Reports

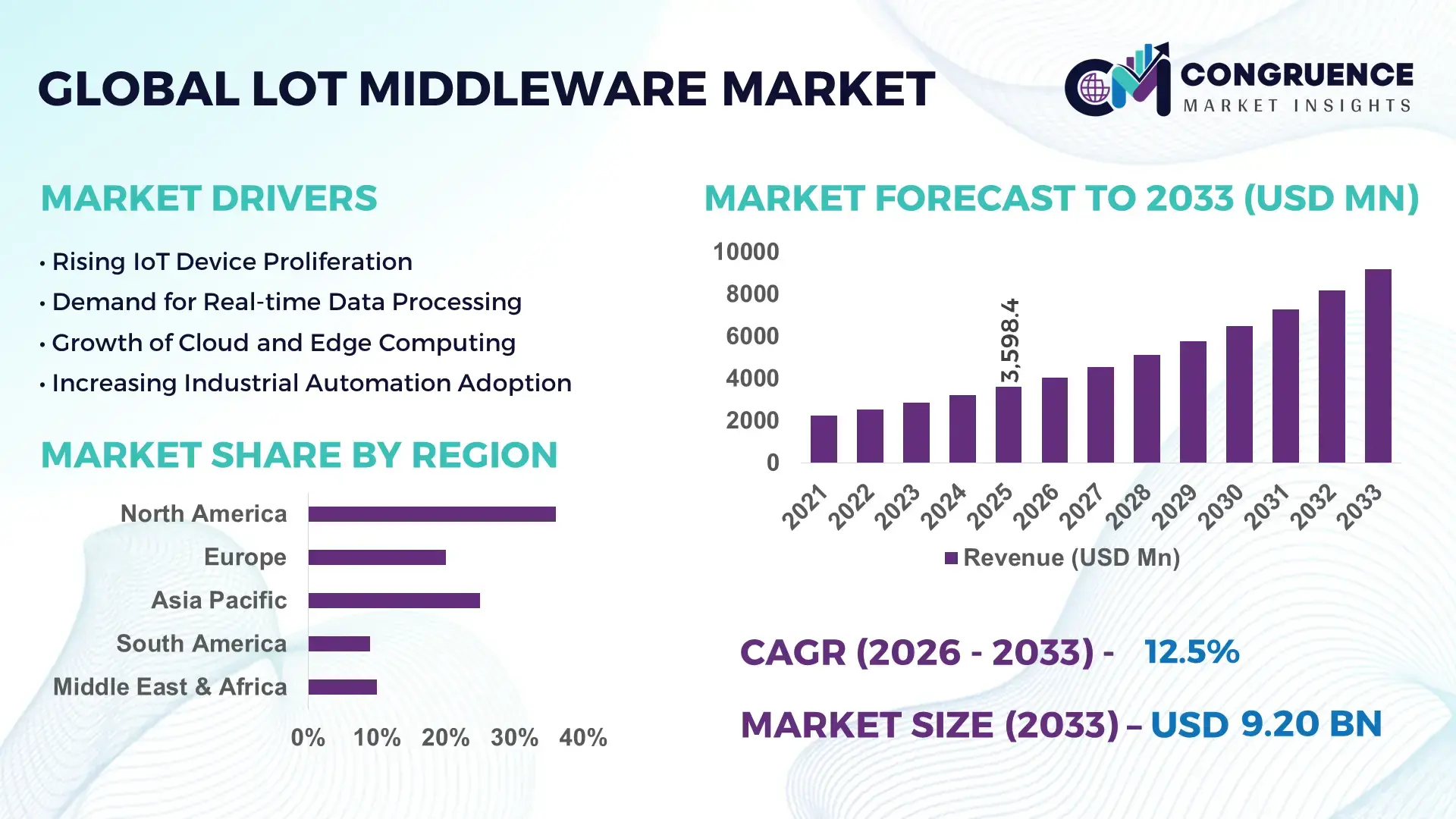

The Global IoT Middleware Market was valued at USD 3598.4 Million in 2025 and is anticipated to reach a value of USD 9199.94 Million by 2033 expanding at a CAGR of 12.45% between 2026 and 2033. This growth is primarily driven by the rapid proliferation of connected devices and enterprise demand for seamless data integration across complex digital ecosystems.

The United States continues to demonstrate strong industrial-scale deployment of IoT middleware platforms across manufacturing, healthcare, and smart infrastructure sectors. Over 68% of large enterprises in the country have implemented IoT middleware solutions to manage device interoperability and real-time analytics. Annual investments in industrial IoT integration exceeded USD 25 billion, with middleware platforms supporting over 15 billion connected endpoints across various industries. Advanced cloud-native middleware architectures and edge computing integration are enabling low-latency data processing, while smart city projects across more than 100 metropolitan regions rely heavily on middleware for traffic, energy, and public safety systems.

Market Size & Growth: Valued at USD 3598.4 Million in 2025, projected to reach USD 9199.94 Million by 2033, growing at 12.45% CAGR driven by large-scale IoT deployments and enterprise digital transformation.

Top Growth Drivers: Connected device adoption (72%), operational efficiency improvements (45%), real-time analytics demand (38%).

Short-Term Forecast: By 2028, IoT middleware adoption is expected to improve system efficiency by 30% and reduce operational costs by 25%.

Emerging Technologies: Edge computing integration, AI-driven middleware orchestration, and containerized microservices architectures.

Regional Leaders: North America projected at USD 3200 Million by 2033 with enterprise IoT expansion; Asia-Pacific at USD 2900 Million driven by smart manufacturing; Europe at USD 2100 Million focusing on regulatory-compliant deployments.

Consumer/End-User Trends: Industrial manufacturing and healthcare sectors account for over 55% of deployments, with increasing adoption in logistics and smart cities.

Pilot or Case Example: In 2024, a smart manufacturing initiative achieved 28% downtime reduction using AI-enabled IoT middleware integration.

Competitive Landscape: Leading player holds approximately 18% share, followed by major competitors including global cloud and enterprise software providers.

Regulatory & ESG Impact: Data privacy regulations and carbon reduction targets are accelerating adoption of efficient middleware systems with up to 20% energy optimization.

Investment & Funding Patterns: Over USD 12 billion invested in IoT middleware innovation and platform development in recent years.

Innovation & Future Outlook: Increasing convergence of AI, edge, and hybrid cloud platforms is shaping scalable and autonomous middleware ecosystems.

The IoT middleware market is expanding across key sectors such as manufacturing, healthcare, transportation, and energy, collectively contributing more than 70% of total deployments. Recent advancements include AI-enabled data orchestration, low-code middleware platforms, and edge-native architectures that enhance scalability and latency management. Regulatory frameworks focused on data security and interoperability standards are accelerating enterprise adoption, particularly in Europe and Asia-Pacific. Consumption patterns show strong growth in smart factories and connected healthcare systems, while emerging trends such as digital twins, predictive maintenance, and autonomous system integration are shaping the future outlook of IoT middleware solutions.

The IoT middleware market plays a critical strategic role in enabling seamless communication between heterogeneous devices, applications, and enterprise systems, forming the backbone of scalable digital ecosystems. Enterprises leveraging AI-enabled middleware platforms are witnessing up to 35% faster data processing speeds compared to traditional integration frameworks. Edge-enabled middleware delivers 40% latency reduction compared to centralized cloud-only architectures, significantly improving real-time decision-making capabilities.

North America dominates in volume due to extensive enterprise infrastructure, while Asia-Pacific leads in adoption with over 60% of manufacturing enterprises deploying IoT middleware to support Industry 4.0 initiatives. By 2028, AI-driven middleware automation is expected to improve operational efficiency by 30% through predictive analytics and intelligent workflow orchestration. Firms are committing to ESG targets, including 25% reduction in energy consumption by 2030 through optimized middleware-enabled device management and energy monitoring systems.

In 2024, a large-scale industrial deployment in Germany achieved a 32% improvement in production efficiency through integration of AI-powered middleware and edge analytics. Strategic pathways for the market include expansion of hybrid cloud middleware solutions, increased adoption of API-driven architectures, and integration of cybersecurity layers within middleware frameworks. As organizations prioritize resilience and regulatory compliance, the IoT middleware market is positioned as a foundational pillar supporting secure, scalable, and sustainable digital transformation across industries.

The IoT middleware market is characterized by rapid technological evolution, increasing enterprise adoption, and rising complexity in connected ecosystems. Middleware platforms are essential for managing interoperability across billions of IoT devices, ensuring seamless data flow between sensors, applications, and cloud infrastructures. Market dynamics are influenced by the expansion of industrial IoT, the growth of smart cities, and the integration of artificial intelligence and edge computing technologies. Increasing regulatory requirements for data security and privacy are also shaping the development of secure middleware frameworks. Additionally, demand for real-time analytics and automation is driving innovation in scalable, cloud-native middleware architectures that can support high-volume data processing and low-latency communication.

The exponential growth of connected devices, expected to exceed 29 billion globally by 2030, is a primary driver of IoT middleware demand. Enterprises require robust middleware platforms to manage device interoperability, data integration, and real-time analytics across diverse systems. Industrial sectors such as manufacturing and energy are deploying large-scale IoT networks, with some facilities operating over 100,000 connected sensors. Middleware solutions enable centralized control, improving operational efficiency by up to 35% and reducing system downtime by 25%. The rise of smart infrastructure and digital transformation initiatives further amplifies the need for scalable middleware capable of handling complex data environments and ensuring seamless communication between devices and applications.

Despite strong growth, the IoT middleware market faces significant challenges related to data security, privacy, and interoperability. Over 60% of enterprises report concerns about vulnerabilities in IoT ecosystems, particularly in industries handling sensitive data such as healthcare and finance. Fragmented device standards and lack of universal protocols create integration complexities, increasing deployment time and costs. Additionally, compliance with stringent data protection regulations requires continuous updates to middleware systems, raising operational overhead. Cybersecurity threats, including unauthorized access and data breaches, further hinder adoption, especially among small and medium enterprises that lack advanced security infrastructure.

The integration of artificial intelligence and edge computing presents significant growth opportunities for the IoT middleware market. AI-driven middleware platforms enable predictive analytics, anomaly detection, and automated decision-making, improving system efficiency by up to 40%. Edge computing reduces latency by processing data closer to the source, making it ideal for applications such as autonomous vehicles and industrial automation. Emerging use cases in smart healthcare, connected logistics, and digital twins are expanding the scope of middleware applications. Additionally, the development of low-code and no-code middleware platforms is enabling faster deployment and accessibility, particularly for enterprises with limited technical resources.

Scalability and infrastructure costs remain critical challenges in the IoT middleware market, particularly for large-scale deployments. Managing millions of connected devices requires significant investment in cloud infrastructure, edge nodes, and data processing capabilities. Enterprises often face difficulties in scaling middleware platforms without compromising performance or security. Integration with legacy systems adds further complexity, increasing implementation time and costs. Additionally, maintaining high availability and reliability in distributed environments demands advanced monitoring and management tools, which can strain IT budgets. These challenges necessitate continuous innovation in cost-efficient and scalable middleware architectures to support the growing demands of IoT ecosystems.

• Rapid Adoption of Edge-Integrated Middleware Platforms (45% Enterprise Uptake): Edge-integrated IoT middleware solutions are witnessing significant adoption, with nearly 45% of enterprises deploying edge-enabled middleware to reduce latency and improve real-time processing. Industrial environments report up to 38% faster response times due to localized data handling. Over 60% of smart manufacturing units now rely on edge middleware to process sensor data on-site, minimizing cloud dependency and improving operational continuity. This trend is particularly strong in sectors requiring sub-second decision-making, such as autonomous systems and energy grid management.

• Expansion of AI-Driven Middleware Automation (40% Efficiency Gains): AI-powered middleware platforms are transforming operational efficiency, with enterprises achieving up to 40% improvement in predictive analytics accuracy and automation workflows. Around 52% of large-scale IoT deployments now incorporate AI-enabled middleware for anomaly detection and system optimization. These intelligent platforms can reduce manual intervention by 30% while improving system uptime by 28%. The integration of machine learning algorithms within middleware layers is accelerating adaptive system behavior across industries such as healthcare and logistics.

• Surge in Cloud-Native and Microservices Architecture (58% Deployment Shift): Cloud-native IoT middleware adoption has increased significantly, with 58% of new deployments utilizing containerized microservices architectures. This shift allows enterprises to scale operations dynamically, with system scalability improving by nearly 35% compared to traditional monolithic middleware systems. Organizations leveraging Kubernetes-based orchestration report 25% faster deployment cycles and enhanced system resilience. Hybrid cloud middleware adoption is also rising, enabling seamless integration between on-premise infrastructure and public cloud environments.

• Rising Demand for Secure and Compliant Middleware Solutions (62% Security Investment Growth): Security-focused middleware solutions are gaining traction, with enterprises increasing cybersecurity investments by 62% to address IoT vulnerabilities. Approximately 70% of organizations now prioritize middleware platforms with built-in encryption, identity management, and compliance features. Regulatory-driven adoption is particularly strong in Europe and North America, where over 65% of deployments adhere to strict data protection frameworks. Advanced middleware security protocols have reduced data breach incidents by 22%, strengthening enterprise trust in IoT ecosystems.

The IoT middleware market segmentation reflects a diversified ecosystem shaped by deployment models, application requirements, and end-user industries. By type, the market is categorized into platform-based middleware, device management middleware, application infrastructure middleware, and connectivity middleware, each serving distinct integration and data orchestration needs. Application-wise, industrial automation, healthcare systems, smart cities, and logistics dominate due to their reliance on real-time data exchange and system interoperability. End-user segmentation highlights manufacturing, healthcare, transportation, and energy sectors as primary adopters, collectively contributing over 70% of total deployments. Increasing digital transformation initiatives and the need for scalable, secure integration frameworks are driving deeper penetration across these segments, with notable growth in edge-based and AI-enabled middleware solutions.

Platform-based IoT middleware currently leads the market, accounting for approximately 38% of total adoption due to its ability to provide comprehensive integration, analytics, and device management capabilities within a unified environment. Device management middleware follows with around 27% share, focusing on monitoring and controlling large-scale connected device networks. However, connectivity middleware is emerging as the fastest-growing segment, expanding at an estimated CAGR of 14.2%, driven by increasing demand for seamless communication across heterogeneous networks and protocols.

Application infrastructure middleware contributes nearly 20% of the market, supporting data processing and workflow automation, while the remaining segments collectively account for approximately 15%, catering to niche use cases such as legacy system integration and protocol translation. The growth of connectivity middleware is fueled by the rapid expansion of 5G networks and the increasing number of IoT endpoints requiring reliable, low-latency communication.

Industrial automation remains the leading application segment, accounting for approximately 42% of IoT middleware usage due to extensive deployment in smart manufacturing and predictive maintenance systems. Healthcare applications hold around 24% share, leveraging middleware for patient monitoring and connected medical devices. Meanwhile, smart city applications are the fastest-growing segment, expanding at an estimated CAGR of 15.1%, driven by urban digitalization and infrastructure modernization initiatives.

Logistics and transportation contribute about 18% of the market, focusing on fleet management and real-time tracking, while other applications such as agriculture and retail collectively account for nearly 16%. The increasing adoption of digital twins and AI-driven analytics is further enhancing middleware utilization across these sectors.

The manufacturing sector dominates the IoT middleware market, accounting for approximately 40% of total adoption due to its reliance on connected machinery, automation systems, and predictive maintenance solutions. The healthcare sector follows with a 22% share, driven by increasing deployment of connected medical devices and remote patient monitoring systems. However, the transportation and logistics sector is the fastest-growing end-user segment, expanding at an estimated CAGR of 13.8%, supported by rising demand for real-time tracking and supply chain optimization.

Energy and utilities contribute around 18% of the market, utilizing middleware for smart grid management and energy monitoring, while other sectors such as retail and agriculture collectively account for approximately 20%, benefiting from improved data integration and operational visibility. Adoption rates in smart logistics have increased by over 35% in recent years, reflecting the growing importance of real-time data insights.

Region North America accounted for the largest market share at 36% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 14.1% between 2026 and 2033.

North America’s dominance is supported by over 70% enterprise-level IoT adoption across sectors such as healthcare, manufacturing, and financial services, with more than 12 billion connected devices actively managed through middleware platforms. Europe holds approximately 27% share, driven by regulatory-compliant deployments and over 65% of enterprises prioritizing secure middleware frameworks. Asia-Pacific accounts for nearly 24% of the market, with more than 50% of manufacturing enterprises deploying IoT middleware solutions to support automation and digital transformation. South America and the Middle East & Africa collectively contribute around 13%, with increasing investments in smart infrastructure and industrial IoT, particularly in energy and logistics sectors. Regional consumption patterns indicate that over 60% of middleware deployments are concentrated in urban and industrial hubs, reflecting strong demand for real-time data integration and scalable connectivity solutions.

How are advanced enterprise integrations reshaping middleware adoption patterns?

North America holds approximately 36% of the IoT middleware market, driven by strong adoption across healthcare, manufacturing, and financial services sectors. Over 72% of large enterprises in the region utilize IoT middleware for real-time data integration and system interoperability. Government initiatives supporting digital infrastructure, including smart city programs in over 80 metropolitan areas, are accelerating deployment. Regulatory frameworks emphasizing data security and privacy compliance have increased middleware adoption with built-in encryption and identity management features. Technological advancements such as AI-driven middleware and edge computing integration are improving system efficiency by up to 35%. A notable example includes a leading cloud provider deploying middleware platforms across industrial clients, enabling 30% faster data processing and 25% reduction in downtime. Consumer behavior reflects high enterprise-driven demand, particularly in healthcare and finance, where over 65% of organizations rely on middleware for secure data exchange and operational continuity.

What factors are driving secure and compliant middleware integration strategies?

Europe accounts for approximately 27% of the IoT middleware market, with key countries such as Germany, the United Kingdom, and France leading adoption. Over 68% of enterprises in the region prioritize middleware solutions that comply with stringent data protection regulations, including GDPR-driven frameworks. Sustainability initiatives and green IT policies are encouraging energy-efficient middleware deployments, with enterprises achieving up to 22% reduction in energy consumption through optimized data management. The region is witnessing strong adoption of AI-enabled and cloud-native middleware platforms, particularly in industrial automation and smart mobility sectors. A prominent European technology provider recently implemented middleware solutions across smart transportation networks, improving traffic management efficiency by 28%. Consumer behavior in the region is influenced by regulatory pressure, with over 60% of organizations demanding transparent, explainable middleware systems that ensure data accountability and compliance.

How is large-scale industrial digitalization accelerating middleware demand?

Asia-Pacific ranks among the fastest-growing regions in the IoT middleware market, contributing nearly 24% of global demand. Countries such as China, India, and Japan are leading adoption, with China alone managing over 5 billion connected IoT devices across industrial and urban applications. Manufacturing-driven economies in the region have achieved over 55% middleware deployment in smart factories, supporting automation and predictive maintenance. Infrastructure expansion, including smart cities and 5G networks, is accelerating middleware integration, with more than 120 smart city projects actively utilizing IoT platforms. A regional technology firm recently deployed middleware solutions across logistics networks, improving supply chain visibility by 32%. Consumer behavior reflects strong growth driven by e-commerce, mobile applications, and industrial automation, with over 58% of enterprises investing in scalable middleware solutions to enhance operational efficiency.

What role do infrastructure modernization and energy projects play in adoption?

South America accounts for approximately 7% of the IoT middleware market, with Brazil and Argentina emerging as key contributors. Over 48% of IoT deployments in the region are concentrated in energy, utilities, and transportation sectors. Infrastructure modernization initiatives, including smart grid projects and urban mobility systems, are driving middleware adoption, enabling real-time monitoring and control. Government incentives supporting digital transformation and foreign investment are increasing adoption rates, with middleware usage growing across industrial and public sectors. A regional energy provider implemented IoT middleware across power distribution networks, improving energy efficiency by 26% and reducing outages significantly. Consumer behavior indicates growing demand for localized solutions, with adoption closely tied to media, language, and regional customization requirements.

How are smart infrastructure and energy diversification shaping adoption trends?

The Middle East & Africa region contributes approximately 6% of the IoT middleware market, with key growth countries including the United Arab Emirates and South Africa. Demand is primarily driven by oil and gas, construction, and smart city projects, with over 40% of deployments focused on infrastructure modernization. Governments are investing heavily in digital transformation, with smart city initiatives in more than 20 major urban centers utilizing IoT middleware platforms. Technological advancements such as AI-enabled analytics and edge computing are improving operational efficiency by up to 30% in industrial applications. A local technology provider deployed middleware solutions in a large-scale construction project, achieving a 24% improvement in project monitoring and resource allocation. Consumer behavior reflects increasing adoption of connected technologies, with enterprises focusing on scalable and secure middleware solutions to support economic diversification and digital innovation.

United States – 32% share: IoT Middleware market leadership driven by high enterprise adoption, advanced cloud infrastructure, and large-scale industrial IoT deployments.

China – 21% share: IoT Middleware market growth supported by massive connected device ecosystem, smart manufacturing expansion, and government-backed digital infrastructure initiatives.

The IoT middleware market is moderately fragmented, with over 50 active global and regional players competing across platform development, integration services, and specialized middleware solutions. The top five companies collectively account for approximately 48% of the total market share, reflecting a competitive yet innovation-driven environment. Market leaders are focusing on strategic partnerships, mergers, and acquisitions to strengthen their technological capabilities and expand global reach.

More than 35% of companies have invested in AI-driven middleware enhancements, enabling predictive analytics and automated system management. Product innovation remains a key competitive factor, with over 40 new middleware solutions launched in the past two years, focusing on edge computing, cloud-native architectures, and cybersecurity integration. Strategic collaborations between cloud providers and industrial enterprises have increased by 28%, accelerating the deployment of scalable middleware platforms.

Additionally, regional players are gaining traction by offering customized solutions tailored to local regulatory requirements and industry-specific needs. Competitive differentiation is increasingly based on interoperability, scalability, and security features, with companies prioritizing low-latency processing and real-time data integration. The evolving competitive landscape highlights the importance of continuous innovation and strategic alignment to maintain market positioning.

IBM

Microsoft

Oracle

SAP

Amazon Web Services

Cisco Systems

PTC

Software AG

Hitachi Vantara

Bosch.IO

Siemens

Huawei Technologies

Fujitsu

TIBCO Software

Red Hat

The IoT middleware market is undergoing rapid technological transformation driven by advancements in edge computing, artificial intelligence, and cloud-native architectures. Edge-enabled middleware platforms are now deployed in over 45% of industrial IoT environments, enabling data processing closer to the source and reducing latency by up to 40%. This is particularly critical for time-sensitive applications such as autonomous systems, smart grids, and real-time healthcare monitoring. The integration of 5G connectivity is further enhancing middleware capabilities, supporting data transfer speeds exceeding 1 Gbps and enabling seamless communication across millions of connected devices.

Artificial intelligence and machine learning are increasingly embedded within middleware platforms, with over 50% of enterprise deployments utilizing AI-driven analytics for predictive maintenance, anomaly detection, and automated decision-making. These technologies have improved system uptime by approximately 30% and reduced operational inefficiencies by nearly 25%. Additionally, containerization and microservices-based architectures are transforming middleware scalability, with 58% of new deployments leveraging Kubernetes orchestration to enable flexible and modular system integration.

Security technologies are also evolving, with more than 70% of middleware solutions now incorporating advanced encryption protocols, identity access management, and real-time threat detection. Blockchain-based middleware frameworks are emerging as a solution for secure data exchange, particularly in supply chain and financial applications, ensuring data integrity and traceability across distributed networks. Furthermore, low-code and no-code middleware platforms are gaining traction, reducing deployment time by up to 35% and enabling broader adoption among enterprises with limited technical expertise. These technological advancements collectively position IoT middleware as a critical enabler of scalable, secure, and intelligent digital ecosystems.

• In March 2025, Microsoft expanded its Azure IoT Operations platform with enhanced edge data processing and unified orchestration capabilities, enabling enterprises to manage over 1 million devices per deployment while improving real-time analytics efficiency by approximately 30%. Source: www.microsoft.com

• In October 2024, IBM introduced new AI-powered capabilities within its Watson IoT Platform, enabling predictive maintenance models that reduced equipment downtime by up to 25% across industrial deployments. The update also improved anomaly detection accuracy by over 20%. Source: www.ibm.com

• In May 2025, Amazon Web Services launched an advanced update to AWS IoT Core, integrating generative AI-based analytics tools that allow enterprises to process and interpret IoT data streams 35% faster, enhancing operational decision-making in logistics and manufacturing environments.

• In September 2024, Siemens enhanced its Industrial IoT middleware portfolio by integrating edge computing and digital twin capabilities into its MindSphere platform, enabling manufacturers to improve production efficiency by 28% and reduce energy consumption across connected facilities. Source: www.siemens.com

The IoT middleware market report provides a comprehensive analysis of the global ecosystem, covering over 10 major technology segments and multiple industry verticals. The scope includes detailed evaluation of middleware types such as platform-based middleware, connectivity middleware, device management solutions, and application infrastructure layers, which collectively support billions of connected devices worldwide. The report examines more than 25 application areas, including industrial automation, healthcare systems, smart cities, transportation, logistics, and energy management, reflecting the diverse adoption of middleware solutions across sectors.

Geographically, the report spans five key regions and analyzes over 20 major countries, capturing regional deployment patterns, enterprise adoption rates, and infrastructure development trends. It highlights that over 60% of IoT middleware implementations are concentrated in industrial and urban environments, with significant growth observed in smart manufacturing and connected healthcare ecosystems. The report also evaluates emerging technologies such as edge computing, AI-driven analytics, blockchain integration, and 5G-enabled middleware, which are collectively transforming system performance, scalability, and security.

In addition, the scope includes analysis of regulatory frameworks, data security standards, and interoperability requirements influencing middleware adoption. The report covers more than 50 key market participants, assessing their technological capabilities, product portfolios, and strategic initiatives. It also identifies niche segments such as low-code middleware platforms and digital twin integration, which are gaining traction among enterprises seeking rapid deployment and enhanced operational visibility. Overall, the report provides a structured and data-driven overview tailored to support strategic decision-making and investment planning in the IoT middleware market.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

12.45% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

IBM, Microsoft, Oracle, SAP, Amazon Web Services, Cisco Systems, PTC, Software AG, Hitachi Vantara, Bosch.IO, Siemens, Huawei Technologies, Fujitsu, TIBCO Software, Red Hat |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |