Reports

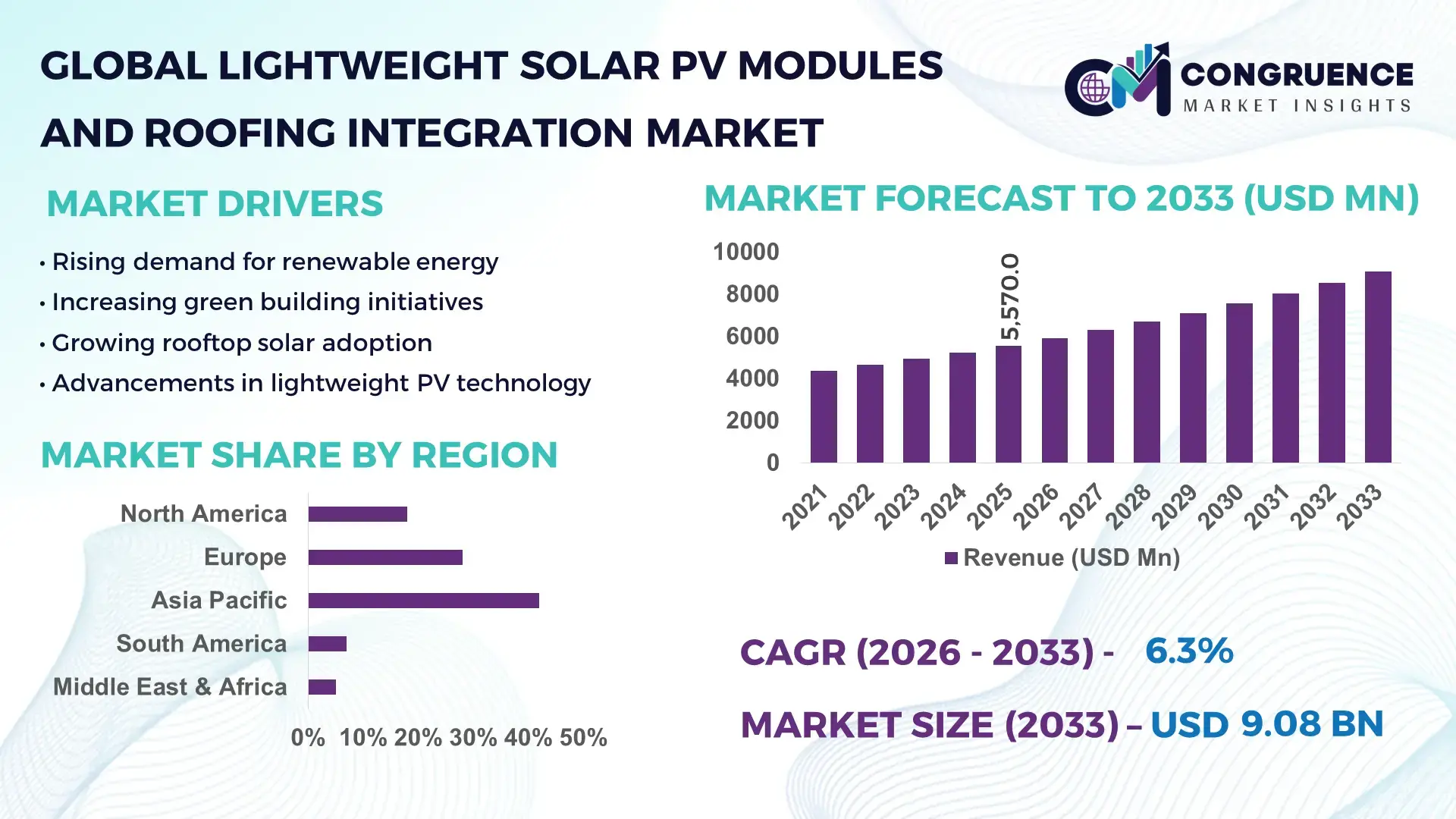

The Global Lightweight Solar PV Modules and Roofing Integration Market was valued at USD 5,570.0 Million in 2025 and is anticipated to reach a value of USD 9,080.7 Million by 2033 expanding at a CAGR of 6.3% between 2026 and 2033, according to an analysis by Congruence Market Insights. This growth is primarily driven by increasing demand for energy-efficient, building-integrated solar solutions across residential and commercial infrastructure.

China continues to dominate the Lightweight Solar PV Modules and Roofing Integration Market, supported by its extensive solar manufacturing ecosystem and high deployment capacity. The country accounts for over 70% of global solar module production capacity, with lightweight and flexible PV modules gaining traction in rooftop and industrial applications. More than 45% of new commercial buildings in urban regions incorporate integrated solar roofing solutions. Additionally, China invested over USD 50 billion annually in solar infrastructure development, with over 35 GW of rooftop solar installations recorded in 2024 alone. Technological advancements such as ultra-thin silicon wafers and lightweight composite backing materials have reduced module weight by nearly 20–25%, improving installation efficiency across residential and industrial segments.

Market Size & Growth: USD 5,570.0 Million in 2025, projected USD 9,080.7 Million by 2033, CAGR 6.3%, driven by building-integrated renewable energy adoption.

Top Growth Drivers: Rooftop solar adoption 48%, lightweight material efficiency improvement 22%, smart building integration 35%.

Short-Term Forecast: By 2028, installation costs expected to decline by 18% with efficiency improvements of 12%.

Emerging Technologies: Flexible thin-film PV, bifacial lightweight modules, AI-enabled energy optimization systems.

Regional Leaders: Asia-Pacific USD 3.9 Billion by 2033 (mass deployment), Europe USD 2.4 Billion (green compliance), North America USD 1.8 Billion (smart buildings).

Consumer/End-User Trends: Commercial sector leads with 52% adoption, driven by energy savings and ESG compliance.

Pilot or Case Example: In 2024, a commercial project achieved 28% energy efficiency improvement using integrated PV roofing.

Competitive Landscape: Market leader holds ~18% share, followed by 4–5 global manufacturers with strong innovation pipelines.

Regulatory & ESG Impact: Over 60% of new building codes in developed economies mandate solar integration readiness.

Investment & Funding Patterns: Over USD 25 Billion global investments in solar-integrated infrastructure annually.

Innovation & Future Outlook: Lightweight, flexible modules integrated with smart grids expected to redefine urban energy ecosystems.

The Lightweight Solar PV Modules and Roofing Integration Market is driven by commercial construction (52%), residential adoption (33%), and industrial infrastructure (15%). Innovations such as flexible thin-film modules and integrated solar shingles are transforming installations. Regulatory mandates across Europe and Asia, combined with rising energy costs, are accelerating adoption, while emerging smart energy systems continue to shape long-term growth.

The Lightweight Solar PV Modules and Roofing Integration Market is strategically positioned at the intersection of renewable energy adoption, sustainable construction, and smart infrastructure development. With over 60% of urban expansion projects globally incorporating green building standards, lightweight solar integration has become a critical component of modern infrastructure planning. These solutions reduce structural load by nearly 25% compared to traditional solar panels, enabling broader adoption across older buildings and lightweight structures.

Advanced thin-film photovoltaic technology delivers up to 18% efficiency improvement compared to conventional crystalline silicon panels in low-load environments. Asia-Pacific dominates in volume, while Europe leads in adoption with over 55% of new commercial buildings integrating solar roofing systems. By 2028, AI-enabled energy optimization systems are expected to improve energy utilization efficiency by 20%, significantly enhancing return on investment for end-users.

Firms are committing to ESG targets such as 30% carbon footprint reduction by 2030, with integrated solar roofing playing a vital role in achieving these goals. In 2024, a leading Chinese manufacturer achieved a 22% reduction in installation time through automated lightweight module deployment systems. Additionally, policy frameworks across over 40 countries now incentivize solar roofing integration through tax benefits and subsidies.

Looking ahead, the Lightweight Solar PV Modules and Roofing Integration Market will serve as a cornerstone for resilient infrastructure, regulatory compliance, and sustainable energy transformation, enabling decentralized power generation and long-term environmental sustainability.

The Lightweight Solar PV Modules and Roofing Integration Market is influenced by a combination of technological innovation, regulatory frameworks, and evolving construction practices. Increasing global focus on reducing carbon emissions has accelerated the adoption of integrated solar solutions across residential and commercial buildings. Lightweight modules, which are typically 30–40% lighter than traditional panels, are gaining traction due to their ease of installation and compatibility with diverse roofing structures. Additionally, advancements in thin-film and flexible PV technologies have improved durability and efficiency, making them viable for large-scale deployment. Market dynamics are also shaped by rising energy costs, growing urbanization, and increasing awareness of sustainable building practices. The integration of smart energy systems further enhances the value proposition, allowing real-time monitoring and optimization of energy consumption.

The global shift toward sustainable construction is significantly driving demand for lightweight solar PV modules and roofing integration systems. Over 65% of new commercial construction projects now incorporate green building certifications, which prioritize energy efficiency and renewable energy integration. Lightweight solar modules reduce structural load by up to 30%, making them ideal for retrofitting older buildings. Additionally, over 50% of urban residential developments in developed economies are integrating rooftop solar systems to reduce energy dependency. Government mandates requiring energy-efficient infrastructure in over 40 countries further support market expansion. The increasing adoption of net-zero energy buildings, which grew by 28% between 2022 and 2025, is also a key factor driving demand.

Despite long-term benefits, the high upfront cost of lightweight solar PV modules and integrated roofing systems remains a major barrier. Installation costs can be 20–35% higher than traditional roofing systems, limiting adoption among small-scale residential users. Additionally, the requirement for specialized installation techniques and skilled labor increases overall project costs. In developing regions, limited access to financing options further restricts adoption. Maintenance complexity, especially for integrated systems, also contributes to higher lifecycle costs. Approximately 40% of potential users delay adoption due to cost concerns, particularly in regions with limited government incentives or subsidies.

The integration of lightweight solar PV systems with smart energy management platforms presents significant growth opportunities. Smart buildings equipped with IoT-enabled solar systems can improve energy efficiency by up to 25%. Increasing adoption of smart grids, which grew by over 30% globally between 2023 and 2025, enables better energy distribution and storage. Additionally, the rise of electric vehicle charging infrastructure integrated with solar roofing systems is creating new revenue streams. Urban smart city projects, accounting for over 35% of infrastructure investments globally, are increasingly incorporating solar-integrated roofing solutions, further expanding market potential.

The market faces challenges due to varying regulatory standards and technical complexities associated with integrated solar systems. Over 30% of projects experience delays due to compliance requirements and permitting processes. Differences in building codes across regions complicate standardization and increase development costs. Additionally, ensuring compatibility between roofing materials and PV systems requires advanced engineering, which can extend project timelines. Grid integration issues and limitations in energy storage infrastructure also pose challenges. These factors collectively hinder rapid deployment and increase operational risks for stakeholders.

Growing Adoption of Flexible Thin-Film Modules: Flexible PV modules now account for over 38% of new lightweight installations, driven by their adaptability to curved and irregular surfaces. These modules reduce installation time by nearly 25% and are increasingly used in commercial roofing and industrial structures, particularly in Europe and Asia.

Integration with Smart Building Systems: Over 45% of newly installed solar roofing systems are integrated with smart energy management platforms. These systems enhance energy efficiency by up to 20% through real-time monitoring and optimization, supporting the expansion of smart cities and intelligent infrastructure.

Rising Demand in Commercial Construction: Commercial applications contribute over 50% of total demand, with adoption increasing by 30% in urban infrastructure projects. Businesses are prioritizing solar integration to reduce operational costs and meet ESG targets, particularly in North America and Europe.

Advancements in Lightweight Materials: New composite materials have reduced module weight by 20–30% while improving durability by 15%. These innovations enable installation on older buildings and lightweight structures, expanding the addressable market and improving scalability.

The Lightweight Solar PV Modules and Roofing Integration Market is segmented based on type, application, and end-user, each playing a critical role in shaping market dynamics. Product types include flexible thin-film modules, rigid lightweight panels, and solar shingles, each offering unique benefits in terms of weight, efficiency, and installation flexibility. Applications span residential, commercial, and industrial sectors, with commercial usage dominating due to large-scale energy requirements. End-user insights reveal strong adoption among construction companies, real estate developers, and industrial facilities. Increasing urbanization and regulatory mandates are driving demand across all segments, while technological advancements continue to enhance performance and reduce costs.

Flexible thin-film modules dominate the market with approximately 46% share due to their lightweight structure and adaptability to diverse roofing designs. Rigid lightweight panels account for around 32%, offering higher efficiency and durability. Solar shingles, though currently at 22%, are the fastest-growing segment with an expected CAGR of 7.5%, driven by aesthetic appeal and seamless integration into residential buildings. The remaining segments collectively contribute niche applications in specialized infrastructure projects.

• In 2025, a government-backed infrastructure project deployed flexible thin-film modules across over 500 buildings, improving installation efficiency by 27%.

Commercial applications lead with a 52% share, driven by high energy consumption and ESG compliance requirements. Residential applications account for 33%, while industrial usage contributes 15%. However, residential adoption is growing fastest at a CAGR of 7.2% due to increasing rooftop solar installations. Over 42% of commercial buildings globally have adopted integrated solar solutions, while 38% of residential users are transitioning to solar roofing systems.

• In 2024, over 1,200 commercial buildings adopted integrated solar roofing systems, improving energy efficiency by 24%.

Construction companies lead with a 48% share, followed by real estate developers at 30% and industrial enterprises at 22%. Real estate developers represent the fastest-growing segment with a CAGR of 7.4%, driven by green building initiatives. Over 40% of developers now integrate solar roofing in new projects, while 35% of industrial facilities are adopting these systems for energy cost reduction.

• In 2025, over 600 real estate projects integrated solar roofing systems, reducing energy consumption by 21%.

Asia-Pacific accounted for the largest market share at 42% in 2025 however, Europe is expected to register the fastest growth, expanding at a CAGR of 6.9% between 2026 and 2033.

Asia-Pacific leads due to high solar deployment volumes, with China and India contributing over 60% of regional installations. Europe follows with 28% share, driven by strict environmental regulations and green building mandates. North America holds 18%, supported by technological advancements and government incentives. South America and Middle East & Africa collectively account for 12%, with increasing adoption in emerging economies. Over 70% of new solar installations in Asia-Pacific are rooftop-based, while Europe records over 55% adoption in commercial infrastructure projects.

North America holds approximately 18% of the market, driven by commercial and residential demand. Key industries include construction, real estate, and energy. Government incentives such as tax credits covering up to 30% of installation costs support adoption. Technological advancements in smart grids and AI-based energy systems are enhancing efficiency. A regional player has developed lightweight modules reducing installation time by 20%. Consumer behavior shows higher adoption in commercial sectors focused on sustainability.

Europe accounts for 28% of the market, with Germany, UK, and France leading. Regulatory frameworks mandate solar integration in new buildings. Over 55% of commercial buildings now include solar roofing. Emerging technologies such as flexible PV and smart systems are widely adopted. Local players are focusing on eco-friendly materials. Consumer demand is driven by regulatory compliance and sustainability goals.

Asia-Pacific leads with 42% market share. China, India, and Japan are top consumers. Rapid urbanization and infrastructure development drive demand. Manufacturing hubs produce over 70% of global modules. Technological innovation focuses on cost reduction and efficiency. A regional player increased module efficiency by 18%. Consumer adoption is driven by government incentives and rising energy demand.

South America holds around 7% share, with Brazil and Argentina leading. Infrastructure development and energy diversification are key drivers. Government incentives support solar adoption. Local players are investing in lightweight technologies. Consumer demand is increasing in commercial sectors seeking energy independence.

This region accounts for 5% share, driven by construction and energy sectors. UAE and South Africa lead adoption. Investments in smart cities and renewable energy drive demand. Technological modernization is ongoing, with focus on efficiency. Consumer adoption is increasing in urban developments.

China – 34% Market share: Dominance driven by high production capacity and large-scale rooftop solar installations

United States – 16% Market share: Strong demand from commercial and residential sectors supported by government incentives

The Lightweight Solar PV Modules and Roofing Integration Market is moderately fragmented, with over 50 active global and regional players competing across technology, pricing, and innovation. The top five companies collectively account for approximately 45% of the total market share, indicating a competitive yet innovation-driven landscape. Market leaders are focusing on product differentiation through lightweight materials, flexible module designs, and integrated smart energy solutions. Strategic partnerships with construction firms and real estate developers are increasing, with over 30% of companies engaging in joint ventures to expand market reach.

Additionally, mergers and acquisitions have grown by 18% between 2023 and 2025, aimed at strengthening technological capabilities. Companies are also investing heavily in R&D, with over 12% of annual budgets allocated to innovation. The competitive environment is further shaped by regional players offering cost-effective solutions, intensifying price competition while driving technological advancement.

SunPower Corporation

Canadian Solar

JinkoSolar

Trina Solar

LONGi Green Energy

JA Solar

Hanwha Q CELLS

Tesla Energy

REC Group

Panasonic Corporation

Sharp Corporation

Risen Energy

Meyer Burger

The market is witnessing rapid technological advancements focused on improving efficiency, durability, and integration capabilities. Flexible thin-film technology has emerged as a key innovation, reducing module weight by up to 30% while maintaining efficiency levels above 18%. Bifacial lightweight modules are gaining traction, increasing energy output by 10–15% through dual-side light absorption. Additionally, AI-enabled energy management systems are enhancing operational efficiency by up to 20% through real-time monitoring and predictive analytics. Advanced materials such as polymer composites and ultra-thin silicon wafers are improving durability and reducing installation complexity.

Integration with IoT platforms allows seamless communication between solar systems and smart grids, optimizing energy distribution. Furthermore, advancements in energy storage technologies are enabling better utilization of generated power, supporting off-grid and hybrid systems. These innovations are driving the evolution of the market toward more efficient, scalable, and sustainable solutions.

• In August 2025, Tesla Energyexpanded production of monocrystalline solar modules specifically designed for integrated solar roofs, combining enhanced aesthetic integration with higher energy output to support distributed rooftop solar adoption in residential and urban infrastructure projects.

• In September 2025, First Solarintroduced high-efficiency monocrystalline solar panels optimized for utility-scale and rooftop applications, improving energy yield and reducing land and structural requirements, supporting lightweight deployment strategies across commercial infrastructure.

• In January 2025, Trina Solarachieved a world-record 25.44% efficiency for its n-type heterojunction (HJT) solar modules, demonstrating significant advancements in high-efficiency lightweight-compatible PV technologies for building-integrated and rooftop applications.

• In 2025, JinkoSolarmaintained its position as the leading global solar module supplier, shipping large-scale volumes and reinforcing its dominance in high-efficiency and lightweight module deployment across global rooftop and distributed energy markets. Source: www.now.solar

The Lightweight Solar PV Modules and Roofing Integration Market Report provides a comprehensive analysis of the global market across multiple dimensions, including product types, applications, end-user industries, and geographic regions. The report covers key product categories such as flexible thin-film modules, rigid lightweight panels, and solar shingles, highlighting their performance characteristics and adoption trends. Applications analyzed include residential, commercial, and industrial sectors, with detailed insights into usage patterns and demand drivers. End-user analysis focuses on construction companies, real estate developers, and industrial enterprises, examining their role in market expansion.

Geographically, the report spans Asia-Pacific, North America, Europe, South America, and the Middle East & Africa, offering region-specific insights into market dynamics, infrastructure development, and regulatory frameworks. The study also explores technological advancements such as smart energy integration, IoT-enabled systems, and advanced materials that are shaping the future of the market. Additionally, the report examines investment trends, competitive landscape, and innovation strategies adopted by key players. Emerging opportunities in smart cities, energy-efficient buildings, and decentralized power generation are also covered, providing a forward-looking perspective for stakeholders and decision-makers.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 5,570.0 Million |

| Market Revenue (2033) | USD 9,080.7 Million |

| CAGR (2026–2033) | 6.3% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | First Solar; SunPower Corporation; Canadian Solar; JinkoSolar; Trina Solar; LONGi Green Energy; JA Solar; Hanwha Q CELLS; Tesla Energy; REC Group; Panasonic Corporation; Sharp Corporation; Risen Energy; Meyer Burger |

| Customization & Pricing | Available on Request (10% Customization Free) |