Reports

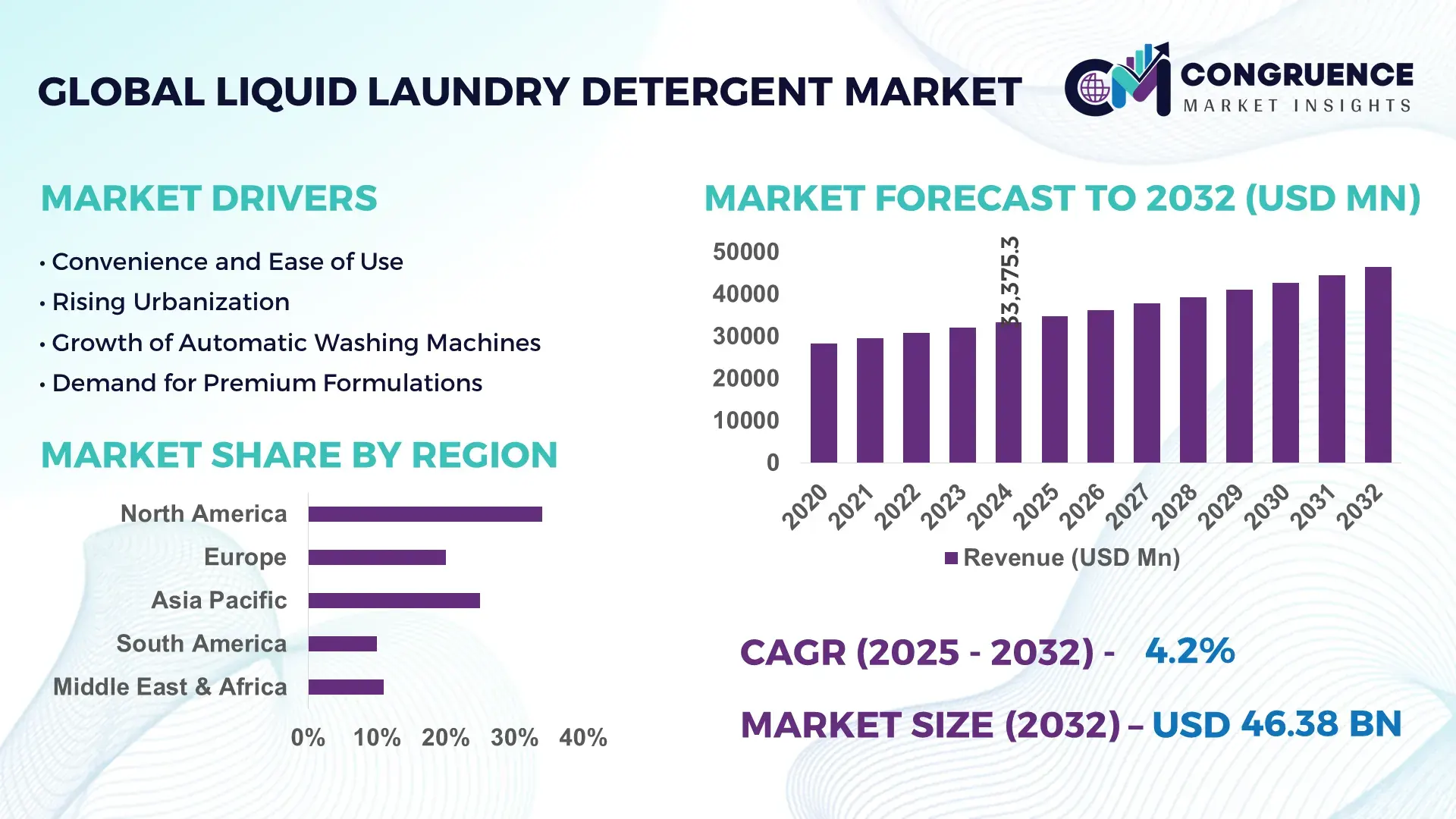

The Global Liquid Laundry Detergent Market was valued at USD 33375.26 Million in 2024 and is anticipated to reach a value of USD 46383.8 Million by 2032 expanding at a CAGR of 4.2% between 2025 and 2032. Growth is primarily supported by rising penetration of automatic washing machines and increasing consumer preference for high-efficiency, low-residue liquid formulations.

The United States represents the most dominant national market for liquid laundry detergents, supported by large-scale production capacity and sustained capital investment by multinational FMCG companies. The country hosts over 120 commercial detergent manufacturing facilities, with annual liquid detergent output exceeding 5.2 million metric tons. In 2024, capital investments in detergent production and packaging automation surpassed USD 1.1 billion, largely focused on concentrated and cold-water-effective formulations. Liquid detergents account for approximately 68% of household laundry detergent consumption in the U.S., driven by widespread use across residential, hospitality, healthcare, and commercial laundry applications. Advanced enzymatic blends, bio-based surfactants, and smart dosing technologies have seen accelerated adoption, with more than 40% of newly launched products integrating sustainability-focused chemical innovations.

Market Size & Growth: Valued at USD 33375.26 Million in 2024, projected to reach USD 46383.8 Million by 2032 at a CAGR of 4.2%, supported by increased adoption of liquid detergents in high-efficiency washing systems.

Top Growth Drivers: Automatic washing machine penetration (62%), shift toward concentrated formulations (48%), growth in urban households (37%).

Short-Term Forecast: By 2028, formulation efficiency is expected to improve by nearly 18%, reducing per-wash detergent consumption.

Emerging Technologies: Enzyme-optimized cold-water formulations, bio-based surfactants, and smart-cap dosing systems.

Regional Leaders: North America projected at USD 14200 Million by 2032 with premium product adoption; Europe at USD 11850 Million driven by eco-label compliance; Asia-Pacific at USD 16100 Million supported by urban consumption growth.

Consumer/End-User Trends: Household users dominate demand, with rising preference for fragrance-free, skin-sensitive, and sustainable liquid variants.

Pilot or Case Example: In 2024, a U.S.-based manufacturing pilot reduced water usage in liquid detergent production by 22% through closed-loop processing.

Competitive Landscape: Procter & Gamble holds approximately 34% share, followed by Unilever, Henkel, Church & Dwight, and Reckitt.

Regulatory & ESG Impact: Stricter wastewater discharge norms and biodegradable ingredient mandates are accelerating reformulation initiatives.

Investment & Funding Patterns: Over USD 3.4 billion invested globally during 2023–2024 in capacity expansion, green chemistry, and smart packaging.

Innovation & Future Outlook: Growth of ultra-concentrated liquids, refill-based distribution models, and AI-assisted formulation design is shaping future market evolution.

The Liquid Laundry Detergent Market continues to evolve across household, commercial laundry, hospitality, and healthcare sectors, which together contribute over 80% of total consumption. Household applications account for nearly 60% of demand, followed by commercial laundries at 18% and institutional users at 12%. Recent product innovations emphasize low-temperature cleaning efficacy, hypoallergenic formulations, and biodegradable surfactants to comply with tightening environmental regulations. Economic factors such as rising disposable income in Asia-Pacific and premiumization trends in North America and Europe are influencing regional consumption patterns. Looking ahead, growth will be driven by refill solutions, concentrated formats, and integration of sustainability metrics into product development and procurement strategies.

The Liquid Laundry Detergent Market holds strong strategic relevance within the global home and fabric care industry due to its alignment with efficiency, sustainability, and technology-led consumption shifts. Liquid formats now account for over 60% of detergent usage in fully automatic washing machines worldwide, reflecting operational compatibility and dosing accuracy advantages. From a strategic standpoint, concentrated liquid detergent technology delivers approximately 30% improvement in cleaning efficiency compared to traditional powder formulations, while reducing packaging weight by nearly 25%. Regionally, Asia-Pacific dominates in volume consumption driven by population density and urbanization, while North America leads in adoption, with over 70% of households using liquid detergents as their primary laundry solution.

Over the short term, by 2027, AI-enabled formulation optimization and smart dosing systems are expected to cut per-wash chemical usage by nearly 20%, improving cost efficiency and reducing environmental load. ESG commitments are increasingly shaping corporate strategies, with leading manufacturers committing to 50% recycled plastic content in detergent bottles by 2030 and achieving water-use reductions of 30% across production facilities. In 2024, the United States achieved a 22% reduction in manufacturing water consumption through closed-loop processing and digital monitoring initiatives deployed across large detergent plants. Looking forward, the Liquid Laundry Detergent Market is positioned as a pillar of resilience, regulatory compliance, and sustainable growth, supporting evolving consumer expectations while enabling scalable, environmentally responsible production pathways.

The increasing adoption of automatic and semi-automatic washing machines is a primary driver of the Liquid Laundry Detergent Market. Globally, automatic washing machine penetration exceeded 55% of urban households in 2024, with liquid detergents preferred in over two-thirds of these machines due to faster dissolution and reduced fabric residue. High-efficiency washers require low-sudsing, concentrated detergents, a requirement best met by liquid formats. In Asia-Pacific alone, more than 45 million new automatic washing machines were installed between 2022 and 2024, directly expanding liquid detergent usage. Additionally, liquid detergents support cold-water washing, enabling energy savings of up to 35% per cycle, reinforcing their relevance as appliance technology and energy-efficiency standards advance.

The Liquid Laundry Detergent Market faces restraints related to volatility in raw material prices and increasingly stringent chemical regulations. Key inputs such as surfactants, enzymes, and fragrances are derived from petrochemical or agricultural feedstocks, both of which experienced price fluctuations exceeding 20% during 2023–2024. Compliance with regulations restricting phosphates, microplastics, and non-biodegradable ingredients increases formulation complexity and testing costs. In the European Union, detergent compliance testing can add up to 12% to product development timelines. Smaller manufacturers are particularly affected, as reformulation and certification require specialized expertise and capital investment, limiting their ability to scale or compete with larger, vertically integrated players.

Sustainable packaging and refill-based distribution models present a significant opportunity for the Liquid Laundry Detergent Market. Refill pouches and concentrated liquids can reduce plastic usage by up to 70% per unit compared to traditional rigid bottles. In 2024, over 35% of urban consumers in developed markets reported willingness to switch to refill formats if available. Retailers are increasingly allocating shelf space to bulk dispensing and refill stations, particularly in Europe and Japan. For manufacturers, these models lower transportation costs and improve supply-chain efficiency. The opportunity extends to private-label and direct-to-consumer channels, where sustainability credentials increasingly influence purchasing decisions.

Supply chain complexity and fragmented regulatory frameworks remain key challenges for the Liquid Laundry Detergent Market. Ingredients sourced across multiple regions expose manufacturers to logistical disruptions and geopolitical risks. Transporting liquid formulations also increases handling and storage costs due to weight and spill risk. Regulatory fragmentation adds further complexity, as labeling, ingredient disclosure, and environmental standards vary significantly between regions such as North America, Europe, and Asia-Pacific. Compliance with country-specific norms can extend product rollout timelines by 6–12 months. These challenges necessitate robust supply-chain planning, regionalized production strategies, and continuous regulatory monitoring, increasing operational overhead for market participants.

Shift Toward Concentrated and Ultra-Concentrated Formulations: Manufacturers are increasingly prioritizing concentrated and ultra-concentrated liquid laundry detergents to optimize logistics and sustainability metrics. In 2024, concentrated formats accounted for nearly 42% of new liquid detergent product launches globally. These formulations reduce packaging material usage by up to 30% and lower transportation weight by approximately 25%, improving supply chain efficiency while maintaining equivalent wash performance per dose.

Acceleration of Cold-Water and Low-Temperature Washing Solutions: Cold-water-compatible liquid detergents are gaining traction as energy efficiency becomes a purchasing criterion. Over 60% of households in developed markets now use cold or low-temperature wash cycles at least once per week. Advanced enzyme blends enable effective stain removal at temperatures below 30°C, contributing to household energy savings of up to 35% per wash and supporting broader carbon reduction objectives.

Growth of Sustainable Packaging and Refill Adoption: Sustainable packaging innovations are reshaping product differentiation in the Liquid Laundry Detergent market. In 2024, refill pouches and bulk formats represented approximately 28% of liquid detergent unit sales in urban retail channels. These formats reduce single-use plastic consumption by as much as 70% per refill cycle. More than 40% of consumers reported preference for detergents packaged in recyclable or reusable containers, influencing retail shelf strategies.

Integration of Smart Dosing and Digital Consumer Engagement: Smart dosing technologies and connected packaging are emerging as measurable efficiency drivers. Automatic dosing systems integrated with washing machines can reduce detergent overuse by nearly 20% per cycle. Additionally, QR-enabled labels and mobile-linked usage guidance increased correct dosing compliance to over 75% among participating users in 2024, improving wash consistency and lowering product wastage across residential and commercial applications.

The Liquid Laundry Detergent Market is segmented by type, application, and end-user, each reflecting distinct usage patterns, formulation preferences, and operational requirements. By type, concentration level and functional formulation define purchasing behavior, particularly as consumers and institutions prioritize efficiency, storage optimization, and environmental impact. Application-wise, household usage remains dominant, while commercial and institutional applications are expanding due to hygiene standards and operational scale. End-user segmentation highlights households as the primary consumers, complemented by strong uptake across hospitality, healthcare, and commercial laundry operators. Across all segments, demand is shaped by washing machine compatibility, sustainability requirements, and precision dosing needs, making segmentation critical for product positioning, capacity planning, and innovation strategies.

Liquid laundry detergents are primarily categorized into regular liquid detergents, concentrated liquids, ultra-concentrated liquids, and specialty formulations such as hypoallergenic and enzyme-enhanced variants. Regular liquid detergents currently account for approximately 46% of total adoption, driven by affordability, familiarity, and broad retail availability. Concentrated liquid detergents hold close to 32% of adoption, offering reduced packaging volume and improved transport efficiency. Ultra-concentrated formulations represent the fastest-growing type, expanding at an estimated 6.1% CAGR, supported by demand for compact packaging and lower per-wash chemical usage. Specialty liquids, including sensitive-skin and antibacterial variants, collectively contribute around 22% of adoption, serving niche but high-value consumer segments.

By application, household laundry remains the leading segment, accounting for nearly 64% of liquid detergent usage, supported by widespread penetration of automatic washing machines and routine domestic consumption. Commercial laundries represent about 18% of application demand, while institutional use in healthcare, hospitality, and education contributes roughly 12%. Industrial and specialty cleaning applications together account for the remaining 6%. While household use dominates, commercial laundry applications are growing fastest at an estimated 5.4% CAGR, driven by outsourcing of laundry services and stricter hygiene protocols in hotels and healthcare facilities.

Households are the leading end-user segment in the Liquid Laundry Detergent Market, accounting for approximately 62% of total consumption. High usage frequency, brand loyalty, and compatibility with residential washing machines support this position. Commercial laundry service providers account for around 20% of end-user adoption, followed by hospitality and healthcare institutions at a combined 14%. Among these, commercial laundry operators represent the fastest-growing end-user group, expanding at an estimated 5.7% CAGR, fueled by urbanization and the rise of shared and outsourced laundry services.

Other end-users, including educational institutions and industrial facilities, collectively contribute about 4% of usage, primarily for uniform and linen cleaning.

North America accounted for the largest market share at 34.8% in 2024 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 5.3% between 2025 and 2032.

North America’s leadership is supported by liquid detergent usage exceeding 70% of households, high penetration of automatic washing machines, and strong preference for premium and concentrated formulations. Europe followed with a 29.1% share, driven by regulatory alignment and sustainability-focused consumption patterns. Asia-Pacific held 27.6% of the market in 2024, supported by rising urbanization and washing machine penetration surpassing 52% of urban households. South America and the Middle East & Africa collectively contributed 8.5%, reflecting gradual adoption supported by retail expansion, improving appliance ownership, and localized manufacturing initiatives.

How is advanced consumer behavior shaping premium detergent adoption?

North America represented approximately 34.8% of the Liquid Laundry Detergent Market in 2024, with demand primarily driven by household usage, healthcare laundries, and hospitality services. More than 72% of households use liquid detergent as their primary format, reflecting compatibility with high-efficiency washing machines. Regulatory focus on phosphate reduction and biodegradable ingredients has accelerated product reformulation. Digital transformation is evident, with nearly 38% of newly sold washing machines equipped with automatic detergent dispensing systems. Regional consumer behavior shows higher enterprise adoption in healthcare and institutional laundries, where precision dosing and hygiene compliance remain critical purchasing factors.

How do sustainability mandates influence formulation and packaging decisions?

Europe accounted for nearly 29.1% of the global Liquid Laundry Detergent Market in 2024, led by Germany, the UK, and France, which together contribute over 60% of regional demand. Regulatory frameworks emphasizing biodegradable surfactants, microplastic elimination, and recyclable packaging strongly influence formulation strategies. Over 45% of liquid detergents sold in the region carry eco-focused claims. Adoption of cold-water washing solutions is widespread, with more than 65% of consumers regularly using low-temperature cycles. Consumer behavior reflects heightened demand for ingredient transparency and environmentally compliant products.

What role does urbanization play in accelerating household adoption?

Asia-Pacific ranked as the second-largest regional market by volume, holding 27.6% share in 2024, with China, India, and Japan as the top consuming countries. Urban washing machine penetration exceeded 52%, directly supporting increased liquid detergent usage. Regional manufacturing capacity expanded by over 18% between 2022 and 2024, strengthening domestic supply chains. Innovation hubs in Japan and South Korea are advancing enzyme efficiency and compact packaging technologies. Consumer behavior in this region is increasingly influenced by e-commerce, which accounts for nearly 30% of detergent purchases in major metropolitan areas.

How are retail expansion and trade policies shaping demand?

South America accounted for approximately 5.2% of the Liquid Laundry Detergent Market in 2024, led by Brazil and Argentina, which together represent more than 65% of regional consumption. Expansion of modern retail infrastructure and private-label penetration has improved product accessibility. Government trade incentives supporting local FMCG production have strengthened domestic supply. Energy-efficient washing machine adoption reached 41% of urban households, supporting gradual transition from powder to liquid detergents. Consumer behavior remains price-sensitive, with value-sized liquid packs gaining preference in urban centers.

How is modernization influencing household cleaning preferences?

The Middle East & Africa region contributed roughly 3.3% of the global Liquid Laundry Detergent Market in 2024, with demand concentrated in the UAE, Saudi Arabia, and South Africa. Urbanization and rising disposable incomes are increasing washing machine penetration beyond 45% in major cities. Modern retail expansion and favorable trade partnerships are improving product availability. Manufacturers are introducing heat-stable liquid formulations suitable for high-temperature environments. Consumer behavior varies widely, with premium adoption in Gulf economies and affordability-driven usage across parts of Africa.

United States Liquid Laundry Detergent Market – 28.4% share

High production capacity, strong household adoption of automatic washing machines, and advanced formulation innovation.

China Liquid Laundry Detergent Market – 19.6% share

Large urban consumer base, expanding domestic manufacturing capacity, and rising household appliance penetration.

The Liquid Laundry Detergent market operates within a moderately consolidated competitive environment, characterized by the presence of approximately 35–40 active multinational and regional manufacturers globally. The market is led by a small group of large FMCG players with extensive production capacity, brand equity, and global distribution networks, while mid-sized and regional companies compete through pricing strategies, private-label manufacturing, and localized product differentiation. The combined share of the top five companies is estimated at around 62%, indicating a consolidated core with competitive intensity at the regional and category level.

Competitive positioning increasingly depends on formulation innovation, sustainability credentials, and packaging efficiency. Over 45% of leading manufacturers have introduced concentrated or ultra-concentrated liquid detergents in the past three years to reduce logistics costs and improve ESG performance. Strategic initiatives include expansion of refill systems, partnerships with appliance manufacturers for smart dosing compatibility, and investments in enzyme optimization technologies that improve cleaning performance in cold-water cycles by up to 30%. Mergers and capacity expansions are primarily focused on Asia-Pacific and Latin America, where manufacturing footprint growth exceeded 15% between 2022 and 2024. Product launch velocity remains high, with leading players introducing an average of 8–12 new SKUs annually to address premium, sensitive-skin, and eco-certified segments.

Procter & Gamble

Unilever

Henkel AG & Co. KGaA

Church & Dwight Co., Inc.

Reckitt

Kao Corporation

Colgate-Palmolive Company

Lion Corporation

Seventh Generation

The Clorox Company

Technology plays a critical role in shaping product performance, sustainability outcomes, and operational efficiency within the Liquid Laundry Detergent Market. One of the most impactful advancements is the development of enzyme-engineered formulations designed for low-temperature washing. Modern multi-enzyme systems improve stain removal efficiency by up to 30% at temperatures below 30°C, enabling households and commercial laundries to reduce energy consumption per wash by approximately 35%. These formulations also extend fabric life, reducing textile fiber damage by nearly 20% over repeated wash cycles.

Another key technological shift is the adoption of ultra-concentrated liquid detergents, enabled by advanced surfactant chemistry and viscosity control technologies. Ultra-concentrated products reduce water content by up to 50%, allowing smaller packaging formats and lowering plastic usage by nearly 40% per unit. This has significant implications for logistics efficiency, with transportation load optimization improving pallet density by more than 25%. Precision blending and automated quality control systems are increasingly deployed in manufacturing facilities, reducing batch variability by approximately 15% and minimizing formulation waste.

Smart dosing technology represents a growing area of innovation, particularly through integration with connected washing machines. Automatic dosing systems can cut detergent overuse by 18–22% per cycle, improving cost efficiency and reducing wastewater chemical load. Packaging technologies are also advancing, with QR-enabled labels, mono-material bottles, and refill pouch systems gaining traction. Refill-based packaging models can reduce single-use plastic consumption by up to 70% per consumer annually. Collectively, these technological advancements are positioning the Liquid Laundry Detergent Market for enhanced performance, regulatory compliance, and long-term sustainability.

• In January 2024, Procter & Gamble introduced Tide Eco-Box in the United States, a new eco-friendly liquid laundry detergent line featuring sustainable packaging and plant-based formulations, designed to reduce plastic use and support household environmental goals.

• In 2024, Unilever expanded its Wonder Wash liquid laundry detergent designed for 15-minute wash cycles, addressing consumer demand for quicker and more convenient laundry care across multiple international markets.

• In 2024, Henkel launched more concentrated liquid versions of its All®, Persil®, and Snuggle® detergents, optimizing dose efficiency, incorporating 50% recycled plastic in packaging, and reducing water and CO₂ intensity in formulation and logistics.

• In 2024, ECOS introduced an Ultra-Concentrated Laundry Detergent at Natural Products Expo West, emphasizing environmental sustainability through highly concentrated formulation that significantly reduces packaging waste and improves transport efficiency.

The Liquid Laundry Detergent Market Report provides a comprehensive assessment of global product categories, geographic regions, technological trends, end-use applications, and competitive dynamics shaping the industry. Segmentation analysis covers various product types—regular, concentrated, ultra-concentrated, and specialty formulations such as hypoallergenic and enzyme-enhanced liquids—highlighting features like cold-water performance and compact packaging designs. The report examines application areas including household laundry, commercial laundries, institutional cleaning, and industrial segments, with measurable adoption patterns across regional markets including North America, Europe, Asia-Pacific, South America, and Middle East & Africa.

Geographic insights focus on regional volumes, consumer preferences, regulatory landscapes, and infrastructure trends influencing product availability and consumer behavior. The scope incorporates analysis of emerging technologies such as smart dosing systems, enzyme optimization for low-temperature washing, and sustainable packaging innovations including refill formats and recycled materials. It also evaluates e-commerce and digital retail strategies, subscription models, and supply chain modernizations driving market access and consumer engagement. Competitive insights detail the positioning, strategic initiatives, and innovation focus areas of leading global and regional players. Emerging or niche segments such as eco-certified detergents, plant-based surfactants, bulk institutional liquids, and AI-assisted formulation tools are explored to help decision-makers identify future opportunities, operational challenges, and investment priorities within the Liquid Laundry Detergent landscape.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 33375.26 Million |

|

Market Revenue in 2032 |

USD 46383.8 Million |

|

CAGR (2025 - 2032) |

4.2% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Procter & Gamble, Unilever, Henkel AG & Co. KGaA, Church & Dwight Co., Inc., Reckitt, Kao Corporation, Colgate-Palmolive Company, Lion Corporation, Seventh Generation, The Clorox Company |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |