Reports

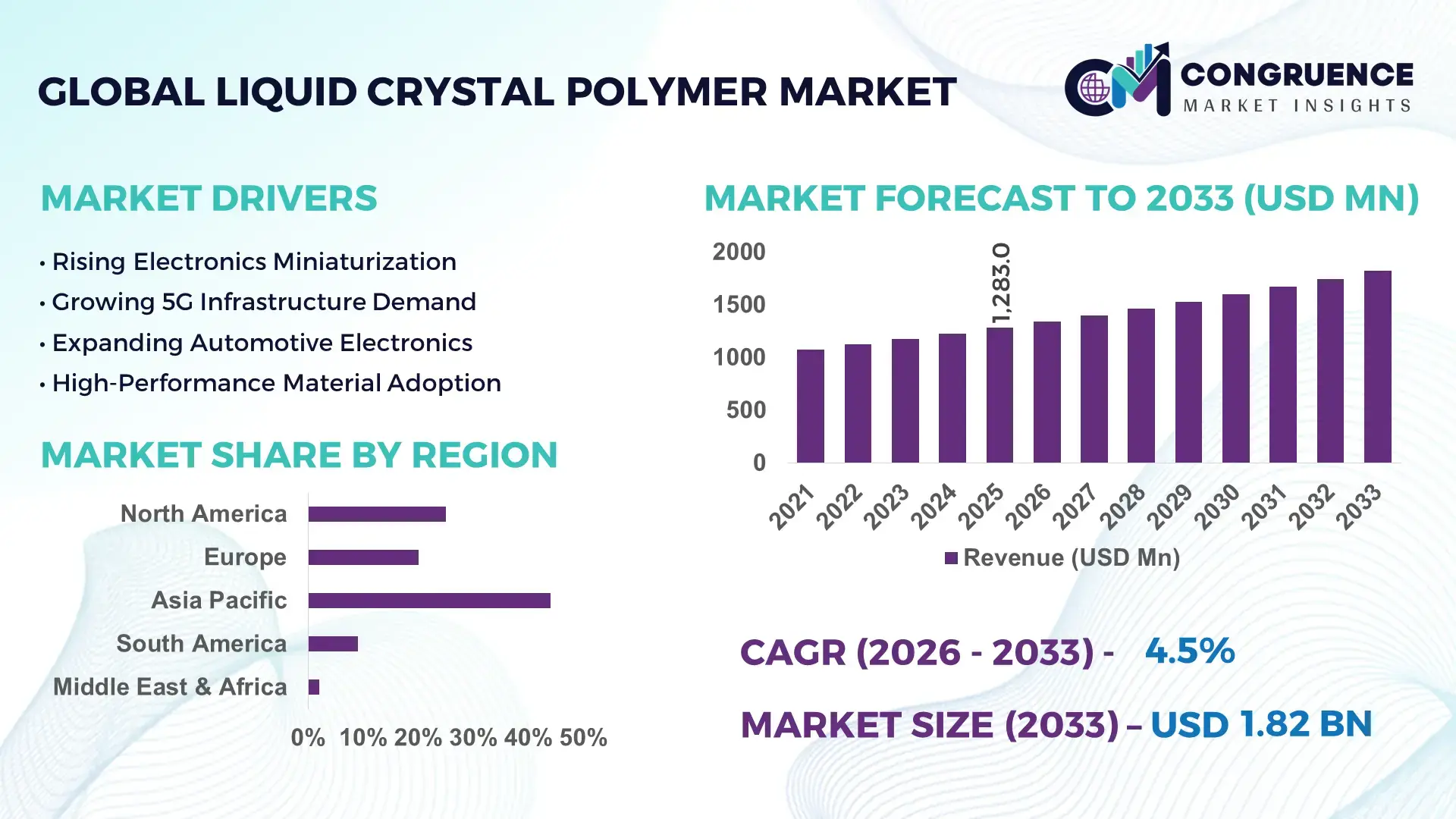

The Global Liquid Crystal Polymer Market was valued at USD 1283 Million in 2025 and is anticipated to reach a value of USD 1824.55 Million by 2033 expanding at a CAGR of 4.5% between 2026 and 2033. Rising deployment of high-frequency 5G connectors, miniaturized automotive electronics, and heat-resistant semiconductor components is accelerating advanced liquid crystal polymer consumption across precision manufacturing supply chains.

China leads the global liquid crystal polymer market with nearly 38% production share, supported by over USD 1.2 billion in electronics material investments linked to semiconductor localization initiatives after Red Sea shipping disruptions increased Asian component sourcing pressure in 2025–2026. Japan maintains stronger high-purity LCP grades for premium connectors and medical electronics, delivering approximately 22% higher thermal stability performance than standard Chinese grades. South Korea continues expanding LCP use in foldable devices and antenna modules, with telecom component integration exceeding 31% across domestic high-frequency circuit manufacturing capacity.

Strategic expansion into Asia-Pacific specialty polymer ecosystems remains critical for manufacturers targeting next-generation electronics, EV architecture, and high-speed data infrastructure applications.

Market Size & Growth: USD 1283 million in 2025 reaching USD 1824.55 million by 2033, driven by 5G connector miniaturization and high-temperature electronics integration.

Top Growth Drivers: Automotive electronics demand up 19%, high-frequency communication components up 24%, semiconductor packaging applications expanding 17%.

Short-Term Forecast: By 2028, precision molded LCP component rejection rates decline 14% through automated micro-injection manufacturing upgrades.

Emerging Technologies: AI-driven defect inspection, ultra-thin LCP films, and advanced automation improve production efficiency by nearly 21%.

Regional Leaders: Asia-Pacific exceeds USD 920 million with telecom adoption growth; North America crosses USD 310 million through aerospace demand; Europe surpasses USD 250 million from EV electrification programs.

Consumer/End-User Trends: Nearly 46% of compact smart device manufacturers increased adoption of high-performance liquid crystal polymer substrates in 2026.

Pilot/Case Example: In 2026, an automotive electronics supplier reduced connector heat failure rates by 18% using advanced LCP resin blends.

Competitive Landscape: Top manufacturers control approximately 57% market share, with leading participation from advanced polymer and specialty materials producers.

Regulatory & ESG Impact: Low-emission processing technologies reduced manufacturing energy consumption by 11% amid stricter industrial sustainability mandates.

Investment & Funding: More than USD 850 million entered specialty polymer expansions through regional partnerships and semiconductor-linked capacity additions.

Innovation & Future Outlook: Next-generation flexible circuits and millimeter-wave applications are shifting strategic focus toward ultra-low dielectric advanced LCP materials.

Liquid crystal polymer demand remains concentrated in high-density connectors, EV battery electronics, medical devices, and high-frequency communication modules requiring thermal resistance above 240°C. Advanced low-dielectric LCP film adoption increased nearly 16% across compact electronics manufacturing in 2026 as manufacturers prioritized lighter and thinner component architectures amid persistent semiconductor supply-chain regionalization. These structural shifts are reinforcing long-term investment focus on precision material engineering and advanced electronics integration strategies.

Liquid crystal polymer is becoming strategically critical as electronics manufacturers prioritize high-frequency performance, thermal resistance, and component miniaturization across EVs, AI servers, and 5G infrastructure. Supply-chain restructuring after recurring semiconductor disruptions pushed OEMs in China, Japan, and the U.S. to localize advanced polymer sourcing and reduce dependency on single-country material processing. More than 42% of high-speed connector suppliers increased procurement of ultra-low dielectric polymers in 2026 to support next-generation communication hardware and compact circuit architectures.

Advanced liquid crystal polymer grades deliver nearly 28% lower moisture absorption and approximately 18% higher dimensional stability than conventional engineering plastics used in precision electronic housings. Japan continues leading high-purity resin innovation for medical and aerospace electronics, while China dominates large-scale connector manufacturing through vertically integrated electronics clusters. In South Korea, foldable device manufacturers accelerated LCP film deployment by over 21% to improve antenna efficiency and reduce component thickness in premium mobile devices.

A 2026 telecom equipment deployment program in Taiwan reduced signal loss by 14% after integrating liquid crystal polymer-based millimeter-wave modules into compact network hardware. Manufacturers are expanding long-term resin partnerships, automated compounding capacity, and semiconductor-linked material alliances to secure performance consistency. Over the next three years, competitive advantage will increasingly depend on localized specialty polymer ecosystems, precision processing expertise, and integration into high-frequency electronics supply chains.

Rapid scaling of 5G infrastructure, EV electronics, and AI-driven computing hardware is accelerating liquid crystal polymer adoption across precision electronic components. Nearly 48% of next-generation RF connector manufacturers shifted toward low-dielectric LCP materials in 2026 to improve signal integrity and thermal endurance. China increased high-speed electronics component production capacity by approximately 19%, while Japanese suppliers expanded specialty resin output for semiconductor packaging applications. Stricter miniaturization requirements in automotive radar systems and compact medical devices are also pushing demand for ultra-thin, heat-resistant polymers. In response, manufacturers are investing in automated molding systems, localized compounding facilities, and strategic semiconductor partnerships to secure long-term supply reliability. A key operational advantage lies in LCP’s ability to reduce component failure rates under high-frequency thermal stress conditions.

Liquid crystal polymer production remains exposed to high raw material concentration and specialized processing dependency, particularly for aromatic monomer inputs sourced through limited supplier networks. Specialty feedstock pricing fluctuated by nearly 16% during 2025–2026 due to shipping disruptions across Asian chemical trade corridors and tightening environmental compliance costs in China. Manufacturing scrap rates for ultra-thin electronic components also remain 11%–13% higher than conventional engineering plastics because of strict precision molding tolerances. These pressures directly affect profitability for mid-scale electronics suppliers and increase qualification timelines for automotive-grade applications. Companies are responding through long-term procurement contracts, dual-sourcing strategies, and localized resin compounding operations in Taiwan and South Korea. A major strategic concern remains maintaining material consistency while controlling processing costs across high-volume electronics manufacturing environments.

Liquid crystal polymer suppliers are gaining new opportunities through advanced mobility systems, AI data infrastructure, and millimeter-wave communication hardware requiring lightweight, thermally stable materials. More than 34% of emerging EV sensor platforms adopted high-performance LCP connectors in 2026 to support compact electronic architectures and higher operating temperatures. India and Vietnam are becoming attractive electronics assembly hubs as manufacturers diversify production footprints beyond China. Simultaneously, next-generation low-loss LCP films are improving antenna transmission efficiency by approximately 17% in compact telecom modules. Companies are accelerating R&D collaboration with semiconductor packaging firms and telecom equipment providers to capture high-margin specialty applications. One non-obvious advantage is reduced cooling demand in dense electronics systems due to improved thermal management characteristics within miniaturized circuit assemblies.

The transition toward ultra-miniaturized electronics is increasing manufacturing complexity for liquid crystal polymer processors. Precision molding tolerances below 0.02 mm are now required across high-frequency connectors and semiconductor packaging components, raising production calibration costs by nearly 14%. Workforce shortages in advanced polymer tooling and micro-component engineering are also constraining output expansion in Japan and Germany. At the same time, evolving reliability standards for autonomous vehicle electronics and aerospace communication systems are extending qualification cycles by up to 20%. These execution pressures affect deployment consistency, product validation timelines, and long-term competitiveness. Companies must strengthen automated inspection systems, AI-assisted quality control, and specialized tooling investments to maintain scalable production efficiency. Long-term market leadership will depend on mastering precision processing capabilities rather than only expanding material supply capacity.

• Miniaturized Connector Production Expansion High-density connector manufacturers in China and Taiwan increased liquid crystal polymer integration by nearly 27% during 2026 as AI servers, foldable devices, and 5G modules required thinner and heat-resistant components. Automated micro-molding systems reduced production cycle times by 13% while improving dimensional precision for compact electronics. In response to persistent semiconductor packaging bottlenecks, suppliers are restructuring procurement contracts and co-locating compounding facilities near electronics assembly clusters to shorten lead times and stabilize specialty resin availability.

• Localized Specialty Resin Manufacturing Electronics supply-chain realignment after Red Sea shipping disruptions accelerated domestic specialty polymer investments across Japan, South Korea, and India. Nearly 31% of advanced electronics suppliers expanded localized sourcing agreements in 2025–2026 to reduce logistics volatility and import dependency. Companies are scaling regional resin blending operations and strategic storage capacity to improve continuity for telecom and automotive electronics programs. A non-obvious shift is growing preference for regional technical support teams to accelerate qualification cycles for customized LCP formulations.

• Advanced Low-Dielectric Film Adoption Deployment of ultra-low dielectric liquid crystal polymer films increased approximately 22% in compact antenna modules and millimeter-wave communication systems. Telecom hardware manufacturers in South Korea improved signal transmission efficiency by nearly 15% through thinner multilayer substrate architectures. Companies are expanding partnerships with semiconductor packaging firms and investing in precision extrusion technologies to support high-frequency applications requiring reduced moisture absorption and stable thermal performance under dense operating conditions.

• Sustainable Precision Processing Upgrades Environmental compliance pressure and rising energy costs pushed manufacturers toward low-emission processing systems and closed-loop material recovery operations. Precision molding facilities in Germany reduced production waste by 12% through AI-assisted defect monitoring and automated resin handling. At the same time, labor shortages in advanced polymer tooling accelerated robotic inspection deployment across Japanese electronics manufacturing plants. Producers are increasingly prioritizing energy-efficient processing equipment to improve operational consistency while meeting stricter industrial sustainability requirements.

Thermotropic liquid crystal polymer remains the dominant segment due to its superior melt-processability, dimensional stability, and scalability across high-frequency electronics manufacturing. Nearly 52% of advanced connector and semiconductor packaging applications relied on thermotropic grades in 2026 because of their compatibility with automated micro-injection molding systems and high-temperature circuit assembly. Filled LCP also maintains strong adoption in automotive electronics and industrial components where glass-fiber reinforcement improves mechanical rigidity by approximately 18%. Companies in Japan and Taiwan continue expanding thermotropic resin capacity to support compact telecom and AI infrastructure hardware production.

High-Temperature LCP is emerging as the fastest-growing segment as EV battery management systems and aerospace communication modules demand continuous thermal resistance above 240°C. Adoption of unfilled LCP increased by nearly 14% in precision medical devices due to improved surface finish and sterilization compatibility, while lyotropic grades remain limited to niche industrial processing applications. Manufacturers are prioritizing advanced compounding technologies, customized dielectric formulations, and localized production partnerships to secure high-margin electronics contracts and reduce qualification delays across specialized applications.

Electrical Connectors remain the leading application segment as telecom equipment, AI servers, and compact consumer electronics require lightweight, heat-resistant, and low-dielectric materials for high-speed signal transmission. Approximately 48% of liquid crystal polymer consumption in 2026 was concentrated in connector manufacturing, particularly across China’s high-density electronics assembly ecosystem. Electronic Components also maintain strong utilization through semiconductor packaging, antenna modules, and miniaturized circuit housings where dimensional stability and moisture resistance directly improve operational reliability. Manufacturers are expanding automated molding lines and precision tooling investments to support rising demand for thinner and higher-frequency component architectures.

Automotive Parts represent the fastest-growing application segment as EV platforms increasingly integrate radar sensors, battery electronics, and advanced driver-assistance systems requiring thermally stable polymers. LCP adoption in automotive electronic modules increased nearly 21% during 2025–2026, while medical devices gained traction through sterilization-compatible micro-components and surgical electronics. Industrial Components continue generating stable demand across precision machinery and factory automation systems. Companies are strengthening partnerships with automotive OEMs, semiconductor suppliers, and telecom hardware manufacturers to secure long-term integration into advanced electronics platforms.

The Electronics Industry remains the dominant end-user group due to large-scale deployment of liquid crystal polymer in smartphones, AI servers, semiconductor packaging, and high-frequency communication systems. Nearly 58% of global LCP demand in 2026 originated from electronics manufacturing hubs in China, South Korea, and Taiwan where miniaturized device architectures continue driving precision polymer integration. Consumer Goods Industry applications are also expanding steadily through foldable devices, wearable electronics, and compact smart appliances requiring lightweight and heat-resistant materials. Producers are increasingly offering customized dielectric formulations and faster prototyping support to secure long-term contracts with electronics OEMs.

The Automotive Industry is emerging as the fastest-growing end-user segment as EV electronics, autonomous driving systems, and advanced sensor modules require stable performance under elevated thermal conditions. Automotive-related LCP integration increased approximately 23% during 2025–2026 across battery management systems and radar communication hardware. Healthcare Industry demand is strengthening through minimally invasive medical electronics and sterilizable diagnostic equipment, while Aerospace Industry adoption remains focused on lightweight communication assemblies. Companies are responding through specialized product portfolios, localized technical support centers, and ecosystem partnerships with semiconductor and automotive suppliers to strengthen competitive positioning.

Asia-Pacific accounted for the largest market share at 46% in 2025 however, Middle East & Africa is expected to register the fastest growth, expanding at a CAGR of 5.9% between 2026 and 2033.

Advanced Semiconductor and EV Electronics Integration

North America maintains strong liquid crystal polymer demand through semiconductor packaging, aerospace electronics, and EV system integration. The region accounted for nearly 24% of global consumption in 2025, supported by growing deployment of AI server infrastructure and high-frequency communication hardware across the United States. Automotive electronics manufacturers increased adoption of heat-resistant LCP connectors by approximately 18% during 2025–2026 to improve reliability in advanced driver-assistance systems. Strategic investments in semiconductor reshoring and electronics supply-chain localization are strengthening domestic specialty polymer processing capacity. Companies are also expanding partnerships with telecom hardware firms to accelerate deployment of ultra-low dielectric materials for next-generation networking equipment and compact computing architectures.

United States Market Outlook: The United States leads regional demand through strong semiconductor manufacturing expansion, aerospace electronics deployment, and AI infrastructure investments. More than 43% of newly commissioned advanced packaging facilities integrated specialty polymer materials into high-density electronic assemblies during 2026. Domestic manufacturers are prioritizing automated precision molding systems and localized material sourcing agreements to reduce dependence on imported electronic-grade polymers. Defense modernization programs and electric vehicle electronics integration continue strengthening long-term demand for thermally stable and low-moisture absorption LCP grades.

Sustainability-Driven Precision Electronics Manufacturing

Europe is strengthening its liquid crystal polymer position through sustainable manufacturing upgrades, automotive electrification, and advanced industrial automation systems. The region represented approximately 21% of global market activity in 2025, with Germany, France, and the Netherlands leading high-performance electronics integration. Environmental compliance measures pushed electronics manufacturers to adopt low-emission polymer processing technologies that reduced operational waste by nearly 12% across selected facilities. Demand for lightweight and thermally resistant components is increasing across EV battery systems, industrial robotics, and aerospace communication equipment. Companies are responding through precision tooling investments, recycling-oriented material handling systems, and long-term partnerships with semiconductor packaging suppliers to improve manufacturing resilience and component reliability.

Germany Market Outlook: Germany remains the region’s operational hub for automotive electronics and industrial automation technologies requiring precision-engineered polymers. Automotive suppliers increased integration of liquid crystal polymer components by approximately 19% in radar modules and battery control systems during 2026. Advanced factory modernization programs and robotics deployment are accelerating demand for high-temperature engineering materials. German manufacturers are also investing in energy-efficient molding infrastructure and collaborative R&D programs focused on lightweight electronics and next-generation mobility systems.

High-Volume Electronics Manufacturing Dominance

Asia-Pacific dominates the liquid crystal polymer market through concentrated electronics manufacturing ecosystems, telecom infrastructure expansion, and semiconductor packaging leadership. The region contributed nearly 46% of global demand in 2025, driven by China, Japan, South Korea, and Taiwan. China alone accounted for over 38% of global LCP production capacity due to large-scale connector manufacturing and vertically integrated electronics supply chains. South Korean manufacturers increased deployment of LCP films by approximately 21% in foldable smartphones and millimeter-wave antenna modules. Regional companies are expanding automated compounding facilities, advanced extrusion lines, and localized specialty resin production to support rising demand for compact and high-frequency electronic devices.

China Market Outlook: China remains the most strategically significant market due to its large electronics assembly base, connector manufacturing scale, and semiconductor localization initiatives. Domestic electronics suppliers expanded precision LCP molding capacity by nearly 24% during 2025–2026 to support AI servers, 5G infrastructure, and EV electronics integration. Government-backed industrial modernization policies and regional semiconductor investments continue strengthening the country’s specialty polymer ecosystem. Chinese producers are increasingly focusing on customized low-dielectric formulations and export-oriented telecom component manufacturing to improve global competitiveness.

Automotive Electronics Demand Expansion

South America is witnessing gradual liquid crystal polymer adoption through automotive electronics manufacturing, industrial automation upgrades, and telecom infrastructure modernization. The region contributed nearly 5% of global demand in 2025, with Brazil and Argentina driving most deployment activity. Automotive component manufacturers increased procurement of heat-resistant engineering polymers by approximately 14% during 2026 to support sensor integration and compact electronic modules. However, dependence on imported specialty materials and limited local compounding infrastructure continue constraining large-scale market expansion. Companies are addressing these limitations through regional distribution partnerships, localized warehousing strategies, and technical collaborations with Asian material suppliers to improve delivery stability and application-specific product customization.

Brazil Market Outlook: Brazil leads the regional market through its automotive manufacturing ecosystem and expanding industrial electronics sector. Vehicle electronics suppliers increased use of advanced polymer connectors by nearly 16% in response to rising deployment of connected mobility systems and factory automation technologies. Industrial modernization initiatives in São Paulo and southern manufacturing clusters are improving adoption of precision-engineered components. Domestic distributors are strengthening partnerships with international polymer producers to improve access to specialized grades required for telecom, industrial control, and automotive electronics applications.

Industrial Diversification and Infrastructure Modernization

Middle East & Africa is emerging as a high-potential market due to industrial diversification programs, smart infrastructure deployment, and expanding telecommunications investment. The region accounted for approximately 4% of global market activity in 2025, with the UAE and Saudi Arabia leading advanced electronics and industrial modernization initiatives. Telecom infrastructure projects increased demand for high-frequency electronic components by nearly 17% during 2025–2026. Governments are prioritizing technology localization and industrial expansion through smart manufacturing zones and advanced logistics infrastructure. Companies are responding by establishing regional distribution hubs, technical service partnerships, and electronics assembly collaborations to support long-term demand for lightweight and thermally stable polymer materials.

Saudi Arabia Market Outlook: Saudi Arabia is strengthening its position through industrial diversification initiatives linked to advanced manufacturing and digital infrastructure deployment. Electronics and industrial automation projects increased procurement of specialty engineering polymers by approximately 15% in 2026, particularly across telecom and smart infrastructure applications. Large-scale investment in technology parks and localized manufacturing ecosystems is improving operational readiness for advanced material integration. Companies are targeting the country through strategic supply agreements and technical partnerships supporting industrial electronics and high-performance communication systems.

The liquid crystal polymer market is led by global specialty material producers including Celanese, Sumitomo Chemical, Polyplastics, Toray Industries, Solvay, and Ueno Fine Chemicals competing against regional compounders and cost-focused Asian suppliers. The top five players collectively control nearly 62% of global supply through integrated production networks, proprietary formulations, and long-term electronics sector partnerships. Competition centers on dielectric performance, thermal resistance, precision molding consistency, and supply-chain responsiveness rather than pricing alone. Advanced LCP grades improved signal efficiency by approximately 15%, while automated compounding systems reduced defect rates by nearly 12% in high-frequency connector manufacturing. Japanese and U.S. suppliers are competing through material innovation and semiconductor alliances, whereas Chinese manufacturers emphasize scale expansion and localized delivery. Vertical integration into specialty monomers and telecom component ecosystems is accelerating market consolidation. Winning requires stable feedstock access, precision engineering capability, application-specific customization, and deep integration with electronics manufacturing supply chains globally.

Celanese Corporation

Polyplastics Co., Ltd.

Sumitomo Chemical Co., Ltd.

Toray Industries, Inc.

Solvay S.A.

Ueno Fine Chemicals Industry, Ltd.

RTP Company

Shanghai PRET Composites Co., Ltd.

Kuraray Co., Ltd.

Chang Chun Group

Kingfa Sci. & Tech. Co., Ltd.

Zhejiang NHU Special Materials Co., Ltd.

SABIC

Ensinger GmbH

Advanced thermotropic liquid crystal polymer technologies are reshaping high-frequency electronics, EV modules, and semiconductor packaging through improved thermal stability and ultra-low dielectric performance. In 2026, nearly 48% of compact connector manufacturers integrated next-generation LCP grades into high-speed transmission systems to reduce signal loss and dimensional distortion. Compared with conventional engineering plastics, advanced LCP materials deliver approximately 28% lower moisture absorption and 18% higher dimensional stability in precision electronic assemblies. Companies in Japan and South Korea are scaling automated micro-molding systems that improve production efficiency by nearly 14% while reducing defect rates in ultra-thin connector manufacturing.

Emerging technologies include ultra-low dielectric LCP films, AI-assisted defect inspection, and precision extrusion platforms supporting millimeter-wave communication hardware and foldable electronics. Deployment of thin-film LCP substrates increased nearly 22% during 2025–2026 as telecom equipment suppliers prioritized lighter and compact antenna architectures. Semiconductor packaging firms are integrating AI-enabled quality monitoring systems that reduce inspection time by approximately 16%, improving operational consistency for dense electronic components and next-generation AI computing hardware.

Disruptive innovation is accelerating through additive manufacturing-compatible LCP powders, advanced compounding formulations, and localized specialty resin ecosystems. New powder-processing technologies improved material flowability by approximately 19% compared with legacy grinding methods, supporting precision prototyping and complex geometry production. Global specialty polymer producers and semiconductor-linked material suppliers benefit most from this transition due to stronger integration with electronics manufacturing supply chains. Between 2026 and 2028, competitive advantage will increasingly depend on low-loss material engineering, automated processing capability, and regionalized production resilience.

May 2026 – Celanese announced strategic expansion of liquid crystal polymer-related operations in China alongside specialty compound upgrades in Europe and localization initiatives in India. The restructuring program strengthened regional supply-chain agility and optimized engineered materials deployment for electronics customers. Source: nasdaq.com

October 2025 – Polyplastics confirmed new liquid crystal polymer capacity expansion plans during K 2025, supporting rising global electronics demand and advanced material supply requirements. The initiative included significant infrastructure investment and broader production scaling to improve operational continuity for high-performance polymer customers. Source: polymerupdate.com

September 2025 – Polyplastics introduced DURAST Powder technology enabling liquid crystal polymer micronization with particle sizes between 1–100 μm for additive manufacturing and advanced prototyping applications. The innovation improved processing flexibility and expanded deployment potential across precision manufacturing and high-density electronic component development.

December 2025 – Polyplastics expanded its LAPEROS LCP portfolio with new LH and TF series materials engineered for electronics miniaturization and high-flow processing performance. The launch strengthened the company’s position in ultra-thin connectors and next-generation communication devices requiring improved dimensional accuracy. Source: plastech.biz

The report provides detailed analysis of liquid crystal polymer market dynamics across thermotropic, lyotropic, filled LCP, unfilled LCP, and high-temperature LCP segments, covering evolving deployment trends in precision electronics, automotive systems, medical devices, and industrial manufacturing. More than 55% of assessed demand concentration originates from high-frequency electrical connectors and semiconductor packaging applications requiring low dielectric performance and advanced thermal resistance. The study evaluates operational shifts across Asia-Pacific, North America, Europe, South America, and Middle East & Africa, with country-level insights focused on electronics manufacturing ecosystems, specialty polymer processing capacity, and industrial modernization strategies.

The report also examines emerging technologies including ultra-low dielectric films, AI-assisted quality inspection, precision extrusion systems, and additive manufacturing-compatible LCP powders shaping competitive differentiation between 2026 and 2033. Strategic analysis includes supply-chain localization trends, production optimization initiatives, partnership activity, and investment positioning across telecom infrastructure, EV electronics, aerospace systems, and AI computing hardware. The assessment supports business expansion planning, procurement strategy, manufacturing prioritization, and long-term competitive positioning for material suppliers, component manufacturers, and advanced electronics enterprises.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 1283 Million |

|

Market Revenue in 2033 |

USD 1824.55 Million |

|

CAGR (2026 - 2033) |

4.5% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Celanese Corporation, Polyplastics Co., Ltd., Sumitomo Chemical Co., Ltd., Toray Industries, Inc., Solvay S.A., Ueno Fine Chemicals Industry, Ltd., RTP Company, Shanghai PRET Composites Co., Ltd., Kuraray Co., Ltd., Chang Chun Group, Kingfa Sci. & Tech. Co., Ltd., Zhejiang NHU Special Materials Co., Ltd., SABIC, Ensinger GmbH |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |