Reports

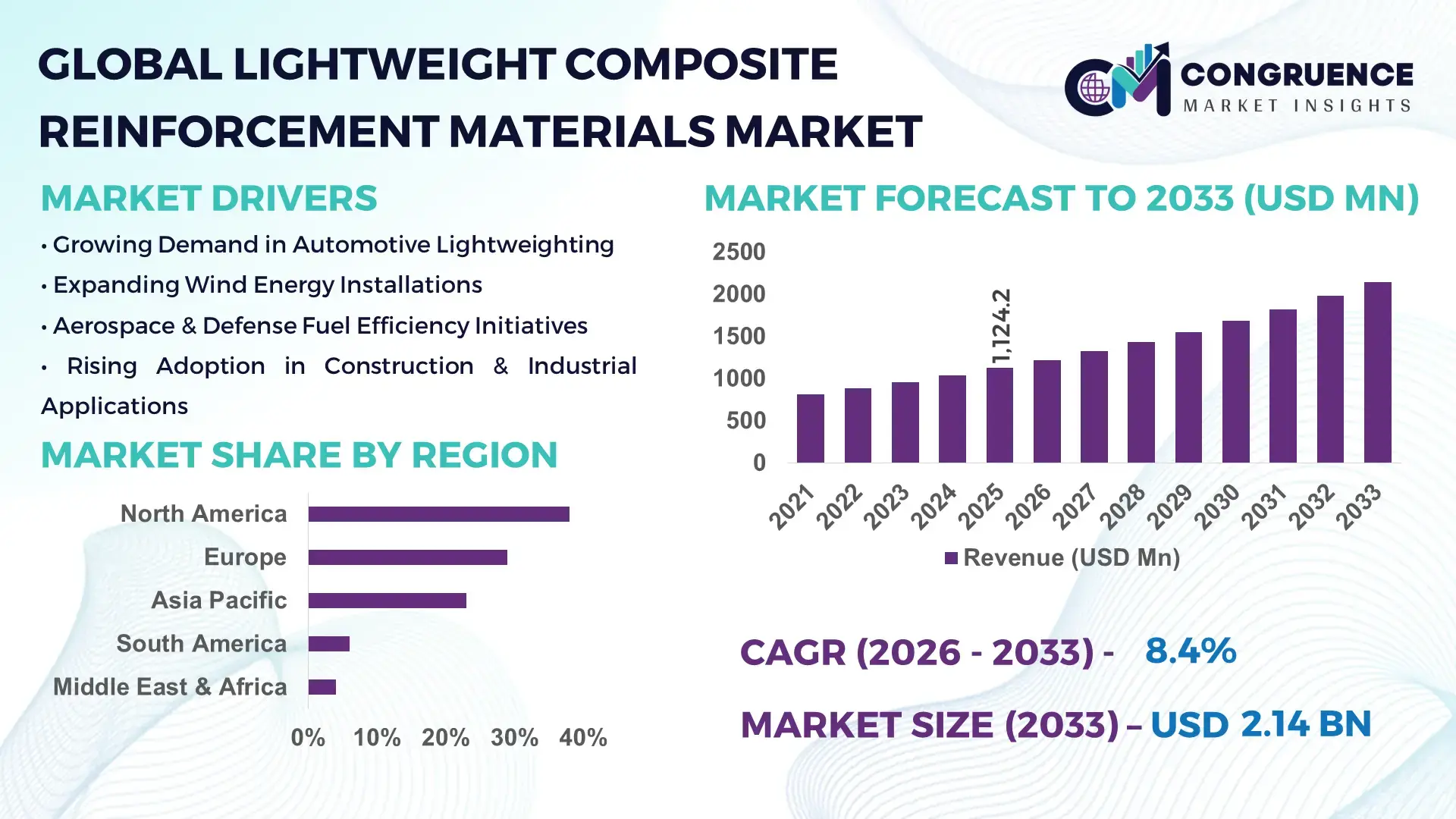

The Global Lightweight Composite Reinforcement Materials Market was valued at USD 1,124.2 Million in 2025 and is anticipated to reach a value of USD 2,143.3 Million by 2033 expanding at a CAGR of 8.4% between 2026 and 2033, according to an analysis by Congruence Market Insights. Growth is primarily driven by rising demand for weight reduction, durability enhancement, and lifecycle efficiency across transportation, construction, and energy-intensive industrial applications.

The United States represents the most influential country within the Lightweight Composite Reinforcement Materials Market, supported by advanced production infrastructure and sustained capital investments. The U.S. hosts more than 35 large-scale composite material manufacturing facilities, with annual reinforcement fiber output exceeding 180 kilotons. Composite reinforcements are widely used in aerospace (over 42% of domestic structural composites consumption), followed by automotive lightweighting programs and wind energy blades. Federal and private investments surpassed USD 2.6 billion between 2021 and 2024 for advanced composites R&D, while automation-enabled layup and resin infusion technologies improved production throughput by 28%. Adoption of thermoplastic composite reinforcements increased by 31% across U.S. industrial users, reflecting strong technology-driven utilization.

Market Size & Growth: Valued at USD 1,124.2 Million in 2025, projected to reach USD 2,143.3 Million by 2033, growing at 8.4% CAGR due to aggressive lightweighting mandates.

Top Growth Drivers: Automotive lightweight adoption 46%, fuel-efficiency improvement 18%, durability enhancement 22%.

Short-Term Forecast: By 2028, composite-enabled structural efficiency is expected to improve by 24%.

Emerging Technologies: Thermoplastic carbon fiber, nano-reinforced glass fibers, automated fiber placement.

Regional Leaders: North America USD 742 Million (2033, aerospace-driven); Europe USD 618 Million (EV adoption); Asia Pacific USD 561 Million (infrastructure scale-up).

Consumer/End-User Trends: OEMs account for 63% of demand, with rising Tier-1 integration.

Pilot or Case Example: In 2024, a German automotive pilot reduced component weight by 32%.

Competitive Landscape: Owens Corning (~18%), followed by Toray, Hexcel, Teijin, and SGL Carbon.

Regulatory & ESG Impact: Composite recycling mandates driving 27% material redesign.

Investment & Funding Patterns: Over USD 4.1 billion invested globally since 2022.

Innovation & Future Outlook: Hybrid fiber systems accelerating multi-sector deployment.

The Lightweight Composite Reinforcement Materials Market serves automotive (38%), aerospace (27%), wind energy (18%), and construction (12%), supported by advancements in hybrid fiber architectures and resin compatibility. Regulatory pressure for emission reduction, regional infrastructure expansion in Asia Pacific, and increased recyclability standards in Europe are shaping demand, while automated manufacturing and bio-based reinforcements define future growth pathways.

The Lightweight Composite Reinforcement Materials Market is strategically positioned as a core enabler of industrial efficiency, decarbonization, and structural optimization. Manufacturers increasingly rely on reinforcement materials to meet stringent performance and sustainability benchmarks across mobility, energy, and infrastructure sectors. Thermoplastic carbon fiber reinforcements deliver 35% faster processing efficiency compared to traditional thermoset-based standards, enabling high-volume manufacturing without compromising mechanical strength.

From a regional standpoint, Asia Pacific dominates in production volume, while Europe leads in adoption with nearly 48% of automotive OEMs integrating lightweight composite reinforcements into new vehicle platforms. In the near term, automation-driven fiber placement and AI-assisted material optimization are reshaping cost structures. By 2028, automated composite layup systems are expected to reduce production waste by 22%, improving margin stability.

ESG compliance is becoming inseparable from strategic planning. Firms are committing to 30–40% recyclable composite content by 2030, aligning reinforcement material innovation with circular economy mandates. A micro-scenario illustrates this shift: In 2024, a Japanese wind turbine manufacturer achieved a 26% blade weight reduction through advanced glass–carbon hybrid reinforcements, improving energy yield per turbine. Looking forward, the Lightweight Composite Reinforcement Materials Market will act as a pillar of resilience, regulatory compliance, and sustainable industrial growth, supporting long-term competitiveness across high-performance sectors.

The Lightweight Composite Reinforcement Materials Market is shaped by evolving industrial performance requirements, material science advancements, and sustainability-driven design changes. Demand continues to rise as industries prioritize strength-to-weight optimization, corrosion resistance, and lifecycle cost reduction. Automotive electrification, renewable energy infrastructure, and aerospace modernization programs are increasing reinforcement material intensity per unit produced. Simultaneously, manufacturers are investing in automated processing, hybrid fiber systems, and improved resin compatibility to enhance scalability. Regional policy frameworks encouraging lightweight structures and energy efficiency further influence procurement strategies, while supply chain localization and recycling initiatives are redefining material selection criteria across end-use industries.

The push for lightweight yet high-strength structures is a major driver of the Lightweight Composite Reinforcement Materials Market. In automotive manufacturing, reducing vehicle weight by 10% improves energy efficiency by approximately 6–8%, accelerating adoption of reinforced composites in body panels, chassis components, and battery enclosures. Aerospace applications increasingly replace metal reinforcements with carbon and glass fiber systems, extending component lifespans by over 20%. Wind energy blades now exceed 80 meters in length, requiring advanced reinforcement materials to maintain structural integrity under cyclic loads. These performance-driven requirements directly expand reinforcement material utilization across industries.

Despite performance advantages, high processing complexity restrains market expansion. Advanced reinforcement materials require controlled environments, skilled labor, and precise curing processes, increasing operational burden. Manufacturing scrap rates can exceed 12% in manual layup operations, raising cost sensitivity among mid-scale manufacturers. Additionally, volatility in precursor materials such as PAN-based carbon fiber impacts procurement planning. Limited recycling infrastructure for reinforced composites further constrains adoption in cost-sensitive construction and consumer goods applications, slowing penetration beyond high-value industrial sectors.

Renewable energy expansion presents strong opportunities for the Lightweight Composite Reinforcement Materials Market. Wind energy installations increasingly depend on reinforced composite blades to achieve higher capacity factors and longer service intervals. Offshore wind projects now account for over 35% of new blade demand, favoring corrosion-resistant reinforcement materials. Similarly, hydrogen storage tanks and solar mounting structures are adopting lightweight reinforcements to improve transport efficiency and structural reliability. These applications open long-term demand channels, particularly in Asia Pacific and Europe.

Recycling limitations pose a significant challenge for the Lightweight Composite Reinforcement Materials Market. Less than 20% of composite reinforcement waste is currently recycled at scale, creating regulatory pressure in regions with strict waste directives. Compliance uncertainty increases redesign costs for manufacturers, particularly in Europe. Additionally, inconsistent standards for recycled fiber quality limit reuse in high-load applications. Addressing these challenges requires coordinated investment in recycling technologies, standardization frameworks, and cross-industry collaboration, which remains uneven across regions.

Accelerated Adoption of Thermoplastic Reinforcements: Thermoplastic-based reinforcement materials are gaining traction due to faster cycle times and recyclability. Adoption increased by 34% between 2022 and 2025, while processing time fell by 40% compared to thermoset systems. Automotive OEMs now integrate thermoplastic reinforcements in over 29% of structural components, improving end-of-life material recovery.

Integration of Automated Fiber Placement Technologies: Automated fiber placement usage rose by 31%, enabling precision reinforcement with material waste reduced by 18%. Aerospace and wind energy sectors report productivity gains of 25%, supporting large-scale component manufacturing with consistent quality outcomes.

Expansion of Hybrid Fiber Architectures: Hybrid reinforcement systems combining carbon and glass fibers now represent 22% of new product designs. These systems achieve 15–20% cost optimization while maintaining high tensile performance, particularly in infrastructure and energy applications.

Rise in Modular and Prefabricated Construction: The adoption of modular construction is reshaping demand dynamics in the Lightweight Composite Reinforcement Materials Market. Research suggests that 55% of new projects reported cost benefits using modular and prefabricated practices. Pre-bent and cut elements are fabricated off-site using automated machines, reducing labor needs by 30% and accelerating project timelines by 25%, particularly across Europe and North America.

The Lightweight Composite Reinforcement Materials Market is segmented primarily by type, application, and end-user, reflecting diverse performance requirements across industries. By type, demand is shaped by tensile strength, thermal stability, cost, and recyclability, leading to differentiated adoption between carbon, glass, aramid, basalt, and natural fibers. Application segmentation centers on structural performance, fatigue resistance, and corrosion tolerance, with transportation, aerospace, wind energy, construction, and marine representing core use cases. End-user insights reveal a clear split between high-precision sectors (aerospace and defense) and high-volume industries (automotive and infrastructure). Material selection increasingly balances performance with sustainability, recyclability, and manufacturability, while regional manufacturing capabilities and regulatory frameworks influence procurement strategies. Automation in composite processing and hybrid reinforcement architectures are also reshaping how segments evolve across value chains.

Carbon fiber reinforcements lead the market, accounting for approximately 46% share, driven by superior strength-to-weight ratio, fatigue resistance, and thermal stability required in aerospace, wind blades, and high-performance automotive components. Their growing integration into battery enclosures and hydrogen tanks further reinforces leadership. Fastest-growing type: Thermoplastic carbon fiber is expanding at roughly 11–12% CAGR, fueled by shorter molding cycles, improved recyclability, and rising use in electric vehicle (EV) structures and mass-produced automotive parts. Glass fiber remains a high-volume alternative, holding about 28% share, favored for cost-effective structural applications in construction, marine, and consumer composites. Aramid fibers serve niche but critical uses in impact-resistant components and protective structures, while basalt fibers are gaining traction in infrastructure and fire-resistant applications. Natural fibers (flax, hemp, jute) collectively contribute around 8–10% share, mainly in sustainable packaging, interior panels, and low-load automotive parts. Hybrid fiber systems—combining carbon and glass—are increasingly adopted to balance cost and performance, particularly in wind energy and heavy transportation.

• In 2025, a large aircraft manufacturer introduced thermoplastic carbon wing ribs using automated tape placement, cutting scrap rates by 22% and reducing assembly time by nearly one-third.

Transportation is the leading application segment with roughly 38% share, as automakers replace steel and aluminum with reinforced composites to meet fuel-efficiency and EV range targets. Structural panels, battery housings, and lightweight chassis components dominate demand. Fastest-growing application: Wind energy components are rising at about 10–11% CAGR, supported by longer turbine blades (80–110 meters) that require high-strength composite reinforcements to withstand cyclic fatigue and offshore corrosion. Aerospace & defense account for around 22% share, prioritizing ultra-lightweight, high-durability materials for fuselage, wings, and interior structures. Construction and infrastructure represent approximately 15% share, driven by corrosion-resistant rebar, bridge panels, and modular elements. Marine, sports equipment, and industrial tooling together contribute the remaining 25%. Consumer adoption trends are visible: in 2025, over 41% of global automotive OEMs reported piloting composite-intensive body structures for next-generation EV platforms. Additionally, more than 35% of wind project developers indicated a shift toward hybrid fiber blades for cost optimization.

• In 2025, a European offshore wind project deployed next-generation hybrid composite blades that improved energy capture efficiency by 6% while reducing blade weight by 18%.

Automotive & transportation is the leading end-user segment with about 36% share, driven by aggressive lightweighting mandates, EV battery protection needs, and structural crash performance requirements. Tier-1 suppliers are increasingly vertically integrating composite reinforcement capabilities. Fastest-growing end-user: Renewable energy (especially wind) is expanding at roughly 10–11% CAGR, propelled by offshore installations, larger turbine designs, and demand for corrosion-resistant materials. Aerospace & defense holds roughly 24% share, supported by long-term aircraft programs and defense modernization initiatives. Construction & infrastructure accounts for about 18%, with growing use of composite rebar, bridge decks, and prefabricated modules. Marine, industrial equipment, and consumer goods together represent the remaining 22%. Industry adoption patterns show that in 2025, around 44% of large industrial manufacturers were testing hybrid composite reinforcements for lighter machinery and corrosion resistance. In addition, nearly 58% of infrastructure developers in Europe prioritized recyclable composite materials in new projects.

• In 2025, a national highway authority in Asia deployed basalt-fiber-reinforced composite bridge panels across 120 kilometers of roadway, reducing maintenance costs by 27% and extending expected service life by over a decade.

North America accounted for the largest market share at 38% in 2025; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 9.1% between 2026 and 2033.

The Lightweight Composite Reinforcement Materials Market shows strong regional variation driven by industrial maturity, infrastructure investment, and sectoral demand. North America leads due to aerospace, defense, and EV manufacturing, with more than 120 active composite manufacturing hubs and high adoption of automation. Europe follows with 29% share in 2025, supported by stringent sustainability regulations, recycling mandates, and green mobility programs across Germany, France, and the UK. Asia-Pacific holds approximately 23% share, but records the highest incremental demand owing to rapid industrialization, wind energy expansion, and large-scale automotive production in China, Japan, and India. South America contributes around 6%, driven by renewable energy and infrastructure modernization, while the Middle East & Africa holds about 4%, supported by oil & gas composites, construction mega-projects, and localized manufacturing initiatives.

North America represents roughly 38% of global consumption of Lightweight Composite Reinforcement Materials, making it the most structurally advanced regional market. Aerospace and defense account for nearly 42% of regional demand, followed by automotive at 31%, wind energy at 17%, and industrial applications at 10%. Strong government backing—such as tax incentives for EV manufacturing, wind projects, and domestic supply chain localization—has accelerated adoption of advanced composites. The U.S. Department of Energy’s materials innovation programs have promoted lightweighting in battery enclosures and hydrogen storage tanks, while aerospace modernization initiatives continue to expand composite usage per aircraft. Digital manufacturing tools, including AI-driven fiber placement and automated layup robotics, have improved production efficiency by over 25% across major facilities. Local players such as Owens Corning are expanding glass fiber capacity while integrating recycled content into reinforcement products. Enterprise users in North America show higher adoption in aerospace, automotive, and industrial sectors, with increasing emphasis on predictive maintenance and digital quality monitoring in composite manufacturing.

Europe accounts for approximately 29% of the global Lightweight Composite Reinforcement Materials Market, with Germany, France, and the UK leading consumption. Automotive and renewable energy together contribute nearly 55% of regional demand, while aerospace and construction represent around 30%. The European Union’s circular economy directives and Extended Producer Responsibility (EPR) regulations are forcing manufacturers to redesign composite materials for recyclability and reuse. Programs such as Fit for 55 and Green Deal funding have accelerated investment in lightweight EV structures and offshore wind blades. Germany has emerged as a hub for thermoplastic composites, while France focuses on aerospace-grade reinforcements and the UK prioritizes wind energy materials. Leading European firms like Hexcel are investing heavily in recyclable carbon fiber technologies and bio-based resin compatibility. European enterprises exhibit strong regulatory-driven behavior, prioritizing explainable, traceable, and certified composite materials to meet compliance and ESG reporting requirements.

Asia-Pacific is the fastest-expanding region and the second-largest in volume usage of Lightweight Composite Reinforcement Materials. China dominates consumption with extensive automotive, wind energy, and infrastructure programs, followed by Japan and India. The region hosts more than 180 composite processing plants, with China alone accounting for nearly 40% of global wind blade production. Rapid urbanization, high-speed rail expansion, and EV manufacturing have driven massive demand for reinforced composites in structural applications. Japan leads in high-precision aerospace composites, while India is rapidly scaling infrastructure-grade basalt and glass fiber usage in bridges and highways. Technology hubs in Shenzhen, Nagoya, and Bengaluru are advancing automated fiber placement, smart composites, and digital material inspection. Local firms such as Toray and Mitsubishi Chemical are expanding carbon fiber capacity and investing in recycling technologies. Regional consumer behavior shows demand growth linked to e-commerce logistics, modular construction, and mobile technology infrastructure.

South America represents roughly 6% of the global market, with Brazil and Argentina as key contributors. Wind and hydropower projects drive nearly 45% of regional demand, followed by construction at 30% and transportation at 15%. Brazil has accelerated wind farm installations along its coastline, increasing consumption of reinforced composite blades and structural components. Argentina’s infrastructure modernization programs have expanded use of composite rebar in bridges and corrosion-resistant materials in coastal projects. Governments are introducing incentives for green construction and renewable energy manufacturing, improving investment confidence. Trade policies favoring domestic composite production have encouraged local material processing and downstream fabrication. Companies such as WEG and local blade manufacturers are strengthening supply chains for glass and hybrid fiber reinforcements. Consumer demand in the region is closely tied to media, language localization, and digital connectivity infrastructure, influencing composite use in telecom towers and data centers.

The Middle East & Africa region holds about 4% of the global market, with demand concentrated in oil & gas, construction, and renewable energy. The UAE and Saudi Arabia lead adoption through mega-infrastructure projects, smart cities, and desalination plants requiring corrosion-resistant composites. South Africa is a growing hub for wind and solar materials, particularly for reinforced mounting structures and turbine components. Regional modernization trends include automated composite fabrication, digital inspection, and high-temperature-resistant reinforcements for industrial pipelines. Governments are promoting local manufacturing through free trade zones, technology parks, and foreign investment incentives. Strategic partnerships between regional players and global composite firms are strengthening supply chains. Companies in the UAE are expanding composite use in aerospace interiors and marine vessels. Consumer behavior reflects rising preference for durable, low-maintenance materials in construction and industrial applications.

United States – 32% Market Share: High aerospace production capacity and strong EV lightweighting demand drive leadership in the Lightweight Composite Reinforcement Materials Market.

China – 26% Market Share: Massive wind energy expansion and large-scale automotive manufacturing fuel dominance in the Lightweight Composite Reinforcement Materials Market.

The competitive environment in the Lightweight Composite Reinforcement Materials Market is moderately consolidated with a diverse mix of large multinational corporations, mid‑sized regional players, and specialized innovators competing across product portfolios and applications. There are 25+ active competitors globally focusing on advanced reinforcement solutions such as carbon fiber, glass fiber, aramid fiber, hybrid systems, and thermoplastic composite reinforcements. Market positioning reflects strong leadership by legacy materials companies integrated into aerospace, automotive, and energy value chains, with several firms pursuing strategic initiatives like new product introductions, capacity expansions, partnerships, and acquisitions to strengthen their market foothold. The combined share of the top 5 companies in related composite reinforcement segments is estimated at around 55–60%, indicating that while top players hold significant influence, there remains substantial room for regional and niche competitors.

Strategic initiatives shaping competition include product launches of next‑generation reinforcement fabrics and tapes tailored for high‑performance applications, expansion of manufacturing footprints in North America and Asia‑Pacific, and cross‑industry collaborations targeting wind energy, EV manufacturing, and infrastructure composites. Innovation trends influencing the competitive landscape include the integration of digital manufacturing technologies (such as automated fiber placement and AI‑powered quality inspection), development of recyclable and bio‑based reinforcement materials, and advanced thermoplastic composite systems that support faster cycle times and improved end‑of‑life sustainability. Competition is also affected by vertical integration strategies aimed at securing precursor supplies (e.g., PAN for carbon fibers) and enhancing cost competitiveness. Overall, the market sees differentiated competition across geographies and end uses, with leaders leveraging scale, technological R&D, and strategic partnerships to maintain competitive advantage.

Solvay

Teijin Limited

DuPont

Mitsubishi Chemical Corporation

Owens Corning

BASF SE

Jushi Group

Hughes Brothers, Inc.

Pultrall Inc.

Dextra Group

GFRP Systems

Engineered Composites Ltd.

Technological innovation is a major driver in the Lightweight Composite Reinforcement Materials Market, as advanced materials and manufacturing technologies increasingly determine performance, cost, and applicability across end uses. Current technologies center on continuous fiber architectures, high‑strength carbon and glass fiber reinforcements, and automated manufacturing systems such as automated fiber placement (AFP) and automated tape laying (ATL), which improve repeatability, reduce waste, and compress production cycles. Reinforcement materials are also benefiting from thermoplastic composite technologies, enabling faster processing, improved recyclability, and design flexibility compared to traditional thermoset systems. Digital transformation trends include the integration of AI‑assisted process control, in‑line quality inspection, and predictive maintenance systems, which collectively enhance manufacturing throughput and product reliability.

Another significant technology trend is hybrid composite systems that combine carbon, glass, and aramid fibers to balance cost, strength, and toughness, particularly in automotive, wind energy, and industrial sectors. These hybrid reinforcements allow designers to tailor stiffness and impact resistance profiles while optimizing material cost. Furthermore, nanotechnology enhancements, such as graphene or nano‑clay additives, are being embedded within matrix materials to elevate mechanical properties, thermal stability, and fatigue resistance of composite reinforcements. Sustainability‑focused innovation is driving adoption of bio‑based and recyclable reinforcement solutions, aligning material performance with environmental and circular economy goals.

Process automation continues to evolve, with robotic composite layup, machine vision for defect detection, and digital twins for factory simulation becoming increasingly mainstream in high‑volume production settings. Such technologies reduce labor dependency, enhance precision, and support quicker adoption of lightweight reinforcements in demanding applications like aerospace primary structures and EV chassis components. With emphasis on digitalization, recyclability, and multi‑material integration, technology development in composite reinforcements is advancing toward delivering stronger, lighter, and more sustainable solutions.

• In February 2026, Toray Composite Materials America, Inc. achieved NCAMP qualification for its next‑generation 3960 prepreg system, enabling aerospace and defense manufacturers to streamline material selection and certification with FAA‑recognized design allowable data now available in the NCAMP database. This system features TORAYCA™ T1100 intermediate modulus fiber optimized for high‑performance structural applications. Source: www.prnewswire.com

• In December 2025, Toray Advanced Composites completed NCAMP qualification for its Cetex® high‑performance thermoplastic composite materials, enhancing certification readiness and broadening thermoplastic reinforced composite solutions for aerospace, automotive, and industrial applications. Source: www.toraytac.com

• In February 2025, Owens Corning agreed to sell its glass reinforcements business to Praana Group in a strategic transaction valued at approximately USD 755 million, reshaping its composites segment focus and creating a new standalone advanced glass fiber reinforcement business serving wind energy, infrastructure, and transportation markets. Source: www.owenscorning.com

• In June 2025, Composite Recycling and Owens Corning’s glass reinforcements division announced a strategic collaboration to scale glass fiber circularity, aiming to integrate reclaimed glass fibers into production lines, reduce landfill waste, and advance industrial-scale recycling of composite materials for automotive, marine, and construction segments. Source: www.chemanalyst.com

The scope of the Lightweight Composite Reinforcement Materials Market Report encompasses a comprehensive examination of market segmentation by product types, applications, end‑users, and geographic regions to provide decision‑makers with actionable insights into strategic opportunities and competitive positioning. Product types include carbon fiber reinforcements, glass fiber reinforcements, aramid fibers, hybrid systems, thermoplastic composites, and natural fiber‑based reinforcement solutions, each evaluated for performance attributes, application fit, and technological readiness. The report also explores application domains such as aerospace, automotive, wind energy, construction, industrial equipment, and marine sectors, detailing how reinforcement requirements vary with structural demands, environmental exposure, and cost constraints.

Geographic coverage spans North America, Europe, Asia‑Pacific, South America, and Middle East & Africa, with region‑specific volume and adoption patterns, regulatory influences, and infrastructure development trends. End‑user analysis dissects adoption drivers across OEMs, Tier‑1 manufacturers, and large infrastructure developers, highlighting differentiated demand for lightweight, high‑strength materials. Technology focus areas include advanced manufacturing processes such as automated fiber placement, digital quality assurance systems, and innovation in recyclable and bio‑based reinforcement materials, reflecting the evolving intersection of performance and sustainability. Competitive landscape insights feature major global players, strategic initiatives (product launches, partnerships, acquisitions), and innovation trends shaping market dynamics. Additionally, niche segments such as tailored composites for defense, modular construction reinforcement, and high‑temperature industrial applications are addressed to capture emerging opportunities and industry evolution.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 1,124.2 Million |

| Market Revenue (2033) | USD 2,143.3 Million |

| CAGR (2026–2033) | 8.4% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Regulatory & ESG Overview, Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Toray Industries, Inc.; Hexcel Corporation; SGL Carbon SE; Solvay; Teijin Limited; DuPont; Mitsubishi Chemical Corporation; Owens Corning; BASF SE; Jushi Group; Hughes Brothers, Inc.; Pultrall Inc.; Dextra Group; GFRP Systems; Engineered Composites Ltd. |

| Customization & Pricing | Available on Request (10% Customization Free) |