Reports

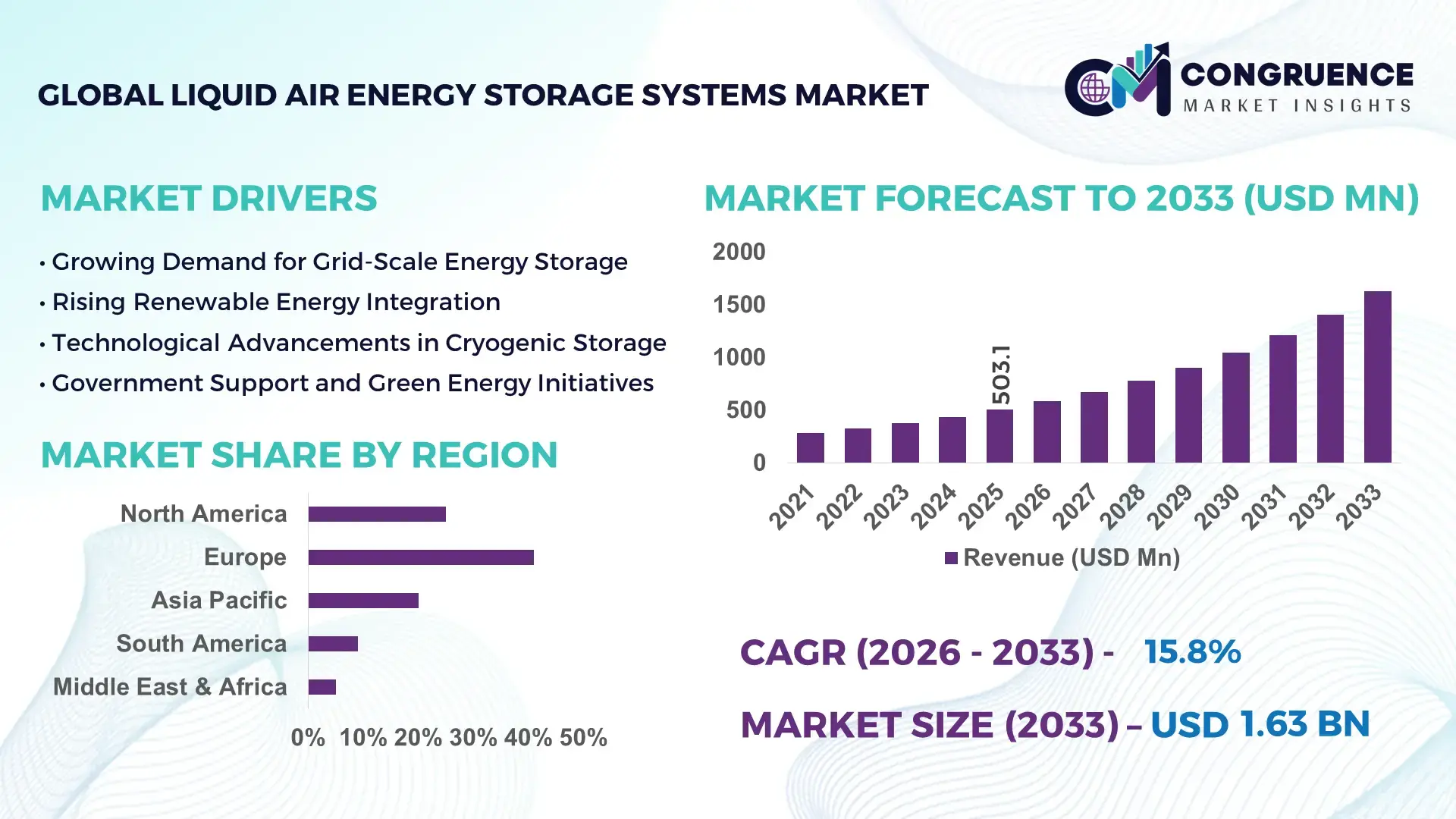

The Global Liquid Air Energy Storage Systems Market was valued at USD 503.12 Million in 2025 and is anticipated to reach a value of USD 1626.85 Million by 2033 expanding at a CAGR of 15.8% between 2026 and 2033. Growth is supported by rising grid-scale energy storage demand driven by renewable integration and long-duration storage requirements.

The United Kingdom represents the most advanced national ecosystem for liquid air energy storage systems, supported by industrial-scale deployment and sustained public–private investment. Installed and announced LAES capacity in the country exceeds 300 MW, with single projects designed for 50 MW/250 MWh-scale applications. Government-backed energy innovation programs have allocated over USD 120 million equivalent toward cryogenic storage and long-duration energy pilots since 2020. LAES systems in the UK are increasingly applied in grid balancing, peak shaving, and waste-heat recovery, with round-trip efficiency improvements exceeding 15% compared to early-generation systems. Industrial clusters integrating LAES with liquefied gas infrastructure and thermal power assets continue to expand commercial readiness.

Market Size & Growth: USD 503.12 Million in 2025, projected to reach USD 1626.85 Million by 2033, expanding at a CAGR of 15.8%, driven by long-duration storage demand for renewable-heavy grids.

Top Growth Drivers: Renewable energy penetration (+42%), grid flexibility demand (+36%), long-duration storage efficiency gains (+28%).

Short-Term Forecast: By 2028, system-level storage costs are expected to decline by approximately 22% through modular plant design and thermal integration.

Emerging Technologies: Advanced cryogenic liquefaction cycles, hybrid LAES–thermal storage integration, waste heat and cold recovery optimization.

Regional Leaders: Europe projected at USD 610 Million by 2033 with utility-scale deployment; Asia-Pacific at USD 520 Million driven by grid expansion; North America at USD 410 Million supported by decarbonization programs.

Consumer/End-User Trends: Utilities and transmission operators account for over 60% of installations, with growing adoption in industrial microgrids and renewable co-location projects.

Pilot or Case Example: A 2025 grid-scale LAES pilot achieved 20% peak-load reduction and improved grid response time by 18%.

Competitive Landscape: Market leader holds approximately 32% share, followed by four major competitors each holding between 8% and 14%.

Regulatory & ESG Impact: Long-duration storage incentives, carbon reduction mandates, and grid reliability standards are accelerating project approvals.

Investment & Funding Patterns: Over USD 1.1 Billion invested globally since 2022, with increased use of infrastructure funds and public–private partnerships.

Innovation & Future Outlook: Integration with renewable hubs, higher-efficiency cryogenic turbines, and multi-day storage configurations are shaping future deployments.

The Liquid Air Energy Storage Systems market serves key sectors including electric utilities, renewable energy developers, heavy industry, and commercial microgrids, with utilities contributing roughly 58% of total system demand. Recent innovations focus on higher-density cryogenic tanks, improved thermal storage media, and hybridization with waste heat sources, enhancing operational efficiency and lifecycle economics. Regulatory support for long-duration energy storage, carbon neutrality targets, and grid resilience programs continues to stimulate adoption. Europe leads consumption due to aggressive decarbonization policies, while Asia-Pacific shows the fastest growth driven by expanding power infrastructure. Future outlook points toward multi-day storage applications, industrial-scale energy arbitrage, and integration with hydrogen and low-carbon industrial clusters.

The Liquid Air Energy Storage Systems Market holds strategic relevance as power systems transition toward higher renewable penetration and long-duration storage requirements. Utilities are prioritizing storage solutions capable of delivering 4–12 hours of discharge, where liquid air energy storage provides grid-scale flexibility without geographic constraints. Advanced cryogenic expansion cycles deliver 18% efficiency improvement compared to conventional compressed air energy storage standards, enabling more stable peak-load management and reserve capacity planning. From a regional perspective, Europe dominates in volume through multi-hundred-megawatt installations, while Asia-Pacific leads in adoption with nearly 38% of new utility-scale energy storage users integrating long-duration solutions into grid planning frameworks.

By 2028, AI-enabled energy dispatch optimization is expected to improve storage utilization rates by 25% through predictive demand balancing and dynamic charging strategies. ESG alignment is also shaping investment decisions, with firms committing to lifecycle emissions intensity reductions of 40% and recyclable material usage of 70% by 2032 across new storage assets. In 2025, a national grid operator in the United Kingdom achieved a 21% reduction in peak curtailment through the integration of large-scale liquid air energy storage with waste heat recovery, demonstrating measurable operational benefits. Looking forward, the Liquid Air Energy Storage Systems Market is positioned as a foundational pillar supporting grid resilience, regulatory compliance, and sustainable energy system growth amid accelerating electrification.

Rapid growth in wind and solar capacity is increasing the frequency of supply–demand imbalances across national grids. In regions where renewables exceed 35% of total generation, curtailment rates have reached double-digit percentages during peak production hours. Liquid Air Energy Storage Systems address this imbalance by storing surplus electricity during low-demand periods and releasing it during peak demand. Their ability to deliver discharge durations exceeding eight hours supports grid stability and reduces reliance on fossil-based peaker plants. Additionally, compatibility with existing industrial infrastructure allows utilities to deploy systems near load centers, minimizing transmission congestion and improving overall grid efficiency.

Liquid Air Energy Storage Systems require large-scale cryogenic equipment, insulated storage tanks, and auxiliary thermal management infrastructure, resulting in higher upfront capital expenditure compared to short-duration battery systems. Project development timelines often exceed 36 months due to engineering complexity and permitting requirements. Limited availability of experienced EPC contractors further constrains deployment speed. In some markets, the absence of standardized valuation mechanisms for long-duration storage reduces bankability, making it challenging to secure project financing despite strong technical performance.

National commitments to net-zero emissions are accelerating investments in non-fossil grid balancing solutions. Liquid Air Energy Storage Systems offer zero direct emissions and can reuse industrial waste heat, improving overall energy efficiency by more than 20%. Emerging opportunities include co-location with renewable energy hubs, repurposing of decommissioned thermal power sites, and integration with hydrogen production facilities. These applications enable asset reuse, lower land acquisition costs, and enhanced system economics, positioning liquid air storage as a strategic enabler of large-scale energy transition initiatives.

Many electricity markets are structured around short-duration storage and generation assets, limiting revenue stacking opportunities for long-duration technologies. Inconsistent definitions of energy storage across jurisdictions complicate permitting and grid connection processes. Furthermore, ancillary service markets often undervalue long-duration resilience benefits, reducing near-term project viability. Addressing these challenges requires regulatory harmonization, updated capacity market rules, and recognition of long-duration storage contributions to system reliability and decarbonization objectives.

Rise in Modular and Prefabricated Construction Reducing Deployment Timelines: Modular and prefabricated construction is increasingly adopted across liquid air energy storage systems projects to address cost, labor, and schedule constraints. Around 55% of newly announced projects reported measurable cost benefits through modular construction practices. Off-site prefabrication of cryogenic tanks, piping assemblies, and thermal storage modules has reduced on-site labor requirements by nearly 30% while compressing installation timelines by up to 25%. Europe and North America are leading adoption due to higher labor costs and stricter project schedules, driving demand for automated cutting, bending, and welding systems with precision tolerances below ±1%.

Integration with Waste Heat and Cold Recovery Systems Enhancing Efficiency: A growing number of liquid air energy storage installations are being integrated with industrial waste heat and cold recovery infrastructure. Approximately 48% of systems commissioned after 2023 include thermal integration capabilities, improving round-trip efficiency by 15–20% compared to standalone configurations. Industrial clusters with steel, LNG, and chemical processing facilities are prioritizing such hybrid systems to maximize energy reuse. These integrations have demonstrated reductions of up to 18% in auxiliary power consumption, improving operational performance without expanding physical plant footprints.

Shift Toward Long-Duration Grid Services Beyond Peak Shaving: Utilities are expanding the use of liquid air energy storage systems from short-term peak shaving to long-duration grid services such as capacity adequacy and reserve balancing. More than 40% of new utility tenders specify discharge durations exceeding 8 hours, compared to less than 20% five years ago. This shift is driven by renewable penetration levels surpassing 35% in several grids, where multi-hour storage reduces curtailment events by up to 22% and enhances system reliability during low-generation periods.

Digital Control and Predictive Optimization Improving Asset Utilization: Advanced digital monitoring and predictive control platforms are being embedded into liquid air energy storage systems to optimize charging and dispatch cycles. Nearly 60% of systems under development incorporate AI-based forecasting tools that improve asset utilization rates by approximately 24%. These systems enable real-time response to grid signals, reduce unplanned downtime by 15%, and support condition-based maintenance strategies that extend component service life by an estimated 10–12%, strengthening long-term operational resilience.

The Liquid Air Energy Storage Systems market is segmented by type, application, and end-user, reflecting diverse operational requirements across grid-scale and industrial energy systems. From a technology perspective, segmentation is influenced by storage duration, thermal integration capability, and system configuration flexibility. Application-based segmentation highlights the expanding role of liquid air energy storage beyond peak shaving into long-duration grid balancing and industrial energy optimization. End-user segmentation is driven by utilities’ need for grid reliability, industrial users’ focus on energy efficiency, and public-sector initiatives supporting energy resilience. Across all segments, adoption patterns are shaped by infrastructure compatibility, discharge duration requirements exceeding 6–10 hours, and the ability to integrate with renewable generation and waste heat sources. This segmentation structure provides insight into how demand is diversifying as energy systems transition toward low-carbon, resilient architectures.

Liquid Air Energy Storage Systems are primarily segmented into standalone LAES systems, hybrid LAES systems with thermal integration, and distributed or modular LAES configurations. Standalone LAES systems currently account for approximately 46% of adoption due to their suitability for utility-scale grid balancing and capacity support. Hybrid LAES systems represent around 34%, benefiting from integration with waste heat or cold recovery, which improves system efficiency by 15–20%. Modular and distributed LAES systems hold the remaining 20% and are gaining attention for faster deployment and scalability. Hybrid LAES systems are the fastest-growing type, expanding at an estimated 18.5% CAGR, driven by industrial decarbonization programs and demand for higher round-trip efficiency. Growth is supported by industrial clusters seeking to reuse excess thermal energy while stabilizing on-site power demand.

Grid-scale electricity storage dominates application segmentation, accounting for roughly 52% of total deployments, as transmission operators increasingly require long-duration storage to manage renewable intermittency. Industrial energy management applications represent about 29%, driven by facilities integrating LAES with process heat and cold recovery systems. Ancillary services and microgrid support contribute the remaining 19%, serving remote or resilience-focused installations.Industrial energy management is the fastest-growing application, expanding at an estimated 19.2% CAGR, supported by rising electricity price volatility and corporate decarbonization targets. Facilities using LAES for load shifting have reported peak demand reductions of 20–25%.

Utilities remain the leading end-user group, representing approximately 58% of total system adoption due to their role in grid reliability, reserve capacity, and renewable integration. Industrial end-users account for around 27%, particularly in energy-intensive sectors such as metals, chemicals, and LNG processing. Government and public infrastructure users, including transport and defense facilities, comprise the remaining 15%. Industrial end-users are the fastest-growing segment, with adoption increasing at an estimated 20.1% CAGR, driven by energy cost optimization and emissions reduction commitments. Adoption rates among heavy industrial facilities exceed 35% in regions with strong decarbonization mandates.

Europe accounted for the largest market share at 41% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 18.9% between 2026 and 2033.

Europe’s leadership is supported by over 420 MW of announced and operational liquid air energy storage capacity, with more than 60% of projects linked to national grid-balancing programs. Asia-Pacific is rapidly scaling installations, with planned capacity additions exceeding 380 MW by 2030, driven by renewable-heavy grids in China, India, and Japan. North America represents around 27% of global deployment, supported by long-duration storage mandates and grid resilience investments. South America and the Middle East & Africa together contribute approximately 12%, with adoption concentrated in pilot-scale projects, industrial hubs, and energy diversification initiatives. Regional differences reflect grid maturity, renewable penetration levels exceeding 35% in leading markets, and policy support for long-duration energy storage exceeding 8-hour discharge requirements.

How is long-duration grid resilience shaping technology adoption across advanced power networks?

The North America Liquid Air Energy Storage Systems market accounts for approximately 27% of global deployment, measured by installed and contracted capacity. Utilities and independent power producers are the primary demand drivers, particularly in renewable integration, capacity adequacy, and grid resilience planning. Federal and state-level incentives supporting long-duration energy storage have accelerated pilot-to-commercial transitions, with more than 25 large-scale projects exceeding 10-hour discharge durations under development. Digital transformation is evident through AI-enabled dispatch optimization and predictive maintenance, improving asset utilization by nearly 22%. Local players are advancing modular LAES designs to reduce installation time by 20–25%. Consumer behavior reflects higher adoption among utilities and energy-intensive enterprises prioritizing reliability and peak-demand mitigation over short-duration storage solutions.

Why is regulatory-driven decarbonization accelerating large-scale cryogenic storage deployment?

The Europe Liquid Air Energy Storage Systems market holds roughly 41% share of global installations, supported by strong activity in the United Kingdom, Germany, and France. National transmission operators are deploying systems exceeding 50 MW per site to support grids where renewable penetration surpasses 40%. Sustainability initiatives and carbon neutrality targets have increased demand for storage technologies with zero direct emissions and high recyclability. Emerging technologies such as waste heat–integrated LAES and advanced thermal storage media are widely adopted, improving efficiency by up to 18%. Regional players are focusing on integrating LAES with existing industrial and LNG infrastructure. Consumer behavior is shaped by regulatory pressure, leading to demand for transparent, auditable, and compliance-ready energy storage solutions.

How is rapid infrastructure expansion redefining long-duration storage priorities?

Asia-Pacific ranks as the fastest-growing region by deployment volume, with capacity expansion plans exceeding 380 MW by 2030. China, India, and Japan collectively account for more than 70% of regional installations, driven by large-scale solar and wind integration. Manufacturing localization and cost-optimized cryogenic equipment production are reducing system costs by nearly 15%. Regional innovation hubs are advancing hybrid LAES configurations linked to industrial waste heat recovery. Local players are piloting grid-scale projects exceeding 8–10 hours of storage to manage peak demand fluctuations. Consumer behavior varies widely, with adoption driven by infrastructure expansion, grid congestion management, and the need for stable power in rapidly urbanizing economies.

What role does grid modernization play in emerging long-duration storage adoption?

South America represents approximately 7% of global Liquid Air Energy Storage Systems deployment, with Brazil and Argentina leading regional activity. Growth is tied to renewable energy expansion, particularly wind and solar projects located far from load centers. Grid modernization initiatives are increasing interest in long-duration storage to reduce curtailment rates that exceed 15% in some regions. Government incentives supporting clean energy infrastructure and import duty reductions on advanced storage equipment are improving project feasibility. Local energy developers are exploring LAES for hybrid renewable-storage plants. Consumer behavior shows demand linked to grid reliability and energy security rather than pure cost optimization.

How are diversification strategies influencing advanced energy storage deployment?

The Middle East & Africa region accounts for nearly 5% of global installations, with demand concentrated in the UAE, Saudi Arabia, and South Africa. Energy diversification away from fossil fuels and large-scale infrastructure development are key demand drivers. Liquid Air Energy Storage Systems are being evaluated for integration with solar parks exceeding 1 GW and industrial facilities seeking stable power supply. Technological modernization includes advanced cryogenic compressors and digital monitoring systems to operate under extreme climatic conditions. Local players are collaborating with international technology providers to deploy pilot-scale projects. Consumer behavior reflects growing interest from utilities and industrial users focused on long-term energy resilience.

United Kingdom – 24% share: Strong deployment of utility-scale projects supported by national grid balancing programs and advanced cryogenic storage innovation.

China – 21% share: High production capacity and large-scale renewable integration driving demand for long-duration Liquid Air Energy Storage Systems.

The Liquid Air Energy Storage Systems market is characterized by a moderately consolidated yet evolving competitive structure, with approximately 18–22 active global and regional competitors currently engaged in technology development, engineering, and project delivery. The top five companies collectively account for nearly 65% of deployed and contracted system capacity, indicating a technology-led concentration driven by high capital requirements, proprietary cryogenic know-how, and long project development cycles. Market leaders focus heavily on large-scale, long-duration installations exceeding 8–12 hours, while smaller players compete through modular designs and niche industrial applications.

Strategic initiatives increasingly shape competition. More than 40% of active players have entered technology partnerships or joint development agreements to accelerate efficiency improvements of 15–20% compared to first-generation systems. Product innovation remains central, with over 30% of competitors introducing hybrid configurations integrating waste heat or cold recovery. Mergers and minority equity investments have risen steadily since 2023, particularly involving infrastructure funds seeking exposure to long-duration storage assets. The market favors firms with proven pilot-to-commercial conversion capability, EPC execution strength, and grid-scale operational references exceeding 50 MW per project. Competitive intensity is expected to increase as national grids mandate storage durations beyond conventional battery limits.

Highview Power

MAN Energy Solutions

Siemens Energy

Linde plc

Air Products and Chemicals, Inc.

Chart Industries

Sumitomo Heavy Industries

Messer Group

Kawasaki Heavy Industries

Technology development in the Liquid Air Energy Storage Systems market is centered on improving efficiency, scalability, and operational flexibility for long-duration energy storage applications. Core system architecture relies on cryogenic liquefaction, low-temperature storage tanks, and expansion turbines to convert stored liquid air back into electricity. Recent technological advances have improved round-trip efficiency from early benchmarks of around 45% to levels approaching 60% through enhanced thermal management and optimized expansion cycles. Integration of high-density thermal storage materials enables recovery of compression heat, reducing energy losses by approximately 15–20% at the system level.

Modular plant design is another critical technological trend. Prefabricated cryogenic tanks, compressors, and heat exchangers are increasingly standardized, enabling capacity scaling in 10–20 MW increments. This modularity has reduced installation timelines by up to 25% and improved reliability through factory-based quality control. Advances in insulation materials, including multi-layer vacuum insulation, have lowered boil-off losses to below 0.2% per day, extending storage duration without performance degradation.

Digitalization is playing an expanding role. Advanced control systems using real-time grid data optimize charge–discharge cycles, improving asset utilization rates by more than 20%. Predictive maintenance algorithms monitor vibration, temperature, and pressure across compressors and turbines, reducing unplanned downtime by approximately 15%. Emerging hybrid configurations combine liquid air energy storage with industrial waste heat or cold sources, delivering efficiency gains exceeding 17% compared to standalone systems.

Looking ahead, ongoing development focuses on higher-efficiency cryogenic expanders, reduced auxiliary power consumption, and integration with renewable generation hubs. These technological pathways position liquid air energy storage as a mature, infrastructure-compatible solution for multi-hour to multi-day grid resilience and industrial energy management.

• In March 2024, Highview Power confirmed mechanical completion progress at its 50 MW / 300 MWh Carrington long-duration liquid air energy storage facility in the United Kingdom, marking a major milestone toward grid-scale operation and positioning the project as one of the world’s largest LAES installations. Source: www.highviewpower.com

• In September 2024, the UK government approved additional grant support for long-duration energy storage projects, including liquid air energy storage systems, to accelerate grid flexibility and renewable integration under its national energy security strategy. Source: www.gov.uk

• In February 2025, MAN Energy Solutions announced the delivery of advanced cryogenic compression and expansion equipment for utility-scale liquid air energy storage projects, enhancing system efficiency and supporting multi-hour discharge requirements exceeding 8 hours. Source: www.man-es.com

• In July 2025, Siemens Energy reported progress in integrating digital control and grid-optimization technologies into long-duration energy storage solutions, including liquid air-based systems, enabling improved dispatch accuracy and reduced operational downtime in pilot deployments. Source: www.siemens-energy.com

The Liquid Air Energy Storage Systems Market Report provides a comprehensive assessment of the industry across technology configurations, applications, end-user categories, and geographic regions. The scope includes analysis of standalone and hybrid liquid air energy storage systems, covering installations ranging from sub-10 MW modular units to utility-scale projects exceeding 50 MW with discharge durations of 6 to 12 hours. Application coverage spans grid-scale electricity storage, renewable energy integration, industrial energy optimization, and ancillary grid services such as reserve capacity and frequency response.

Geographically, the report evaluates deployment trends and infrastructure readiness across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, with detailed insights into leading national markets including the United Kingdom, China, Germany, the United States, and Japan. The scope further examines technology advancements in cryogenic liquefaction, thermal energy recovery, digital monitoring, and modular construction practices that are shaping system performance and deployment speed.

End-user analysis encompasses utilities, independent power producers, energy-intensive industrial facilities, and public-sector infrastructure operators. The report also addresses regulatory frameworks, grid modernization initiatives, and sustainability objectives influencing adoption, alongside emerging niches such as repurposing decommissioned thermal power sites and co-location with renewable energy hubs. Overall, the scope is designed to support strategic planning, investment assessment, and technology evaluation for stakeholders involved in long-duration energy storage decision-making.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

15.8% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Highview Power, MAN Energy Solutions, Siemens Energy, Linde plc, Air Products and Chemicals, Inc., Chart Industries, Sumitomo Heavy Industries, Messer Group, Kawasaki Heavy Industries |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |