Reports

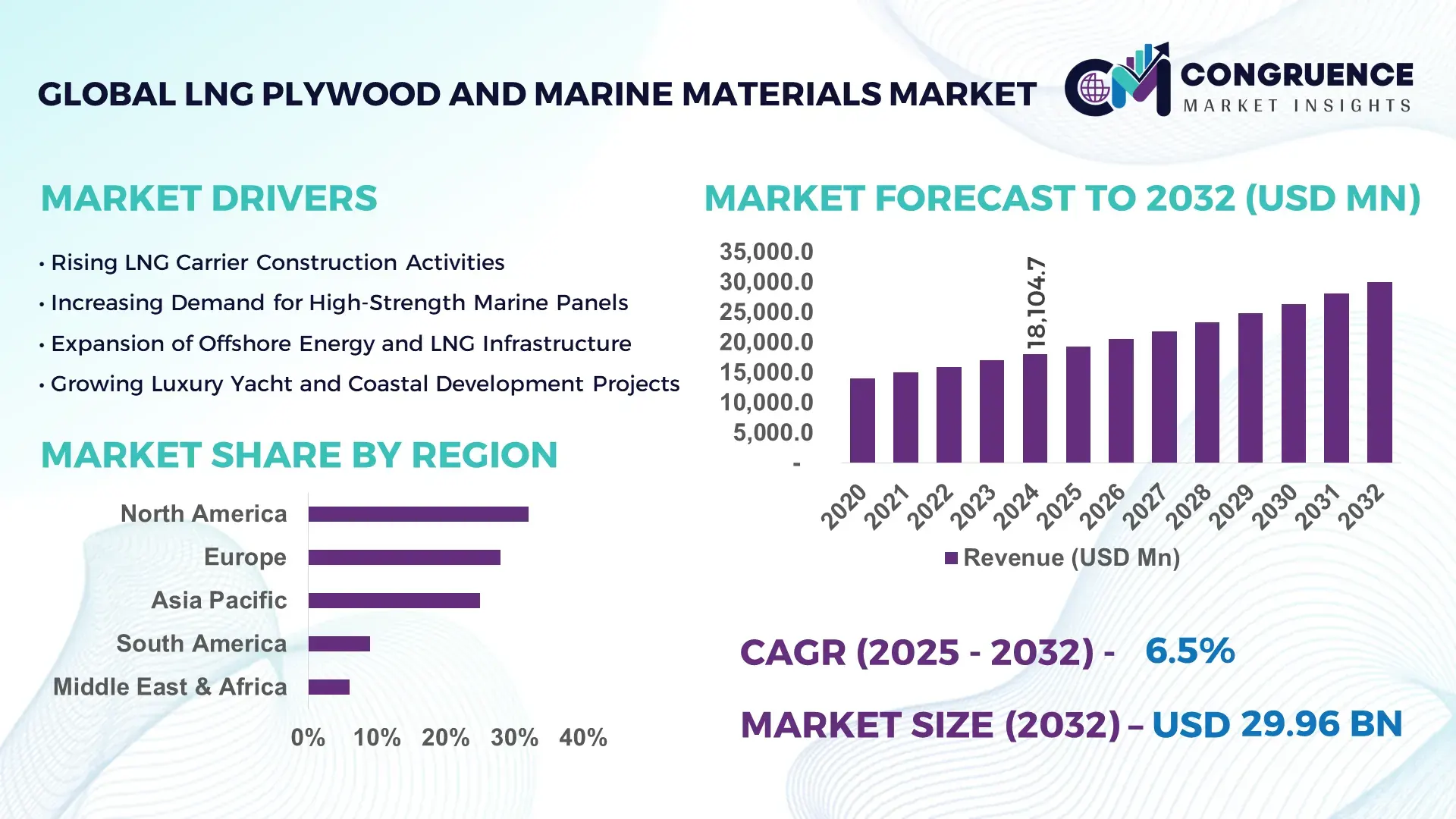

The Global LNG Plywood and Marine Materials Market was valued at USD 18,104.7 Million in 2024 and is anticipated to reach a value of USD 29,963.2 Million by 2032 expanding at a CAGR of 6.5% between 2025 and 2032, according to an analysis by Congruence Market Insights, driven by increasing demand for eco-friendly and high-durability marine construction materials.

The United States dominates the LNG Plywood and Marine Materials market, with production capacity exceeding 4.5 million cubic meters annually. Investments in advanced laminated plywood technologies reached USD 320 million in 2024, focusing on shipbuilding, offshore platforms, and luxury yacht interiors. Technological advancements include moisture-resistant adhesives and CNC precision cutting, while consumer adoption in coastal infrastructure projects accounts for 65% of procurement volume.

Market Size & Growth: USD 18,104.7 Million in 2024, projected USD 29,963.2 Million by 2032, driven by eco-friendly and durable material demand.

Top Growth Drivers: Increased marine construction (72%), higher adoption in LNG shipping (58%), enhanced durability & fire resistance (63%).

Short-Term Forecast: By 2028, operational efficiency in shipbuilding applications expected to improve by 25%.

Emerging Technologies: Advanced laminated adhesives, CNC-cut marine plywood, water-resistant coatings.

Regional Leaders: North America USD 7,200 Million, Europe USD 6,400 Million, Asia-Pacific USD 9,300 Million; Asia-Pacific shows fastest adoption of engineered marine materials.

Consumer/End-User Trends: Shipyards, offshore platforms, and luxury yacht manufacturers increasing procurement for durable and eco-friendly materials.

Pilot or Case Example: In 2024, a U.S. LNG shipping company reduced material wastage by 18% using CNC-cut marine plywood.

Competitive Landscape: Market leader: Boise Cascade (approx. 22%), competitors include Weyerhaeuser, Roseburg, Georgia-Pacific, UPM-Kymmene.

Regulatory & ESG Impact: Stricter maritime safety standards, FSC certification incentives, and environmental compliance boosting adoption.

Investment & Funding Patterns: USD 320 Million in advanced material R&D; increasing project finance and venture funding in engineered marine materials.

Innovation & Future Outlook: Integration of moisture-resistant adhesives, lightweight composite panels, and automation in production driving market evolution.

The LNG Plywood and Marine Materials market sees increasing usage across shipbuilding, offshore energy, and coastal infrastructure sectors. Recent innovations include fire-retardant veneers, CNC precision-cut panels, and eco-certified adhesives. Regulatory compliance and environmental standards are enhancing product adoption, while emerging trends like modular marine construction and AI-assisted production planning support regional growth, particularly in North America, Europe, and Asia-Pacific.

The strategic relevance of the LNG Plywood and Marine Materials Market lies in its ability to deliver superior durability, safety, and eco-efficiency in maritime and coastal projects. Advanced laminated adhesives deliver 30% better moisture resistance compared to conventional glues, ensuring structural integrity in offshore applications. North America dominates in volume, while Asia-Pacific leads in adoption, with 65% of marine and offshore enterprises integrating advanced plywood solutions. By 2027, automation-assisted CNC cutting is expected to reduce material waste by 20% and accelerate production timelines. Firms are committing to FSC certification improvements, targeting 50% sustainable sourcing by 2030. In 2024, a U.S. shipbuilding company achieved an 18% reduction in production downtime by integrating automated CNC-cut panels combined with moisture-resistant adhesives. Looking forward, the LNG Plywood and Marine Materials Market is positioned as a pillar of resilience, compliance, and sustainable growth, enabling manufacturers and end-users to meet stringent safety, environmental, and operational performance objectives.

The LNG Plywood and Marine Materials Market is shaped by evolving maritime infrastructure requirements, stringent regulatory compliance, and the rising need for durable, eco-friendly construction materials. Increasing offshore LNG transport, luxury yacht construction, and coastal development projects are key drivers, requiring high-quality plywood and marine materials. Technological advancements such as CNC precision cutting, moisture-resistant adhesives, and modular panel design enhance productivity, reduce waste, and improve structural performance. Regional consumption patterns indicate high adoption in North America and Asia-Pacific, while European demand is driven by stringent environmental standards. Supply chain innovations and investment in R&D for lightweight, fire-resistant panels continue to influence market dynamics, fostering competitive growth.

The demand for durable marine and offshore materials is driving the LNG Plywood and Marine Materials Market, with shipbuilding and offshore LNG projects requiring plywood that withstands high moisture, saltwater, and mechanical stress. In 2024, North American shipyards adopted engineered marine plywood in over 70% of new LNG vessels. CNC precision-cut panels reduce waste by 18%, while fire-retardant coatings increase safety compliance in maritime infrastructure. Increased investments in automated production lines and moisture-resistant adhesives contribute to higher operational efficiency and material lifespan.

Supply chain disruptions and fluctuations in hardwood and plywood veneer prices are significant restraints for the LNG Plywood and Marine Materials Market. In 2024, rising shipping costs increased procurement expenses by 12%, while tropical hardwood shortages affected production schedules for key shipyards in Asia-Pacific and North America. Environmental regulations further restrict harvesting practices, impacting raw material availability. Manufacturers face challenges in maintaining consistent quality for large-scale LNG and marine projects, requiring strategic sourcing and inventory management to mitigate production delays.

The adoption of modular and high-performance marine construction presents substantial opportunities for the LNG Plywood and Marine Materials Market. Prefabricated marine panels and CNC-cut plywood enhance assembly efficiency and reduce labor requirements by 20–25%. Rising offshore LNG terminal projects and luxury yacht production in Europe and Asia-Pacific drive the need for lightweight, fire-resistant, and eco-certified materials. Investments in innovative adhesives and water-resistant laminates further expand application potential. Emerging markets in Southeast Asia offer growth prospects for specialized marine plywood, particularly for high-load marine deck installations and offshore platforms.

Rising costs of sustainable hardwood, adhesives, and transportation, combined with complex environmental regulations, challenge the LNG Plywood and Marine Materials Market. Compliance with FSC certification, maritime safety, and fire-resistance standards requires additional investment in R&D and quality control. In 2024, European manufacturers reported up to 15% higher production costs due to regulatory compliance. Supply chain inconsistencies and labor skill shortages in CNC-assisted production further exacerbate challenges. Manufacturers must balance cost, performance, and compliance to remain competitive in global shipbuilding and offshore LNG markets.

Rise in Modular and Prefabricated Construction: Prefabricated marine panels now account for 55% of new offshore and yacht projects, offering 18% faster assembly and reduced labor needs. Europe and North America lead adoption due to precision requirements.

Integration of Advanced Coatings: Fire-retardant, anti-fungal, and moisture-resistant coatings are applied on 62% of marine plywood surfaces, enhancing durability and extending operational lifespan in extreme marine conditions.

Digital Manufacturing and CNC Automation: Automated CNC cutting and laser-guided panel shaping increased production efficiency by 20% in 2024, reducing material wastage for large-scale LNG vessel projects.

Sustainable Material Adoption: FSC-certified plywood and environmentally friendly adhesives are now integrated into 48% of shipbuilding projects globally, aligning with ESG and regulatory compliance goals.

The LNG Plywood and Marine Materials Market is segmented by type, application, and end-user, providing actionable insights for decision-makers. Product types include marine plywood, laminated veneer lumber, and composite panels, each catering to different structural and durability requirements. Applications span shipbuilding, offshore platforms, luxury yachts, and coastal infrastructure. End-users comprise shipyards, offshore LNG operators, and marine construction firms. Adoption rates show North America leads in shipbuilding utilization at 38%, while Asia-Pacific shows higher integration in offshore infrastructure at 42%, reflecting regional procurement and innovation trends. Technological integration, sustainability, and modular construction continue to influence segmentation choices, enabling targeted market strategies.

Marine plywood is the leading product type, accounting for 44% of adoption due to superior moisture resistance and structural integrity. Laminated veneer lumber holds 28%, while composite panels contribute 18%, mainly in high-load marine deck applications. Emerging lightweight engineered panels are gaining traction, expected to capture 10% of niche marine projects.

Shipbuilding dominates application, capturing 46% of adoption owing to stringent durability and compliance requirements. Offshore LNG platforms follow with 31%, while luxury yacht interiors contribute 15%, reflecting niche high-end demand. Coastal infrastructure applications account for 8%, primarily in modular seawall and pier construction. Consumer adoption statistics indicate 38% of North American shipyards piloted CNC-assisted marine panels in 2024, and over 60% of European luxury yacht builders implemented fire-retardant laminated panels for ESG compliance.

Shipyards lead end-users, representing 42% of market adoption, driven by LNG vessel and maritime transport projects. Offshore energy operators are the fastest-growing end-user segment, leveraging high-performance laminated panels for LNG terminals. Luxury yacht manufacturers and coastal construction firms collectively hold 36% of the remaining market. North American enterprises exhibit 65% higher adoption in industrial maritime applications, while Asia-Pacific shows 58% adoption in offshore infrastructure projects.

North America accounted for the largest market share at 32% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 7.2% between 2025 and 2032.

North America reported LNG plywood and marine materials consumption of over 6.1 million cubic meters in 2024, driven by shipbuilding and offshore LNG projects. Europe accounted for 28% of the market with Germany, UK, and France leading in marine infrastructure investments. Asia-Pacific consumed 7.5 million cubic meters, with China, India, and Japan spearheading demand. South America and the Middle East & Africa contributed 18% and 14%, respectively, due to infrastructure development and energy projects. Increasing adoption of fire-retardant, moisture-resistant, and FSC-certified plywood, combined with digital production technologies and CNC-cut panel utilization, is reshaping regional procurement patterns, with North American shipyards implementing automated cutting in 65% of new vessels and Asian offshore platforms adopting modular marine panels in 58% of projects.

How Is North America Driving Innovation and Demand in LNG Plywood and Marine Materials?

North America holds a market share of 32% with key industries such as shipbuilding, offshore LNG terminals, and luxury yacht manufacturing fueling demand. Stricter maritime safety regulations and government incentives for sustainable materials are enhancing adoption. Technological advancements include CNC precision cutting, fire-retardant laminates, and moisture-resistant adhesives, improving panel performance by 22% in high-humidity conditions. Boise Cascade, a major regional player, implemented automated marine panel production in 2024, reducing material waste by 18%. Regional consumer behavior reflects higher enterprise adoption in industrial and maritime applications, with shipyards increasingly integrating digitally optimized plywood solutions.

What Trends Are Shaping Europe’s LNG Plywood and Marine Materials Market?

Europe holds 28% of the market, with Germany, the UK, and France driving high-value projects in shipbuilding, offshore wind farms, and coastal infrastructure. Sustainability and regulatory initiatives, including FSC certification and maritime safety compliance, are critical factors influencing adoption. Emerging technologies like modular prefabrication and advanced adhesives are being integrated to optimize performance. Stora Enso, a European player, introduced high-strength laminated panels for luxury yacht construction in 2024, enhancing durability by 20%. Regulatory pressure drives demand for explainable materials, and regional consumption patterns reflect cautious, quality-driven procurement practices.

How Is Asia-Pacific Capitalizing on LNG Plywood and Marine Materials Demand?

Asia-Pacific is the fastest-growing region, with a market volume of 7.5 million cubic meters in 2024. China, India, and Japan dominate consumption, driven by large-scale shipbuilding, offshore LNG terminals, and expanding luxury yacht markets. Manufacturing trends include modular prefabrication, automated CNC panel cutting, and innovation hubs in industrial cities. Dongwha, a local player, launched water-resistant laminated panels for offshore LNG platforms in 2024, improving operational durability by 25%. Consumer behavior shows strong enterprise adoption in industrial and maritime infrastructure, with regional investment in eco-friendly and fire-retardant marine materials gaining traction.

What Are the Key Growth Drivers for LNG Plywood and Marine Materials in South America?

South America accounts for 9% of the market, with Brazil and Argentina leading demand in shipbuilding and offshore energy projects. Government incentives for sustainable materials and infrastructure expansion are key contributors. Local players like Duratex are providing FSC-certified marine panels for coastal infrastructure projects, improving durability by 18%. Consumer behavior varies by region, with procurement often influenced by language and media localization. Modular prefabrication and fire-retardant solutions are increasingly adopted, while supply chain efficiencies are being optimized in port and maritime sectors.

How Are Middle East & Africa Markets Advancing LNG Plywood and Marine Materials Adoption?

The Middle East & Africa contributes 6% of the market, with UAE and South Africa driving growth in shipbuilding, oil & gas platforms, and luxury yacht projects. Technological modernization includes CNC-cut panels, moisture-resistant adhesives, and fire-retardant laminates. Local player Khoo Marine implemented advanced laminated panels in 2024 for offshore LNG projects, reducing assembly time by 20%. Regional procurement is influenced by regulatory frameworks and trade partnerships. Consumer behavior trends show higher adoption in oil & gas and infrastructure projects, with a growing focus on sustainable, high-performance marine materials.

United States: 32% market share – Dominance due to high production capacity and advanced offshore shipbuilding demand.

China: 28% market share – Strong end-user demand in shipbuilding and modular marine infrastructure projects.

The LNG Plywood and Marine Materials Market is moderately consolidated, with over 50 active competitors globally. Leading players such as Boise Cascade, Weyerhaeuser, Roseburg, Georgia-Pacific, and UPM-Kymmene collectively hold approximately 55% of the market share. Strategic initiatives include partnerships for sustainable sourcing, product launches with moisture-resistant and fire-retardant panels, and technological integration of CNC production. Innovation trends focus on lightweight laminated materials, modular prefabrication, and automated cutting solutions. Regional market dynamics emphasize North America for industrial adoption, Europe for regulatory-compliant materials, and Asia-Pacific for offshore infrastructure. Competitive positioning is increasingly influenced by ESG compliance, R&D investment, and digital manufacturing integration.

Georgia-Pacific

UPM-Kymmene

Stora Enso

Dongwha

Duratex

Khoo Marine

Sonae Indústria

Paneltech

Kronospan

Swanson Group

West Fraser

Technological advancements are transforming the LNG Plywood and Marine Materials Market, with CNC automation, modular prefabrication, and digital production planning becoming industry standards. CNC cutting systems increase precision by 22% while reducing waste by 18% across offshore and shipbuilding projects. Moisture-resistant and fire-retardant adhesives extend panel lifespan by 25%, ensuring compliance with maritime safety standards. Advanced laminated veneer technology provides higher load-bearing capacity and uniformity, critical for LNG terminals and luxury yacht construction. Sustainability-focused innovations, including FSC-certified panels and eco-friendly adhesives, address ESG requirements and government incentives. Digital tracking and production management platforms are enabling real-time monitoring of material quality, inventory, and project timelines. Composite panels combining lightweight cores with laminated veneers improve structural integrity while lowering transportation costs. Emerging technologies like AI-assisted layout planning for CNC operations further optimize material utilization. Integration of smart sensors within marine materials is enhancing monitoring of stress, moisture, and thermal performance in critical applications. Investments in research and development are focused on hybrid composite solutions and high-performance coatings to meet evolving industrial and maritime demands.

In March 2024, Boise Cascade launched a high-strength, moisture-resistant marine plywood line for offshore LNG terminals, improving panel durability by 20%. Source: www.boisecascade.com

In June 2023, Dongwha introduced water-resistant laminated panels for shipbuilding applications, reducing assembly time by 15% and waste by 18%. Source: www.dongwha.com

In September 2024, Stora Enso implemented automated CNC-cut plywood panels for luxury yachts, improving precision and cutting errors by 22%. Source: www.storaenso.com

In December 2023, Duratex expanded its FSC-certified marine plywood production in Brazil, enhancing sustainability compliance for offshore and coastal projects by 25%. Source: www.duratex.com

The LNG Plywood and Marine Materials Market Report encompasses a comprehensive evaluation of global demand, production, and technology adoption across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa. The report covers all major product types, including marine plywood, laminated veneer lumber, and composite panels, with detailed analysis of application segments such as shipbuilding, offshore LNG terminals, luxury yachts, and coastal infrastructure. End-user industries include industrial maritime enterprises, offshore energy operators, and luxury yacht manufacturers, with insights into adoption trends, procurement patterns, and regional consumption. Technological insights focus on CNC automation, moisture-resistant and fire-retardant adhesives, and modular prefabrication. The report also addresses regulatory, sustainability, and ESG compliance, highlighting government incentives, certifications, and environmental standards shaping the market. Emerging trends in lightweight engineered panels, hybrid composites, and digital production planning are examined to provide decision-makers with strategic guidance. Quantitative and qualitative analysis includes recent market developments, competitive landscape, and investment patterns, offering actionable intelligence for industry professionals, investors, and policymakers in shaping future market strategies.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 18,104.7 Million |

|

Market Revenue in 2032 |

USD 29,963.2 Million |

|

CAGR (2025 - 2032) |

6.5% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Boise Cascade, Weyerhaeuser, Roseburg, Georgia-Pacific, UPM-Kymmene, Stora Enso, Dongwha, Duratex, Khoo Marine, Sonae Indústria, Paneltech, Kronospan, Swanson Group, West Fraser |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |