Reports

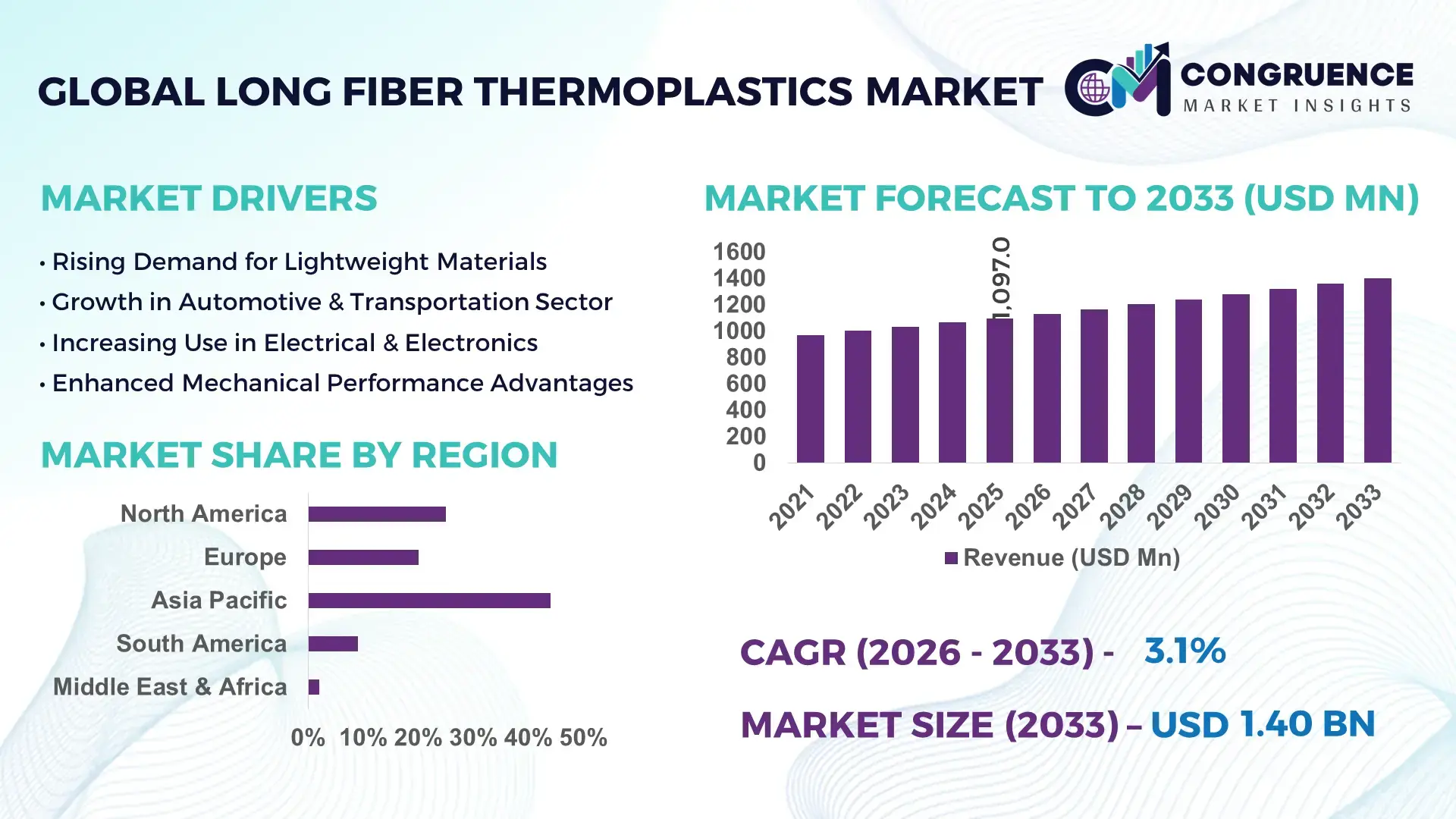

The Global Long Fiber Thermoplastics Market was valued at USD 1096.97 Million in 2025 and is anticipated to reach a value of USD 1400.44 Million by 2033 expanding at a CAGR of 3.1% between 2026 and 2033. Growth is primarily driven by rising demand for lightweight, high-strength composite materials in automotive and industrial applications.

China continues to lead the Long Fiber Thermoplastics market with substantial production capacity exceeding 450,000 metric tons annually, supported by over 120 active manufacturing facilities specializing in reinforced thermoplastics. The country has witnessed investments surpassing USD 1.8 billion in advanced composite manufacturing infrastructure since 2022, particularly in automotive lightweighting programs. Long fiber thermoplastics are increasingly used in electric vehicle components, contributing to over 35% adoption in structural parts across domestic EV production. Additionally, industrial automation and construction sectors account for nearly 28% of consumption, while technological advancements in pultrusion and injection molding processes have improved material efficiency by approximately 18%.

Market Size & Growth: Valued at USD 1096.97 Million in 2025, projected to reach USD 1400.44 Million by 2033 at a CAGR of 3.1%, driven by increasing demand for lightweight and durable composite materials in transportation and construction sectors.

Top Growth Drivers: Automotive lightweighting adoption increased by 42%, industrial material efficiency improved by 28%, and sustainability-driven material substitution rose by 35%.

Short-Term Forecast: By 2028, advanced processing technologies are expected to reduce material waste by 22% and improve component strength by 18%.

Emerging Technologies: Innovations include automated pultrusion systems, hybrid fiber reinforcement technology, and AI-driven material design optimization.

Regional Leaders: Asia-Pacific projected to reach USD 620 Million by 2033 with strong manufacturing demand, Europe to hit USD 410 Million driven by sustainability regulations, North America to reach USD 300 Million with advanced automotive adoption trends.

Consumer/End-User Trends: Automotive accounts for over 45% of usage, followed by construction and industrial machinery with growing preference for corrosion-resistant materials.

Pilot or Case Example: In 2024, a European automotive OEM achieved 20% weight reduction and 15% fuel efficiency improvement using long fiber thermoplastics in structural components.

Competitive Landscape: Market leader holds approximately 24% share, followed by key players including BASF, SABIC, Celanese, Solvay, and RTP Company.

Regulatory & ESG Impact: Increasing regulations on carbon emissions are driving 30% higher adoption of recyclable thermoplastics and eco-friendly composites.

Investment & Funding Patterns: Over USD 2.5 billion invested globally in composite material innovation and production expansion between 2022 and 2025.

Innovation & Future Outlook: Integration of digital manufacturing and recyclable composite technologies is shaping next-generation product development and long-term sustainability strategies.

The Long Fiber Thermoplastics market is witnessing diversified growth across automotive, aerospace, and construction sectors, with automotive contributing nearly 45% of total demand, followed by industrial applications at 30% and construction at 20%. Recent innovations such as glass fiber and carbon fiber hybrid composites have enhanced tensile strength by up to 25%, enabling broader structural applications. Regulatory pressures around carbon emissions and recyclability are accelerating adoption, particularly in Europe where over 60% of manufacturers are integrating sustainable materials. Asia-Pacific shows strong consumption growth due to infrastructure expansion, while North America focuses on high-performance applications. Future trends include bio-based thermoplastics and advanced recycling technologies, positioning the market for steady, innovation-led expansion.

The Long Fiber Thermoplastics market holds significant strategic relevance as industries prioritize lightweight, high-performance materials to meet efficiency and sustainability goals. The shift toward electric vehicles and energy-efficient infrastructure has increased demand for advanced composite materials capable of reducing overall system weight by up to 30% while maintaining structural integrity. Long fiber thermoplastics offer superior impact resistance and durability, making them critical in next-generation manufacturing strategies.

Advanced automated pultrusion technology delivers 25% improvement in production efficiency compared to conventional short fiber processing methods, enabling faster throughput and reduced material waste. Asia-Pacific dominates in production volume due to large-scale manufacturing capabilities, while Europe leads in adoption with over 55% of enterprises integrating sustainable composite materials into production processes. This regional differentiation reflects both cost advantages and regulatory-driven innovation. By 2028, AI-driven material engineering is expected to improve product design accuracy by 20% while reducing prototyping costs by 18%, enabling manufacturers to optimize performance and reduce time-to-market. ESG commitments are reshaping the industry, with firms targeting up to 35% reduction in carbon footprint and achieving over 40% recyclability in thermoplastic components by 2030.

In 2024, a leading automotive manufacturer in Germany achieved a 22% reduction in component weight and a 17% increase in fuel efficiency through the integration of advanced long fiber thermoplastic structures. Such measurable outcomes highlight the material’s role in enhancing operational performance. The Long Fiber Thermoplastics market is positioned as a critical enabler of industrial resilience, regulatory compliance, and sustainable growth, with continuous innovation reinforcing its importance across global manufacturing ecosystems.

The automotive industry’s focus on weight reduction to improve fuel efficiency and electric vehicle range is a major driver of the Long Fiber Thermoplastics market. Long fiber thermoplastics can reduce component weight by up to 30% compared to traditional metals, while maintaining high mechanical strength. With electric vehicle production increasing by over 40% globally, manufacturers are incorporating these materials into structural components such as front-end modules and battery enclosures. Additionally, regulatory standards targeting emission reduction have pushed automakers to adopt advanced composites. The use of long fiber thermoplastics in automotive applications has grown by approximately 35% in the past five years, supported by advancements in molding technologies that enhance production scalability and cost efficiency.

Despite strong demand, high production costs remain a significant restraint for the Long Fiber Thermoplastics market. The manufacturing process requires specialized equipment such as pultrusion lines and advanced injection molding systems, which increase capital expenditure by up to 25% compared to conventional plastic processing. Additionally, raw materials like carbon fiber and glass fiber contribute to higher input costs, limiting adoption among small and medium enterprises. Complex processing requirements also result in longer production cycles, reducing operational efficiency. These cost-related challenges have restricted widespread penetration in price-sensitive markets, particularly in developing regions where traditional materials remain more economically viable for large-scale applications.

Sustainability initiatives are creating significant opportunities in the Long Fiber Thermoplastics market, particularly through the development of recyclable and bio-based materials. Advances in recycling technologies now allow recovery of up to 70% of fiber content from used composites, enabling circular economy practices. Governments and regulatory bodies are promoting the use of eco-friendly materials, leading to increased adoption in industries such as construction and packaging. The demand for sustainable composites has risen by over 30% in recent years, driven by environmental regulations and corporate ESG commitments. Additionally, innovations in bio-based thermoplastics are opening new avenues for reducing carbon emissions while maintaining performance standards, positioning the market for long-term growth.

Processing complexities and maintaining consistent performance present key challenges in the Long Fiber Thermoplastics market. The uniform distribution of long fibers within the polymer matrix is difficult to achieve, leading to variability in mechanical properties across finished products. Production defects can increase rejection rates by up to 15%, impacting overall efficiency. Furthermore, the need for precise temperature and pressure control during molding processes adds operational complexity. Skilled labor shortages in advanced composite manufacturing further exacerbate these challenges. Ensuring consistent quality while scaling production remains a critical hurdle, particularly as demand increases across high-performance applications such as automotive and aerospace industries.

• 45% Surge in Automotive Lightweighting Integration: The automotive sector continues to accelerate the adoption of long fiber thermoplastics, with over 45% of newly designed structural components in electric vehicles now incorporating these materials. Weight reduction of up to 30% has enabled manufacturers to improve vehicle efficiency by nearly 20%, while maintaining crash performance standards. Increased electrification has driven demand for battery enclosures and underbody systems, with usage in these components growing by 38% over the past three years. Advanced injection molding technologies have further reduced cycle times by 25%, enabling higher production scalability.

• 32% Growth in Sustainable and Recyclable Material Adoption: Sustainability-driven innovation is reshaping material selection, with approximately 32% of manufacturers shifting toward recyclable long fiber thermoplastics. New recycling processes now recover up to 70% of fiber content, significantly reducing material waste. Regulatory compliance requirements have increased the adoption of eco-friendly composites by 28%, particularly in Europe where over 60% of industrial producers are integrating circular material strategies. Bio-based thermoplastics are also gaining traction, with pilot production volumes increasing by 22% since 2023.

• 40% Expansion in Industrial Automation Applications: Industrial machinery and automation sectors are witnessing a 40% increase in the use of long fiber thermoplastics for high-strength, corrosion-resistant components. These materials have improved equipment lifespan by 18% and reduced maintenance costs by nearly 15%. Adoption in robotic arms and conveyor systems has grown by 27%, driven by the need for lightweight yet durable materials. Manufacturers are also leveraging hybrid fiber composites to enhance load-bearing capacity by 20%, enabling broader use in heavy-duty applications.

• 55% Rise in Modular and Prefabricated Construction Adoption: The adoption of modular construction is significantly influencing the Long Fiber Thermoplastics market, with nearly 55% of new construction projects reporting cost benefits through prefabrication. Pre-engineered thermoplastic components are increasingly used in structural panels and reinforcement systems, reducing on-site labor requirements by 30% and project timelines by 25%. Demand for precision-engineered materials has grown by 35% in North America and Europe, where efficiency and sustainability standards are driving construction innovation.

The Long Fiber Thermoplastics market segmentation reflects a well-defined structure across types, applications, and end-user industries, each contributing uniquely to overall demand. Product types such as glass fiber reinforced and carbon fiber reinforced thermoplastics dominate due to their mechanical strength and lightweight properties. Application-wise, automotive leads due to extensive use in structural and semi-structural components, followed by industrial machinery and construction sectors. End-user segmentation highlights automotive manufacturers, aerospace firms, and industrial equipment producers as primary consumers. Approximately 45% of total demand originates from transportation-related applications, while industrial and construction sectors collectively account for over 50%. The segmentation also reveals a shift toward sustainable and high-performance materials, with increasing adoption of recyclable composites and advanced processing technologies shaping future market dynamics.

The Long Fiber Thermoplastics market is categorized into glass fiber reinforced thermoplastics (GFRT), carbon fiber reinforced thermoplastics (CFRT), and other specialty fiber composites. Glass fiber reinforced thermoplastics currently dominate the segment, accounting for approximately 58% of total adoption due to their cost-effectiveness, high strength-to-weight ratio, and versatility across automotive and industrial applications. In comparison, carbon fiber reinforced thermoplastics hold around 27% share, offering superior stiffness and durability, particularly in aerospace and high-performance automotive components. However, CFRT is the fastest-growing segment, expanding at a CAGR of approximately 5.4%, driven by increasing demand for ultra-lightweight materials in electric vehicles and advanced engineering applications.

Other fiber types, including aramid and hybrid composites, collectively contribute around 15% of the market, serving niche applications where enhanced impact resistance and thermal stability are required. These materials are gaining traction in specialized industrial and defense applications.

The application landscape of the Long Fiber Thermoplastics market is led by the automotive sector, which accounts for nearly 45% of total usage due to the increasing focus on lightweighting and fuel efficiency. Industrial machinery follows with approximately 25% share, leveraging these materials for durability and reduced maintenance requirements. Construction applications contribute around 18%, particularly in modular and prefabricated structures where strength and corrosion resistance are critical.

While automotive remains dominant, aerospace is the fastest-growing application segment, expanding at a CAGR of approximately 6.1%, driven by demand for high-performance materials that reduce aircraft weight and improve fuel efficiency by up to 15%. Electrical and electronics applications, along with consumer goods, collectively hold around 12% share, benefiting from improved insulation and structural properties.

Automotive manufacturers represent the leading end-user segment in the Long Fiber Thermoplastics market, accounting for approximately 48% of total demand due to extensive use in vehicle structural components and electric vehicle systems. Industrial equipment manufacturers follow with around 22% share, utilizing these materials for enhanced durability and reduced maintenance cycles. Construction companies contribute nearly 15%, particularly in modular building systems and infrastructure projects.

Aerospace emerges as the fastest-growing end-user segment, expanding at a CAGR of approximately 6.3%, supported by increasing demand for lightweight and high-strength materials in aircraft manufacturing. Other end-users, including electrical and electronics and consumer goods industries, collectively account for approximately 15% of the market, with adoption rates increasing by over 20% in high-performance applications.

Region Asia-Pacific accounted for the largest market share at 46% in 2025 however, Europe is expected to register the fastest growth, expanding at a CAGR of 4.2% between 2026 and 2033.

Asia-Pacific’s dominance is supported by production volumes exceeding 520,000 metric tons annually, driven by large-scale manufacturing clusters in China, India, and Japan. The region contributes over 50% of global automotive component production using long fiber thermoplastics, with EV-related applications rising by 38%. Europe holds approximately 27% share, supported by stringent environmental regulations that have increased recyclable composite usage by 34%. North America accounts for nearly 18%, with high adoption in aerospace and industrial automation, where material efficiency improvements of up to 22% are recorded. South America and the Middle East & Africa collectively contribute around 9%, with infrastructure projects and energy sector applications driving demand growth by 20% across these regions.

How are advanced manufacturing and lightweight material demand transforming industrial adoption?

North America holds approximately 18% of the global Long Fiber Thermoplastics market, with annual consumption exceeding 210,000 metric tons. The region’s demand is primarily driven by automotive, aerospace, and industrial machinery sectors, which collectively account for over 70% of total usage. Government initiatives promoting lightweight materials and fuel efficiency standards have increased adoption rates by 28% across automotive OEMs. Technological advancements such as automated injection molding and digital manufacturing systems have improved production efficiency by 20%. A notable example includes a leading U.S.-based manufacturer integrating long fiber thermoplastics into EV platforms, reducing component weight by 25%. Consumer behavior reflects strong enterprise-level adoption, particularly in aerospace and automotive industries, where over 60% of manufacturers prioritize high-performance composite materials.

What role do sustainability mandates and advanced engineering play in shaping material innovation?

Europe accounts for nearly 27% of the global Long Fiber Thermoplastics market, with key contributions from Germany, the UK, and France. The region is strongly influenced by regulatory frameworks focused on carbon emission reduction, leading to a 34% increase in the adoption of recyclable thermoplastics. Sustainability initiatives have driven over 65% of manufacturers to integrate eco-friendly composites into production processes. Advanced engineering applications in automotive and aerospace sectors account for over 55% of demand. A regional player has recently expanded its production capacity by 18% to meet rising demand for high-strength composites in electric vehicles. Consumer behavior is shaped by regulatory compliance, with over 70% of enterprises prioritizing sustainable material sourcing and lifecycle transparency.

How is rapid industrial expansion accelerating demand for high-performance composite materials?

Asia-Pacific leads the global Long Fiber Thermoplastics market in both volume and consumption, with production surpassing 520,000 metric tons annually. China, India, and Japan are the top consuming countries, collectively accounting for over 75% of regional demand. Infrastructure development and automotive manufacturing growth have increased material usage by 40% in the past five years. The region is also witnessing rapid adoption of advanced processing technologies, improving production efficiency by 22%. A major regional manufacturer has expanded its composite production facilities by 30%, targeting increased demand from EV and construction sectors. Consumer behavior reflects strong industrial demand, with over 65% of applications focused on cost-effective, high-strength materials for large-scale manufacturing.

How are infrastructure investments and industrial growth influencing material adoption patterns?

South America represents approximately 6% of the global Long Fiber Thermoplastics market, with Brazil and Argentina as key contributors. Infrastructure development projects have driven demand growth by 18%, particularly in construction and transportation sectors. The energy sector, including oil and gas, accounts for nearly 30% of regional usage, benefiting from corrosion-resistant material properties. Government incentives supporting industrial modernization have increased adoption rates by 15% across manufacturing industries. A regional manufacturer has introduced advanced composite solutions for pipeline systems, improving durability by 20%. Consumer behavior shows a preference for cost-efficient materials, with over 55% of demand concentrated in infrastructure and industrial applications.

How are energy sector expansion and construction projects driving composite material demand?

The Middle East & Africa region accounts for approximately 3% of the global Long Fiber Thermoplastics market, with demand primarily driven by oil & gas and construction industries. Countries such as the UAE and South Africa are leading growth, with infrastructure investments increasing by 22% over recent years. The use of long fiber thermoplastics in pipeline systems and construction materials has improved durability by up to 18%. Technological modernization initiatives have enhanced production capabilities by 15%, supporting regional demand. A local manufacturer has developed high-performance composite materials for energy applications, reducing maintenance costs by 12%. Consumer behavior reflects industry-specific demand, with over 60% of usage tied to energy and infrastructure sectors.

China – 32% market share: Long Fiber Thermoplastics market leadership driven by high production capacity, exceeding 450,000 metric tons annually and strong automotive manufacturing demand.

Germany – 18% market share: Long Fiber Thermoplastics market growth supported by advanced engineering capabilities and strong regulatory push for sustainable composite materials adoption.

The Long Fiber Thermoplastics market is moderately fragmented, with over 40 active global and regional players competing across diverse application segments. The top five companies collectively account for approximately 48% of the total market share, indicating a competitive yet partially consolidated structure. Leading players are focusing on product innovation, strategic partnerships, and capacity expansion to strengthen their market positioning. Over 25 major product launches have been recorded between 2023 and 2025, primarily targeting lightweight automotive and aerospace applications.

Strategic collaborations between material suppliers and automotive OEMs have increased by 30%, enabling co-development of advanced composite solutions. Additionally, mergers and acquisitions activity has grown by 18%, reflecting consolidation efforts among key players to enhance technological capabilities and geographic reach. Investment in R&D has increased by approximately 22%, with a strong focus on recyclable and bio-based thermoplastics.

Innovation trends such as hybrid fiber composites and automated manufacturing technologies are intensifying competition, with companies aiming to achieve performance improvements of up to 25% in strength and durability. Regional players are also expanding production capacities by 15–20% to meet rising demand, particularly in Asia-Pacific and Europe. Overall, the competitive landscape is defined by continuous innovation, strategic alliances, and a strong emphasis on sustainability-driven product development.

BASF SE

SABIC

Celanese Corporation

Solvay SA

RTP Company

LANXESS AG

Asahi Kasei Corporation

Toray Industries Inc.

Daicel Corporation

DSM Engineering Materials

Sumitomo Chemical Co., Ltd.

Mitsubishi Chemical Group

Covestro AG

Ensinger GmbH

PolyOne Corporation

Technological advancements in the Long Fiber Thermoplastics market are significantly enhancing material performance, processing efficiency, and application versatility. One of the most impactful innovations is automated pultrusion technology, which has improved production throughput by approximately 25% while ensuring consistent fiber alignment. This advancement enables manufacturers to produce high-strength components with up to 30% better load-bearing capacity compared to conventional short fiber composites. Additionally, advancements in direct long fiber thermoplastic (D-LFT) processing have reduced cycle times by nearly 20%, making large-scale production more feasible for automotive and industrial applications.

Hybrid reinforcement technologies combining glass and carbon fibers are gaining traction, improving tensile strength by up to 35% while optimizing cost efficiency. These hybrid composites are increasingly used in electric vehicle battery enclosures and structural components, where both durability and lightweight properties are critical. Furthermore, developments in injection molding simulation software have enhanced precision, reducing material waste by 15% and improving product quality consistency across high-volume manufacturing lines.

Digital transformation is also influencing the market, with AI-driven material design platforms enabling optimization of fiber orientation and polymer composition. These systems have demonstrated up to 18% improvement in product performance metrics, including impact resistance and thermal stability. In parallel, advancements in recycling technologies are allowing recovery of up to 70% of fiber content, supporting circular economy initiatives.

Emerging bio-based thermoplastics are gaining momentum, with production volumes increasing by over 20% since 2023. These materials reduce carbon emissions by approximately 25% compared to traditional polymers while maintaining comparable mechanical properties. Collectively, these technological developments are positioning long fiber thermoplastics as a high-performance, sustainable solution across automotive, aerospace, and industrial sectors.

• In March 2025, BASF expanded its Ultramid® Advanced portfolio with new long glass fiber reinforced thermoplastics designed for automotive structural components. The materials deliver up to 20% higher stiffness and improved thermal resistance, supporting lightweight EV applications and enhancing component durability. Source: www.basf.com

• In September 2024, SABIC introduced new long fiber thermoplastic solutions under its STAMAX™ range, targeting electric vehicle battery housings. These materials offer 15% weight reduction and improved flame retardancy, aligning with stricter safety regulations in EV manufacturing. Source: www.sabic.com

• In May 2025, Celanese Corporation enhanced its Celstran® LFT portfolio with improved carbon fiber reinforced grades, achieving up to 30% higher strength-to-weight ratio for aerospace and industrial applications. The development supports high-performance requirements in advanced engineering sectors. Source: www.celanese.com

• In November 2024, Solvay advanced its composite materials strategy by introducing new thermoplastic-based solutions for aerospace interiors, improving recyclability by 25% and reducing component weight by 18%, aligning with sustainability targets across aviation manufacturing. Source: www.solvay.com

The Long Fiber Thermoplastics Market Report provides a comprehensive analysis of key industry segments, covering material types such as glass fiber reinforced, carbon fiber reinforced, and hybrid composites, which collectively account for over 85% of total demand. The report evaluates applications across automotive, aerospace, construction, and industrial machinery, with transportation-related uses contributing nearly 45% of global consumption. Geographically, the report spans Asia-Pacific, Europe, North America, South America, and the Middle East & Africa, with Asia-Pacific leading in production volumes exceeding 500,000 metric tons annually. It further examines regional adoption patterns, regulatory frameworks, and technological advancements influencing market growth.

The study also explores emerging segments such as bio-based thermoplastics and recyclable composite solutions, which have seen adoption increases of over 30% in recent years. Additionally, the report assesses manufacturing technologies including pultrusion, injection molding, and direct long fiber processing, highlighting efficiency improvements of up to 25%. Industry focus areas include sustainability initiatives, material innovation, and digital manufacturing integration, offering actionable insights for stakeholders seeking to optimize production strategies and capitalize on evolving market opportunities.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

3.1% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

BASF SE, SABIC, Celanese Corporation, Solvay SA, RTP Company, LANXESS AG, Asahi Kasei Corporation, Toray Industries Inc., Daicel Corporation, DSM Engineering Materials, Sumitomo Chemical Co., Ltd., Mitsubishi Chemical Group, Covestro AG, Ensinger GmbH, PolyOne Corporation |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |