Reports

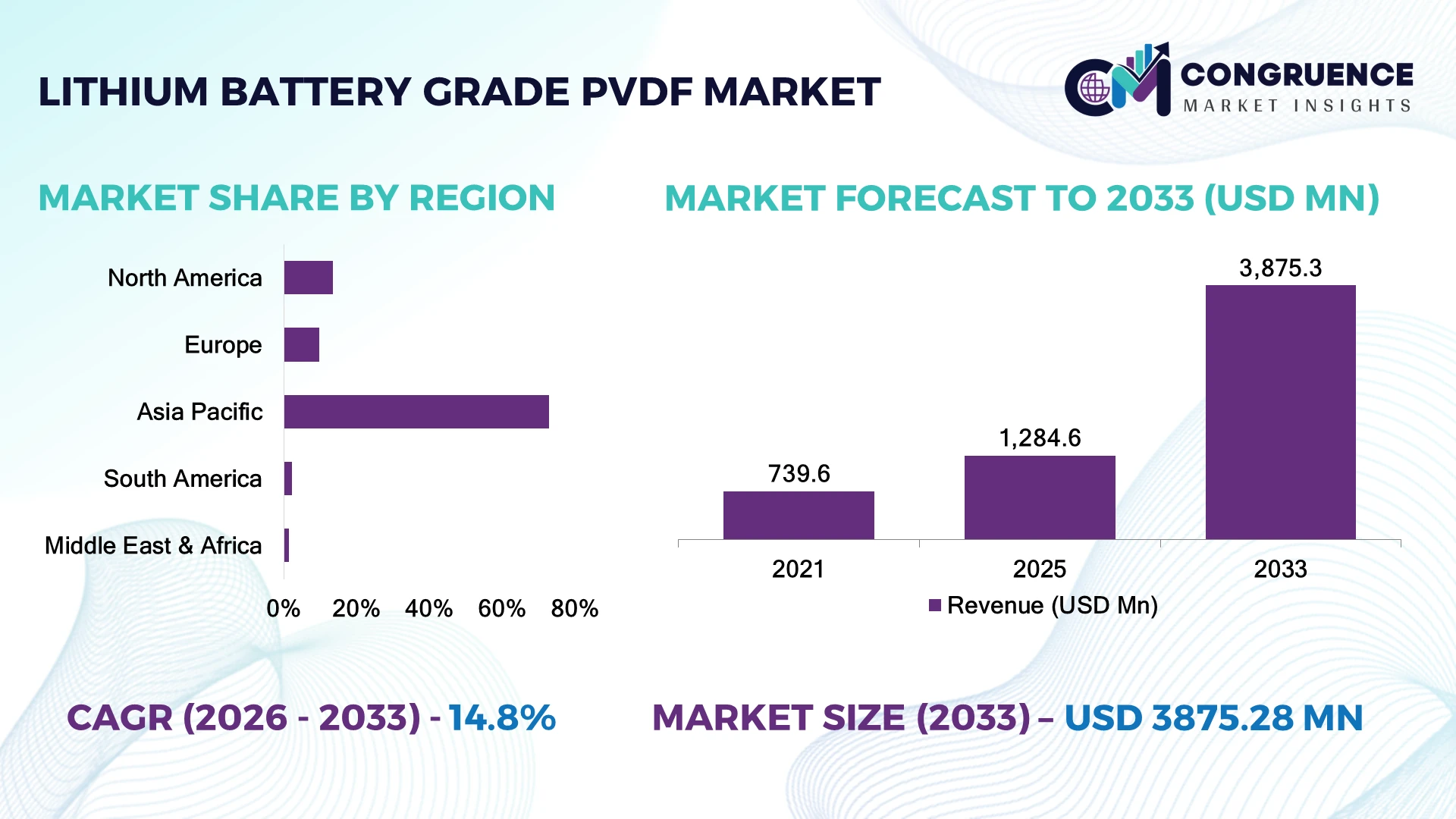

The Global Lithium Battery Grade PVDF Market was valued at USD 1,284.6 Million in 2025 and is anticipated to reach a value of USD 3,875.3 Million by 2033 expanding at a CAGR of 14.8% between 2026 and 2033. Rapid expansion of lithium-ion battery gigafactories, higher-energy-density cathode technologies, and localized battery material supply chains is accelerating demand for high-purity lithium battery grade PVDF binders.

China remains the dominant country, accounting for approximately 68% of global lithium battery grade PVDF production capacity, supported by integrated battery material ecosystems, large-scale EV manufacturing, and continuous cathode expansion projects. More than 74% of newly commissioned lithium-ion cell production lines in China utilize domestically supplied PVDF materials, while South Korea focuses on premium battery technologies and advanced binder formulations. Ongoing geopolitical supply-chain diversification is encouraging additional PVDF investments across North America and Europe.

Companies securing integrated fluoropolymer production, battery-grade quality consistency, and long-term cathode manufacturer partnerships will strengthen strategic market leadership.

Market Size & Growth: USD 1,284.6 Million in 2025, projected to reach USD 3,875.3 Million by 2033 at a CAGR of 14.8%, driven by global battery gigafactory expansion.

Top Growth Drivers: EV battery production (+38%), energy storage deployment (+29%), cathode manufacturing expansion (+25%).

Short-Term Forecast: By 2028, PVDF processing efficiency improves 21% through advanced polymerization and production automation.

Emerging Technologies: High-purity PVDF, solvent optimization, and AI-driven process control improve material consistency.

Regional Leaders: Asia-Pacific exceeds USD 2,500 Million, Europe approaches USD 540 Million, North America surpasses USD 490 Million through battery localization.

Consumer/End-User Trends: Nearly 71% of new battery plants prioritize locally sourced battery-grade binders.

Pilot/Case Example: A 2026 gigafactory optimization program reduced electrode coating defects by 19% using advanced PVDF formulations.

Competitive Landscape: Leading suppliers control approximately 58% market share, led by Arkema, Solvay, Kureha, Dongyue Group, and Sinochem Lantian.

Regulatory & ESG Impact: Closed-loop solvent recovery reduces manufacturing emissions by approximately 23%.

Investment & Funding: More than USD 4.2 Billion supports PVDF capacity expansion and battery material integration.

Innovation & Future Outlook: Next-generation ultra-high-purity PVDF and localized supply chains are strengthening battery manufacturing resilience.

The lithium battery grade PVDF market is becoming central to electric vehicles, stationary energy storage, and high-performance lithium-ion batteries where binder stability directly influences electrode durability and charging performance. Nearly 65% of newly commissioned cathode manufacturing facilities now specify advanced battery-grade PVDF formulations. Continued localization of battery material production and integrated fluoropolymer manufacturing is reinforcing supply-chain resilience, leading into the strategic market discussion.

The lithium battery grade PVDF market has become strategically important as battery manufacturers seek secure access to critical materials supporting higher energy density, longer cycle life, and localized production. Supply-chain restructuring, industrial policy incentives, and rapid gigafactory expansion are encouraging battery producers to establish regional sourcing strategies while reducing dependence on imported specialty polymers. Material security has become as important as production scale for long-term competitiveness.

Advanced high-purity PVDF formulations improve electrode adhesion by approximately 18% compared with conventional grades while reducing coating defects by nearly 16% during high-speed manufacturing. Asia-Pacific continues leading large-scale PVDF production and battery material integration, whereas North America and Europe are accelerating localized manufacturing through new battery supply-chain investments. Over the next two to three years, localized binder production, automated quality monitoring, and next-generation polymer engineering are expected to significantly improve production consistency and supply resilience.

A practical example is the integration of dedicated PVDF production alongside cathode manufacturing facilities to shorten logistics cycles and improve quality control. Manufacturers are expanding fluoropolymer capacity, forming long-term supply agreements with battery producers, and investing in advanced purification technologies. Companies combining material purity, manufacturing scale, and regional supply integration will secure durable competitive advantages across the rapidly evolving lithium-ion battery ecosystem.

Rapid expansion of lithium-ion battery manufacturing capacity is the primary driver for lithium battery grade PVDF demand, as high-performance binders remain essential for electrode integrity and cycle stability. More than 76% of newly commissioned battery production lines now utilize high-purity PVDF binders, while advanced coating processes improve electrode consistency by approximately 22%. China continues expanding integrated cathode and binder manufacturing through large-scale battery material investments, shortening procurement cycles and improving production efficiency. This structural shift is strengthening localized supply ecosystems. Manufacturers are increasing fluoropolymer production capacity, investing in purification technologies, and establishing long-term supply agreements with cathode producers. A critical strategic advantage now lies in vertically integrated production that ensures material quality while reducing supply-chain disruptions.

Production of lithium battery grade PVDF depends heavily on fluorinated raw materials, specialty chemical processing, and stringent purification requirements that increase manufacturing complexity. Raw materials account for nearly 47% of production costs, while fluctuations in fluorspar and fluorochemical availability continue influencing procurement strategies. Tight environmental regulations governing fluorochemical production in China have increased operational compliance requirements for manufacturers. These pressures directly affect production planning, inventory management, and contract pricing across battery supply chains. Companies are reducing exposure by localizing fluorochemical sourcing, securing long-term supply contracts, expanding recycling initiatives, and investing in process optimization technologies that improve material utilization while stabilizing production costs.

Next-generation lithium-ion batteries featuring high-nickel cathodes, silicon-enhanced anodes, and solid-state development are creating new opportunities for specialized battery grade PVDF formulations. Nearly 41% of advanced battery development programs now require customized PVDF binders with enhanced electrochemical stability, while optimized polymer formulations improve electrode adhesion by approximately 19%. South Korea continues investing in premium battery materials supporting next-generation cell technologies. Manufacturers are expanding R&D programs, collaborating with battery producers, and developing application-specific PVDF grades tailored for emerging battery chemistries. A significant strategic opportunity lies in customized binder formulations that improve manufacturing yields while supporting higher-energy-density battery platforms.

Maintaining consistent battery-grade purity across rapidly expanding production capacity remains a significant long-term execution challenge. Approximately 32% of newly commissioned facilities require additional qualification periods before achieving full commercial supply, while high-purity processing increases production complexity by nearly 18%. Stringent quality requirements from global battery manufacturers demand exceptional consistency across every production batch. Variations in polymer molecular weight distribution and impurity levels directly affect battery performance and qualification timelines. Companies must strengthen automated quality control, invest in advanced purification systems, standardize manufacturing processes, and deepen technical collaboration with battery producers to maintain long-term competitiveness within increasingly demanding global supply chains.

Localized Supply Expansion Battery manufacturers now source approximately 69% of battery-grade PVDF through regional suppliers to improve supply resilience and reduce logistics exposure. Government-backed battery localization programs are accelerating domestic material production. Producers are expanding integrated fluoropolymer facilities, strengthening long-term supply partnerships, and increasing regional manufacturing capacity.

Higher Purity Material Focus Ultra-high-purity PVDF adoption has increased by approximately 27%, while advanced purification technologies reduce electrode coating defects by nearly 18%. Premium battery manufacturers are tightening material qualification standards for high-energy cells. Companies continue investing in automated purification systems, digital quality monitoring, and precision polymer processing to strengthen product consistency.

Integrated Cathode Partnerships More than 46% of new PVDF expansion projects are aligned with cathode manufacturing facilities, reducing raw material logistics and improving production coordination. China's integrated battery ecosystem continues accelerating this operational model. Manufacturers are expanding joint development programs and vertically integrated production strategies to improve supply efficiency and customer responsiveness.

Process Automation Accelerates AI-assisted production monitoring improves polymerization consistency by approximately 21% while reducing manufacturing deviations by nearly 17%. Rising battery quality requirements are driving wider deployment of intelligent manufacturing technologies. Producers are implementing advanced process control, predictive maintenance, and digital production analytics to improve operational stability and support large-scale battery material manufacturing.

Homopolymer PVDF represents the leading segment, accounting for approximately 63% of global lithium battery grade PVDF consumption because of its superior chemical stability, excellent binder strength, and proven compatibility with NCM, NCA, and LFP cathode materials. Its consistent electrochemical performance and ease of integration into large-scale electrode manufacturing make it the preferred choice for high-volume battery production. Copolymer PVDF is the fastest-growing segment as battery manufacturers increasingly adopt high-energy-density cells requiring greater flexibility, electrolyte affinity, and enhanced adhesion. Advanced copolymer formulations improve coating uniformity by nearly 18% while supporting longer battery cycle life, encouraging broader adoption in premium electric vehicle batteries.

Modified PVDF grades and specialty formulations continue expanding across silicon-rich anodes and next-generation battery chemistries where customized binder performance is becoming increasingly important. Manufacturers are investing in polymer engineering, production capacity expansion, and collaborative product development with battery cell producers. As battery technologies evolve, investment priorities are steadily shifting toward high-purity specialty PVDF grades capable of improving manufacturing yields while supporting advanced lithium-ion battery architectures.

According to the U.S. Department of Energy's Argonne National Laboratory during 2025 battery materials research activities, optimized PVDF binder formulations significantly improved electrode mechanical integrity and manufacturing consistency for advanced lithium-ion battery cells.

Cathode binder applications dominate the lithium battery grade PVDF market with an estimated 81% share, supported by PVDF's outstanding adhesion, chemical resistance, and long-term electrochemical stability. As lithium-ion battery production continues expanding, cathode manufacturing remains the largest consumer of battery-grade PVDF. Separator coating applications are the fastest-growing segment as battery manufacturers prioritize higher thermal stability and enhanced electrolyte wettability for improved battery safety. Advanced separator coating technologies increase thermal resistance by approximately 20%, strengthening their adoption across high-performance electric vehicle and energy storage batteries.

Electrolyte membranes and emerging specialty battery interface applications continue gaining strategic relevance alongside solid-state battery research, although commercial deployment remains comparatively limited. Companies are expanding automated coating technologies, integrating advanced material qualification systems, and developing customized PVDF formulations tailored to evolving battery designs. Commercial demand is increasingly concentrating on applications that enhance manufacturing efficiency, battery durability, and production consistency across next-generation lithium-ion cells.

According to technical findings published through the U.S. Department of Energy's Oak Ridge National Laboratory during 2025 battery manufacturing programs, optimized binder and separator coating technologies demonstrated measurable improvements in electrode durability and production consistency.

Electric vehicle manufacturers account for approximately 54% of lithium battery grade PVDF demand due to continuous battery gigafactory expansion, increasing EV production volumes, and widespread adoption of high-energy-density lithium-ion cells. Energy storage system manufacturers represent the fastest-growing end-user segment as grid-scale renewable integration accelerates globally. Battery materials supplied to stationary energy storage projects have increased by approximately 28%, reflecting stronger demand for durable binders capable of supporting long-life battery systems. Consumer electronics continue providing stable demand, while industrial battery manufacturers are adopting premium PVDF formulations for material handling equipment and specialized industrial applications.

Manufacturers are strengthening long-term supply agreements with automotive battery producers, expanding localized production capacity, and developing customized PVDF formulations optimized for different battery chemistries. Strategic partnerships with automotive OEMs, battery cell manufacturers, and cathode suppliers are becoming increasingly important as buyers prioritize consistent quality, qualified supply chains, and technical collaboration for next-generation battery platforms.

According to the International Energy Agency's 2025 Global EV Outlook, electric vehicles remained the largest consumer of lithium-ion batteries, reinforcing EV manufacturers as the primary end-user driving demand for battery-grade PVDF binders and advanced electrode materials.

Asia-Pacific accounted for the largest market share at 72.8% in 2025 however, North America is expected to register the fastest growth, expanding at a CAGR of 16.3% between 2026 and 2033.

Battery Supply Chain Localization Accelerates Material Investments

North America accounted for approximately 13.6% of the global Lithium Battery Grade PVDF market in 2025, supported by rapid expansion of domestic battery manufacturing and government-backed critical mineral strategies. Large-scale gigafactory construction across the United States is driving localized demand for battery-grade fluoropolymers, while battery producers increasingly seek regional suppliers to reduce import dependency. More than 65% of announced battery manufacturing projects now emphasize localized material procurement. Strategic investments in cathode manufacturing, fluorochemical processing, and battery recycling infrastructure are strengthening regional competitiveness. Chemical manufacturers are expanding purification capabilities, entering long-term supply partnerships, and integrating digital quality control systems to satisfy increasingly stringent battery qualification standards.

United States Market Outlook: The United States remains the region's largest market owing to aggressive battery manufacturing expansion supported by the Inflation Reduction Act and large-scale EV investments. More than 35 announced battery gigafactory projects are strengthening domestic demand for high-purity PVDF. Producers are investing in integrated battery material supply chains, localized fluoropolymer production, and advanced quality assurance systems to reduce import dependence while improving long-term supply security.

Localized Battery Materials Strengthen Industrial Independence

Europe represented approximately 9.8% of global demand in 2025 as battery manufacturing localization and industrial decarbonization continue reshaping the regional supply chain. Battery Alliance initiatives and expanding EV manufacturing are encouraging investment across cathode materials, fluoropolymer production, and battery recycling infrastructure. Nearly 58% of planned battery manufacturing projects prioritize regional sourcing of strategic materials to improve supply resilience. Chemical companies are strengthening technical partnerships with battery manufacturers while expanding sustainable production technologies and solvent recovery systems to comply with evolving environmental regulations.

Germany Market Outlook: Germany leads the European market through its advanced automotive manufacturing ecosystem, expanding battery cell production, and strong chemical industry capabilities. Gigafactory investments and cathode material facilities continue driving demand for premium battery-grade PVDF. Manufacturers are focusing on localized production, advanced purification technologies, and collaborative development programs supporting next-generation lithium-ion battery platforms.

Integrated Manufacturing Ecosystems Sustain Global Leadership

Asia-Pacific dominates the global Lithium Battery Grade PVDF market with approximately 72.8% market share, supported by vertically integrated battery material manufacturing, large-scale fluoropolymer production, and global leadership in lithium-ion cell manufacturing. China, South Korea, and Japan collectively account for the majority of global battery production capacity, creating sustained demand for high-purity PVDF. More than 75% of global cathode manufacturing capacity operates within the region, enabling efficient integration between raw materials and battery production. Manufacturers continue expanding polymer purification facilities, automation technologies, and specialty binder production to support advanced battery chemistries.

China Market Outlook: China remains the world's largest producer and consumer of lithium battery grade PVDF due to its extensive battery manufacturing ecosystem and integrated fluorochemical industry. Domestic suppliers support the majority of national cathode production while continuously expanding high-purity PVDF capacity. Strong collaboration between chemical manufacturers and battery producers enables rapid commercialization of advanced binder formulations for high-energy-density battery applications.

Critical Minerals Support Future Battery Materials Growth

South America represents an emerging market supported by its strategic lithium resource base and expanding participation in the global battery materials value chain. Regional governments continue encouraging downstream processing investments to strengthen domestic battery material industries. Approximately 61% of global lithium resources are concentrated within the region, creating long-term opportunities for battery chemical integration. Infrastructure limitations and limited fluoropolymer manufacturing capacity currently constrain broader commercialization, prompting companies to pursue international technology partnerships and phased industrial expansion strategies.

Chile Market Outlook: Chile remains the region's most strategically important market because of its leadership in lithium production and growing emphasis on value-added battery material processing. Government initiatives encourage domestic investment in battery supply chains while international partnerships support chemical processing capabilities. Expansion of lithium conversion facilities creates favorable conditions for future battery-grade PVDF demand as downstream manufacturing gradually develops.

Industrial Diversification Expands Battery Material Investments

The Middle East & Africa market is progressing through industrial diversification strategies, energy transition investments, and growing participation in battery material processing. Countries across the Gulf region are supporting advanced chemical manufacturing while African nations strengthen critical mineral processing capabilities. Approximately 24% of announced industrial diversification projects within regional chemical sectors now include advanced materials or battery-related manufacturing initiatives. International partnerships and infrastructure investments continue improving long-term competitiveness despite limited current PVDF production capacity.

Saudi Arabia Market Outlook: Saudi Arabia is emerging as the region's leading market through large-scale industrial diversification, advanced chemical manufacturing investments, and strategic participation in battery value chains. Government-backed industrial programs encourage downstream specialty chemical production while international collaborations strengthen technology transfer and manufacturing capabilities. Expansion of integrated industrial complexes provides a favorable foundation for future lithium battery material production and regional supply chain development.

Global specialty polymer leaders including Arkema, Kureha, Solvay, Dongyue Group, and Sinochem Lantian compete directly with rapidly expanding Chinese fluoropolymer manufacturers and regional battery material suppliers. The top five companies collectively command approximately 61% of the global lithium battery grade PVDF market. Competition centers on material purity, production scale, localized supply, and long-term battery qualification rather than price alone. Premium suppliers deliver impurity levels below 50 ppm while improving batch consistency by nearly 20%, whereas integrated Chinese producers reduce supply lead times by approximately 25%. Companies are expanding PVDF capacity, integrating upstream fluorochemical production, signing multi-year supply agreements with battery manufacturers, and accelerating customized binder development. The competitive landscape is shifting toward vertically integrated supply chains and localized manufacturing near gigafactories. High capital investment, qualification cycles exceeding 12 months, and stringent purity standards remain major barriers. Success depends on scalable high-purity production, reliable regional supply, and continuous material innovation.

Arkema

Kureha Corporation

Solvay

Dongyue Group

Sinochem Lantian

Shanghai Huayi 3F New Materials

Zhejiang Juhua Co., Ltd.

Shandong Deyi New Material Co., Ltd.

Zhejiang Fotech International Co., Ltd.

Daikin Industries, Ltd.

Gujarat Fluorochemicals Limited

Sinochem International Corporation

3M

High-purity suspension-polymerized PVDF remains the benchmark technology for lithium-ion battery binders because it delivers excellent adhesion, chemical resistance, and electrochemical stability. More than 72% of newly commissioned battery production lines now specify ultra-high-purity PVDF with automated quality monitoring. Advanced purification technologies reduce metallic impurities by nearly 30%, improving electrode consistency and lowering defect rates during high-volume manufacturing. Digital process control and inline particle-size monitoring are becoming standard across premium PVDF production facilities, strengthening supply reliability for gigafactory customers.

Emerging technologies include low-residual-solvent PVDF, tailored copolymer formulations, AI-assisted polymerization control, and advanced molecular weight optimization. Compared with conventional PVDF grades, next-generation binder formulations improve electrode adhesion by approximately 19% while reducing coating defects by nearly 17%. Premium battery manufacturers benefit most because consistent binder performance directly supports longer battery life and faster production qualification. Companies investing in automated purification and customized binder engineering are securing stronger positions with automotive battery manufacturers requiring application-specific material performance.

Between 2026 and 2028, intelligent manufacturing, continuous polymerization systems, and binder formulations designed for silicon-rich anodes and solid-state batteries will reshape the market. Automated quality analytics are expected to improve production efficiency by approximately 18% while reducing material variability across commercial batches. Producers that integrate fluorochemical production, advanced purification technologies, and collaborative battery material development will strengthen long-term competitiveness as next-generation lithium-ion battery platforms continue advancing.

February 2025 – Arkema announced a 15% expansion of PVDF production capacity at its Calvert City, Kentucky facility, supported by an investment of approximately USD 20 million to strengthen North American lithium-ion battery supply. Source: Arkema

March 2026 – Arkema unveiled a 20% expansion of Kynar® PVDF production capacity at its Changshu, China facility, reinforcing supply for electric vehicle batteries, energy storage systems, and advanced manufacturing applications. Source: Arkema

June 2026 – Arkema successfully commissioned its North American PVDF capacity expansion on schedule, increasing output by 15% to strengthen regional supply for EV batteries, semiconductors, and energy storage manufacturers. Source: Arkema

August 2025 – Arkema's Kynar® HSV 900 PVDF binder was recognized for enabling batteries powering more than 10 million electric vehicles, highlighting its established role in commercial LFP battery manufacturing. Source: arkema.com

The report provides comprehensive analysis of the Lithium Battery Grade PVDF Market across major product types, battery applications, end-user industries, and regional markets. It evaluates homopolymer, copolymer, and specialty PVDF formulations used in cathode binders, separator coatings, and emerging battery technologies. Coverage extends across electric vehicles, stationary energy storage, consumer electronics, and industrial battery manufacturing, where nearly 80% of material demand remains concentrated in electrode binder applications.

The study examines market developments across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa while assessing manufacturing capacity, technology innovation, supply-chain localization, and competitive positioning between 2026 and 2033. It highlights deployment trends, material qualification practices, regional production patterns, and strategic investments supporting battery manufacturing expansion. The report enables informed investment planning, capacity expansion decisions, supplier benchmarking, product development, and long-term competitive strategy within the global battery materials ecosystem.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 1,284.6 Million |

|

Market Revenue in 2033 |

USD 3,875.3 Million |

|

CAGR (2026 - 2033) |

14.8% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Arkema, Kureha Corporation, Solvay, Dongyue Group, Sinochem Lantian, Shanghai Huayi 3F New Materials, Zhejiang Juhua Co., Ltd., Shandong Deyi New Material Co., Ltd., Zhejiang Fotech International Co., Ltd., Daikin Industries, Ltd., Gujarat Fluorochemicals Limited, Sinochem International Corporation, 3M |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |