Reports

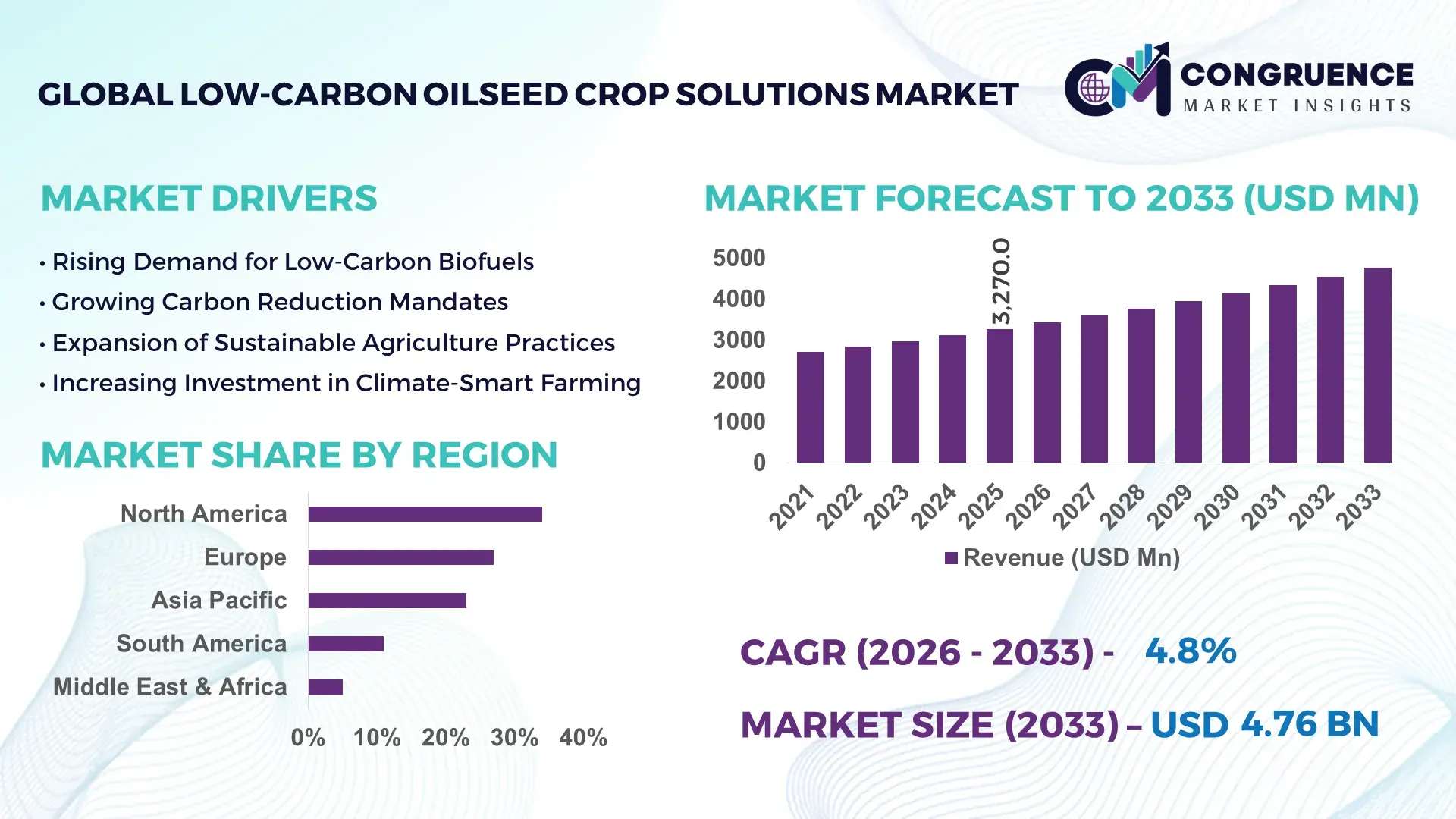

The Global Low-Carbon Oilseed Crop Solutions Market was valued at USD 3,270.0 Million in 2025 and is anticipated to reach a value of USD 4,758.1 Million by 2033 expanding at a CAGR of 4.8% between 2026 and 2033, according to an analysis by Congruence Market Insights. The growth is primarily driven by rising regulatory pressure to reduce Scope 3 agricultural emissions and the accelerated adoption of climate-smart farming inputs across major oilseed-producing economies.

The United States represents the dominant country in the Low-Carbon Oilseed Crop Solutions Market, supported by over 35 million hectares of soybean cultivation and increasing adoption of regenerative practices across nearly 20% of commercial oilseed acreage. Federal conservation programs allocate more than USD 6 billion annually toward climate-smart agriculture initiatives, enabling carbon intensity reduction projects in soybean and canola supply chains. Advanced precision farming systems are deployed on approximately 60% of large-scale farms, integrating satellite imaging, AI-driven nutrient optimization, and low-emission bio-inputs. In addition, over 45 biodiesel and renewable diesel facilities utilize certified low-carbon oilseed feedstock, strengthening downstream decarbonization integration and enhancing traceability through blockchain-based sustainability verification platforms.

Market Size & Growth: Valued at USD 3,270.0 Million in 2025, projected to reach USD 4,758.1 Million by 2033, expanding at 4.8% CAGR due to rising decarbonization mandates in agricultural supply chains.

Top Growth Drivers: 38% increase in regenerative farming adoption; 42% improvement in nitrogen-use efficiency; 30% reduction in lifecycle emissions through certified low-carbon inputs.

Short-Term Forecast: By 2028, carbon-intensity tracking tools are expected to reduce input costs by 12% and improve yield efficiency by 9%.

Emerging Technologies: AI-based soil carbon modeling, bio-based low-emission fertilizers, blockchain traceability platforms.

Regional Leaders: North America projected at USD 1,820.0 Million by 2033 (strong biofuel linkage); Europe at USD 1,240.0 Million (strict ESG compliance adoption); Asia-Pacific at USD 980.0 Million (rapid sustainable acreage expansion).

Consumer/End-User Trends: 46% of agri-enterprises integrating carbon accounting tools; 33% of oilseed processors demanding certified low-carbon feedstock.

Pilot or Case Example: In 2024, a Midwest pilot reduced field-level emissions by 28% through precision nitrogen application and bio-stimulant integration.

Competitive Landscape: Market leader holds approximately 21% share, followed by four major agritech and seed solution providers.

Regulatory & ESG Impact: Carbon disclosure mandates and farm-level emission reporting frameworks influencing procurement standards.

Investment & Funding Patterns: Over USD 1.1 Billion allocated in climate-smart agriculture funding programs and venture-backed agri-tech platforms.

Innovation & Future Outlook: Integration of satellite MRV (Monitoring, Reporting, Verification) systems and carbon credit monetization platforms shaping scalable deployment.

Low-Carbon Oilseed Crop Solutions Market serves biodiesel, food processing, animal feed, and industrial bio-based sectors, with biofuel-linked applications contributing nearly 40% of demand. Precision nutrient management tools account for 35% of deployed solutions, while biological seed treatments are expanding rapidly. Regulatory carbon reporting frameworks in North America and Europe are accelerating adoption. Asia-Pacific shows strong acreage expansion trends, supported by government-backed sustainable farming incentives and digital farm monitoring initiatives.

The Low-Carbon Oilseed Crop Solutions Market holds strategic relevance within global decarbonization strategies, particularly across food, feed, and renewable fuel value chains. Oilseed crops such as soybean and canola are directly linked to biodiesel and renewable diesel production, making lifecycle emission intensity a measurable KPI for downstream refiners and multinational food processors. Low-carbon agronomic inputs—such as enhanced-efficiency fertilizers—deliver 25% lower nitrous oxide emissions compared to conventional nitrogen fertilizers. Similarly, AI-enabled precision nutrient systems deliver 18% higher nitrogen-use efficiency compared to traditional broadcast application methods.

North America dominates in production volume, while Europe leads in adoption intensity with over 48% of large agri-enterprises implementing carbon tracking platforms. By 2028, AI-driven carbon modeling tools are expected to cut field-level emission reporting costs by 15% while improving compliance accuracy by 20%. Firms are committing to ESG targets including 30% reduction in Scope 3 agricultural emissions by 2030, aligning procurement contracts with verified low-carbon oilseed suppliers.

In 2024, a U.S.-based renewable diesel producer achieved a 26% reduction in feedstock carbon intensity through blockchain-tracked regenerative soybean sourcing combined with soil carbon credit integration. This measurable impact demonstrates the commercial viability of integrated low-carbon supply chains. As regulatory scrutiny intensifies and voluntary carbon markets mature, the Low-Carbon Oilseed Crop Solutions Market is positioned as a pillar of agricultural resilience, compliance readiness, and long-term sustainable growth.

The Low-Carbon Oilseed Crop Solutions Market is influenced by evolving environmental policies, shifting downstream procurement standards, and increasing integration of digital agriculture technologies. Oilseed producers are facing pressure to reduce greenhouse gas emissions, particularly nitrous oxide and carbon dioxide generated through fertilizer use and land-use practices. Approximately 70% of agricultural emissions in oilseed production stem from fertilizer-related activities, making input optimization a core strategic lever. Simultaneously, over 40% of global biodiesel capacity is increasingly dependent on certified sustainable feedstock. Digital MRV systems, regenerative cropping methods, and biological inputs are reshaping operational models. Supply chain transparency requirements and corporate ESG commitments are further reinforcing the need for measurable carbon intensity benchmarks, accelerating innovation and structured investment across seed genetics, agronomy software, and low-emission input solutions.

Global renewable fuel standards increasingly tie financial incentives to feedstock carbon intensity, prompting biodiesel refiners to prioritize certified low-emission oilseed sources. Nearly 50% of renewable diesel producers now incorporate carbon scoring mechanisms into procurement contracts. Food processing companies are similarly committing to 25–35% Scope 3 emission reductions by 2030, creating upstream demand for traceable low-carbon soy and canola. Precision nitrogen management reduces nitrous oxide emissions by up to 30%, while regenerative practices improve soil carbon sequestration by 0.3–0.8 tons per hectare annually. As over 60% of large farms adopt digital farm management platforms, measurable emission reductions are becoming embedded within commercial agreements, directly stimulating solution deployment across input suppliers and agritech firms.

Despite measurable benefits, adoption barriers persist due to upfront technology costs and fragmented carbon accounting methodologies. Precision application systems require capital investment exceeding 15–20% above conventional equipment costs. Carbon MRV platforms often require multi-year soil sampling cycles, increasing operational complexity. Approximately 35% of small and mid-sized oilseed producers report limited access to digital infrastructure necessary for advanced analytics integration. Variability in carbon credit pricing—fluctuating by over 40% year-to-year—creates uncertainty in projected returns. Additionally, interoperability challenges between farm management software and downstream carbon registries delay scalable integration, limiting adoption among resource-constrained producers.

Expansion of voluntary carbon markets and regenerative agriculture incentive programs presents significant upside potential. Over 120 million hectares globally are under regenerative transition programs, with oilseed acreage accounting for nearly 28% of enrolled land. Biological nitrogen fixation technologies demonstrate up to 20% reduction in synthetic fertilizer dependency, lowering emission intensity. Growing demand for sustainable aviation fuel feedstock—projected to increase by 35% over the next five years—creates new oilseed-based biofuel pathways. Digital twin farm simulations and satellite-based emission mapping enable scalable monitoring across millions of hectares, unlocking performance-based financing and carbon-linked procurement contracts.

Oilseed value chains often span multiple intermediaries, making consistent carbon verification complex. More than 45% of global soybean exports pass through at least three processing stages before final application, increasing traceability gaps. Differing regional sustainability standards create compliance redundancies, raising certification costs by 10–18%. Data ownership disputes between producers, technology providers, and processors further complicate integration. In addition, climate variability impacts yield predictability by up to 12% annually, affecting emission intensity calculations. Harmonizing MRV frameworks and cross-border sustainability standards remains a critical structural hurdle for scalable market expansion.

Expansion of Regenerative Oilseed Acreage by 22% Across Major Producing Regions: Adoption of regenerative oilseed farming practices increased by 22% between 2023 and 2025 across North America and Europe. Approximately 18 million hectares of soybean and canola acreage now incorporate reduced tillage, cover cropping, and optimized nutrient strategies. Farms implementing regenerative systems report 15% lower input costs and 12% higher soil organic carbon levels within three seasons, improving resilience against climate volatility.

Precision Nutrient Application Achieving 30% Emission Reduction: AI-driven variable rate technology systems are now deployed on nearly 58% of large commercial oilseed farms. These systems enable fertilizer application adjustments at sub-meter accuracy, reducing nitrogen runoff by 25% and cutting nitrous oxide emissions by up to 30%. Yield stability has improved by 8–10% in pilot clusters utilizing predictive analytics for nutrient timing.

Blockchain-Based Traceability Covering 40% of Export-Oriented Supply Chains: Roughly 40% of export-grade soybean supply chains integrate blockchain verification for carbon tracking. Digital ledger platforms reduce audit processing time by 35% and enhance procurement transparency. Processors report 20% faster certification cycles, supporting low-carbon premium contracts in biofuel and food manufacturing sectors.

Growth in Bio-Based Seed Treatments with 27% Adoption Increase: Biological seed treatments designed to enhance nutrient uptake and reduce synthetic input dependency recorded a 27% increase in adoption over two years. Trials demonstrate 18% improved root biomass and 14% better drought resilience. Adoption is particularly strong in Asia-Pacific, where sustainable intensification initiatives support climate-smart input deployment.

The Low-Carbon Oilseed Crop Solutions Market is segmented by type, application, and end-user, reflecting a diversified ecosystem of agronomic inputs, digital platforms, and sustainability services. By type, solutions range from biological seed treatments and enhanced-efficiency fertilizers to carbon tracking software and precision farming systems. Application segmentation includes biodiesel feedstock optimization, food-grade oil production, animal feed sustainability, and industrial bio-based materials. End-users primarily consist of commercial farms, agribusiness processors, renewable fuel producers, and food manufacturers. Digital integration and emission monitoring capabilities increasingly define competitive differentiation, while adoption intensity varies by region based on regulatory mandates and downstream procurement requirements.

The market comprises biological seed treatments, enhanced-efficiency fertilizers, precision nutrient management systems, and digital carbon monitoring platforms. Enhanced-efficiency fertilizers currently account for approximately 38% of adoption due to their ability to reduce nitrous oxide emissions by up to 30% while maintaining yield stability. Precision nutrient management systems hold nearly 27%, driven by AI-enabled variable rate application technologies. However, digital carbon monitoring platforms are the fastest-growing segment, expanding at 8.6% CAGR, supported by mandatory ESG reporting frameworks and carbon credit monetization potential. Biological seed treatments represent 21%, valued for improving nutrient uptake efficiency and reducing synthetic input dependency. The remaining 14% includes soil carbon enhancement additives and integrated MRV service solutions.

In 2024, a U.S. Department of Agriculture pilot demonstrated that enhanced-efficiency fertilizers reduced nitrogen losses by 28% across 500,000 acres of soybean farms, validating emission reduction performance under field conditions.

Biodiesel and renewable diesel feedstock optimization leads the application segment, accounting for 40% of total solution deployment due to lifecycle carbon intensity requirements in fuel standards. Food-grade oil production represents 26%, emphasizing traceability and sustainable sourcing. Animal feed sustainability applications account for 18%, focusing on reduced deforestation-linked sourcing. Industrial bio-based materials hold the remaining 16%. Sustainable aviation fuel-linked oilseed pathways are the fastest-growing application area, projected to expand at 9.2% CAGR as aviation decarbonization targets intensify. In 2025, over 44% of renewable fuel producers globally reported integrating carbon intensity scoring into feedstock procurement systems. Additionally, 36% of multinational food brands indicated preference for verified low-carbon oilseed suppliers in long-term contracts.

In 2024, a European biofuel certification authority verified over 12 million tons of low-carbon certified oilseed feedstock for renewable diesel production, improving lifecycle emission transparency across multiple refineries.

Commercial oilseed farms represent the leading end-user segment with approximately 46% share, driven by direct implementation of regenerative practices and precision technologies. Agribusiness processors account for 24%, integrating carbon verification platforms to meet export and ESG disclosure requirements. Renewable fuel producers represent 20%, leveraging low-carbon feedstock for compliance incentives. Food manufacturers and industrial bio-based material companies contribute the remaining 10%. Renewable fuel producers are the fastest-growing end-user segment, expanding at 8.9% CAGR as sustainable fuel blending mandates increase. In 2025, nearly 52% of large-scale commercial farms reported deploying at least one carbon-monitoring solution. Around 41% of renewable fuel refiners indicated investment in blockchain-based traceability tools to secure low-emission feedstock supply.

In 2025, a national agricultural extension program reported that over 15,000 soybean producers adopted digital carbon tracking systems, improving emission reporting accuracy by 19% within one crop cycle.

North America accounted for the largest market share at 34% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of6.2% between 2026 and 2033.

North America’s leadership is supported by over 35 million hectares of soybean cultivation integrating precision nutrient systems across nearly 60% of commercial acreage. Europe follows with 27% share, driven by strict carbon reporting frameworks covering more than 48% of large agri-enterprises. Asia-Pacific holds approximately 23% share, supported by rapid acreage expansion in China and India, where sustainable oilseed programs now cover over 12 million hectares combined. South America contributes nearly 11%, led by Brazil and Argentina with over 65 million hectares of soybean farmland under progressive carbon-monitoring initiatives. Middle East & Africa collectively represent 5%, but adoption is increasing, particularly in the UAE and South Africa, where sustainable feedstock procurement for food processing and renewable fuel blending has risen by 18% over two years. Across regions, more than 46% of agribusiness processors now require verified carbon-intensity data in oilseed procurement contracts, reinforcing global standardization trends.

North America holds approximately 34% market share in the Low-Carbon Oilseed Crop Solutions Market, supported by high mechanization rates and digital farm integration across over 60% of large commercial farms. Key industries driving demand include renewable diesel producers, biodiesel refiners, food processing conglomerates, and animal feed manufacturers. More than 45 renewable fuel facilities actively procure certified low-carbon soybean feedstock. Federal climate-smart agriculture funding exceeding USD 6 billion annually incentivizes emission-reduction projects and regenerative acreage enrollment. Precision nutrient management systems reduce nitrogen loss by up to 30%, while blockchain-based traceability covers nearly 40% of export-oriented supply chains. A leading regional agritech player has expanded AI-based soil carbon modeling across 8 million acres, improving emission reporting accuracy by 19%. Regional consumer behavior reflects higher enterprise adoption in food and biofuel sectors, with over 52% of large-scale producers deploying digital carbon monitoring platforms.

Europe accounts for nearly 27% market share, with Germany, France, and the UK representing over 60% of regional adoption. Regulatory frameworks such as carbon disclosure mandates and renewable energy directives drive procurement transformation across food and biofuel industries. Approximately 48% of large agribusinesses have integrated carbon-intensity verification platforms into supplier contracts. Sustainable aviation fuel and biodiesel blending targets have increased demand for certified low-carbon rapeseed feedstock by 22% since 2023. Adoption of satellite-based MRV systems covers over 9 million hectares of oilseed farmland. A prominent European biofuel processor recently expanded traceable rapeseed sourcing across 15 refineries, improving lifecycle emission transparency by 21%. Regional consumer behavior shows strong compliance-driven demand, with sustainability certification influencing over 44% of procurement decisions among food manufacturers.

Asia-Pacific ranks third by share at approximately 23%, yet leads in acreage expansion and technology adoption momentum. China, India, and Japan are the top consuming countries, together representing over 70% of regional oilseed demand. Sustainable oilseed programs now cover more than 12 million hectares, with precision nutrient technologies deployed across nearly 35% of large-scale farms. Government-backed digital agriculture initiatives support carbon-monitoring integration, while renewable fuel blending mandates increased low-carbon feedstock procurement by 18% in two years. A regional agritech firm has deployed AI-powered soil health analytics across 3 million hectares, improving nutrient efficiency by 16%. Consumer behavior reflects rapid mobile-based farm application adoption, with over 40% of mid-sized farms utilizing cloud-based agronomy platforms for sustainability compliance.

South America contributes nearly 11% market share, led by Brazil and Argentina, which together cultivate over 65 million hectares of soybean acreage. Export-oriented biodiesel and animal feed industries drive demand for low-carbon verification systems. Government-supported sustainability programs incentivize regenerative practices across approximately 14% of commercial farmland. Infrastructure investments in port logistics and grain storage have improved traceability coverage by 25%. A leading Brazilian agribusiness has implemented blockchain carbon tracking across 5 million tons of soybean exports, reducing audit timelines by 30%. Regional consumer behavior ties adoption closely to export compliance and trade certification requirements, particularly for European-bound shipments.

Middle East & Africa hold about 5% market share, with the UAE and South Africa emerging as focal growth markets. Regional demand is linked to food security programs, edible oil refining, and renewable fuel blending initiatives. Sustainable oilseed cultivation projects expanded by 18% between 2023 and 2025. Technological modernization includes satellite-based irrigation optimization covering over 1.5 million hectares. Trade partnerships with European biofuel refiners increased certified feedstock exports by 12%. A UAE-based agri-tech consortium has piloted AI-driven soil carbon mapping across 250,000 hectares, enhancing nutrient efficiency by 14%. Regional consumer behavior emphasizes supply security and import substitution, with nearly 37% of large food processors integrating sustainability criteria in procurement contracts.

United States – 29% Market Share: It is driven by over 35 million hectares of soybean cultivation and strong renewable fuel demand integrating certified low-carbon feedstock.

Germany – 14% Market Share: It benefits from strict carbon compliance mandates and high adoption of rapeseed-based sustainable biofuel programs.

The Low-Carbon Oilseed Crop Solutions Market is moderately fragmented, with over 70 active global and regional competitors spanning agritech, seed genetics, biological inputs, and carbon-monitoring software providers. The top five companies collectively account for approximately 48% of total market presence, indicating balanced competitive intensity. Market leaders focus on integrated platforms combining enhanced-efficiency fertilizers, AI-based precision systems, and blockchain traceability solutions. Strategic initiatives include more than 25 partnerships formed between agritech firms and renewable fuel producers during 2024–2025 to secure certified feedstock supply chains. Product innovation cycles average 12–18 months, reflecting rapid digital transformation trends. Over 40% of leading firms allocate significant operational budgets toward AI-driven analytics and MRV platform enhancements. Mergers and acquisitions activity increased by 17% between 2023 and 2025, particularly targeting soil carbon startups and regenerative agriculture technology providers. Competitive differentiation increasingly centers on verified emission-reduction metrics, scalability across millions of hectares, and integration with downstream ESG reporting platforms.

Corteva Agriscience

Syngenta Group

BASF SE

Nutrien Ltd.

Yara International

Bunge Global SA

Cargill Incorporated

Wilmar International

Archer Daniels Midland Company

Indigo Ag

Pivot Bio

Benson Hill

Trimble Inc.

Technological innovation in the Low-Carbon Oilseed Crop Solutions Market is centered on emission quantification, input efficiency, and digital traceability. Precision nutrient management systems using AI-driven variable rate technology are deployed across nearly 58% of large-scale oilseed farms in developed markets, reducing nitrogen runoff by 25–30%. Enhanced-efficiency fertilizers incorporate nitrification inhibitors that cut nitrous oxide emissions by up to 30% compared to conventional blends.

Satellite-enabled Monitoring, Reporting, and Verification (MRV) platforms now cover over 20 million hectares globally, offering sub-meter resolution soil carbon analytics. Blockchain-based traceability systems reduce certification processing times by 35%, supporting premium pricing for verified low-carbon feedstock. Biological nitrogen fixation technologies lower synthetic fertilizer dependence by approximately 20%, enhancing soil microbial activity and long-term carbon sequestration potential.

Emerging digital twin farm modeling simulates yield and emission scenarios with up to 85% predictive accuracy, enabling proactive agronomic decisions. IoT-enabled soil sensors deployed across high-value farms deliver real-time nutrient and moisture data with 15-minute update intervals, improving irrigation efficiency by 18%. These integrated technologies collectively enhance compliance readiness, supply chain transparency, and performance benchmarking for sustainability-driven procurement contracts.

• In January 2026, bp and Corteva Agriscience officially launched Etlas™, a 50:50 strategic joint venture to produce sustainable, crop-based feedstocks* — including canola, mustard, and sunflower — for renewable diesel and sustainable aviation fuel (SAF). The venture aims to produce ~1 million metric tonnes of feedstock annually by the mid-2030s, expanding low-carbon crop supply across North America and Europe with initial production anticipated as early as 2027. Sources: www.biofuels-news.com

• In November 2024, Corteva shared its intent to partner with bp to form a joint venture that will deliver crop-based biofuel feedstocks, targeting one million metric tons per year for SAF, by contracting growers in North America, South America, and Europe to grow proprietary low-carbon feedstock crops such as mustard seed, sunflower, and canola.

• In February 2026, Bayer unveiled newgold®, its first multi-crop seed brand focused on low-carbon intensity oilseed crops such as camelina and winter canola, targeting participation in the fast-growing biofuels economy and supporting farmers with enhanced market access and agronomic performance in low-carbon rotations.

• In January 2026, Bayer and ADM announced they will quadruple their reach to 100,000 soybean farmers in Maharashtra, scaling cultivation from 35,000 to 200,000 hectares and embedding sustainability practices into oilseed systems, strengthening low-carbon agriculture linkages.

The Low-Carbon Oilseed Crop Solutions Market Report provides comprehensive coverage across product types, applications, end-users, technologies, and geographic regions. The scope includes enhanced-efficiency fertilizers, biological seed treatments, precision nutrient management systems, digital carbon monitoring platforms, and integrated MRV solutions deployed across more than 100 million hectares of global oilseed farmland. Application analysis spans biodiesel and renewable diesel feedstock optimization, food-grade edible oil production, animal feed sustainability, and industrial bio-based materials.

Geographically, the report evaluates five major regions—North America, Europe, Asia-Pacific, South America, and Middle East & Africa—capturing market share distribution, acreage coverage, technology penetration rates, and regulatory influence metrics. End-user assessment covers commercial farms, agribusiness processors, renewable fuel producers, and food manufacturers, with adoption rates exceeding 50% among large-scale producers in developed markets.

The study further analyzes technology integration trends such as AI-driven soil analytics, satellite-based carbon mapping across 20+ million hectares, blockchain traceability systems covering nearly 40% of export-oriented supply chains, and biological nitrogen fixation solutions reducing fertilizer dependency by 20%. Emerging niches include sustainable aviation fuel-linked oilseed pathways and carbon credit monetization platforms. The report is structured to provide decision-makers with actionable insights into operational optimization, compliance readiness, investment prioritization, and long-term sustainability alignment within the evolving Low-Carbon Oilseed Crop Solutions Market.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 3,270.0 Million |

| Market Revenue (2033) | USD 4,758.1 Million |

| CAGR (2026–2033) | 4.8% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Bayer AG; Corteva Agriscience; Syngenta Group; BASF SE; Nutrien Ltd.; Yara International; Bunge Global SA; Cargill Incorporated; Wilmar International; Archer Daniels Midland Company; Indigo Ag; Pivot Bio; Benson Hill; Trimble Inc. |

| Customization & Pricing | Available on Request (10% Customization Free) |