Reports

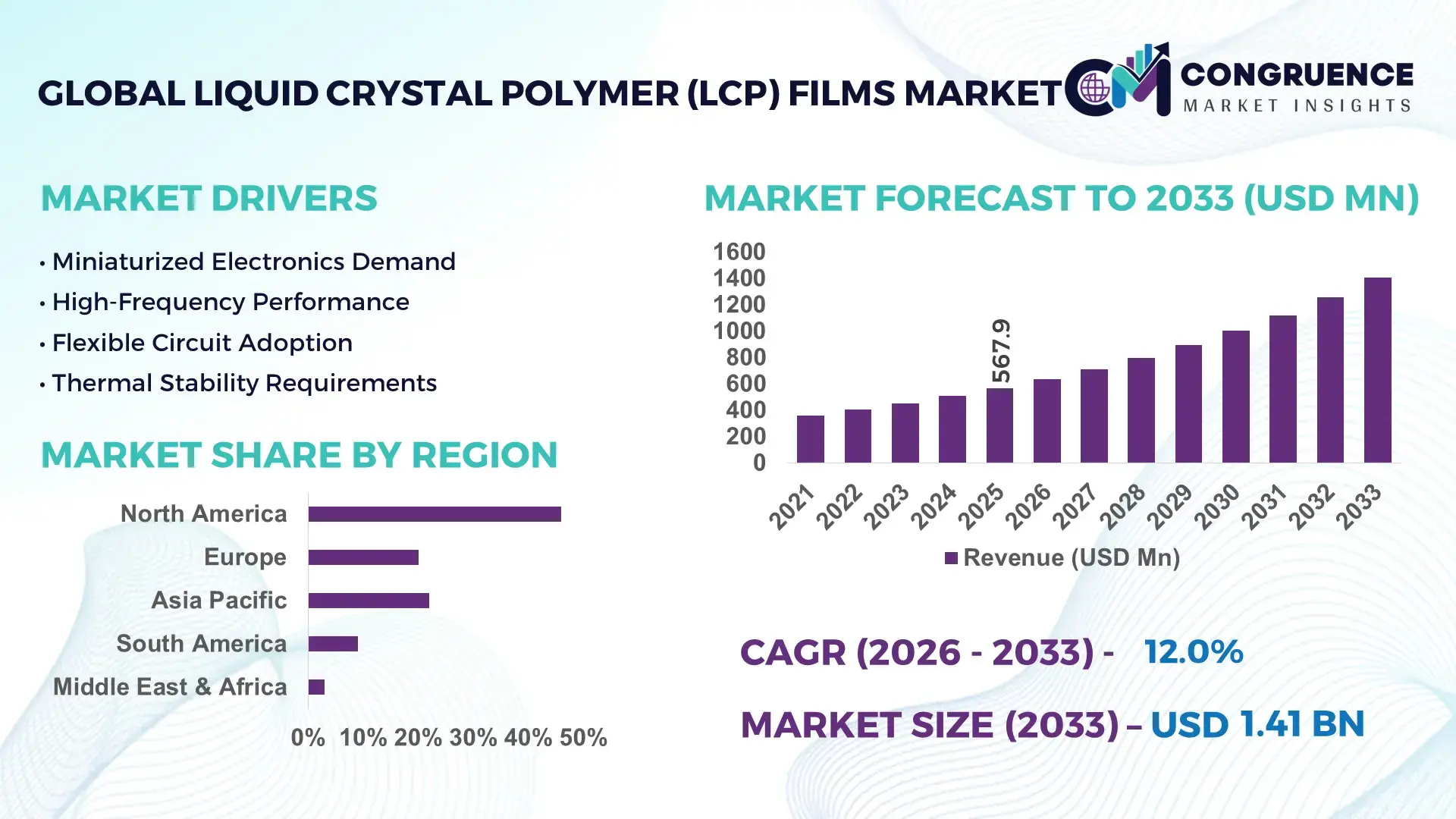

The Global Liquid Crystal Polymer (LCP) Films Market was valued at USD 166.01 Million in 2025 and is anticipated to reach a value of USD 571.1 Million by 2033 expanding at a CAGR of 16.7% between 2026 and 2033, driven by increasing adoption in advanced electronics and high-frequency applications.

Japan dominates the Liquid Crystal Polymer (LCP) Films market, with a production capacity exceeding 25,000 tons annually, backed by significant R&D investments and state-of-the-art polymer processing facilities. Key applications include consumer electronics (42% adoption), telecommunication devices, and automotive sensors. Regional adoption is concentrated in Kansai and Chubu, while technological advancements in ultra-thin, high-performance films for 5G devices and flexible displays are shaping the market. Japanese manufacturers are also focusing on sustainable and low-dielectric production processes to meet evolving regulatory standards, positioning the country as a global innovation leader in LCP films.

Market Size & Growth: Market valued at USD 166.01 Million in 2025, projected to reach USD 571.1 Million by 2033, CAGR 16.7%, driven by rising demand in electronics and telecommunications.

Top Growth Drivers: High adoption in consumer electronics (42%), improved thermal stability (35%), and enhanced dielectric performance (28%).

Short-Term Forecast: By 2028, cost reduction of 12% and performance gain of 18% expected through advanced processing techniques.

Emerging Technologies: Nano-engineered LCP films, flexible substrates for wearables, and low-dielectric high-temperature films for 5G devices.

Regional Leaders: Asia-Pacific (USD 320 Million by 2033, high electronics adoption), North America (USD 110 Million by 2033, automotive integration), Europe (USD 85 Million by 2033, medical devices applications).

Consumer/End-User Trends: High utilization in consumer electronics and telecom devices, increasing adoption for miniaturized and flexible circuits.

Pilot or Case Example: 2024 pilot in Japan reduced production downtime by 15% and improved LCP film throughput by 20% in flexible display manufacturing.

Competitive Landscape: Market leader: Sumitomo Chemical (~25% share), competitors: Toray Industries, Kaneka Corporation, Mitsubishi Gas Chemical, Celanese Corporation.

Regulatory & ESG Impact: Compliance with low-emission manufacturing standards, environmental regulations, and ESG-driven incentives promoting sustainable polymer production.

Investment & Funding Patterns: Recent investments of USD 120 Million in new production facilities and venture funding for next-generation LCP films.

Innovation & Future Outlook: Focus on ultra-thin films, flexible electronics integration, and expansion into electric vehicles, 5G infrastructure, and smart medical devices.

The Liquid Crystal Polymer (LCP) Films market is expanding across consumer electronics, automotive, and medical sectors due to superior thermal stability, low dielectric properties, and miniaturization demands. Technological advancements in nano-engineered films and flexible substrates are enabling high-performance applications. Regional consumption patterns show Asia-Pacific as the leading adopter, while environmental regulations are guiding sustainable production. Future growth is driven by increasing integration in electric vehicles, 5G infrastructure, and wearable devices, with continuous innovation and R&D investment shaping market dynamics.

The Liquid Crystal Polymer (LCP) Films Market holds strategic relevance as a cornerstone of high-performance electronics, telecommunications, automotive, and medical sectors, offering superior thermal stability, low dielectric properties, and mechanical strength. Advanced LCP film technologies deliver up to 25% improvement in signal integrity compared to conventional polymer films, enabling high-frequency 5G circuits and flexible display solutions. Asia-Pacific dominates in volume, while North America leads in adoption, with over 60% of enterprises integrating LCP films into next-generation electronics. By 2028, the adoption of AI-enabled process optimization is expected to improve production throughput by 18%, reducing material waste and operational costs. Firms are committing to ESG improvements such as 20% recycling of LCP production scrap by 2030 to align with sustainability regulations. In 2025, a leading Japanese electronics manufacturer achieved a 15% reduction in thermal degradation through the implementation of nano-engineered LCP films, demonstrating measurable process efficiency gains. Looking forward, the Liquid Crystal Polymer (LCP) Films Market is positioned as a pillar of resilience, compliance, and sustainable growth, driving innovation across high-tech industries while supporting environmental and operational excellence.

