Reports

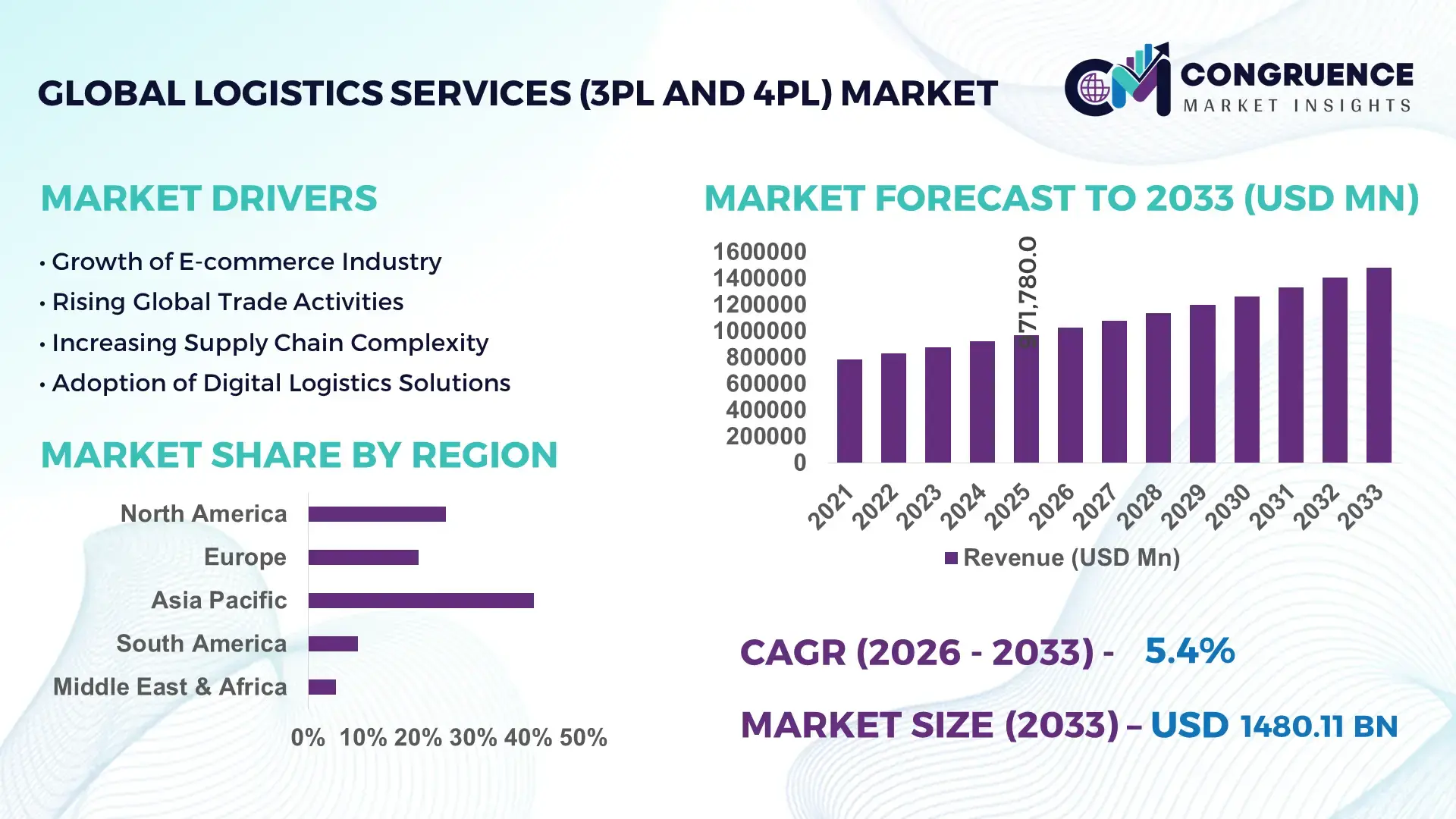

The Global Logistics Services (3PL and 4PL) Market was valued at USD 971780 Million in 2025 and is anticipated to reach a value of USD 1480106.08 Million by 2033 expanding at a CAGR of 5.4% between 2026 and 2033. Cross-border e-commerce expansion, AI-enabled warehouse orchestration, nearshoring strategies, and post-Red Sea shipping route disruptions are accelerating demand for integrated freight management, contract logistics, and multimodal transportation services across manufacturing, retail, automotive, and healthcare supply chains.

China dominates the global logistics services landscape with nearly 24% freight handling share and over 7.5 billion tons of annual port throughput, supported by aggressive smart warehouse deployment and autonomous trucking pilots across eastern industrial corridors. The United States leads in 4PL adoption, with over 42% of large enterprises integrating predictive supply-chain analytics into transportation planning. Compared to Germany’s high-efficiency manufacturing logistics networks, China maintains stronger export-linked fulfillment scalability and lower average warehousing turnaround time by approximately 18%.

Strategic expansion into AI-driven control towers, regional distribution hubs, and resilient multi-country sourcing networks remains critical for logistics providers targeting long-term contract retention and operational margin stability.

Market Size & Growth: USD 971780 Million in 2025 reaching USD 1480106.08 Million by 2033, driven by AI-enabled freight optimization and regional supply-chain restructuring.

Top Growth Drivers: E-commerce logistics demand up 31%, warehouse automation adoption up 27%, and cross-border trade digitization expanding by 22%.

Short-Term Forecast: By 2027, advanced route optimization platforms will reduce average delivery costs by 14% and improve fleet utilization efficiency by 19%.

Emerging Technologies: AI control towers, robotic picking systems, and IoT fleet tracking improve shipment visibility by 35% across high-volume logistics networks.

Regional Leaders: Asia-Pacific exceeds USD 520000 Million with smart port investments, North America crosses USD 360000 Million through 4PL integration, while Europe advances sustainable freight corridors above USD 280000 Million.

Consumer/End-User Trends: Nearly 58% of enterprise shippers prioritize real-time cargo tracking and same-day fulfillment capabilities within contract logistics agreements.

Pilot/Case Example: In 2026, automated warehouse deployment in Southeast Asia improved order processing speed by 28% and reduced labor dependency by 17%.

Competitive Landscape: Top providers control approximately 38% market share, led by integrated transportation, warehousing, and supply-chain visibility specialists across global trade routes.

Regulatory & ESG Impact: Carbon-emission compliance programs reduced empty-mile freight movement by 13% across major European and North American logistics corridors.

Investment & Funding: More than USD 48 Billion entered warehouse automation, cold-chain expansion, and regional distribution infrastructure projects during 2025–2026.

Innovation & Future Outlook: Digital twin logistics networks, autonomous delivery ecosystems, and predictive inventory orchestration are reshaping high-growth global supply-chain operations.

The Logistics Services (3PL and 4PL) Market is expanding through high-volume retail fulfillment, cold-chain pharmaceutical distribution, and automotive supply-chain consolidation. AI-assisted route planning and robotics-enabled warehousing now improve order accuracy by nearly 26% across advanced logistics hubs. Southeast Asia and Gulf trade corridors are emerging as strategic expansion zones following manufacturing diversification and tighter customs compliance requirements, creating stronger demand for integrated, technology-led logistics partnerships and long-term operational resilience.

Global logistics services providers are becoming central to industrial competitiveness as manufacturers, retailers, and healthcare suppliers restructure sourcing networks beyond single-country dependency models. Advanced 4PL operators now manage integrated procurement, transportation, warehousing, and customs visibility through centralized digital control towers, reducing average supply-chain response time by nearly 21%. Red Sea shipping disruptions and stricter carbon-emission compliance across Europe accelerated investment in multimodal freight corridors, automated fulfillment infrastructure, and regional inventory localization strategies during 2025–2026.

AI-enabled freight orchestration platforms deliver approximately 18% lower transportation planning costs compared to legacy spreadsheet-driven logistics systems while improving shipment accuracy and route utilization. The United States leads in predictive logistics analytics deployment across large enterprises, whereas China maintains stronger automated port handling capacity and warehouse robotics density. Germany continues advancing rail-linked sustainable freight systems, reducing inland cargo transfer delays by nearly 14% across manufacturing clusters.

In 2026, several automotive and consumer electronics companies expanded nearshore distribution partnerships in Mexico and Southeast Asia to shorten replenishment cycles and improve geopolitical resilience. Logistics providers are increasing investments in cold-chain automation, digital twin simulation, and electric delivery fleets to secure longer enterprise contracts and operational differentiation. Companies capable of combining technology-led visibility with flexible regional execution are strengthening long-term competitive positioning across global supply networks.

Enterprise demand for integrated logistics orchestration is accelerating as manufacturers and retailers prioritize faster inventory turnover, real-time shipment visibility, and resilient sourcing models. AI-enabled warehouse management systems improve order accuracy by nearly 26%, while automated route optimization reduces fleet fuel consumption by approximately 15%. India and Vietnam are witnessing rapid expansion of contract logistics parks following manufacturing diversification away from single-country sourcing dependence. In response to Red Sea shipping instability and rising lead-time volatility, logistics providers are expanding regional fulfillment hubs and multimodal freight partnerships. Major operators are integrating predictive analytics with customs management and inventory planning to secure longer-term enterprise contracts. The strongest competitive advantage now lies in synchronized cross-border execution rather than standalone transportation capacity.

Persistent fuel-price fluctuations, port congestion, and fragmented transport infrastructure continue limiting operational scalability across several logistics-intensive economies. In Brazil and Indonesia, inland freight delays increase average shipment turnaround time by nearly 17%, while container repositioning costs remain approximately 12% above pre-disruption levels. Smaller 3PL operators face margin pressure from rising warehouse lease rates and mandatory fleet compliance upgrades tied to emissions standards. Rail-road interoperability gaps in several industrial corridors also reduce multimodal freight efficiency during peak trade cycles. To reduce exposure, logistics companies are diversifying transportation networks, securing long-term carrier contracts, and investing in localized distribution centers closer to manufacturing clusters. Operational resilience increasingly depends on network flexibility rather than asset-heavy expansion strategies alone.

The rapid deployment of AI control towers, autonomous inventory systems, and digital freight marketplaces is opening new efficiency-driven business models across contract logistics operations. Smart warehouse adoption in China and the United States has improved labor productivity by approximately 24%, while IoT-enabled fleet tracking reduces cargo visibility gaps by nearly 31%. Government-backed logistics corridor modernization in Saudi Arabia and India is accelerating cross-border trade digitization and bonded warehousing expansion. Companies are investing heavily in robotics integration, cold-chain analytics, and predictive demand planning to strengthen pharmaceutical and high-value electronics logistics capabilities. A non-obvious opportunity is emerging in mid-sized industrial exporters seeking outsourced 4PL coordination to reduce internal supply-chain complexity without major infrastructure ownership.

As logistics ecosystems become increasingly digitized, operational consistency depends on seamless integration between transportation systems, warehouse platforms, customs interfaces, and enterprise resource planning software. Nearly 43% of logistics operators report interoperability limitations across multi-vendor digital infrastructure, while cyberattack incidents targeting freight management systems increased by approximately 28% during 2025–2026. Japan and Germany face mounting pressure to modernize aging logistics IT architecture without disrupting high-volume industrial exports. Workforce shortages in automation engineering and data-driven fleet management further complicate large-scale deployment. Companies must strengthen cloud-security frameworks, invest in interoperable platforms, and expand strategic technology partnerships to maintain shipment continuity and regulatory compliance. Long-term competitiveness increasingly depends on digital reliability as much as transportation capacity.

AI-Controlled Freight Coordination AI-powered logistics control towers are transforming shipment orchestration across manufacturing and retail supply chains. Enterprises deploying predictive route planning report nearly 19% lower fuel usage and 24% faster exception handling compared to manual dispatch systems. In the United States and Germany, logistics operators are integrating machine learning with warehouse execution systems to reduce idle inventory cycles. Companies are scaling cloud-based freight visibility platforms and forming software partnerships to improve cross-border shipment synchronization amid volatile trade routes and tighter customs monitoring.

Regionalized Distribution Network Expansion Supply-chain decentralization is accelerating warehouse and distribution hub deployment closer to industrial consumption zones. Mexico and Vietnam recorded over 21% growth in leased logistics space tied to nearshoring strategies during 2025–2026. Multi-node fulfillment models are reducing average last-mile delivery time by approximately 16% for automotive and consumer electronics suppliers. Logistics firms are restructuring transportation networks around secondary ports and inland freight corridors to improve operational continuity during geopolitical shipping disruptions and seasonal congestion spikes.

Cold-Chain Automation Acceleration Pharmaceutical and food exporters are rapidly adopting sensor-based cold-chain infrastructure to reduce spoilage and compliance risks. Automated temperature-monitoring systems improved shipment integrity by nearly 27% across vaccine and biologics transportation workflows in India and Singapore. Robotics-assisted pallet handling is also reducing cold-storage labor dependency by approximately 14%. Companies are expanding refrigerated fleet partnerships and investing in AI-linked compliance analytics to meet stricter handling standards for high-value perishable products.

Sustainable Fleet Transition Strategies Electric delivery fleets and low-emission freight operations are becoming competitive procurement differentiators across contract logistics agreements. European logistics operators using electric urban delivery vehicles reported nearly 18% lower maintenance costs and 22% reduced urban fuel dependency. Carbon-tracking integration within transportation management systems is improving route efficiency and supporting enterprise ESG reporting mandates. Several large logistics providers are prioritizing renewable-energy warehouse operations and battery-leasing partnerships to stabilize long-term operating costs while meeting stricter emissions regulations.

Transportation Services remain the dominant segment due to their central role in freight movement, route optimization, and multimodal supply-chain execution across manufacturing, retail, and industrial sectors. Large enterprises increasingly rely on integrated transportation networks to reduce delivery lead times by nearly 18% while improving shipment traceability across domestic and international trade lanes. Freight Forwarding continues maintaining strategic importance through customs coordination and cross-border consolidation, particularly across China–Europe and U.S.–Mexico industrial corridors. Warehousing Services are evolving through robotics deployment and AI-enabled inventory management, improving order accuracy by approximately 25% in high-volume fulfillment environments.

Supply Chain Management is emerging as the fastest-growing segment as enterprises shift toward centralized logistics orchestration and predictive analytics integration. Companies are prioritizing end-to-end visibility platforms capable of synchronizing procurement, transportation, inventory, and supplier coordination within a single operational ecosystem. Distribution Services are also gaining traction through decentralized fulfillment models supporting same-day delivery expectations and regional inventory localization. Logistics providers are expanding automation partnerships, smart warehouse infrastructure, and digital freight ecosystems to strengthen contract retention and improve operational resilience across increasingly fragmented global trade networks.

E-commerce Fulfillment dominates application demand due to rising same-day delivery expectations, automated order processing requirements, and expanding direct-to-consumer retail ecosystems. High-volume fulfillment centers now process approximately 32% more orders through robotics-assisted picking and AI-enabled inventory sequencing compared to conventional warehouse workflows. Domestic Logistics remains operationally critical for retail replenishment, industrial transportation, and regional freight distribution, particularly in India, the United States, and Germany where rapid urban consumption patterns are reshaping delivery infrastructure planning. Reverse Logistics is also expanding steadily as return-processing automation becomes essential for online retail profitability and customer retention strategies.

Cold Chain Logistics is the fastest-growing application segment, driven by pharmaceutical distribution, biologics transportation, and temperature-sensitive food exports. Sensor-linked monitoring systems reduce product spoilage by nearly 21% while improving regulatory compliance consistency across healthcare and food supply chains. International Logistics continues evolving through customs digitization and multimodal corridor expansion supporting nearshoring strategies and diversified sourcing models. Logistics providers are scaling regional fulfillment hubs, automated returns processing, and refrigerated transport infrastructure to strengthen operational continuity and capture specialized contract opportunities across high-value cargo categories.

The Retail Industry remains the largest end-user segment due to extensive warehousing dependency, rapid inventory turnover requirements, and high-frequency distribution operations across omnichannel commerce networks. Retail-focused logistics contracts increasingly prioritize automated fulfillment, real-time shipment visibility, and decentralized inventory placement to support faster delivery cycles. E-commerce Companies represent the fastest-growing buyer group, with AI-enabled fulfillment systems improving order processing efficiency by nearly 29% and reducing delivery exceptions by approximately 17%. Companies are responding through robotics integration, regional micro-fulfillment deployment, and advanced transportation management partnerships designed for high-volume parcel movement.

Manufacturing Industry demand remains strong as industrial producers expand supplier diversification and nearshore sourcing strategies across Mexico, Vietnam, and Eastern Europe. Automotive Industry logistics operations are becoming more synchronization-intensive due to electric vehicle component sourcing and just-in-time production requirements. Healthcare Industry buyers continue increasing investments in compliant cold-chain transportation and serialized inventory tracking, while Food and Beverage Industry operators are scaling temperature-controlled logistics networks for export stability and spoilage reduction. Logistics providers are tailoring sector-specific solutions through specialized warehousing, dedicated fleet expansion, and predictive supply-chain analytics to secure long-term enterprise agreements.

Asia-Pacific accounted for the largest market share at 41% in 2025 however, Middle East & Africa is expected to register the fastest growth, expanding at a CAGR of 6.8% between 2026 and 2033.

AI-Led Network Optimization Reshaping Freight Operations

North America remains a highly advanced logistics services hub driven by automated warehousing, integrated transportation networks, and large-scale enterprise outsourcing. The region contributes nearly 28% of global 4PL deployment activity, supported by strong retail, healthcare, and automotive supply-chain demand. U.S.-based logistics operators are accelerating AI-enabled route orchestration and predictive inventory planning to reduce transportation delays and improve fulfillment responsiveness. In 2026, multiple cross-border logistics partnerships between the United States and Mexico expanded regional nearshoring capacity, improving industrial replenishment cycles by approximately 16%. Cold-chain expansion and robotics-assisted fulfillment remain priority investment areas as companies target faster delivery execution and labor-efficiency gains across high-volume logistics corridors.

United States Market Outlook: The United States leads regional logistics transformation through advanced warehouse automation, large-scale freight digitization, and strong enterprise adoption of integrated 4PL platforms. More than 45% of large retailers now operate AI-supported fulfillment environments linked with predictive transportation management systems. Major industrial hubs including Texas, California, and Illinois continue attracting distribution infrastructure investment due to high freight density, multimodal connectivity, and expanding e-commerce delivery requirements.

Sustainable Freight Modernization Driving Structural Change

Europe’s logistics services market is increasingly shaped by low-emission freight modernization, rail-linked cargo movement, and regulatory pressure surrounding transport efficiency. The region maintains approximately 24% global logistics outsourcing penetration through highly integrated industrial supply chains across Germany, France, and the Netherlands. Smart customs processing and multimodal transport infrastructure are improving cross-border shipment consistency within manufacturing and pharmaceutical sectors. In 2025–2026, electric delivery fleet deployment across urban logistics networks increased by nearly 22%, reducing fleet operating costs and improving compliance with tightening carbon regulations. Logistics providers are prioritizing automated warehousing, digital freight exchanges, and energy-efficient transportation systems to strengthen operational resilience across high-density trade corridors.

Germany Market Outlook: Germany remains Europe’s most strategically significant logistics market due to its manufacturing concentration, rail freight integration, and advanced industrial export infrastructure. Logistics automation adoption across German industrial hubs improved warehouse throughput efficiency by approximately 19% during 2026. The country’s strong automotive and engineering sectors continue driving demand for synchronized just-in-time transportation systems, customs optimization platforms, and high-capacity multimodal distribution networks connecting Eastern and Western European supply chains.

Manufacturing Scale Accelerates Logistics Expansion

Asia-Pacific dominates the global logistics services landscape through extensive manufacturing capacity, export-driven trade activity, and rapid fulfillment infrastructure deployment. China, India, Vietnam, and Japan collectively account for a major share of industrial freight movement and warehouse construction activity. Smart logistics park development and AI-integrated distribution systems improved order processing efficiency by nearly 27% across large e-commerce and electronics supply chains during 2025–2026. Cross-border logistics corridors linked to Southeast Asian manufacturing diversification are also accelerating demand for contract logistics and multimodal transportation services. Companies continue expanding automated fulfillment hubs, regional distribution centers, and digital freight ecosystems to support rising industrial production and high-volume retail delivery requirements.

China Market Outlook: China leads the Asia-Pacific logistics market through unmatched port infrastructure, manufacturing density, and large-scale warehouse automation deployment. The country processes over 7 billion tons of annual port throughput while maintaining one of the world’s largest smart warehousing ecosystems. AI-enabled fulfillment centers across eastern industrial provinces reduced average inventory processing time by approximately 23%, supporting faster export coordination, domestic retail replenishment, and cross-border e-commerce expansion.

Infrastructure Modernization Supporting Trade Efficiency

South America’s logistics services market is expanding through agricultural exports, retail distribution growth, and improving transportation infrastructure investments. Brazil and Chile are strengthening port modernization and inland freight connectivity to reduce cargo delays and improve export competitiveness. Regional logistics operators are increasingly adopting transportation management software and warehouse automation to improve shipment visibility and reduce manual processing inefficiencies. In 2026, freight corridor upgrades linked to agribusiness exports improved cargo turnaround efficiency by nearly 14% across selected Brazilian logistics routes. Despite infrastructure gaps and fuel-cost volatility, demand for outsourced logistics coordination continues rising as enterprises seek more resilient transportation networks and integrated supply-chain execution capabilities.

Brazil Market Outlook: Brazil remains the region’s largest logistics market due to its extensive agricultural exports, industrial freight volumes, and expanding domestic consumption networks. Distribution infrastructure investment is accelerating across São Paulo and southern manufacturing corridors, where automated warehouse adoption increased by approximately 18% during 2025–2026. The country’s growing reliance on multimodal freight systems and cold-chain transportation is strengthening long-term demand for integrated 3PL and 4PL operational support.

Trade Corridor Investments Transforming Logistics Capacity

Middle East & Africa is rapidly emerging as a strategic logistics gateway driven by port modernization, free-zone expansion, and large-scale trade corridor investments. Gulf economies are prioritizing smart logistics infrastructure, automated customs processing, and integrated distribution ecosystems to strengthen non-oil economic diversification. Regional warehouse capacity linked to e-commerce and industrial trade zones expanded by nearly 20% during 2025–2026. African logistics providers are also increasing adoption of mobile freight coordination platforms to improve cargo visibility and reduce inland transportation inefficiencies. Strategic investments in multimodal transport corridors, bonded warehousing, and cold-chain facilities continue reshaping regional supply-chain competitiveness and cross-border trade execution capabilities.

Saudi Arabia Market Outlook: Saudi Arabia is becoming the region’s most influential logistics transformation hub through aggressive infrastructure modernization and trade-network expansion initiatives. The country is rapidly scaling smart ports, industrial logistics zones, and AI-assisted customs systems to strengthen global freight connectivity. In 2026, logistics infrastructure deployment linked to industrial diversification programs improved cargo processing efficiency by approximately 21%, supporting stronger regional distribution capabilities and faster multimodal trade coordination across Gulf and Red Sea corridors.

Global leaders including DHL Supply Chain, Kuehne+Nagel, DB Schenker, DSV, and GXO Logistics compete aggressively against regional contract logistics specialists and technology-driven freight orchestration providers. The top five players collectively control nearly 36% of integrated 3PL and 4PL operations, with competition centered on fulfillment speed, AI-enabled visibility, multimodal coverage, and customized enterprise logistics execution. Advanced warehouse automation improves order accuracy by approximately 25%, while predictive route optimization reduces transportation costs by nearly 18%, forcing mid-sized operators to accelerate digital infrastructure investments. Leading firms are expanding through nearshoring partnerships, cold-chain acquisitions, electric fleet deployment, and vertically integrated distribution ecosystems. Competition is shifting from pure transportation scale toward synchronized supply-chain intelligence and end-to-end operational control. High capital requirements for automation, cybersecurity integration, and cross-border infrastructure remain major entry barriers. Winning increasingly depends on combining technology-led orchestration, resilient regional networks, and sector-specific logistics specialization.

DHL Supply Chain

Kuehne+Nagel

DSV

DB Schenker

GXO Logistics

Nippon Express

CEVA Logistics

C.H. Robinson

Expeditors International

Sinotrans

XPO Logistics

Ryder System

GEODIS

UPS Supply Chain Solutions

AI-enabled transportation management systems, robotics-assisted warehousing, and IoT-linked fleet monitoring are becoming core operational technologies across global logistics networks. More than 48% of large logistics providers now operate AI-assisted route optimization platforms that reduce fuel consumption by approximately 15% and improve delivery scheduling accuracy by nearly 22%. Modern warehouse orchestration systems outperform legacy manual inventory coordination by reducing order-processing time almost 30% while lowering picking errors by nearly 25%. Companies deploying integrated digital control towers gain stronger shipment visibility, faster customs coordination, and improved contract retention across high-volume retail and manufacturing supply chains.

Emerging technologies including autonomous mobile robots, digital twins, and predictive inventory analytics are accelerating operational scalability. Robotics integration deployments now occur up to 12 times faster through modular plug-and-play automation frameworks compared to traditional custom-coded systems. Nearly 40% of advanced fulfillment operators in the United States, Germany, and China are expanding cloud-based warehouse ecosystems supporting real-time workflow synchronization. Logistics providers investing early in interoperable automation platforms are securing stronger enterprise partnerships and lower labor dependency across multi-node distribution environments.

Between 2026 and 2028, humanoid robotics, electric freight fleets, and AI-led multimodal orchestration will reshape competitive positioning across contract logistics operations. Companies capable of integrating automation with cybersecurity resilience and predictive supply-chain intelligence will dominate high-value healthcare, electronics, and cold-chain logistics contracts.

March 2025 – DHL Supply Chain deployed SVT Robotics’ SOFTBOT platform across its warehouse network, accelerating robotics integration deployments up to 12 times faster than traditional coding environments. The initiative strengthened modular automation scalability and reduced implementation bottlenecks across thousands of collaborative robotic workflows.

June 2024 – GXO Logistics signed an industry-first multi-year agreement with Agility Robotics to deploy humanoid Digit robots within live warehouse operations. The deployment expanded robotics-assisted fulfillment capabilities and improved operational flexibility for high-volume retail logistics environments through Robots-as-a-Service integration. Source: (GXO Logistics, Inc.)

April 2025 – DSV completed the acquisition of DB Schenker in a transaction valued at approximately EUR 14.3 billion, effectively doubling DSV’s operational scale and strengthening global freight forwarding and contract logistics coverage across more than 90 countries. Source: (DSV)

March 2026 – DHL Supply Chain announced expansion of North American data-center logistics infrastructure through 10 dedicated warehouse sites exceeding 7 million square feet. The investment improved hyperscale equipment handling capacity and strengthened end-to-end logistics support for rapidly expanding AI-driven data-center deployments.

The report provides detailed analysis of logistics outsourcing models across Transportation Services, Warehousing Services, Distribution Services, Freight Forwarding, and Supply Chain Management. It evaluates operational deployment trends across Domestic Logistics, International Logistics, E-commerce Fulfillment, Cold Chain Logistics, and Reverse Logistics while assessing demand patterns across retail, healthcare, automotive, manufacturing, food and beverage, and e-commerce sectors. More than 45% of enterprise logistics operators are increasing investments in AI-enabled visibility platforms, robotics-assisted warehousing, and multimodal transportation optimization systems between 2026 and 2033.

Regional coverage includes North America, Europe, Asia-Pacific, South America, and Middle East & Africa with country-level analysis focused on industrial infrastructure, fulfillment expansion, automation adoption, and cross-border trade execution. The report also examines emerging areas including digital freight orchestration, electric logistics fleets, smart warehousing ecosystems, and predictive supply-chain analytics. Strategic insights support expansion planning, technology investment prioritization, competitive benchmarking, partnership development, and long-term operational positioning across increasingly digitized logistics networks.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 971780 Million |

|

Market Revenue in 2033 |

USD 1480106.08 Million |

|

CAGR (2026 - 2033) |

5.4% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

DHL Supply Chain, Kuehne+Nagel, DSV, DB Schenker, GXO Logistics, Nippon Express, CEVA Logistics, C.H. Robinson, Expeditors International, Sinotrans, XPO Logistics, Ryder System, GEODIS, UPS Supply Chain Solutions |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |