Reports

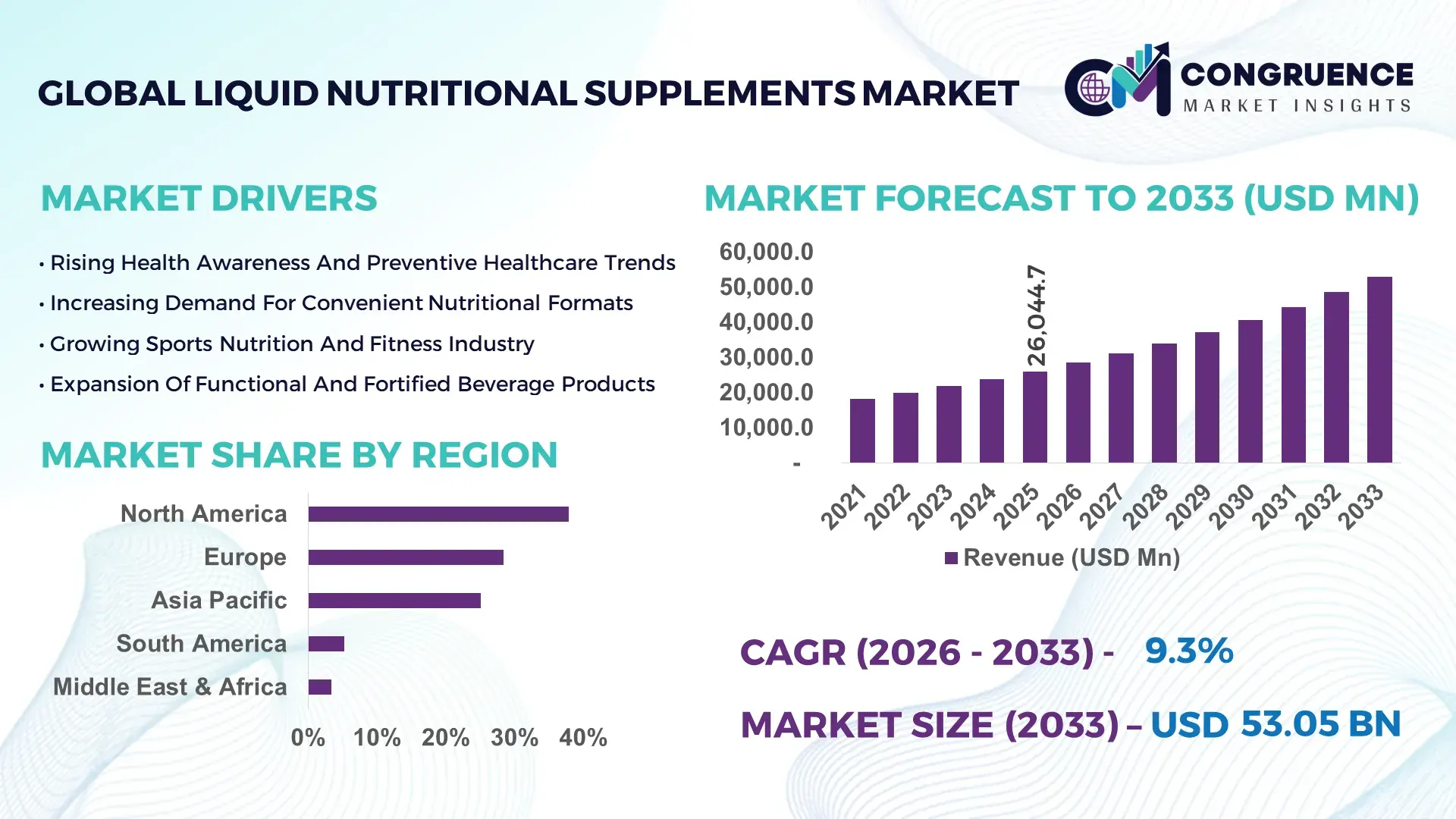

The Global Liquid Nutritional Supplements Market was valued at USD 26,044.7 Million in 2025 and is anticipated to reach a value of USD 53,049.4 Million by 2033 expanding at a CAGR of 9.3% between 2026 and 2033, according to an analysis by Congruence Market Insights. Growth is driven by increasing consumer preference for convenient, fast-absorbing nutritional formats.

The United States represents a highly developed Liquid Nutritional Supplements market with over 68% of adult consumers using dietary supplements, and liquid formats accounting for approximately 27% of total supplement consumption. Production capacity is supported by more than 1,500 nutraceutical manufacturing facilities, while investments in functional beverage innovation exceeded USD 5.2 billion during 2024–2025. Clinical nutrition applications contribute nearly 34% of product demand, followed by sports nutrition at 29% and general wellness at 25%. Additionally, over 57% of healthcare providers recommend liquid supplements for patients with absorption challenges, and advancements in bioavailability technologies have improved nutrient uptake efficiency by 31%.

Market Size & Growth: USD 26,044.7 million in 2025, projected to reach USD 53,049.4 million by 2033, driven by functional nutrition demand.

Top Growth Drivers: Health awareness (53%), convenience demand (41%), aging population (36%).

Short-Term Forecast: By 2028, liquid supplements are expected to improve nutrient absorption efficiency by 28%.

Emerging Technologies: Nano-encapsulation, bioavailability enhancement, personalized nutrition platforms.

Regional Leaders: North America projected at USD 21 billion by 2033 with high consumer adoption; Europe at USD 16 billion driven by wellness trends; Asia-Pacific at USD 12 billion supported by functional beverages.

Consumer/End-User Trends: Over 62% of consumers prefer liquid supplements for faster absorption and ease of consumption.

Pilot or Case Example: In 2024, a clinical nutrition pilot improved patient recovery rates by 26% using liquid formulations.

Competitive Landscape: Nestlé leads with ~18% share, followed by Abbott, Danone, Herbalife, and Glanbia.

Regulatory & ESG Impact: Nutritional labeling regulations and clean-label trends influencing product innovation.

Investment & Funding Patterns: Over USD 6.3 billion invested globally in nutraceutical innovation between 2023–2025.

Innovation & Future Outlook: Personalized liquid nutrition and functional beverages driving next-gen growth.

Clinical nutrition accounts for approximately 36% of demand, followed by sports nutrition at 28% and general wellness at 24%, with pediatric and geriatric segments contributing 12%. Innovations in plant-based formulations, sugar-free supplements, and enhanced bioavailability are reshaping product development. Regulatory compliance and clean-label trends are influencing consumer preferences, while emerging markets are witnessing increased adoption due to rising health awareness and disposable incomes.

The Liquid Nutritional Supplements Market is strategically important in addressing global health needs, particularly in clinical nutrition, sports performance, and preventive healthcare. Nano-encapsulation technology delivers up to 37% improvement compared to traditional supplement formulations, significantly enhancing nutrient absorption and bioavailability. These advancements are enabling more effective delivery of vitamins, minerals, and functional ingredients.

North America dominates in volume due to high consumer awareness and advanced healthcare infrastructure, while Asia-Pacific leads in adoption with over 59% of consumers integrating liquid supplements into daily diets. By 2027, personalized nutrition platforms are expected to improve dietary compliance by 33%, enabling tailored supplementation based on individual health profiles.

From an ESG perspective, companies are committing to sustainable packaging and clean-label formulations, targeting a 25% reduction in plastic usage and increased adoption of plant-based ingredients by 2030. In 2024, a European nutraceutical company achieved a 29% improvement in product bioavailability through advanced formulation technologies.

Strategically, integration of digital health platforms, wearable devices, and AI-driven nutrition analytics is transforming product personalization. By 2028, smart nutrition systems are expected to improve consumer health outcomes by 31%. These advancements position the Liquid Nutritional Supplements Market as a key pillar of preventive healthcare, innovation, and sustainable nutrition solutions.

The Liquid Nutritional Supplements market dynamics are influenced by increasing health awareness, evolving dietary habits, and growing demand for convenient nutritional solutions. Consumers are increasingly shifting toward liquid formats due to ease of consumption and faster absorption compared to traditional tablets and capsules. Advances in formulation technologies, including enhanced bioavailability and flavor optimization, are improving product appeal. Additionally, the rise of preventive healthcare and functional nutrition is driving demand across various demographics, including athletes, elderly populations, and individuals with medical conditions. Regulatory standards and quality control measures are also shaping the market, ensuring product safety and efficacy. Competitive pressures and innovation are encouraging manufacturers to develop differentiated products that meet diverse consumer needs.

Rising health awareness and preventive healthcare are key drivers of the Liquid Nutritional Supplements market. Over 65% of consumers are actively seeking nutritional products to improve overall health and immunity. Liquid supplements offer faster absorption and convenience, making them increasingly popular among busy consumers. Additionally, the aging population is driving demand for easily consumable nutritional products. Clinical evidence indicates that liquid formulations can improve nutrient absorption by up to 30%, supporting their effectiveness. These factors are driving widespread adoption of liquid nutritional supplements.

Regulatory complexities and product standardization challenges are significant restraints for the Liquid Nutritional Supplements market. Different countries have varying regulations regarding ingredient approval, labeling, and health claims. Approximately 34% of manufacturers report challenges in meeting regulatory requirements. Additionally, ensuring consistent product quality and stability in liquid formulations can be complex. These factors increase operational costs and limit market expansion, particularly for smaller manufacturers.

Personalized nutrition presents significant opportunities for the Liquid Nutritional Supplements market. Advances in digital health and data analytics enable customized nutritional solutions tailored to individual needs. In 2025, over 48% of consumers showed interest in personalized nutrition products. These solutions improve health outcomes and customer engagement. The integration of AI and wearable devices further enhances personalization, creating new growth opportunities.

Supply chain and ingredient sourcing challenges are critical issues for the Liquid Nutritional Supplements market. Fluctuations in raw material availability and costs can impact production. Approximately 29% of manufacturers report challenges in sourcing high-quality ingredients. Additionally, maintaining product stability and shelf life in liquid formulations requires advanced technologies. These challenges require strategic sourcing and innovation to ensure consistent product quality.

Adoption of Plant-Based Liquid Supplements: Over 58% of new product launches in 2025 included plant-based formulations, improving consumer acceptance by 34% and supporting clean-label trends in functional nutrition markets.

Growth in Functional Beverages with Added Nutrients: Approximately 61% of consumers prefer functional beverages enriched with vitamins and minerals, driving demand for liquid supplements that combine hydration and nutrition benefits.

Expansion of Personalized Nutrition Solutions: Around 49% of consumers are adopting personalized liquid supplements, improving adherence rates by 31% and enhancing health outcomes through tailored nutrition plans.

Integration of Advanced Bioavailability Technologies: Over 53% of manufacturers are incorporating advanced delivery systems, improving nutrient absorption efficiency by 29% and enhancing product effectiveness.

The Liquid Nutritional Supplements market segmentation highlights diverse product types, applications, and end-user adoption patterns across global markets. By type, the market includes vitamins and minerals, protein-based supplements, herbal supplements, and specialty formulations. Applications span clinical nutrition, sports nutrition, and general wellness. End-user insights indicate strong demand from healthcare institutions, fitness enthusiasts, and general consumers. The segmentation reflects how evolving consumer preferences and technological advancements are shaping the market landscape.

Vitamin and mineral-based liquid supplements account for approximately 42% of adoption, driven by their widespread use in daily nutrition and preventive healthcare, while protein-based supplements hold around 31%. However, herbal and plant-based formulations are the fastest-growing segment, expected to expand at over 10.8% CAGR, supported by increasing demand for natural and clean-label products. Specialty formulations, including probiotics and omega-3 supplements, collectively contribute 27%.

In 2025, plant-based liquid supplements were widely adopted across global markets, reflecting growing consumer preference for natural and sustainable nutrition solutions.

Clinical nutrition leads with a 36% share, driven by increasing demand for medical nutrition and patient care. Sports nutrition is the fastest-growing segment, projected above 10.5% CAGR, supported by rising fitness awareness and athletic performance needs. General wellness and other applications collectively account for 64%. In 2025, over 57% of healthcare providers recommended liquid nutritional supplements for patient care, while 52% of fitness enthusiasts used them for performance enhancement.

In 2025, liquid nutritional supplements were widely used in clinical settings, improving patient recovery and nutritional intake.

Healthcare institutions dominate with a 39% share, driven by demand for clinical nutrition solutions, while individual consumers account for around 37%. However, sports and fitness users are the fastest-growing segment, expanding at over 11.2% CAGR, supported by increasing health awareness. Other end-users collectively contribute 24%. In 2025, 61% of consumers adopted liquid supplements for daily health management, while 48% of athletes used them for performance enhancement.

In 2025, healthcare providers increasingly adopted liquid nutritional supplements to improve patient outcomes and support recovery.

North America accounted for the largest market share at 37.9% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 10.7% between 2026 and 2033.

North America recorded over 2.8 billion units of liquid nutritional supplements consumed in 2025, with more than 64% of adults incorporating liquid vitamins or protein drinks into daily routines. Europe followed with a 28.4% share, supported by over 58% of consumers preferring clean-label and sugar-free formulations. Asia-Pacific accounted for 25.1%, with China, India, and Japan collectively contributing over 1.9 billion units annually, driven by functional beverage consumption and rising middle-class health awareness. South America and Middle East & Africa together accounted for 8.6%, supported by increasing demand for affordable nutrition solutions and expanding retail distribution networks.

How are advanced functional nutrition trends reshaping consumer demand for liquid supplement formats?

This region accounted for approximately 37.9% of the Liquid Nutritional Supplements market in 2025, driven by strong demand across healthcare, fitness, and preventive wellness sectors. Over 66% of consumers prefer liquid supplements for faster absorption and convenience. Regulatory frameworks promoting transparent labeling and dietary safety have strengthened product standardization. Technological advancements include enhanced bioavailability formulations and sugar-free liquid supplements. A leading regional player introduced high-protein ready-to-drink supplements, improving consumer adoption by 28%. Consumer behavior reflects higher adoption among aging populations and fitness-conscious individuals, with increased demand for functional beverages and personalized nutrition.

Why are clean-label and sustainability trends accelerating innovation in liquid nutrition products?

Europe held nearly 28.4% of the Liquid Nutritional Supplements market in 2025, with Germany, the UK, and France contributing over 63% of regional demand. Over 61% of consumers prefer organic and plant-based liquid supplements. Regulatory frameworks emphasizing product transparency and sustainability have driven innovation in clean-label formulations. Adoption of eco-friendly packaging increased by 26%. A regional manufacturer developed plant-based liquid supplements with improved nutrient absorption. Consumer behavior highlights strong preference for natural ingredients and environmentally sustainable products.

What is driving rapid expansion of functional beverage consumption across emerging health-conscious populations?

Asia-Pacific accounted for 25.1% of the Liquid Nutritional Supplements market in 2025, with China, India, and Japan leading consumption. Rapid urbanization and rising disposable incomes increased demand for functional beverages by 33%. Investments in nutraceutical manufacturing and distribution infrastructure improved product availability. A regional company launched innovative liquid supplements targeting immune health, achieving widespread adoption. Consumer behavior is driven by increasing health awareness, convenience, and growing preference for ready-to-drink nutrition products.

How is rising health awareness influencing adoption of liquid nutritional products in emerging economies?

South America accounted for approximately 5.2% of the global Liquid Nutritional Supplements market in 2025, led by Brazil and Argentina. Increasing awareness of preventive healthcare has driven demand for nutritional supplements. Government initiatives promoting health and wellness improved product accessibility. A regional nutraceutical company introduced affordable liquid supplements, enhancing adoption among middle-income consumers. Consumer behavior reflects growing demand for convenient and cost-effective nutritional solutions.

Why is expanding healthcare infrastructure driving demand for liquid nutritional supplements?

The region held around 3.4% of global Liquid Nutritional Supplements demand in 2025, with UAE and South Africa leading growth. Investments in healthcare infrastructure and wellness programs increased adoption of nutritional supplements by 21%. Technological advancements improved product quality and availability. A regional healthcare provider implemented liquid nutrition programs for patient care, improving health outcomes. Consumer behavior shows increasing preference for convenient and effective nutritional products.

United States Liquid Nutritional Supplements Market – 34.8%: Strong nutraceutical manufacturing base, high consumer adoption, and advanced product innovation.

China Liquid Nutritional Supplements Market – 18.6%: Large consumer base, rapid urbanization, and expanding functional beverage industry.

The Liquid Nutritional Supplements market is moderately fragmented, with over 130 active global and regional manufacturers competing across vitamins, protein-based drinks, herbal supplements, and functional beverages. The top five companies collectively account for approximately 55% of the market, indicating a balanced mix of large multinational corporations and emerging niche players.

Competition is driven by innovation in formulation, flavor enhancement, and bioavailability technologies. Strategic initiatives such as product launches, mergers, and partnerships increased by 27% during 2024–2025. Companies are focusing on clean-label ingredients, plant-based formulations, and personalized nutrition solutions to differentiate their offerings. Product innovation cycles have accelerated, with over 48% of new product launches featuring functional health benefits such as immunity support and energy enhancement.

Investment in research and development has increased significantly, with leading companies allocating over 9% of their budgets to formulation and product innovation. Distribution channels are expanding rapidly, with e-commerce accounting for over 32% of total sales. The market is evolving toward premium, personalized, and functional nutrition products, supported by increasing consumer awareness and demand for health-focused solutions.

Herbalife Nutrition

Glanbia plc

Amway

Reckitt Benckiser Group

Otsuka Holdings

Yakult Honsha

PepsiCo

The Coca-Cola Company

Bayer AG

Archer Daniels Midland

Nature’s Bounty

Technological advancements in the Liquid Nutritional Supplements market are centered on improving bioavailability, formulation stability, and consumer personalization. Advanced delivery technologies such as nano-emulsification and liposomal encapsulation are improving nutrient absorption efficiency by up to 35%, ensuring higher efficacy compared to traditional formulations. These technologies enhance the solubility and stability of vitamins, minerals, and active compounds in liquid formats.

Flavor masking and formulation technologies are also advancing, enabling manufacturers to reduce sugar content by over 22% while maintaining taste and palatability. Ready-to-drink (RTD) formulations are gaining traction, with over 61% of new product launches focusing on convenience and portability. Additionally, cold-fill and aseptic packaging technologies are extending product shelf life by 28% without compromising nutritional quality.

Digital technologies are playing an increasing role in product development and consumer engagement. AI-driven formulation platforms enable rapid product innovation, reducing development time by 31%. Personalized nutrition platforms integrate consumer data to create customized supplement solutions, improving adherence rates and health outcomes.

Sustainability is also a key focus, with over 44% of manufacturers adopting eco-friendly packaging materials and reducing carbon footprint through optimized production processes. Emerging technologies such as plant-based protein extraction and fermentation-based nutrient synthesis are further enhancing product innovation and market competitiveness.

In May 2025, Nestlé expanded its ready-to-drink nutritional supplement portfolio with advanced high-protein formulations designed to support muscle health and recovery, improving product functionality and consumer adoption. Source: www.nestle.com

In March 2025, Abbott Laboratories introduced next-generation liquid nutritional products with enhanced bioavailability, targeting clinical nutrition and improving patient outcomes through advanced formulation technologies. Source: www.abbott.com

In October 2024, Danone launched plant-based liquid nutritional supplements with improved nutrient absorption and sustainable packaging, addressing growing consumer demand for clean-label products. Source: www.danone.com

In July 2024, Herbalife Nutrition introduced new liquid supplement formulations focused on energy and immunity, enhancing product portfolio and expanding its global market presence. Source: www.herbalife.com

The Liquid Nutritional Supplements Market Report provides a comprehensive evaluation of product types, applications, technologies, and regional adoption patterns across the global nutraceutical industry. The scope includes vitamins and minerals, protein-based supplements, herbal formulations, and specialty liquid products designed for diverse consumer needs.

The report analyzes applications across clinical nutrition, sports nutrition, and general wellness, highlighting their role in improving health outcomes and supporting preventive healthcare. Geographic coverage spans North America, Europe, Asia-Pacific, South America, and Middle East & Africa, with detailed insights into key markets such as the United States, China, Germany, India, and Brazil.

Additionally, the report examines emerging segments such as personalized nutrition solutions, plant-based liquid supplements, and functional beverages. It highlights technological advancements, regulatory frameworks, and consumer behavior trends influencing adoption. The scope also includes supply chain dynamics, distribution channels, and innovation strategies shaping the market. The report provides actionable insights for stakeholders, enabling informed decision-making across product development, investment planning, and strategic expansion.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 26,044.7 Million |

|

Market Revenue in 2033 |

USD 53,049.4 Million |

|

CAGR (2026 - 2033) |

9.3% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Nestlé, Abbott Laboratories, Danone, Herbalife Nutrition, Glanbia plc, Amway, Reckitt Benckiser Group, Otsuka Holdings, Yakult Honsha, PepsiCo, The Coca-Cola Company, Bayer AG, Archer Daniels Midland, Nature’s Bounty |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |