Reports

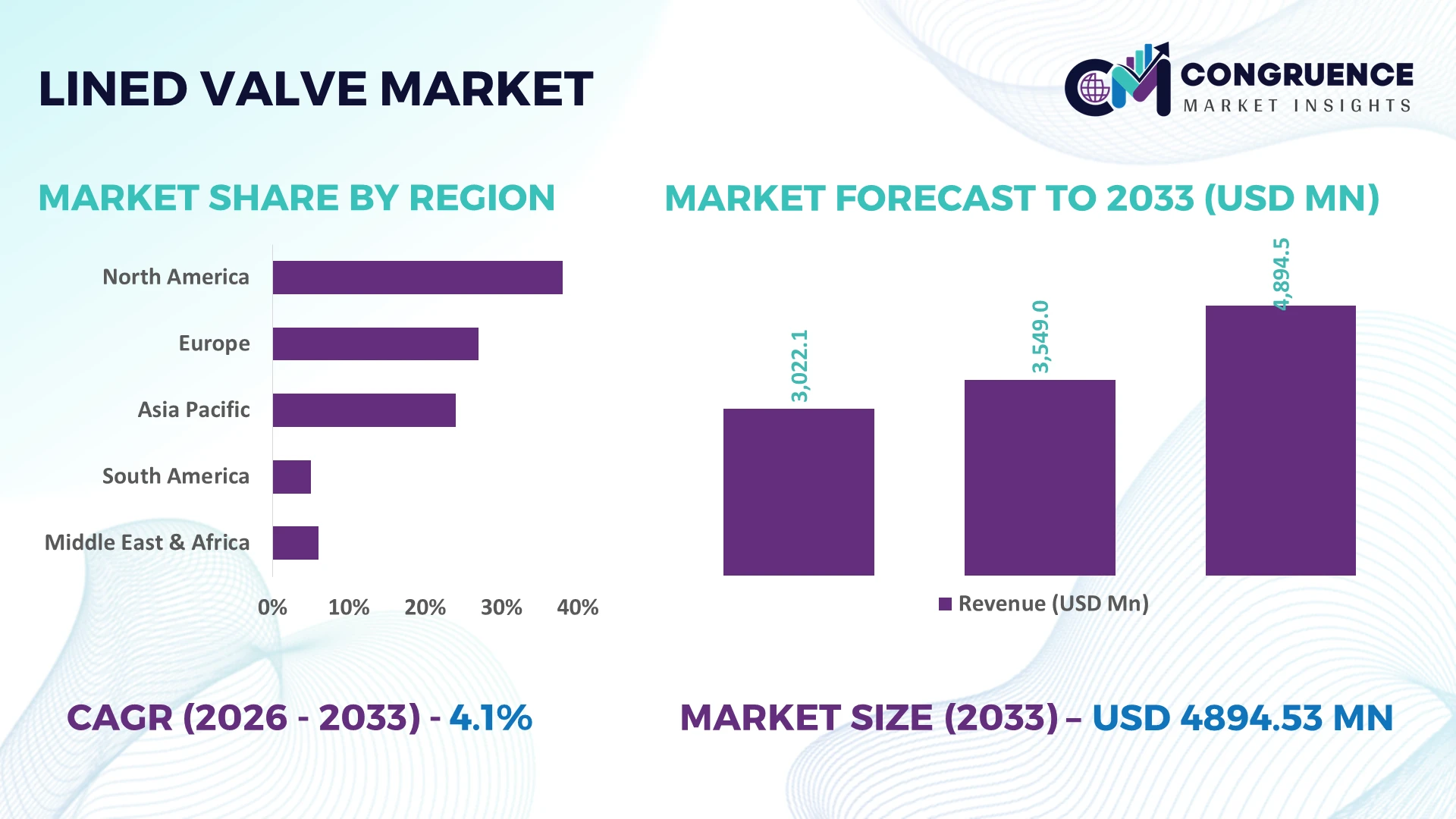

The Global Lined Valve Market was valued at USD 3549 Million in 2025 and is anticipated to reach a value of USD 4894.53 Million by 2033 expanding at a CAGR of 4.1% between 2026 and 2033. Rising investments in corrosion-resistant process infrastructure, expanding specialty chemical production, and stricter industrial emission compliance are accelerating adoption of advanced lined valves across chemical, pharmaceutical, mining, and water treatment facilities.

China leads the global lined valve market with approximately 38% of worldwide production capacity, supported by more than USD 20 billion in chemical manufacturing investments and over 65% adoption of fluoropolymer-lined flow systems across new processing facilities. India is emerging as the fastest-expanding manufacturing hub through specialty chemical expansion, while China's installed capacity remains nearly 2.7 times higher. Ongoing supply-chain diversification following Red Sea shipping disruptions continues to strengthen regional manufacturing competitiveness.

Strategic investment in localized production, high-performance fluoropolymer technologies, and smart valve solutions will determine long-term competitive positioning across global industrial markets.

Market Size & Growth: USD 3549 Million (2025) to USD 4894.53 Million (2033) at 4.1% CAGR, supported by corrosion-resistant process equipment adoption across industrial manufacturing.

Top Growth Drivers: Chemical processing (+32%), pharmaceutical manufacturing (+26%), and industrial water treatment (+19%) remain the primary demand accelerators.

Short-Term Forecast: By 2028, predictive maintenance and smart monitoring improve valve reliability by 23% while reducing maintenance costs by 17%.

Emerging Technologies: AI-enabled diagnostics, Industrial IoT monitoring, and advanced PTFE/PFA lining technologies extend operational service life by over 21%.

Regional Leaders: Asia-Pacific exceeds USD 2.2 billion, Europe approaches USD 1.1 billion, and North America surpasses USD 920 million through industrial modernization and supply-chain expansion.

Consumer/End-User Trends: More than 49% of newly commissioned chemical plants specify high-performance lined valves for corrosive media applications.

Pilot/Case Example: 2026 chemical processing facility modernization increased equipment uptime by 28% after deploying advanced fluoropolymer-lined valve systems.

Competitive Landscape: Leading manufacturers collectively account for approximately 39% market share alongside globally established industrial valve suppliers.

Regulatory & ESG Impact: Industrial emission regulations reduced fugitive leakage by nearly 16% through advanced sealing and corrosion-control technologies.

Investment & Funding: More than USD 2.5 billion is directed toward manufacturing expansion, strategic partnerships, and regional production localization amid global supply-chain shifts.

Innovation & Future Outlook: Smart asset management, lightweight composite materials, and intelligent flow monitoring are strengthening next-generation industrial valve competitiveness.

The Lined Valve Market continues to gain momentum across specialty chemicals, pharmaceuticals, mining, semiconductor manufacturing, and industrial water treatment where corrosion resistance directly improves operational reliability. Advanced fluoropolymer linings, digital condition monitoring, and predictive maintenance platforms are increasing equipment availability by nearly 20%. Growing localization of industrial supply chains and tighter environmental compliance requirements in 2026 are reshaping procurement priorities, setting the stage for the strategic market discussion.

The lined valve market has become strategically important as process industries prioritize corrosion-resistant infrastructure to improve plant reliability, reduce lifecycle costs, and comply with increasingly stringent environmental regulations. Industrial supply-chain restructuring following global logistics disruptions has encouraged manufacturers to localize production while expanding sourcing partnerships for fluoropolymer materials. This transition is strengthening competitive positioning across chemical processing, pharmaceuticals, semiconductor manufacturing, and high-purity industrial applications where operational continuity is critical.

Advanced PTFE- and PFA-lined valves deliver up to 25% longer service life and reduce maintenance interventions by nearly 20% compared with conventional metal valves operating in highly corrosive environments. China continues to lead large-scale manufacturing through integrated chemical production clusters, while Germany emphasizes precision-engineered valve systems with higher levels of automation and digital diagnostics. During the next two to three years, smart condition monitoring is expected to exceed 35% adoption across newly commissioned high-value processing facilities, improving maintenance planning and reducing unplanned shutdowns.

A 2026 specialty chemical plant modernization program demonstrated a 22% reduction in maintenance downtime after replacing legacy valves with digitally monitored lined valve systems. Manufacturers are expanding localized production, investing in advanced lining technologies, and strengthening engineering partnerships to deliver customized process solutions. Companies that integrate digital monitoring with high-performance corrosion protection will establish stronger competitive differentiation and long-term operational resilience.

Rapid expansion of specialty chemicals, pharmaceuticals, and industrial water treatment is increasing demand for high-performance lined valves capable of handling aggressive media. More than 62% of new chemical processing projects specify corrosion-resistant flow-control equipment, while predictive maintenance deployment has improved equipment availability by approximately 18%. India's specialty chemical capacity expansion and China's refinery modernization programs continue to accelerate procurement of advanced lined valves. In response, manufacturers are increasing fluoropolymer production, expanding regional assembly facilities, and developing smart valve portfolios with integrated diagnostics. The strategic shift from replacement-based procurement to lifecycle optimization is enabling suppliers to secure higher-value industrial contracts and strengthen long-term customer relationships.

Price volatility in fluoropolymer raw materials continues to pressure production economics, with material costs fluctuating by nearly 15% in recent procurement cycles. Around 40% of high-performance lining materials remain dependent on concentrated supplier networks, increasing sourcing complexity for valve manufacturers. Environmental compliance requirements for fluoropolymer processing have also extended qualification timelines for new production facilities in several industrial markets. Companies are mitigating these pressures through multi-country sourcing strategies, localized manufacturing investments, and long-term procurement agreements. Strengthening regional supply resilience has become a strategic priority to stabilize production schedules, protect operating margins, and improve delivery reliability for industrial customers.

Digital transformation is creating significant opportunities for intelligent lined valve solutions combining corrosion resistance with predictive maintenance capabilities. Industrial facilities deploying connected valve monitoring have reported maintenance cost reductions approaching 20% and inspection efficiency improvements exceeding 25%. Japan and South Korea are accelerating adoption of Industrial IoT platforms across semiconductor and precision manufacturing facilities, creating demand for digitally enabled process equipment. Manufacturers are expanding R&D programs focused on embedded sensors, remote diagnostics, and digital asset management while partnering with industrial automation providers. The combination of intelligent monitoring and advanced lining technology offers differentiated value beyond conventional mechanical performance.

Expanding advanced lined valve deployment requires specialized engineering expertise, digital integration capability, and standardized maintenance practices across complex industrial facilities. Approximately 34% of industrial operators report shortages of qualified maintenance personnel for intelligent valve systems, while digital integration projects increase commissioning timelines by nearly 18%. Germany and the United States continue to experience rising demand for multidisciplinary engineering resources supporting automated process facilities. Manufacturers must strengthen technical training, expand digital engineering partnerships, and develop standardized software interoperability to ensure consistent deployment quality. Long-term competitiveness will depend on combining advanced materials expertise with scalable digital service capabilities across global industrial operations.

Digital Valve Intelligence Expansion: Industrial operators are integrating smart sensors and predictive diagnostics into lined valves, with connected asset deployment increasing by nearly 34% and maintenance inspections declining by 21%. Germany and Japan are accelerating digital plant modernization as skilled maintenance shortages intensify. Manufacturers are expanding automation partnerships and embedding remote monitoring capabilities, enabling faster maintenance planning, lower downtime, and more efficient lifecycle management across corrosion-intensive processing facilities.

Localized Manufacturing Networks: Supply-chain restructuring continues to reshape production strategies, with over 40% of manufacturers increasing regional sourcing and localized assembly while reducing average component lead times by approximately 18%. Continued logistics uncertainty and industrial resilience initiatives are driving this transition. Companies are expanding domestic production capacity, qualifying multiple fluoropolymer suppliers, and strengthening strategic procurement agreements to improve delivery reliability and operational continuity.

Advanced Fluoropolymer Material Adoption: High-performance PFA and modified PTFE linings are replacing conventional materials across critical processing applications, extending valve service life by nearly 24% while reducing leakage incidents by approximately 16%. Pharmaceutical and semiconductor facilities increasingly require ultra-high-purity flow systems. Manufacturers are investing in material engineering, precision molding technologies, and collaborative product development to deliver customized corrosion-resistant solutions with longer maintenance intervals.

Lifecycle Service Business Models: Industrial buyers are shifting from product-based procurement toward lifecycle service contracts, with service-based agreements growing by roughly 29% and planned maintenance compliance exceeding 70% across large processing facilities. Rising regulatory oversight and asset optimization targets are supporting this transition. Valve manufacturers are expanding digital service platforms, performance monitoring programs, and engineering support partnerships, creating recurring customer engagement while improving operational efficiency and long-term equipment reliability.

Ball Valves represent the dominant segment because they combine reliable shutoff performance, low maintenance requirements, and compatibility with aggressive chemical media across continuous processing environments. Nearly 42% of new industrial flow-control installations utilize lined ball valves due to their operational efficiency and ease of automation. Diaphragm Valves are the fastest-growing segment as pharmaceutical and semiconductor manufacturers increasingly require contamination-free fluid handling and higher purity standards. Companies are expanding fluoropolymer-lined product portfolios while improving sealing technologies to meet evolving industrial specifications.

Butterfly Valves maintain relevance in large-diameter water and chemical transfer systems where installation costs remain competitive, while Plug Valves continue serving specialized corrosive process applications requiring dependable isolation. Gate Valves retain importance within high-capacity industrial infrastructure despite slower adoption in automated facilities. Manufacturers are strengthening production capabilities, introducing modular valve platforms, and expanding engineering partnerships to address application-specific requirements while shifting investments toward digitally compatible product designs.

Chemical Processing is the leading application segment because corrosive media handling, continuous production cycles, and strict process reliability requirements create sustained demand for lined valves. Approximately 46% of installed lined valves operate within chemical production facilities. Pharmaceuticals represent the fastest-growing application as sterile manufacturing expansion and higher purity standards accelerate deployment of fluoropolymer-lined systems. Companies are introducing specialized valve configurations, expanding validation services, and integrating intelligent monitoring technologies to improve process control and regulatory compliance.

Water Treatment continues expanding through industrial wastewater modernization and desalination investments, while Oil & Gas maintains stable demand for corrosion-resistant process equipment in aggressive fluid environments. Power Generation increasingly adopts lined valves for chemical dosing and emissions-control systems supporting operational efficiency. Suppliers are strengthening regional manufacturing, investing in customized engineering, and expanding service capabilities to meet evolving customer requirements across diversified industrial applications.

The Chemical Industry remains the largest end-user because continuous exposure to aggressive chemicals requires highly reliable corrosion-resistant flow-control systems throughout production assets. Nearly 48% of industrial lined valve purchases originate from chemical manufacturing operations. Pharmaceutical Companies represent the fastest-growing buyer group as expansion of sterile production, biologics manufacturing, and high-purity processing increases demand for precision-engineered lined valves. Manufacturers are responding through customized product development, validation support, and collaborative engineering partnerships tailored to regulated production environments.

Oil & Gas continues investing in specialized corrosion management for selected processing applications, while Water Utilities increasingly deploy lined valves to improve infrastructure durability and minimize maintenance requirements. Power Plants remain important buyers for chemical handling and water treatment operations supporting reliable plant performance. Suppliers are expanding localized inventories, strengthening aftermarket services, and offering application-specific product configurations to improve customer retention and competitive differentiation across diverse industrial sectors.

Asia-Pacific accounted for the largest market share at 43.8% in 2025 however, North America is expected to register the fastest growth, expanding at a 4.8% CAGR between 2026 and 2033.

Digital modernization strengthens process reliability

North America is accelerating lined valve deployment through modernization of chemical processing, pharmaceutical manufacturing, and industrial water infrastructure. The region accounts for approximately 24% of global demand, supported by high adoption of automated process control and predictive maintenance systems. More than 45% of newly upgraded chemical plants now integrate digitally monitored lined valves to improve asset utilization and reduce maintenance frequency. Investments in resilient domestic manufacturing and localized engineering services continue to improve procurement flexibility while strengthening industrial supply chains. Companies are expanding production partnerships and application engineering capabilities to address increasing demand for corrosion-resistant process equipment.

United States Market Outlook: The United States remains the regional leader through its extensive chemical manufacturing base, advanced pharmaceutical production, and large industrial water treatment network. More than 60% of North American lined valve installations are concentrated in the country, supported by continuous plant modernization and automation investments. Domestic manufacturers are expanding engineered valve production, strengthening aftermarket support, and integrating intelligent monitoring technologies to improve operational reliability across high-value industrial facilities.

Sustainability and industrial modernization reshape procurement

Europe maintains a strong position through advanced industrial automation, stringent environmental regulations, and modernization of mature manufacturing facilities. The region contributes approximately 22% of global demand, with chemical and pharmaceutical industries driving specification of high-performance lined valves. More than 38% of industrial process upgrades now include corrosion-resistant flow-control systems designed to reduce leakage and maintenance requirements. Manufacturers are increasing investment in precision engineering, digital diagnostics, and environmentally compliant production technologies to strengthen long-term operational efficiency.

Germany Market Outlook: Germany leads the European market through its globally competitive chemical sector, precision engineering expertise, and advanced industrial automation ecosystem. Nearly one-third of regional industrial valve production is associated with German manufacturing facilities. Companies continue investing in digitally integrated valve systems, specialized fluoropolymer processing, and collaborative engineering programs that improve equipment reliability while supporting sustainable industrial production.

Manufacturing scale drives global leadership

Asia-Pacific remains the largest lined valve market due to rapid industrial expansion, integrated chemical production, and strong manufacturing capacity. The region represents approximately 43.8% of global market activity, supported by extensive investments in specialty chemicals, pharmaceuticals, and semiconductor manufacturing. More than 50% of newly established corrosion-intensive industrial projects are concentrated across major manufacturing hubs. Companies continue expanding localized production, strengthening export capabilities, and increasing automation within valve manufacturing operations to improve delivery efficiency and product consistency.

China Market Outlook: China dominates the regional market through its extensive chemical manufacturing infrastructure, fluoropolymer processing capability, and integrated industrial supply chains. The country accounts for more than 38% of global lined valve production capacity and continues investing in advanced manufacturing technologies. Domestic suppliers are expanding precision production facilities, increasing automation levels, and strengthening export-oriented partnerships to meet growing international industrial demand.

Industrial infrastructure upgrades stimulate demand

South America is experiencing steady demand growth driven by mining operations, chemical manufacturing, and expanding industrial water treatment infrastructure. The region contributes approximately 6% of global market activity, with modernization of industrial processing facilities supporting replacement of conventional valve systems. More than 30% of major industrial maintenance projects now prioritize corrosion-resistant equipment to improve operational continuity. Manufacturers are expanding regional distribution networks and technical service partnerships while balancing infrastructure limitations and import dependency across several industrial markets.

Brazil Market Outlook: Brazil leads regional demand through its diversified chemical industry, mining sector, and expanding industrial processing infrastructure. Large manufacturing complexes increasingly specify lined valves for corrosive media handling and long-term maintenance optimization. Companies are strengthening domestic assembly capabilities, expanding engineering services, and improving local inventory management to shorten procurement cycles and enhance support for industrial customers.

Process industry investments accelerate modernization

The Middle East & Africa market is expanding through refinery modernization, petrochemical investments, desalination projects, and industrial diversification initiatives. The region accounts for approximately 4.2% of global market demand, supported by increasing deployment of corrosion-resistant equipment across critical processing infrastructure. More than 35% of newly commissioned industrial fluid-handling projects include advanced lined valve technologies to improve operational reliability in aggressive environments. Suppliers are strengthening regional partnerships, expanding service centers, and increasing engineering support to meet evolving industrial requirements.

Saudi Arabia Market Outlook: Saudi Arabia represents the region's largest opportunity due to large-scale petrochemical expansion, industrial diversification initiatives, and continued investment in advanced processing infrastructure. Industrial operators are increasing deployment of high-performance lined valves across chemical production and water treatment facilities while expanding localized maintenance capabilities. Equipment suppliers continue establishing strategic partnerships and technical support networks to strengthen long-term participation in national industrial development programs.

The competitive landscape is shaped by Emerson Electric Co., Flowserve Corporation, Crane Company, KSB SE & Co. KGaA, and Bray International, competing against specialized regional valve manufacturers and application-focused engineering suppliers. Global leaders leverage integrated engineering, digital monitoring, and worldwide service networks, while regional manufacturers compete through faster delivery, lower production costs, and customized fluoropolymer-lined solutions. The top five players collectively account for approximately 37% of global market activity, reflecting a moderately consolidated structure. Competition increasingly depends on technology integration, localized manufacturing, and supply-chain resilience rather than pricing alone. Digitally enabled valve solutions improve maintenance efficiency by nearly 20%, while localized production shortens delivery cycles by approximately 18%. Manufacturers are expanding production capacity, forming automation partnerships, investing in advanced lining materials, and strengthening aftermarket service capabilities through vertical integration. Consolidation is accelerating as companies acquire engineering expertise and application-specific technologies. Certification requirements, fluoropolymer processing capability, and qualification cycles remain significant entry barriers. Sustainable competitive advantage depends on combining material innovation, engineering support, digital diagnostics, and resilient regional supply networks.

Emerson Electric Co.

Flowserve Corporation

Crane Company

KSB SE & Co. KGaA

Bray International

AVK Holding A/S

SAMSON AG

Velan Inc.

Richter Chemie-Technik GmbH

Asahi Yukizai Corporation

NIBCO Inc.

EBRO Armaturen GmbH

Digital monitoring, advanced fluoropolymer engineering, and intelligent automation are redefining lined valve performance across corrosion-intensive industries. AI-enabled predictive maintenance platforms reduce unplanned downtime by nearly 22%, while Industrial IoT connectivity has reached approximately 36% deployment across newly commissioned high-value processing facilities. Companies integrating digital asset management with valve diagnostics achieve faster maintenance planning, greater operational visibility, and improved process reliability compared with conventional inspection-based maintenance programs.

Advanced PFA and modified PTFE lining technologies are replacing legacy lining materials by extending operational service life by approximately 25% while lowering leakage incidents by nearly 18%. Automated quality inspection using machine vision improves manufacturing consistency by over 15% compared with traditional manual inspection methods. Premium industrial manufacturers benefit most because higher material precision and digital quality assurance strengthen product differentiation, regulatory compliance, and lifecycle performance in demanding process applications.

Between 2026 and 2028, embedded sensors, digital twins, and cloud-based asset optimization platforms will become standard features for critical process industries. More than 40% of new premium lined valve installations are expected to include intelligent monitoring capabilities supporting predictive maintenance and remote diagnostics. Companies investing now in smart manufacturing, advanced material science, and integrated engineering ecosystems will strengthen competitive positioning through superior operational reliability, faster customer response, and lower lifecycle ownership costs.

February 2026 Flowserve Corporation signed a definitive agreement to acquire Trillium Flow Technologies' Valves Division for USD 490 million, adding an installed base exceeding 200,000 valve units. The acquisition significantly strengthens Flowserve's nuclear, industrial, and critical infrastructure valve portfolio while expanding its global aftermarket capabilities. Source: flowserve.com

June 2026 Flowserve Corporation completed the acquisition of Trillium Flow Technologies' Valves Division, integrating products deployed across 115 operating nuclear reactors. The transaction expands mission-critical valve offerings and reinforces the company's competitive position in high-performance industrial flow control markets. Source: mdm.com

February 2026 Industry publication Valve World reported Flowserve's strategic expansion into nuclear and traditional power markets through the Trillium Valves acquisition. The acquired business supports more than 300 nuclear reactors worldwide, strengthening long-term service capabilities and increasing penetration across high-value industrial applications. Source: valve-world.net

February 2026 Chemical Engineering highlighted Flowserve's acquisition of Trillium Flow Technologies' Valves Division, emphasizing its installed base of over 200,000 engineered valve units serving industrial and critical infrastructure applications. The move enhances aftermarket opportunities while broadening advanced valve technology deployment across global process industries. Source: chemengonline.com

The report delivers a comprehensive assessment of the global lined valve market across manufacturing, technology, procurement, and end-use industries between 2026 and 2033. It evaluates five major product types, five core application areas, and five key end-user groups while examining adoption trends, operational performance, material innovations, and competitive positioning. Regional coverage spans North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, incorporating country-level industrial developments and deployment patterns. More than 40% of the analysis focuses on high-growth corrosion-intensive processing sectors and evolving automation practices.

The study further examines digital valve technologies, fluoropolymer lining advancements, predictive maintenance integration, and supply-chain localization strategies shaping procurement decisions. It profiles leading market participants, compares competitive strategies, and identifies emerging opportunities across specialty chemicals, pharmaceuticals, semiconductor manufacturing, industrial water treatment, and critical infrastructure. The report supports investment prioritization, capacity expansion planning, product portfolio optimization, competitive benchmarking, and long-term strategic decision-making through detailed segmentation, regional intelligence, and technology-driven market evaluation.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2025 | USD 3549 Million |

Market Revenue in 2033 | USD 4894.53 Million |

CAGR (2026 - 2033) | 4.1% |

Base Year | 2025 |

Forecast Period | 2026 - 2033 |

Historic Period | 2021 - 2025 |

Segments Covered | By Type

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | Emerson Electric Co., Flowserve Corporation, Crane Company, KSB SE & Co. KGaA, Bray International, AVK Holding A/S, SAMSON AG, Velan Inc., Richter Chemie-Technik GmbH, Asahi Yukizai Corporation, NIBCO Inc., EBRO Armaturen GmbH |

Customization & Pricing | Available on Request (10% Customization is Free) |