – ServiceNow introduced its Yokohama platform release featuring thousands of preconfigured AI agents for CRM, HR, and IT operations. The release improved workflow deployment speed and enabled faster AI lifecycle management, significantly optimizing enterprise automation execution across operational environments. [Agentic Workflow Scaling]

May 2025 – ServiceNow launched AI Control Tower and AI Agent Fabric to centralize governance, security, and interoperability across enterprise AI agents and workflows. Strategic integrations with companies including IBM and Google Cloud strengthened enterprise orchestration capabilities while improving responsible AI deployment visibility. [Governance Layer Integration]

This report delivers comprehensive analysis of the low code AI platform market across core technology segments, deployment models, applications, end-user industries, and regional ecosystems. Coverage includes Cloud-Based, On-Premises, No-Code Platforms, Hybrid Development Platforms, and AI-Assisted Development Tools, alongside critical applications such as Workflow Automation, Predictive Modeling, Data Analytics, and Process Optimization. The study evaluates enterprise adoption across BFSI, healthcare, manufacturing, retail, IT and telecom, and government sectors spanning North America, Europe, Asia-Pacific, South America, and the Middle East & Africa. Advanced technology assessment includes generative AI copilots, autonomous workflow orchestration, AI governance layers, multi-agent systems, and hybrid cloud automation architectures shaping enterprise deployment strategies between 2026 and 2033.

The report analyzes more than 20 strategic market indicators including enterprise adoption concentration, deployment trends, workflow automation penetration, and operational efficiency benchmarks. Over 62% enterprise integration levels for AI-assisted workflows and nearly 48% deployment concentration in cloud-based environments are evaluated to identify execution-level market shifts and competitive positioning patterns. Detailed company profiling, regional demand mapping, technology benchmarking, and operational comparison frameworks provide actionable insight for investment planning, expansion prioritization, partnership evaluation, and competitive differentiation. The report also highlights emerging niche opportunities including decentralized AI governance, industry-trained automation ecosystems, and autonomous enterprise orchestration environments redefining long-term market evolution.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 13760 Million |

|

Market Revenue in 2033 |

USD 128371.93 Million |

|

CAGR (2026 - 2033) |

32.2% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Microsoft Corporation, Salesforce Inc., ServiceNow Inc., OutSystems, Mendix, Appian Corporation, Pegasystems Inc., Oracle Corporation, SAP SE, Zoho Corporation, Creatio, Kissflow, Quickbase, IBM Corporation |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |