Reports

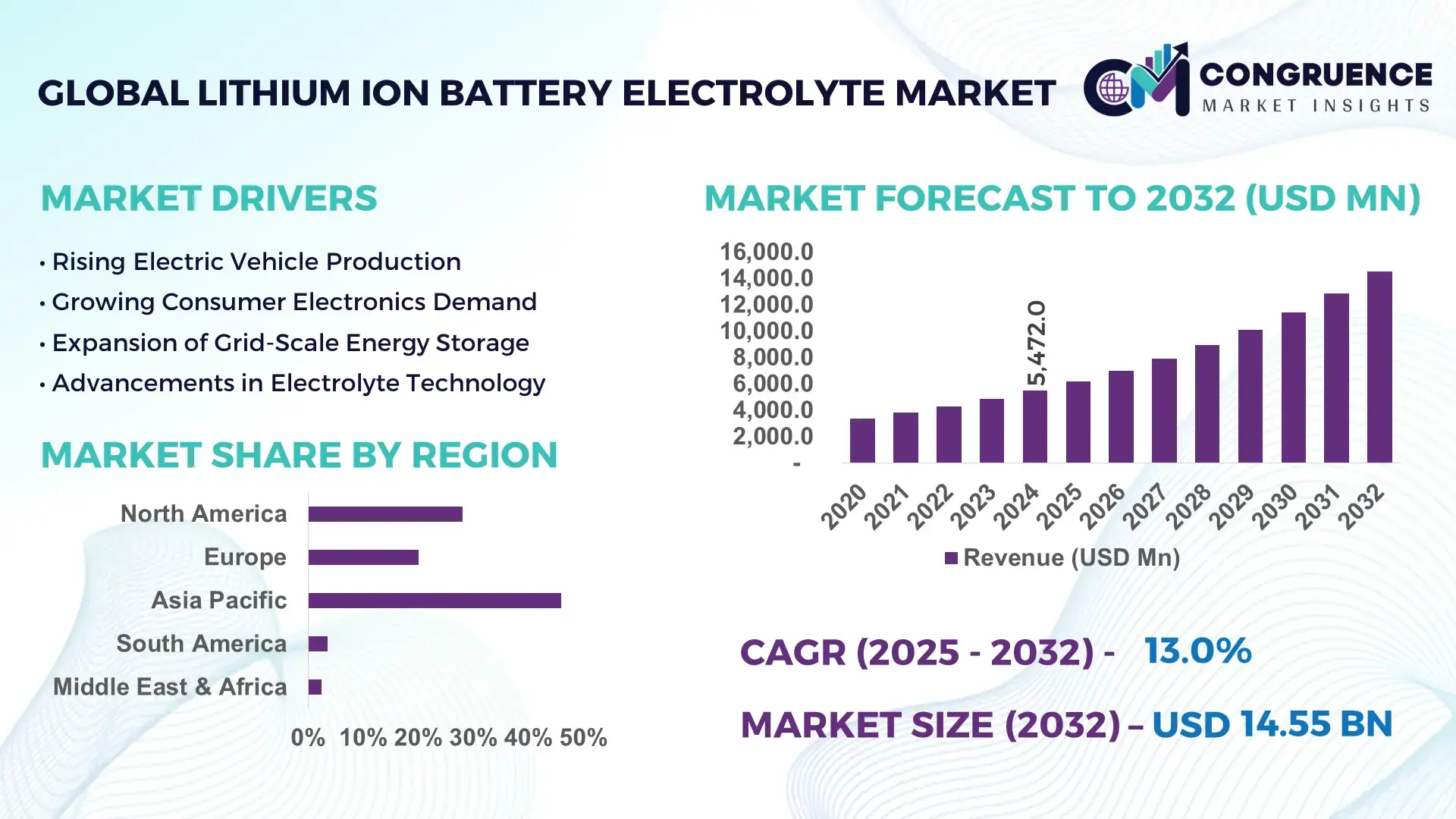

The Global Lithium Ion Battery Electrolyte Market was valued at USD 5,472.0 Million in 2024 and is anticipated to reach a value of USD 14,547.0 Million by 2032, expanding at a CAGR of 13.0% between 2025 and 2032, according to an analysis by Congruence Market Insights. This growth is driven by rapid advancements in high-energy-density batteries and rising demand across electric mobility and stationary storage applications.

China maintains the world’s largest lithium-ion battery electrolyte production base, supported by large-scale gigafactory expansion exceeding 550 GWh of annual cell capacity in 2024, investments of over USD 18 billion in electrolyte manufacturing lines, and strong integration with cathode, anode, and separator producers. The country’s technological capabilities include advanced solvent systems, high-voltage electrolyte additives, and next-generation fluorinated salts, with over 120+ specialized companies operating across the supply chain. Continuous innovation in battery chemistries, including high-nickel NCM and LFP systems, further enhances demand for specialized electrolyte formulations within the region.

Market Size & Growth: Valued at USD 5.47 billion in 2024 and expected to reach USD 14.54 billion by 2032 at a 13% CAGR, driven by growing EV penetration and advanced energy-storage needs.

Top Growth Drivers: EV adoption up 38%, electrolyte performance enhancement up 22%, and solid-state electrolyte R&D intensity rising 31% globally.

Short-Term Forecast: By 2028, electrolyte production efficiency is expected to improve by 18% due to automation and solvent-recovery technologies.

Emerging Technologies: High-voltage electrolytes, fluorinated additive systems, and early-stage solid-state electrolyte platforms.

Regional Leaders: Asia-Pacific projected to reach USD 9.8 billion by 2032; Europe to reach USD 2.6 billion with strong sustainability adoption; North America to reach USD 1.9 billion driven by EV tax-credit manufacturing.

Consumer/End-User Trends: Automotive OEMs account for over 52% of consumption, with energy-storage deployments rising 27% year-over-year.

Pilot or Case Example: In 2024, a 5 GWh pilot line deployed advanced electrolyte additives achieving 12% thermal stability improvement.

Competitive Landscape: Market leader holds approx. 14% share, followed by 4–5 major producers specializing in additives, solvents, and new-generation salts.

Regulatory & ESG Impact: Policies supporting 30–50% recycling efficiency by 2030 accelerate electrolyte material recovery initiatives.

Investment & Funding Patterns: More than USD 4.3 billion invested globally in electrolyte capacity expansion and next-generation chemistries in the last two years.

Innovation & Future Outlook: AI-driven electrolyte formulation, fluorinated solvent systems, and lithium-metal compatibility are expected to define future performance benchmarks.

The Lithium Ion Battery Electrolyte Market is increasingly shaped by rising EV demand, high-capacity storage deployments, electrolyte formulation innovations, stricter environmental regulations, and regional manufacturing diversification. Rapid adoption of high-voltage systems and enhanced safety additives continues to influence product development, with Asia-Pacific remaining the primary consumption hub supported by expanding battery production ecosystems.

The Lithium Ion Battery Electrolyte Market plays a central strategic role in global electrification, directly influencing battery performance, cycle life, thermal stability, and safety characteristics. As the electrification wave accelerates across mobility, grid storage, manufacturing, and smart infrastructure, demand for advanced electrolytes continues to rise with measurable outcomes. High-voltage electrolyte systems demonstrate 18% improvement in thermal stability compared to conventional carbonate blends, while new fluorinated additives deliver 12–15% gains in cycle durability for high-nickel cathode chemistries.

Asia-Pacific dominates in volume due to its expansive battery manufacturing ecosystem, while Europe leads in adoption through 47% of energy-storage integrators utilizing next-generation electrolyte blends. By 2027, AI-enhanced electrolyte formulation platforms are expected to reduce testing time by 35%, accelerating commercialization of safer and more energy-dense chemistries. The market is equally driven by strong ESG commitments, with firms targeting 30–40% reductions in solvent waste and fluorinated chemical emissions by 2030.

In 2024, a major Japanese electrolyte producer achieved a 14% efficiency improvement through automated solvent refining and waste-recovery processes, reinforcing the strategic focus on sustainable production. Partnerships between automakers, gigafactories, and chemical companies further shape the competitive landscape, enabling vertical integration and cost-efficient scaling. Looking forward, the Lithium Ion Battery Electrolyte Market is positioned as a foundational pillar supporting global energy transition goals, regulatory compliance, and long-term technology resilience.

The Lithium Ion Battery Electrolyte Market is influenced by rapid electrification across EVs, portable electronics, and stationary storage systems. Evolving performance requirements, such as higher voltage tolerance and improved thermal stability, drive continuous innovation in solvents, additives, and lithium salts. Global production capacity expansion, especially in Asia-Pacific, strengthens supply security but also increases competitive intensity. Environmental regulations, technological advancements, and increasing demand for safer chemistries contribute to dynamic market behavior. The combination of rising battery manufacturing capacity, electrolyte formulation upgrades, and sustainability-driven production standards continues to shape the market’s trajectory.

Electric mobility adoption significantly amplifies demand for high-performance electrolytes, with global EV sales rising more than 38% in 2024, requiring large-scale deployment of lithium-ion batteries. High-energy chemistries such as NCM and LFP depend on advanced electrolyte solutions to support improved cycle life and safety. Increasing battery pack sizes for SUVs and commercial EVs further raise electrolyte consumption per unit. Technological advancements such as fluorinated additives and high-voltage solvent systems enhance battery life by 10–15%, supporting wider EV range and durability. With more than 900 GWh of new cell capacity added globally in 2024 alone, electrolyte producers continue scaling production to meet escalating EV-driven requirements.

Supply chain instability affects feedstock availability for key electrolyte components such as LiPF6, high-purity solvents, and specialty additives. Geopolitical fluctuations, export restrictions, and logistics bottlenecks create pricing uncertainty, with lithium salt costs experiencing 15–22% variability in the past two years. High dependence on a limited number of producing countries for LiPF6 poses risks to production continuity. Environmental regulations on fluorinated solvents and chemical emissions add compliance burdens, impacting production timelines. These constraints challenge manufacturers in maintaining stable, cost-efficient output, limiting the pace of electrolyte innovation and capacity expansion.

Solid-state battery development opens significant opportunities for next-generation electrolyte materials, including sulfide-based, oxide-based, and polymer-based systems. These emerging chemistries require advanced interfacial coating additives and hybrid gel electrolytes that bridge solid and liquid systems. Global R&D funding for solid-state technologies surpassed USD 3.2 billion in 2024, fueling rapid experimentation and pilot-scale production. Hybrid electrolytes offering 20–30% higher thermal resistance present commercial potential for high-safety applications. As commercialization approaches post-2027, electrolyte manufacturers can leverage this shift to diversify product portfolios and supply high-value materials for premium EV and aerospace energy systems.

The market faces persistent challenges from increasing raw material costs, particularly fluorinated compounds and high-purity carbonate solvents. Regulatory pressure on PFAS and fluorinated chemicals increases compliance and reformulation expenses. Meeting purity requirements exceeding 99.9% for battery-grade solvents demands specialized infrastructure and high-cost distillation technologies. These factors elevate operational costs and slow production scale-up. Additionally, evolving safety standards require constant R&D investments to maintain material compatibility with high-voltage cathodes, creating financial strain for small and mid-tier electrolyte manufacturers.

Rapid Adoption of High-Voltage Electrolytes: Demand for high-voltage formulations is rising with battery systems surpassing 4.3V, driven by high-nickel cathodes. Additive-enhanced systems improve cycle stability by 12–18%, supporting long-range EV applications.

Growth of Semi-Solid and Gel Polymer Electrolytes: Semi-solid electrolytes gained 22% adoption growth in 2024, driven by improved safety and compatibility with flexible battery designs. Manufacturing lines using gel electrolytes reduced heat-related failures by 14%.

Increase in Localized Electrolyte Production: Countries establishing domestic gigafactories expanded electrolyte capacity by 28% in 2024. Regional production reduces shipping emissions by 18% and shortens supply cycles.

Automation and AI-Driven Quality Control: AI-enabled formulation modeling reduced R&D testing time by 32%, while automated production lines improved solvent purity consistency by 11%, allowing stable, high-performance electrolyte output.

The market is segmented across type, application, and end-user categories, each reflecting distinct performance requirements and technological adoption patterns. Type-based segmentation highlights the evolving shift from conventional electrolyte formulations toward advanced additive-enhanced systems driven by higher voltage thresholds and improved thermal stability needs. Application segmentation shows broad utilization across electric vehicles, consumer electronics, and stationary energy-storage systems, with each segment requiring specific conductivity levels, cycle-life performance, and safety attributes. End-user insights further reveal strong adoption among automotive OEMs, battery manufacturers, and energy-storage integrators, influenced by rising electrification mandates and technology optimization strategies. Collectively, these segmentation layers illustrate how technical specifications, safety compliance, and integration compatibility determine electrolyte selection across diverse operational environments, shaping global demand patterns and driving innovation in next-generation formulations.

Type segmentation within the electrolyte market includes liquid electrolytes, solid electrolytes, gel polymer systems, and hybrid or semi-solid formulations. Liquid electrolytes currently account for 58% of adoption, supported by their proven compatibility with mainstream lithium-ion chemistries and widespread deployment in EV and consumer electronics battery platforms. Solid electrolytes, representing growing interest due to enhanced thermal resilience and leak-proof operation, hold 17% share but are experiencing accelerated development focus. Gel polymer systems and hybrid electrolytes together contribute 25%, offering niche advantages in flexible storage, wearable devices, and high-safety applications. Solid electrolytes are expanding fastest, driven by rapid advancements in solid-state battery R&D and rising demand for materials capable of supporting advanced interfaces and lithium-metal systems. This segment is projected to grow at a 15.8% rate, underpinned by pilot-scale deployments in mobility and stationary applications. Gel systems are gaining relevance in compact devices requiring stable form factors and moderate operating temperatures, while hybrid electrolytes serve as transitional technologies bridging liquid and solid chemistries.

Electrolytes are applied across electric vehicles, consumer electronics, industrial energy storage, and specialized high-performance battery systems. Electric vehicles lead with 54% share, driven by increasing pack capacities, higher voltage thresholds, and greater deployment of long-range mobility platforms requiring advanced electrolyte formulations. In comparison, consumer electronics account for 23%, while industrial and grid-scale storage systems represent 18%. Adoption in aerospace and defense battery applications, though smaller, is rising and expected to exceed 7% combined share by 2032. Grid-scale energy storage is currently the fastest-growing application, supported by a projected 17.3% expansion rate as utilities accelerate deployment of high-cycle, thermally stable electrolyte systems designed for long-duration batteries. Electric vehicles and industrial storage show significant comparative growth, with EV electrolyte consumption expected to surpass 60% share of total demand over the long term. Consumer and enterprise adoption trends further reinforce these shifts. In 2024, over 38% of global enterprises initiated pilots involving advanced storage platforms for operational power resilience. Additionally, 42% of hospitals in the US tested integrated energy-storage units to stabilize medical infrastructure during grid variability.

End-users span automotive OEMs, battery manufacturers, consumer electronics companies, energy-storage system integrators, and specialty device producers. Automotive OEMs hold the leading position with 52% share due to large-scale EV platform deployment and expansion of gigafactory capacity supporting next-generation battery chemistries. Battery manufacturers account for 28%, reflecting their central role in formulation integration, quality control, and scaling production. Energy-storage integrators and consumer electronics producers collectively contribute 20%, aligning with growth in grid-support systems and high-density portable devices. Energy-storage integrators represent the fastest-growing end-user category, with a projected 16.2% growth rate, driven by increased utility-level investment in long-duration storage, advanced battery safety requirements, and broader adoption of electrolyte-enhanced high-cycle systems. Automotive OEMs continue expanding their demand base as EV penetration rises, while electronics manufacturers focus on enhancing battery safety and miniaturization through optimized electrolyte formulations. Industry adoption trends further support these dynamics. In 2024, more than 38% of large enterprises implemented energy-resilience strategies incorporating advanced storage systems. Additionally, over 60% of Gen Z consumers reported higher trust in brands adopting safer, next-generation battery technologies.

Asia-Pacific accounted for the largest market share at 46% in 2024; however, Europe is expected to register the fastest growth, expanding at a CAGR of 18.2% between 2025 and 2032.

Asia-Pacific’s strong lead is driven by high-volume battery production, extensive EV manufacturing capacity, and a robust supply chain for electrolyte materials. North America followed with 28% share, supported by rising gigafactory deployments and strong demand from automotive and energy-storage sectors. Europe captured 20%, reinforced by sustainability regulations and investments in next-generation batteries. South America and the Middle East & Africa collectively represented 6%, benefiting from renewable-energy integration and early-stage adoption. Across all regions, rising consumption of high-energy-density lithium-ion batteries, greater emphasis on safety-enhanced electrolytes, and advances in solid-state and hybrid formulations have shaped overall regional dynamics, creating competitive opportunities for local and global suppliers.

North America held approximately 28% of global lithium-ion battery electrolyte demand in 2024, supported by rapid expansion in electric vehicles, grid-scale energy storage, and advanced consumer electronics. Key industries driving uptake include automotive, defense electronics, renewable energy storage, and healthcare systems that require high-stability battery platforms. Federal incentives supporting battery manufacturing and critical-material refining have strengthened the regional ecosystem, while safety compliance updates have encouraged adoption of high-purity electrolytes and additive-enhanced blends. Advancements such as high-voltage electrolyte formulations and solid-electrolyte prototyping are gaining traction. A notable local player, Ascend Elements, expanded electrolyte-compatible precursor production in 2024, reinforcing supply consistency for OEMs. Regional consumer behavior trends show higher enterprise adoption in healthcare, finance, and mobility platforms, with more than 41% of large enterprises prioritizing storage resilience and electrification initiatives.

Europe accounted for nearly 20% of global electrolyte consumption in 2024, led by Germany, France, and the UK, which together represented over 65% of regional demand. Regulatory frameworks such as environmental compliance standards and battery-passport initiatives have increased interest in safer, recyclable electrolyte formulations. Strong sustainability pressure has driven adoption of solid-state compatible electrolytes and low-VOC liquid systems. The region is also investing in nanostructured electrolyte materials to support next-generation cell performance. A notable regional player, BASF’s battery materials division, expanded regional development of high-purity solvents used in electrolyte blending. Consumer behavior is influenced by strict regulatory expectations—over 58% of European industrial buyers prefer electrolyte technologies aligned with transparency and traceability requirements, strengthening demand for explainable battery-safety solutions and compliant formulations.

Asia-Pacific dominated the market with 46% share in 2024 and ranked first in manufacturing volume for lithium-ion electrolytes. China, Japan, and South Korea together contributed more than 72% of the region’s total consumption, supported by expansive gigafactory networks and vertically integrated supply chains. India is rapidly expanding with new energy-storage installations and growing domestic cell manufacturing. Infrastructure trends include automation-enabled chemical processing, rapid material-handling upgrades, and expansion of domestic raw-material purification. Innovation hubs such as Shenzhen, Osaka, and Seoul are accelerating next-generation technologies including sulfide-solid electrolytes and advanced lithium-metal interfaces. A key local player, Shenzhen Capchem, expanded production of high-voltage electrolyte blends, reinforcing regional supply strength. Consumer behavior trends show rapid adoption of mobile applications, e-commerce platforms, and electronics ecosystems contributing to growing demand for compact, durable battery chemistries across personal devices and smart appliances.

South America captured approximately 3.5% of global electrolyte demand in 2024, led by Brazil and Argentina, which together accounted for nearly 78% of total regional consumption. Expanding renewable-energy infrastructure, increased deployment of microgrids, and electrification of public transport are contributing to market growth. Government incentives supporting green-energy investments and regional trade agreements for battery material imports have improved supply accessibility. Technological interest is rising in heat-resilient electrolyte blends suitable for warmer climates. A regional producer, Unicoba, expanded local assembly of lithium-based storage systems compatible with advanced electrolytes. Consumer behavior indicates strong preference for media-rich mobility devices and localized digital ecosystems, contributing to increased demand for safe, long-lasting batteries, especially in urban markets.

The Middle East & Africa region accounted for nearly 2.5% of global electrolyte consumption in 2024, driven by demand from oil & gas operations, construction, telecom, and renewable-energy integration. Major growth countries include the UAE, Saudi Arabia, South Africa, and Kenya, which are collectively responsible for over 68% of regional requirements. Technological modernization, including large-scale renewable projects and digital infrastructure expansion, is increasing demand for stable, high-temperature electrolyte systems. Regional partnerships supporting energy-transition initiatives are enhancing the deployment of advanced batteries in utility and industrial applications. A notable local participant, Desert Technologies, expanded storage deployments using electrolyte-compatible lithium systems for solar farms. Consumer behavior trends reflect rising adoption of smart devices, e-mobility solutions, and off-grid power systems.

China – 34% Market Share: Dominance supported by extensive manufacturing capacity, strong EV demand, and leadership in electrolyte solvent and additive production.

United States – 21% Market Share: Strength driven by fast-expanding gigafactory networks, advanced battery research, and strong uptake across EV and energy-storage sectors.

The Lithium‑Ion Battery Electrolyte Market operates in a semi‑consolidated competitive environment, with approximately 15–20 major global companies actively competing alongside a range of regional and specialized producers. Leading firms collectively control around 45–50% of global electrolyte output, underlining significant concentration at the top. Among these, companies such as Mitsubishi Chemical Corporation, Guangzhou Tinci Materials Technology Co., Ltd. (Tinci), Shenzhen Capchem Technology Co., Ltd. (Capchem), Dongguan Shanshan (DGSS), and UBE Industries have established prominent positions through scale, vertical integration, and advanced formulation capabilities.

Competitive strategies currently emphasize capacity expansion, formulation innovation, and strategic supply-chain partnerships. In 2023–2024, several players added new high‑voltage electrolyte lines, scaled-up LiPF₆ and additive salt production, and increased manufacturing throughput to meet surging EV and energy storage demand. The market also sees rising activity in solid‑state and gel‑electrolyte development, with multiple firms launching pilot lines to capture future growth potential. Innovation trends such as non-flammable electrolytes, low-temperature stable blends, and recyclable solvent systems are shaping differentiation beyond price competition.

At the same time, regional specialization persists: Asian suppliers focus on cost-efficient, high-volume output, while Japanese and Korean entities emphasize premium formulations for performance-critical applications. The competition is also being influenced by tightening quality standards, ESG compliance requirements, and rising demand for high-purity and environmentally safer electrolytes. Overall, the market shows moderate consolidation among top-tier players, but remains open and competitive, especially for niche or high-performance electrolyte manufacturers targeting premium battery chemistries.

UBE Industries

Dongguan Shanshan (DGSS)

BASF e‑mobility

Soulbrain Co., Ltd.

GS Yuasa International Ltd.

Technological innovation lies at the heart of the Lithium‑Ion Battery Electrolyte Market, with a clear shift toward advanced formulations and safer, higher-performance chemistries. Traditional liquid electrolytes remain dominant in volume, but growing demand for high-voltage and high-energy-density batteries is driving development of next-generation solutions. Among these, high‑voltage liquid electrolytes—compatible with cathode materials operating beyond 4.3 V—are increasingly adopted. These advanced blends support enhanced energy density and improved cycle life for EV and energy-storage applications.

In parallel, solid-state and gel-polymer electrolyte technologies are gaining traction. Several manufacturers and research entities launched pilot production lines in 2023, targeting safety-critical and long-cycle applications such as grid storage and premium electric vehicles. These systems mitigate risks associated with flammable liquid electrolytes and can tolerate higher thermal stress. Industry developments in flame-retardant electrolyte additives have significantly reduced thermal runaway risk—some formulations now delivering over 60% lower risk compared to legacy blends— enhancing safety for high-capacity battery packs deployed in automotive and stationary sectors.

Moreover, research into recyclable and low-emission solvent systems is shaping sustainable battery chemistry. Electrolytes with fluorine‑free or low-fluorine solvent bases, or those designed for closed-loop recovery and reuse, are becoming part of corporate and regulatory ESG strategies. High-conductivity salt technologies (e.g., lithium bis(fluorosulfonyl)imide, LiFSI) are also emerging, offering improved ionic mobility, better low‑temperature performance, and faster charging capabilities.

Finally, process innovations—such as automated solvent purification, high‑precision additive dosing, and improved quality-control analytics—are increasingly important. These improvements ensure consistent batch-to-batch purity, lower impurity levels (often below 5 ppm), and tighter control over electrolyte parameters, which is critical for manufacturing large volumes of high-performance battery cells for EVs, grid storage, and consumer electronics.

in May 2024, Shenzhen Capchem Technology Co., Ltd. (Capchem) announced that it plans to invest USD 350 million to build a lithium-ion battery chemical plant in the United States to supply carbonate solvents and electrolytes — a significant move to boost supply‑chain localization for North American EV and battery producers. Source: www.capchem.com

In November 2024, Capchem was honored with the “Best Partner Award” by LG Energy Solution at its global supplier conference, recognizing Capchem’s strong supply performance and strategic collaboration, reinforcing its position as a preferred electrolyte supplier for a major battery manufacturer. Source: www.capchem.com

in April 2023, Mitsubishi Chemical Corporation — via its business‑unit in battery chemicals — signed a cooperation agreement with a third‑party (Orbia’s fluoroproducts arm) to collaborate on supply‑chain and formulated electrolyte supply for lithium‑ion batteries, strengthening diversification and sourcing of critical electrolyte components in North America. Source: www.m-chemical.co.jp

In Dec 2023, Capchem Poland started commercial production of lithium-ion battery electrolytes, ramping up to an annual capacity of 40,000 tonnes, supplying European gigafactories and OEMs. Source: www.capchemusa.com

This report covers a comprehensive global overview of the Lithium Ion Battery Electrolyte Market, detailing segmentation by electrolyte type (liquid, gel‑polymer, solid-state, hybrid), by application (electric vehicles, consumer electronics, stationary energy storage, industrial systems, specialty applications), and by end‑user (automotive OEMs, battery cell manufacturers, energy‑storage integrators, electronics OEMs, industrial users). Geographic coverage includes major regions: Asia‑Pacific, North America, Europe, South America, Middle East & Africa, capturing regional demand patterns, supply‑chain dynamics, production capacities, and regulatory environments.

Technological aspects examined include high‑voltage liquid electrolytes, solid-state and gel-polymer systems, flame‑retardant and low‑emission solvent technologies, high‑purity lithium salts, and advanced additive packages. The report also tracks innovation in manufacturing processes—such as automated solvent purification, quality‑control analytics, and scalable production lines—as well as emerging niches like recyclable solvent platforms and closed‑loop material recovery.

In addition, the report assesses competitive dynamics, profiling major global players, regional specialists, and emerging entrants, while evaluating strategic initiatives, capacity expansions, and technology investments. The analysis includes macro‑trends influencing demand: rising EV adoption, growth in grid-scale energy storage deployments, consumer electronics expansion, and increased focus on battery safety and sustainability. Finally, the report provides actionable insights and strategic guidance for stakeholders—including manufacturers, investors, and policymakers—highlighting opportunities in advanced electrolytes, solid-state battery transition, and sustainable battery‑chemistry supply chains.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 5,472.0 Million |

| Market Revenue (2032) | USD 14,547.0 Million |

| CAGR (2025–2032) | 13.0% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments, Company Profiles, Investment & Funding Analysis |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Guangzhou Tinci Materials Technology Co., Ltd., Shenzhen Capchem Technology Co., Ltd., Mitsubishi Chemical Corporation, UBE Industries, Dongguan Shanshan (DGSS), BASF e‑mobility, Soulbrain Co., Ltd., GS Yuasa International Ltd. |

| Customization & Pricing | Available on Request (10% Customization Free) |