Reports

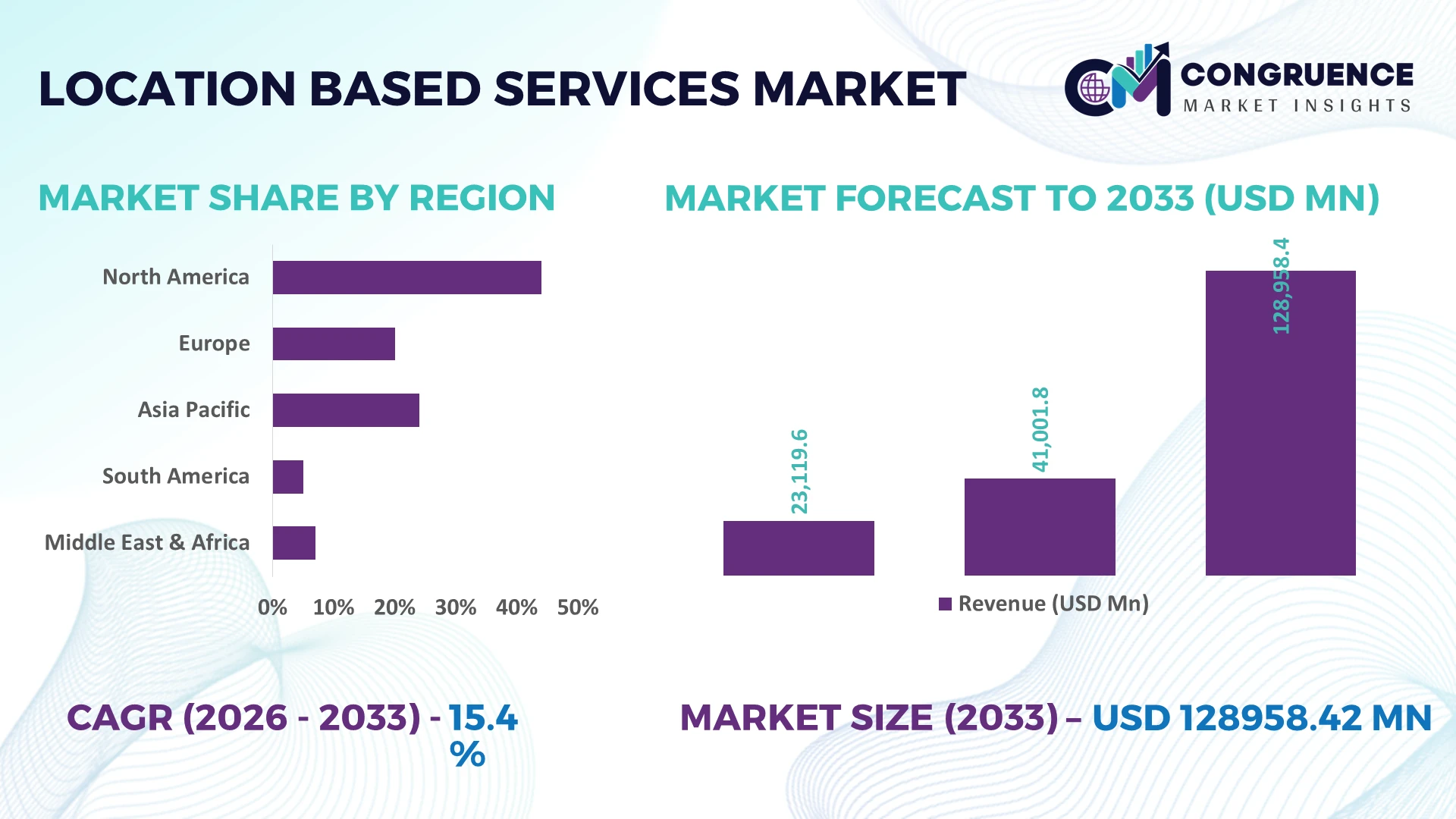

The Global Location Based Services Market was valued at USD 41001.83 Million in 2025 and is anticipated to reach a value of USD 128958.42 Million by 2033 expanding at a CAGR of 15.4% between 2026 and 2033. AI-powered geospatial intelligence, nationwide 5G deployment, connected mobility ecosystems, and enterprise demand for real-time asset visibility are accelerating Location Based Services adoption across transportation, retail, logistics, healthcare, and public safety.

The United States holds approximately 34% of global Location Based Services adoption, supported by over USD 65 billion in digital infrastructure and geospatial technology investments across transportation, retail, defense, and smart city initiatives. More than 87% of smartphones actively use advanced positioning capabilities, surpassing Japan's enterprise deployment rate, while ongoing 2026 digital infrastructure expansion strengthens nationwide location intelligence capabilities.

Businesses investing in scalable, privacy-compliant location intelligence platforms will strengthen operational efficiency, customer engagement, and long-term digital competitiveness.

Market Size & Growth: USD 41,001.83 million (2025) to USD 128,958.42 million (2033) at a CAGR of 15.4%, driven by AI-powered geospatial analytics and expanding 5G infrastructure.

Top Growth Drivers: Smartphone penetration exceeds 82%, enterprise IoT deployments grow above 20%, and connected vehicle adoption advances by nearly 18%.

Short-Term Forecast: By 2028, real-time location intelligence improves fleet efficiency by 22% while reducing operational costs by approximately 15%.

Emerging Technologies: AI, edge computing, and high-precision GNSS improve positioning accuracy by over 30% for advanced enterprise applications.

Regional Leaders: North America exceeds USD 44 billion, Asia-Pacific approaches USD 39 billion, and Europe surpasses USD 27 billion with accelerating smart mobility adoption.

Consumer/End-User Trends: More than 76% of smartphone users actively use location-enabled applications, while enterprise asset tracking adoption exceeds 60%.

Pilot/Case Example: In 2026, a smart logistics deployment improved delivery accuracy by 28% and reduced fleet idle time by 19% through AI-enabled routing.

Competitive Landscape: Leading providers collectively account for nearly 42% market share, with Google, Apple, HERE Technologies, TomTom, and Esri driving innovation.

Regulatory & ESG Impact: Privacy-focused compliance and optimized routing reduce fleet emissions by approximately 12% while supporting expanding digital governance initiatives.

Investment & Funding: More than USD 9 billion supports platform expansion, AI integration, strategic partnerships, and global digital infrastructure modernization.

Innovation & Future Outlook: AI-driven predictive location intelligence, digital twins, and ultra-precise indoor positioning are reshaping next-generation enterprise decision-making and regional expansion strategies.

Location Based Services Market is experiencing strong enterprise adoption across mobility, retail, logistics, healthcare, and smart city applications as organizations prioritize real-time geospatial intelligence and personalized digital services. AI-enhanced mapping, indoor positioning, and predictive analytics continue advancing platform capabilities, while over 68% of enterprises are expanding location-enabled operations amid evolving data privacy requirements and resilient digital infrastructure strategies, setting the stage for the strategic discussion.

Location Based Services has become a strategic digital capability as enterprises increasingly depend on real-time geospatial intelligence to optimize operations, personalize customer engagement, and improve decision-making. Rapid 5G deployment, AI-enabled mapping, and stricter digital governance are accelerating enterprise adoption, while infrastructure modernization and national digital transformation programs are reshaping competitive priorities across transportation, retail, logistics, healthcare, and public services.

AI-driven location analytics can process spatial data nearly 35% faster than conventional GIS workflows while reducing manual route planning efforts by approximately 25%, enabling higher operational efficiency across large enterprise networks. The United States continues to lead advanced commercial deployments through mature cloud and digital infrastructure, whereas India is expanding rapidly through smart mobility initiatives, digital payments integration, and large-scale smartphone adoption, creating distinct innovation and deployment dynamics over the next two to three years.

A leading logistics operator deploying AI-powered location intelligence achieved a 21% reduction in delivery delays by combining predictive routing with live traffic analytics. In response, technology providers are strengthening cloud partnerships, expanding edge-computing capabilities, and investing in privacy-centric geospatial platforms to enhance enterprise scalability. Companies that integrate intelligent location ecosystems with operational workflows will secure stronger competitive differentiation, faster service execution, and sustainable long-term market positioning.

Enterprises are accelerating investment in AI-enabled location intelligence to improve logistics visibility, customer engagement, and operational planning. More than 82% of smartphones now support advanced positioning capabilities, while enterprise IoT deployments continue expanding by over 20%, increasing demand for real-time spatial analytics. The nationwide rollout of standalone 5G networks is enabling lower-latency positioning for connected mobility and industrial applications. This structural shift is driving technology vendors to expand cloud-native mapping platforms, establish strategic telecommunications partnerships, and integrate predictive analytics into enterprise software. Organizations adopting intelligent geospatial platforms are improving resource utilization, reducing dispatch times, and strengthening data-driven operational decision-making across complex business environments.

Complex data privacy regulations and inconsistent positioning infrastructure continue limiting seamless Location Based Services deployment across multiple markets. Nearly 38% of enterprises identify regulatory compliance as a major implementation challenge, while indoor positioning accuracy can decline by more than 20% in infrastructure-constrained environments. Cross-border data localization requirements also increase integration complexity for multinational organizations. To reduce deployment risks, companies are investing in privacy-by-design architectures, localized cloud infrastructure, and standardized APIs that improve interoperability. Vendors emphasizing secure geospatial processing and regional compliance frameworks are better positioned to maintain scalability while minimizing operational disruption and implementation costs.

Growing adoption of digital twins, autonomous operations, and intelligent buildings is creating high-value opportunities for advanced Location Based Services platforms. Indoor positioning deployments are improving operational productivity by nearly 30% in manufacturing and healthcare environments, while AI-assisted navigation increases asset visibility by approximately 25%. Japan and Singapore continue expanding smart infrastructure programs that encourage precise location intelligence across industrial ecosystems. Companies are responding through R&D investments, strategic software partnerships, and integrated edge-computing platforms supporting real-time analytics. The convergence of digital twins with high-precision positioning enables enterprises to unlock measurable efficiency gains beyond conventional navigation applications.

Integrating Location Based Services across legacy enterprise systems, connected devices, and multi-cloud environments remains a major execution challenge. More than 40% of large organizations report interoperability issues during digital transformation projects, while cybersecurity incidents targeting connected infrastructure continue increasing. Maintaining consistent positioning accuracy across diverse hardware ecosystems further complicates enterprise deployment. Companies are addressing these challenges through zero-trust security architectures, open geospatial standards, cloud-native platform modernization, and long-term technology alliances. Organizations that successfully standardize secure location intelligence across distributed operations will achieve stronger operational resilience, higher service consistency, and greater long-term competitive advantage.

AI-Driven Spatial Intelligence: Enterprises are embedding AI into location platforms to automate route optimization, customer targeting, and predictive asset management. AI-enabled geospatial workflows improve routing accuracy by nearly 30% and reduce manual planning time by around 25%. Growing deployment of edge computing and enterprise cloud platforms enables faster decision-making, prompting technology providers to expand AI capabilities through strategic partnerships and integrated analytics solutions.

Indoor Positioning Expansion: Warehouses, hospitals, airports, and manufacturing facilities are rapidly adopting indoor positioning technologies to overcome GPS limitations. Enterprise deployments have increased by approximately 28%, while asset retrieval time has declined by nearly 22% through Bluetooth Low Energy and Ultra-Wideband integration. Labor shortages and warehouse automation initiatives are encouraging companies to scale precision tracking platforms and collaborate with infrastructure providers for enterprise-wide deployments.

Privacy-Centric Location Platforms: Stricter digital privacy regulations are reshaping how enterprises collect, process, and monetize location data. More than 40% of large organizations are redesigning geospatial architectures around consent-based data management, while encrypted location processing reduces compliance risks by roughly 18%. Software vendors are restructuring platform design, expanding localized cloud infrastructure, and strengthening cybersecurity capabilities to support secure enterprise adoption.

Connected Mobility Integration: Connected vehicles, intelligent transportation systems, and smart city infrastructure are driving real-time location intelligence beyond traditional navigation. Vehicle telematics adoption exceeds 65% across commercial fleets, reducing dispatch delays by approximately 20% through continuous tracking and predictive routing. Infrastructure modernization and nationwide 5G deployment are accelerating ecosystem partnerships, enabling enterprises to integrate mobility data with supply-chain, fleet, and customer engagement platforms.

Mapping Services remain the dominant segment because they form the foundation for navigation, geofencing, logistics optimization, and enterprise mobility applications. Their scalability, API-based integration, and compatibility with AI-powered platforms support deployment across multiple industries. More than 70% of enterprise location applications rely on digital mapping infrastructure, while cloud-based mapping deployments have increased by approximately 26% as organizations modernize operational workflows. Navigation Services and Tracking Services continue to represent mature segments supporting transportation and fleet visibility, whereas Geofencing strengthens customer engagement and operational automation through real-time location triggers.

Location Analytics is the fastest-growing segment as enterprises increasingly convert geospatial data into predictive business intelligence. Adoption has expanded by nearly 32% among large enterprises seeking demand forecasting, site selection, and operational optimization. Companies are strengthening investments through AI integration, analytics partnerships, and cloud-native platforms while expanding advanced geospatial capabilities across enterprise ecosystems. Investment priorities are gradually shifting from standalone mapping tools toward integrated analytics platforms that deliver measurable operational intelligence.

Fleet Management represents the largest application segment due to extensive deployment across transportation, logistics, public transit, and field service operations. Organizations increasingly depend on real-time positioning to improve vehicle utilization, reduce fuel consumption, and optimize dispatch performance. Fleet operators report route optimization improvements approaching 24%, while GPS-enabled fleet visibility exceeds 80% among large logistics enterprises. Navigation remains a mature application supporting mobility ecosystems, whereas Retail Marketing continues expanding through personalized customer engagement and location-aware promotions.

Asset Tracking is emerging as the fastest-growing application as manufacturers, warehouses, and healthcare providers require continuous monitoring of high-value assets. Enterprise deployments have increased by approximately 29% following greater adoption of IoT sensors and AI-enabled tracking platforms. Emergency Services are also expanding advanced location intelligence to improve response coordination and incident management. Technology providers are responding through cloud integration, automation, and strategic partnerships to strengthen enterprise deployment while improving operational visibility across complex supply chains.

Transportation remains the dominant end-user because large-scale fleet operations, intelligent mobility systems, and connected infrastructure require continuous location intelligence. High operational intensity and infrastructure dependency make real-time positioning essential for dispatch optimization, route planning, and traffic management. More than 75% of commercial fleet operators utilize advanced tracking solutions, while intelligent route optimization reduces delivery delays by nearly 21%. Logistics continues as a mature buyer segment, supported by expanding warehouse automation and multimodal transportation networks.

Healthcare is the fastest-growing end-user as hospitals increasingly deploy indoor positioning, patient monitoring, and medical asset tracking technologies. Adoption of location-enabled hospital operations has increased by approximately 27%, improving equipment utilization and reducing asset search times by nearly 20%. Retail continues strengthening personalized engagement strategies, while Government agencies are expanding public safety, emergency response, and smart infrastructure programs. Vendors are responding through industry-specific platforms, strategic healthcare partnerships, customized pricing models, and integrated ecosystem development to capture evolving enterprise demand.

North America accounted for the largest market share at 36.8% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 17.2% between 2026 and 2033.

AI-Driven Enterprise Location Intelligence Leadership

North America maintains its leadership through advanced cloud infrastructure, mature digital ecosystems, and widespread enterprise deployment of AI-enabled location intelligence. The region represents approximately 36.8% of global adoption, supported by large-scale implementation across transportation, retail, logistics, healthcare, and public safety. More than 84% of enterprise fleets utilize advanced GPS and telematics platforms, while nationwide 5G expansion strengthens real-time positioning capabilities. Technology companies continue expanding strategic partnerships with telecom providers and cloud vendors, accelerating deployment of high-precision geospatial analytics that improve operational visibility, customer engagement, and enterprise automation.

United States Market Outlook: The United States remains the regional innovation hub due to strong investments in cloud computing, AI, and digital infrastructure. Over 87% of smartphones actively utilize advanced location capabilities, supporting large-scale deployment across logistics, connected vehicles, healthcare, and smart city programs. Federal infrastructure modernization and enterprise AI adoption continue encouraging companies to strengthen geospatial platforms, expand cloud-native mapping services, and integrate predictive location analytics into commercial operations.

Privacy-Driven Digital Infrastructure Modernization

Europe continues strengthening enterprise deployment through digital infrastructure modernization, strict data governance, and intelligent mobility initiatives. The region accounts for nearly 27% of global market activity, supported by advanced transportation networks, connected manufacturing, and expanding smart city programs. More than 65% of logistics providers have integrated location intelligence into operational workflows, improving fleet visibility and delivery planning. Organizations increasingly prioritize privacy-centric geospatial platforms, while cross-industry collaborations accelerate deployment of secure location-enabled enterprise applications across multiple industrial sectors.

Germany Market Outlook: Germany leads the regional market through advanced automotive manufacturing, industrial automation, and enterprise digitalization. More than 72% of large manufacturers deploy location-enabled production and logistics systems to improve operational efficiency. Strong Industry 4.0 implementation, connected mobility initiatives, and continuous investment in digital infrastructure encourage technology providers to expand AI-powered geospatial solutions across industrial and commercial ecosystems.

Massive Smartphone Ecosystem Accelerates Deployment

Asia-Pacific is experiencing the fastest deployment momentum due to rapid smartphone adoption, expanding 5G networks, and large-scale digital transformation across commercial sectors. Enterprise location platform deployment has increased by approximately 31%, while mobile internet penetration continues supporting high-volume consumer and enterprise applications. Governments are accelerating smart infrastructure investments, encouraging companies to integrate AI-powered mapping, intelligent mobility platforms, and real-time location analytics into transportation, retail, healthcare, and logistics operations to improve service efficiency and operational resilience.

China Market Outlook: China dominates regional deployment through extensive digital infrastructure, large-scale mobile ecosystems, and integrated smart city development. More than 1 billion mobile users support continuous expansion of location-enabled digital services across transportation, e-commerce, and public infrastructure. Domestic technology companies continue strengthening AI-powered mapping, autonomous mobility, and enterprise geospatial analytics through sustained innovation and strategic ecosystem partnerships.

Digital Logistics Modernization Expands Demand

South America is witnessing increasing adoption of location intelligence as logistics modernization, digital retail, and connected transportation projects expand across major economies. Approximately 58% of large logistics providers now utilize advanced fleet tracking platforms, improving operational visibility and delivery coordination. Infrastructure limitations remain in selected markets, yet enterprise investment in cloud-based geospatial platforms continues increasing. Technology vendors are strengthening regional partnerships and localized service delivery models to improve deployment efficiency while supporting transportation, agriculture, and public sector digital transformation initiatives.

Brazil Market Outlook: Brazil represents the largest regional opportunity due to its extensive logistics network, growing digital economy, and expanding enterprise cloud adoption. Connected fleet deployments continue increasing across freight and retail distribution, while smart mobility initiatives improve urban transportation management. Companies are investing in localized geospatial platforms and AI-enabled fleet optimization solutions to address operational complexity across the country's vast transportation infrastructure.

Smart Infrastructure Investment Drives Adoption

The Middle East & Africa market is expanding through smart infrastructure programs, digital government initiatives, and increasing investment in intelligent mobility systems. Enterprise deployment of location-enabled platforms has risen by approximately 24%, supported by modernization projects across transportation, energy, and public safety sectors. Governments continue investing in advanced telecommunications infrastructure and connected city development, encouraging technology providers to establish regional partnerships and deploy scalable cloud-based geospatial platforms that strengthen operational efficiency and service coordination.

United Arab Emirates Market Outlook: The United Arab Emirates leads regional deployment through ambitious smart city programs, advanced digital infrastructure, and rapid enterprise technology adoption. More than 90% 5G population coverage supports real-time location applications across transportation, tourism, logistics, and public services. Public-private collaboration and continuous investment in intelligent infrastructure are enabling enterprises to integrate AI-powered location intelligence into next-generation urban and commercial operations.

Google, Apple, HERE Technologies, TomTom, and Esri compete aggressively for enterprise and consumer location intelligence, while Mapbox and regional geospatial providers challenge established leaders through flexible platforms and industry-specific customization. Global technology leaders compete on AI integration, cloud ecosystems, and developer reach, whereas regional vendors differentiate through localized mapping accuracy, compliance, and implementation speed. The top five players collectively account for approximately 62% of market activity. Competition increasingly depends on positioning accuracy, API performance, platform scalability, and data freshness, with AI-enabled routing improving operational efficiency by nearly 30% and cloud-native deployments reducing integration time by approximately 25%. Companies are expanding through telecom partnerships, edge-computing integration, digital mapping innovation, and acquisitions that strengthen geospatial data capabilities. The competitive landscape is shifting toward AI-driven predictive location intelligence and privacy-centric architectures, raising barriers for new entrants lacking proprietary mapping assets and enterprise ecosystems. Sustained success requires continuous innovation, trusted geospatial datasets, scalable cloud infrastructure, and strategic ecosystem partnerships.

Apple

HERE Technologies

TomTom

Esri

Mapbox

Hexagon AB

Trimble Inc.

Garmin Ltd.

NextNav Inc.

Foursquare

Qualcomm Technologies

Maxar Technologies

Verizon Connect

Location Based Services platforms are rapidly evolving through AI-powered geospatial analytics, high-precision GNSS, edge computing, and cloud-native mapping architectures. AI-driven route optimization improves navigation efficiency by approximately 30%, while edge processing reduces response latency by nearly 20% for real-time enterprise applications. More than 70% of large enterprises are integrating cloud-based location intelligence into transportation, retail, and logistics operations, enabling continuous data synchronization and faster operational decisions across distributed business environments.

Ultra-Wideband, Bluetooth Low Energy, and visual positioning technologies are replacing conventional GPS-only systems for indoor environments. Compared with legacy positioning methods, integrated indoor location platforms improve asset tracking accuracy by nearly 40% while reducing search time by approximately 25%. Global technology leaders and logistics providers gain the strongest competitive advantage through precise inventory visibility, autonomous workflow coordination, and intelligent facility management, while healthcare organizations benefit from faster equipment utilization and patient movement tracking.

Between 2026 and 2028, predictive location intelligence, digital twins, satellite augmentation, and privacy-preserving geospatial processing will redefine enterprise deployment strategies. Adoption of AI-assisted spatial intelligence is expected to exceed 75% among large digital enterprises, supporting automated decision-making, resilient supply-chain coordination, and highly personalized customer engagement. Organizations investing early in interoperable, AI-enabled geospatial ecosystems will establish stronger operational agility, differentiated service capabilities, and sustainable competitive positioning.

May 2026 – HERE Technologies launched HERE Location Reasoning, an AI-powered geospatial grounding solution that combines live traffic, enterprise-grade maps, and road intelligence. The platform supports more than 238 million connected vehicles, strengthening enterprise AI decision-making and accelerating intelligent mobility deployments.

August 2025 – HERE Technologies and Samsara partnered to integrate advanced mapping and geolocation services into the Connected Operations Platform, improving fleet routing, dispatch, and visibility. The collaboration enhances operations across millions of connected assets used by logistics and transportation customers worldwide. Source: here.com

July 2025 – HERE Technologies and Genesys International announced a strategic collaboration to develop next-generation in-vehicle navigation with integrated ADAS and real-time traffic intelligence for India. The solution combines live mapping, hazard alerts, and connected cockpit capabilities, supporting safer and more intelligent mobility services. Source: here.com

January 2026 – Apple expanded Apple Maps through iOS 26 with Detailed City Experience reaching 34 cities, while Share Item Location became available across 36 airlines, contributing to a 90% reduction in unrecoverable baggage according to WorldTracer data and strengthening location-enabled travel services. Source: apple.com

This report provides comprehensive analysis of the global Location Based Services market across Mapping Services, Navigation Services, Tracking Services, Geofencing, and Location Analytics. It evaluates applications including Fleet Management, Retail Marketing, Navigation, Asset Tracking, and Emergency Services while assessing demand across Transportation, Retail, Healthcare, Government, and Logistics. Regional analysis covers North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, highlighting deployment patterns, enterprise adoption, and evolving competitive dynamics.

The study examines AI-powered geospatial analytics, cloud-native mapping platforms, edge computing, high-precision positioning, indoor navigation, and digital twin integration alongside enterprise deployment strategies. It assesses operational trends, technology adoption exceeding 70% in large enterprises for cloud-based location intelligence, competitive positioning of leading providers, and shifting investment priorities. The report supports strategic decision-making for expansion planning, product development, partnership evaluation, technology adoption, market entry, and long-term business positioning across the evolving Location Based Services ecosystem between 2026 and 2033.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2025 | USD 41001.83 Million |

Market Revenue in 2033 | USD 128958.42 Million |

CAGR (2026 - 2033) | 15.4% |

Base Year | 2025 |

Forecast Period | 2026 - 2033 |

Historic Period | 2021 - 2025 |

Segments Covered | By Type

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | Google, Apple, HERE Technologies, TomTom, Esri, Mapbox, Hexagon AB, Trimble Inc., Garmin Ltd., NextNav Inc., Foursquare, Qualcomm Technologies, Maxar Technologies, Verizon Connect |

Customization & Pricing | Available on Request (10% Customization is Free) |