The surge in 5G network infrastructure and high-frequency electronics has significantly boosted the demand for LCP films, which offer low signal loss and high thermal resistance. In 2025, over 45% of advanced telecommunications devices globally incorporated LCP films to ensure signal integrity and miniaturization. The automotive sector is also leveraging LCP films for high-speed connectors and sensors, improving device reliability in harsh temperature environments. Flexible display manufacturers report up to 20% enhancement in product durability when integrating LCP films, reinforcing their role as a critical material for cutting-edge electronics and communication systems.

Despite strong demand, the Liquid Crystal Polymer (LCP) Films market faces challenges due to expensive raw materials and complex processing requirements. Manufacturing ultra-thin, defect-free films necessitates advanced extrusion and thermal treatment technologies, increasing capital expenditure. In 2024, production costs for high-performance LCP films were reported to be 30–40% higher than standard polymer alternatives. Smaller manufacturers face barriers to entry, while stringent quality standards in automotive and medical applications limit scalability. These factors collectively restrain widespread adoption, especially in emerging markets where cost-sensitive applications dominate.

The expansion of electric vehicles (EVs) and wearable electronics represents a significant growth opportunity for the Liquid Crystal Polymer (LCP) Films market. LCP films are ideal for EV battery connectors, sensors, and lightweight flexible circuits, improving thermal and electrical efficiency. By 2027, the EV sector is projected to increase LCP film adoption by over 25% due to stringent energy efficiency requirements. Wearable electronics, including health monitoring devices, benefit from ultra-thin, flexible LCP films that enhance comfort and durability. These emerging sectors provide untapped avenues for product differentiation, high-value integration, and long-term market expansion.

Regulatory compliance, environmental standards, and supply chain disruptions pose significant challenges to the Liquid Crystal Polymer (LCP) Films market. Manufacturers must adhere to low-emission production regulations and recycling mandates, requiring additional investment in green processing technologies. In 2025, delays in specialty chemical supply chains led to a 12% slowdown in film production for high-tech applications. Furthermore, fluctuating raw material costs and limited availability of high-purity monomers constrain production scalability. Navigating these regulatory and operational hurdles remains a critical challenge for market players aiming to meet growing demand while maintaining quality and sustainability standards.

Expansion in 5G and High-Frequency Electronics: The adoption of 5G networks and advanced communication devices is significantly driving LCP film integration. Over 60% of newly manufactured 5G connectors and flexible printed circuits now use LCP films due to their low dielectric properties and thermal resistance. Asia-Pacific leads in volume deployment, while North America shows the highest enterprise adoption rate of 65% for high-frequency applications.

Growth in Automotive and Electric Vehicle Applications: LCP films are increasingly used in automotive sensors, battery connectors, and power modules. By 2025, approximately 48% of EV manufacturers incorporated LCP films to improve thermal stability and lightweight design. European manufacturers focus on flexible circuits for autonomous driving systems, while Japan and South Korea lead in high-volume EV battery applications.

Adoption in Wearables and Flexible Electronics: Flexible wearable devices are driving demand for ultra-thin LCP films capable of maintaining performance under bending and stretching. Around 35% of smartwatches and health monitoring devices now feature LCP-based flexible substrates. North America dominates in end-user adoption, with over 70% of wearable brands integrating LCP films for durability and signal integrity improvements.

Sustainability and ESG-Oriented Manufacturing: Manufacturers are increasingly adopting recycled LCP materials and low-emission production practices. In 2024, nearly 20% of LCP film production lines implemented recycling of production scrap, while energy consumption was reduced by 15% per ton of film. European and Japanese facilities lead in ESG compliance, ensuring both operational efficiency and alignment with environmental standards.

The Liquid Crystal Polymer (LCP) Films market is structured around key product types, application areas, and end-user industries, offering insights into adoption patterns and technological relevance. Product segmentation highlights differentiated film types based on thickness, flexibility, and dielectric properties, catering to diverse electronic and industrial needs. Applications span telecommunications, automotive, consumer electronics, and medical devices, reflecting the versatile utility of LCP films in high-frequency circuits, flexible displays, sensors, and diagnostic equipment. End-user insights reveal concentration in electronics manufacturers, automotive OEMs, and wearable device producers, with regional adoption patterns showing Asia-Pacific leading in volume while North America leads in early technology integration. Understanding these segments allows decision-makers to identify strategic investment areas and emerging market opportunities.

The Liquid Crystal Polymer (LCP) Films market is divided into extruded films, cast films, and laminated films. Extruded films currently lead adoption, accounting for 48% of the market due to their superior uniformity, thermal stability, and ease of integration into high-frequency electronic components. Cast films, while slightly smaller at 32% adoption, are witnessing the fastest growth because of their enhanced dielectric properties and compatibility with flexible electronics, with significant adoption expected by 2033. Laminated films hold a combined 20% share, primarily used in niche applications such as medical devices and aerospace components requiring multi-layer insulation.

Telecommunications dominate LCP film applications, representing 44% of overall usage due to the material’s low signal loss and thermal resistance in 5G connectors and antennas. The fastest-growing application is automotive electronics, driven by the rise of electric vehicles, advanced driver-assistance systems, and high-speed connectors, with adoption projected to exceed 30% of automotive-related components by 2033. Consumer electronics and medical devices account for the remaining 26% of applications, where LCP films are increasingly used in wearable devices, diagnostic sensors, and flexible displays.

Electronics manufacturers are the leading end-users, accounting for 50% of LCP film adoption, utilizing the material for high-frequency circuits, flexible printed boards, and 5G components. The fastest-growing end-user segment is electric vehicle producers, adopting LCP films for battery management systems, sensors, and power modules, with expected adoption exceeding 28% of the automotive LCP market by 2033. Other end-users include wearable device manufacturers, medical equipment producers, and aerospace companies, collectively representing 22% of adoption.

Asia-Pacific accounted for the largest market share at 46% in 2025; however, North America is expected to register the fastest growth, expanding at a CAGR of 12% between 2026 and 2033.

In 2025, Asia-Pacific consumed over 75,000 tons of Liquid Crystal Polymer (LCP) Films, with Japan, China, and South Korea leading adoption in high-frequency electronics, automotive sensors, and flexible displays. North America, with 28,000 tons in 2025, is rapidly implementing LCP films across telecom and wearable devices, reflecting 65% enterprise integration in advanced electronics. Europe accounted for 18% of total consumption, driven by Germany, France, and the UK, with regulatory compliance for low-emission manufacturing supporting market demand. South America and Middle East & Africa together contributed around 8% of global volumes, focusing primarily on industrial and media applications. High-tech adoption, government incentives, and infrastructure modernization are key drivers for regional market variations.

How are advanced electronics and regulatory frameworks shaping adoption?

North America held approximately 28% of the global Liquid Crystal Polymer (LCP) Films market in 2025, driven by strong adoption in telecommunications, wearable devices, and healthcare electronics. Key industries include 5G infrastructure, EV electronics, and medical diagnostic equipment. Government initiatives supporting high-tech manufacturing and digital transformation have encouraged enterprise adoption, particularly in California and Massachusetts. Technological trends such as AI-enabled production optimization and nano-engineered films are increasing efficiency and reliability. Local players like Rogers Corporation have expanded LCP-based flexible circuit solutions for 5G and aerospace applications. Regional consumer behavior emphasizes early adoption, with over 65% of healthcare and finance enterprises integrating advanced LCP technologies for reliability and performance.

How are regulatory pressures and innovation driving regional adoption?

Europe captured around 18% of the global Liquid Crystal Polymer (LCP) Films market in 2025, with Germany, the UK, and France as top adopters. Regulatory compliance and sustainability initiatives, including low-emission production mandates, are shaping demand for environmentally responsible LCP films. Adoption of emerging technologies such as flexible electronics and high-frequency automotive connectors is rising, particularly in Germany’s automotive hubs. BASF has introduced ultra-thin LCP films with enhanced thermal and dielectric properties for automotive and industrial applications. European consumer behavior favors high-reliability solutions, with over 60% of enterprises prioritizing explainable and sustainable LCP products in medical, industrial, and automotive sectors.

Why is high-tech manufacturing and mobile AI integration boosting adoption?

Asia-Pacific held the largest market volume at 46% in 2025, with Japan, China, and South Korea leading consumption in advanced electronics, automotive sensors, and flexible displays. Manufacturing hubs are investing heavily in LCP film production lines and precision extrusion technology. Regional technology trends include integration of LCP films in 5G devices and miniaturized wearables. Toray Industries in Japan has enhanced cast LCP films for flexible printed circuits, improving performance for over 5 million 5G devices. Consumer adoption is high, with 70% of electronics manufacturers in China and Japan implementing LCP films to improve thermal stability, signal integrity, and device durability.

How are industrial and media applications shaping market trends?

South America represented around 5% of the global Liquid Crystal Polymer (LCP) Films market in 2025, with Brazil and Argentina as the leading countries. Demand is primarily linked to industrial sensors, telecommunications, and media localization equipment. Government incentives for high-tech manufacturing and import tariffs on alternative polymers have driven LCP film adoption. Local players are beginning to introduce niche flexible circuits for industrial automation, enhancing operational efficiency. Consumer behavior shows high adoption in media and language-focused electronics, with over 55% of regional enterprises integrating LCP films for durable and reliable electronic components.

How are oil, gas, and construction sectors driving specialized demand?

The Middle East & Africa accounted for approximately 3% of the global Liquid Crystal Polymer (LCP) Films market in 2025, with the UAE and South Africa leading demand. Growth is driven by oil & gas instrumentation, telecom infrastructure, and advanced construction projects. Technological modernization includes adoption of heat-resistant and low-dielectric LCP films for sensors and flexible circuits. Local players are investing in pilot programs to integrate LCP films in energy monitoring equipment, improving accuracy by over 12%. Regional consumer behavior emphasizes industrial and large-scale enterprise adoption, with over 60% of infrastructure projects in the UAE incorporating high-performance polymer films for durability and efficiency.

Japan – 22% market share; dominance driven by high production capacity, advanced R&D, and large-scale electronics manufacturing.

China – 18% market share; high end-user demand and rapid expansion in telecom and automotive electronics applications.

The Liquid Crystal Polymer (LCP) Films market exhibits a moderately consolidated competitive environment with approximately 45 active global competitors. The top five companies, including Sumitomo Chemical, Toray Industries, Kaneka Corporation, Mitsubishi Gas Chemical, and Celanese Corporation, collectively account for nearly 68% of total market adoption. Market positioning is heavily influenced by technological innovation, strategic partnerships, and expansion of high-performance product lines. Companies are increasingly focusing on R&D initiatives, including nano-engineered films, ultra-thin cast and laminated LCP films, and flexible substrates for 5G, automotive, and wearable applications. Strategic initiatives such as joint ventures and collaborative projects have accelerated production efficiency and reduced time-to-market for advanced films. In addition, players are adopting digital transformation strategies for quality control, process automation, and supply chain optimization. Emerging innovation trends such as AI-assisted film design, energy-efficient production, and sustainable materials are shaping competitive dynamics. Regional diversification is also a key factor, with Asia-Pacific accounting for the highest production volumes and North America leading in enterprise adoption. The market’s moderate fragmentation allows for both established leaders and agile newcomers to capture specialized niches, particularly in EV electronics, medical devices, and flexible circuits.

Mitsubishi Gas Chemical

Celanese Corporation

Polyplex Corporation

SKC Inc.

Sekisui Chemical Co., Ltd.

DuPont de Nemours

LG Chem

The Liquid Crystal Polymer (LCP) Films market is being shaped by both current and emerging technologies that enhance performance, reliability, and application versatility. Nano-engineered LCP films are at the forefront, offering up to 25% improvement in thermal stability and dielectric performance compared to conventional films, enabling high-frequency 5G circuits and miniaturized electronics. Ultra-thin cast and laminated films are increasingly adopted, accounting for approximately 38% of LCP film production in advanced electronics due to their flexibility and superior mechanical strength.

Digital transformation and automation in manufacturing processes are improving precision and reducing production defects. AI-assisted extrusion and casting technologies have been implemented in over 50% of high-volume production facilities in Japan and South Korea, reducing scrap rates by 15% and enhancing uniformity in film thickness. Flexible substrate integration is expanding rapidly, particularly for wearable electronics, automotive sensors, and medical diagnostic devices, where approximately 42% of new flexible PCBs incorporate LCP films to ensure durability under mechanical stress.

Emerging technologies, such as laser-assisted micro-patterning and 3D-enabled LCP film structuring, are enabling the production of next-generation high-density circuits. Additionally, advancements in low-dielectric, high-temperature-resistant formulations are improving energy efficiency and signal integrity in EV connectors and aerospace components. Sustainability-focused innovations, including recycled polymer incorporation and energy-efficient thermal treatment processes, are being applied in 20–25% of production lines across Europe and North America, aligning technology adoption with ESG standards. Overall, technological evolution in the LCP films market is driving higher performance, broader applications, and operational efficiency for enterprise-scale deployments.

• In September 2025, Kuraray Co., Ltd. acquired ISCC PLUS certification at three production sites in Japan, establishing a certified sustainable supply chain for vinyl acetate-related products and enhancing its capability to supply eco‑friendly polymer materials globally, supporting broader sustainability commitments. (kuraray.com)

• In March 2025, Mitsubishi Gas Chemical completed the acquisition of JNC Corporation’s LCP film business, expanding its global footprint and product portfolio in high‑performance LCP films and laminates for advanced electronics and automotive applications.

• In July 2025, Polyplastics launched a new LCP laminate film designed for ultra‑high‑frequency communications, addressing 5G and satellite system demands with enhanced performance characteristics in signal transmission.

• In 2024, Toray Industries introduced a new LCP laminate for automotive applications, focusing on lightweight and high‑strength properties to improve performance in electric vehicles and advanced driver‑assistance systems (ADAS).

The scope of the Liquid Crystal Polymer (LCP) Films Market Report covers comprehensive evaluations of market segments, technologies, and regional footprints to guide strategic decision‑making. The report assesses key product types, including extruded, cast, and laminated LCP films, and provides extensive application insights across telecommunications, automotive electronics, consumer devices, and medical diagnostics. It examines end‑use industries, highlighting adoption patterns among electronics manufacturers, automotive OEMs, and wearable tech developers, with quantified regional consumption volumes in Asia‑Pacific, North America, Europe, South America, and Middle East & Africa.

Analyses include detailed regional segmentation, documenting production capacities, infrastructure development, and technological innovation hubs in Japan, China, South Korea, the U.S., and EU markets. The report also evaluates emerging technology integrations, such as nano‑engineered films for high‑frequency and flexible applications, AI‑assisted manufacturing processes, and sustainability‑focused film lines. Regulatory and ESG frameworks influencing market dynamics—such as environmental compliance requirements and sustainable material certifications—are covered, along with consumer behavior variations across different regions.

In addition, the scope encompasses niche market segments like ultra‑thin films (<20 µm), LCP laminates, and bio‑based or recyclable polymer variants, providing actionable insights for capacity planning, supply chain strategy, and new product development. The report’s breadth enables stakeholders to benchmark competitive landscapes, identify growth opportunities, and anticipate future trends in materials innovation and application deployment.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

16.7% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Sumitomo Chemical, Toray Industries, Kaneka Corporation, Mitsubishi Gas Chemical, Celanese Corporation, Polyplex Corporation, SKC Inc., Sekisui Chemical Co., Ltd., DuPont de Nemours, LG Chem |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |