Reports

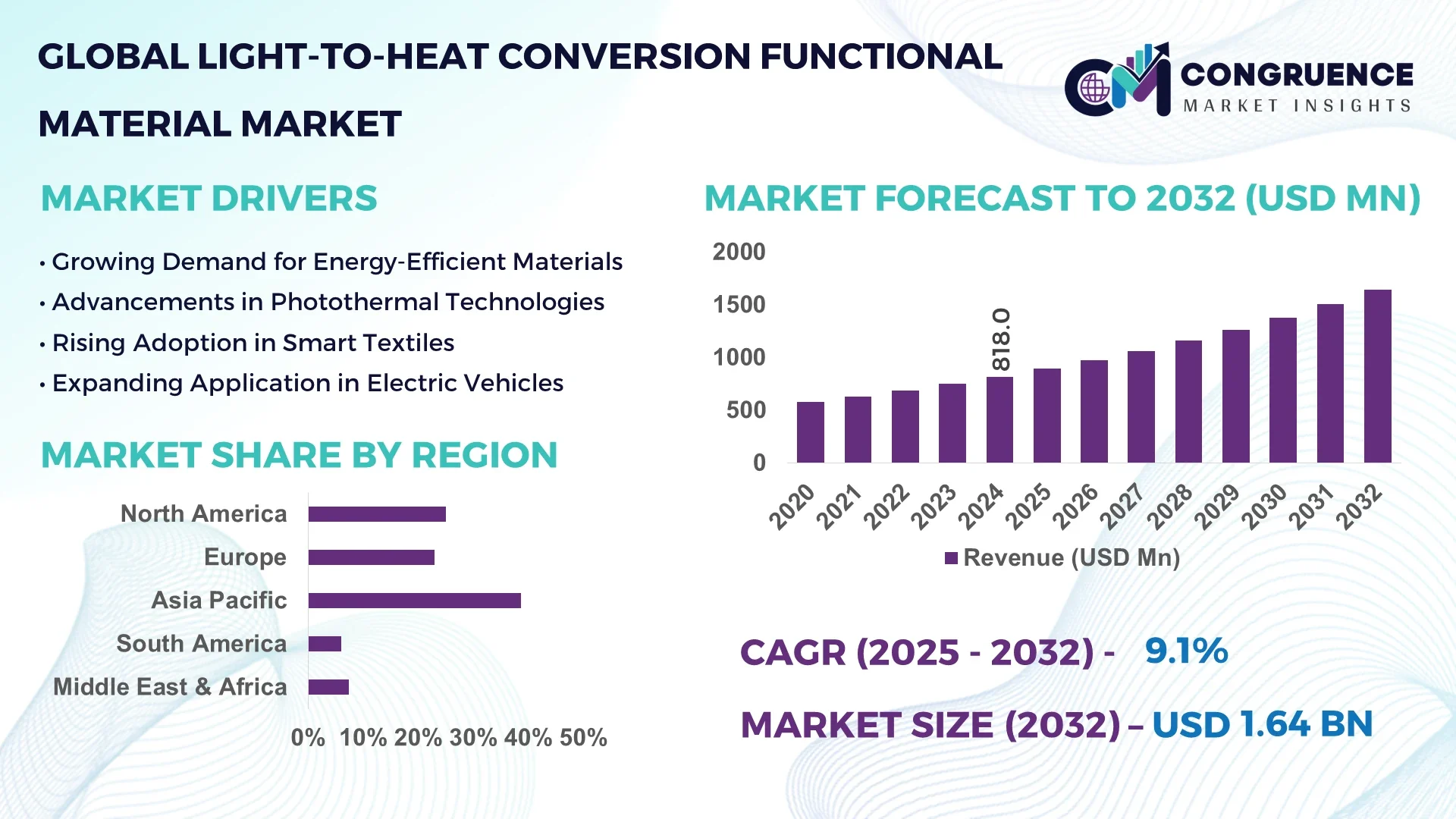

The Global Light-to-heat Conversion Functional Material Market was valued at USD 818.0 Million in 2024 and is anticipated to reach a value of USD 1,641.9 Million by 2032 expanding at a CAGR of 9.1% between 2025 and 2032.

To Learn More About This Report, Request A Free Sample Copy

China dominates the Light-to-heat Conversion Functional Material Market, driven by its vast manufacturing base and significant investments in energy-efficient materials. The country’s government initiatives to promote sustainable construction and automotive industries have accelerated the adoption of light-to-heat conversion materials across various sectors, particularly in urban development and green building projects.

The Light-to-heat Conversion Functional Material Market is characterized by rapid innovation in materials science, enabling enhanced thermal management solutions across multiple industries. These materials are increasingly integrated into smart textiles, automotive components, and energy-saving building elements, improving efficiency and reducing energy consumption. The growing emphasis on environmental regulations and the need for sustainable product alternatives continue to fuel market expansion worldwide, making these materials crucial for future industrial applications.

Artificial intelligence (AI) is revolutionizing the Light-to-heat Conversion Functional Material Market by optimizing material design, accelerating research, and enhancing manufacturing precision. AI-driven simulations allow researchers to predict thermal behaviors and light absorption properties more accurately, reducing the need for extensive physical prototyping. Machine learning algorithms analyze large datasets from material experiments, identifying patterns that guide the development of more efficient light-to-heat conversion materials with tailored performance characteristics.

In manufacturing, AI-powered automation enhances quality control by detecting defects and inconsistencies in real-time, ensuring higher product reliability. Predictive maintenance models powered by AI reduce downtime in production facilities, improving operational efficiency. Furthermore, AI aids in supply chain optimization by forecasting demand fluctuations and managing inventory for these niche materials, minimizing waste and cost.

The integration of AI in product development cycles also accelerates the customization of light-to-heat materials for specific applications, such as adaptive building facades or automotive heating systems. By utilizing AI insights, companies can rapidly iterate designs that maximize energy efficiency and user comfort. Overall, AI’s role spans the entire value chain, enabling smarter innovation, cost reductions, and faster market introduction of advanced functional materials.

“In 2024, a breakthrough was reported where AI algorithms successfully predicted the thermal conversion efficiency of novel phase change materials, reducing experimental time by 40%. This development enabled manufacturers to fast-track the commercialization of next-generation light-to-heat materials tailored for building insulation applications.”

The growing focus on reducing energy consumption in residential and commercial buildings is a primary driver of the Light-to-heat Conversion Functional Material Market. These materials improve thermal insulation and enable passive heating solutions, reducing reliance on conventional heating systems. Adoption of green building standards and energy codes across multiple countries has led to increased demand for such functional materials. In particular, their use in window coatings and façade elements enhances energy conservation, contributing to lower operational costs and carbon emissions.

The adoption of light-to-heat conversion materials is sometimes restrained by their higher upfront costs compared to traditional alternatives. Manufacturers and end-users may hesitate due to budget constraints, especially in developing markets. Additionally, the cost of integrating these materials into existing products or construction projects can be substantial. This financial barrier slows widespread adoption, particularly among small and medium enterprises that prioritize short-term expenditure over long-term energy savings.

The increasing use of light-to-heat conversion functional materials in automotive interiors and wearable technologies presents significant growth opportunities. These materials provide innovative solutions for thermal comfort and energy efficiency in vehicles, reducing the load on HVAC systems. Similarly, in wearables, they enhance temperature regulation, improving user comfort and functionality. As automotive manufacturers and wearable tech developers seek sustainable and efficient materials, this expanding application segment is expected to drive market growth.

One of the major challenges facing the Light-to-heat Conversion Functional Material Market is the complexity involved in integrating these materials into diverse product platforms. Compatibility with existing manufacturing processes and ensuring consistent performance across applications require significant technical expertise. Moreover, lack of standardized testing methods and certifications creates uncertainty among buyers regarding material reliability and effectiveness, hindering faster adoption. Overcoming these challenges demands collaborative efforts among researchers, manufacturers, and regulatory bodies.

Rise of Smart Coatings with Dynamic Thermal Properties: The market is witnessing increased adoption of smart coatings that can adjust their thermal properties based on environmental stimuli. These coatings help buildings and vehicles better manage heat gain and loss, leading to improved energy efficiency without sacrificing comfort. Their ability to respond dynamically to changing light or temperature conditions makes them highly valuable in energy-conscious applications.

Advances in Nanotechnology for Enhanced Light Absorption: Incorporating nanotechnology into material formulations has enabled significant improvements in light absorption and heat conversion rates. This technology allows the creation of thinner, lighter materials that maintain or even boost performance. Such advancements make it easier to integrate light-to-heat functional materials into a wider range of products, including flexible and wearable items.

Growth in Wearable Technology Integration: Consumer demand for enhanced thermal comfort in wearable products is driving market growth in this segment. Light-to-heat conversion materials are being increasingly incorporated into clothing and accessories, offering active temperature regulation. The trend toward multifunctional textiles—combining heating capabilities with moisture management and UV protection—is becoming a key differentiator for manufacturers.

Regional Leadership and Focus on Sustainability: The Asia-Pacific region continues to dominate market adoption due to rapid urbanization and supportive government policies promoting sustainable materials in construction and transportation. Meanwhile, North America and Europe emphasize innovation through research collaborations and pilot projects showcasing the real-world benefits of light-to-heat conversion materials. Additionally, a global shift toward eco-friendly and recyclable components is shaping product development to align with environmental regulations and consumer preferences.

The Light-to-heat Conversion Functional Material Market is segmented based on type, application, and end-user industries, providing a comprehensive view of market dynamics. Different types of materials cater to varied requirements in thermal management, influencing their adoption across sectors. Applications range from construction and automotive to consumer electronics and wearables, each driven by unique performance demands. End-user insights reveal the sectors investing heavily in these materials to enhance energy efficiency, comfort, and sustainability. This segmentation enables stakeholders to understand market trends, identify growth opportunities, and tailor strategies accordingly, ensuring alignment with evolving customer needs and technological advancements.

The market includes types such as phase change materials (PCMs), photothermal materials, and carbon-based materials. Phase change materials hold the leading market position due to their superior ability to store and release thermal energy efficiently, making them highly suitable for building insulation and energy-saving applications. Photothermal materials are the fastest-growing segment, benefiting from advances in nanotechnology that enhance their light-to-heat conversion efficiency, which is particularly valuable in solar energy harvesting and automotive defrosting systems. Carbon-based materials, known for their lightweight and excellent thermal conductivity, are gaining traction in wearable and electronics sectors. Their versatility and performance improvements continue to drive demand across industries, positioning them as an essential part of the material portfolio in this market.

Applications of light-to-heat conversion functional materials include building & construction, automotive, consumer electronics, and textiles & wearables. Building and construction dominate the market, accounting for the largest share due to increasing energy-efficiency regulations and the rising adoption of sustainable building materials. These materials are extensively used in insulation panels, window coatings, and roofing solutions. The fastest-growing application is automotive, where manufacturers leverage these materials for improved thermal comfort and energy savings in vehicle interiors, especially in electric vehicles where thermal management is critical. Consumer electronics also present significant growth potential as devices require efficient heat dissipation to maintain performance and longevity. The textiles and wearables segment is emerging rapidly, driven by consumer demand for comfort and smart functionalities.

End-users of light-to-heat conversion functional materials span construction companies, automotive manufacturers, electronics producers, and apparel brands. The construction sector leads in market share due to extensive investments in green buildings and infrastructure projects aimed at reducing energy consumption. Automotive manufacturers represent the fastest-growing end-user segment, driven by the shift towards electric vehicles and the need for efficient cabin heating solutions without excessive battery drain. Electronics companies are increasingly adopting these materials to enhance device durability and user comfort through better thermal regulation. Apparel brands are capitalizing on the demand for smart, temperature-regulating fabrics, integrating these materials into sportswear and outdoor gear, marking a rising trend that supports market expansion.

The Asia-Pacific region accounted for the largest market share at 38.6% in 2024; however, North America is expected to register the fastest growth, expanding at a CAGR of 9.8% between 2025 and 2032.

To Learn More About This Report, Request A Free Sample Copy

Asia-Pacific's dominance is driven by rapid industrialization, urbanization, and strong government initiatives promoting energy-efficient construction and automotive sectors. Meanwhile, North America's growth is fueled by technological innovation, increasing adoption of smart materials, and growing investments in electric vehicle thermal management solutions. Europe, South America, and the Middle East & Africa also contribute significantly, focusing on sustainability and renewable energy integration in their respective markets.

Innovations Driving Smart Thermal Solutions

In North America, market growth is propelled by advancements in smart coating technologies and nanomaterials designed for improved light-to-heat conversion efficiency. The U.S. leads adoption in residential and commercial green building projects, with increasing use of phase change materials in insulation products. Additionally, automotive manufacturers in Canada and the U.S. are integrating these materials into electric vehicle cabins to enhance thermal comfort and battery efficiency. Consumer electronics companies are also exploring lightweight carbon-based materials for better heat dissipation in portable devices. These factors collectively support North America’s position as a rapidly evolving market.

Sustainability and Regulatory Compliance Fuel Demand

Europe’s market is shaped by stringent energy efficiency regulations and strong environmental policies driving the adoption of light-to-heat conversion functional materials. Germany and France are at the forefront, incorporating photothermal materials in building facades and automotive thermal management systems. The region also emphasizes recycling and eco-friendly manufacturing processes. Integration of these materials in textiles for smart wearables is gaining traction, especially in Nordic countries where thermal comfort is critical due to colder climates. Collaborative research initiatives across EU countries further foster innovation and accelerate market expansion.

Rapid Urbanization and Infrastructure Development Lead Market

Asia-Pacific remains the largest market due to significant investments in urban infrastructure and rising consumer awareness about energy-efficient solutions. China and Japan dominate, leveraging phase change and carbon-based materials in large-scale construction projects and public transport systems. The booming automotive industry in India and Southeast Asia is increasingly adopting these materials for cabin heating and defrosting technologies. Government incentives supporting green buildings and smart cities also contribute to heightened demand. The region’s vast population and expanding middle class drive growth in wearable thermal comfort products.

Emerging Demand from Infrastructure and Automotive Sectors

South America is witnessing a steady increase in the use of light-to-heat conversion materials, particularly in Brazil and Argentina. Growth is attributed to expanding construction activities focused on sustainability and rising demand for energy-efficient automotive components. Although the market is still developing, interest in photothermal coatings for residential buildings is gaining momentum. Moreover, local manufacturers are exploring cost-effective carbon-based materials to meet regional climate challenges. Economic development and urbanization trends continue to encourage adoption across multiple end-user sectors.

Focus on Energy Conservation Amid Harsh Climate Conditions

The Middle East & Africa market is driven by the need for efficient thermal management in regions experiencing extreme temperatures. Saudi Arabia and the UAE are leading the adoption of phase change materials in commercial and residential buildings to reduce cooling energy consumption. The automotive sector is also exploring light-to-heat functional materials for temperature regulation to enhance passenger comfort. Increasing infrastructure projects and investments in renewable energy initiatives further stimulate market growth. Innovations in lightweight, durable materials suited for harsh environments are gaining traction.

China - It holds the highest market share with a value of USD 315.4 million in 2024, driven by large-scale urbanization and government-led green building programs.

United States - Follows closely with USD 192.7 million, supported by technological advancements in smart materials and the growing electric vehicle market. Both countries benefit from strong industrial bases and continuous R&D investments, positioning them as leaders in the Light-to-heat Conversion Functional Material Market.

The Light-to-heat Conversion Functional Material Market is characterized by a competitive environment with several global and regional players focusing on innovation and strategic partnerships. Leading companies invest heavily in research and development to enhance the efficiency and durability of light-to-heat conversion materials. The market sees a mixture of established chemical manufacturers and specialized startups entering with novel nanomaterial-based products. Companies are also focusing on expanding their production capabilities to meet rising demand across construction, automotive, and wearable sectors. Additionally, mergers and acquisitions are common as players seek to consolidate their market position and diversify their product portfolios. Product differentiation through proprietary technologies, patents, and eco-friendly formulations plays a crucial role in gaining competitive advantage. Overall, the competitive landscape encourages continuous innovation, fostering advancements that cater to evolving consumer and industrial needs.

BASF SE

Dupont de Nemours, Inc.

Arkema S.A.

Mitsubishi Chemical Corporation

Covestro AG

Evonik Industries AG

Saint-Gobain S.A.

3M Company

Solvay S.A.

Mitsui Chemicals, Inc.

Technological advancements are central to the growth of the light-to-heat conversion functional materials market. Recent innovations focus on enhancing the photothermal efficiency and thermal storage capacity of materials, particularly through the use of nanostructured coatings and phase change materials. Developments in carbon-based materials, such as graphene composites, offer lightweight and flexible solutions with exceptional thermal conductivity, suitable for wearables and electronics. Furthermore, advances in polymer chemistry allow the formulation of smart coatings that dynamically adjust their heat absorption properties in response to ambient light and temperature changes. Integration of AI and machine learning in material design accelerates the optimization of these functional materials, enabling faster development cycles and improved performance. Production processes are increasingly geared towards sustainability, employing bio-based raw materials and energy-efficient manufacturing techniques to reduce environmental impact. These technological insights are driving broader adoption across multiple industries seeking energy-efficient thermal management solutions.

In December 2023, Mitsubishi Chemical Corporation launched a new range of phase change materials optimized for building insulation, enhancing energy savings by up to 20% compared to conventional materials.

In March 2024, BASF SE announced a collaboration with a leading automotive manufacturer to develop photothermal coatings for electric vehicle batteries, improving thermal regulation and extending battery life.

In January 2024, Arkema S.A. unveiled its latest carbon-based nanomaterial composites designed for wearable applications, providing superior heat retention with reduced weight and improved flexibility.

In May 2023, Covestro AG introduced a sustainable polymer-based thermal material featuring bio-based components, reducing carbon emissions during production by 30%, targeted at green construction and consumer electronics markets.

The scope of the Light-to-heat Conversion Functional Material Market Report covers detailed analysis of product types, applications, and end-user industries across global regions. It encompasses the evaluation of key market drivers, restraints, and opportunities, along with technological trends and competitive landscape assessments. The report offers insights into emerging materials such as phase change materials, photothermal coatings, and carbon-based composites, highlighting their performance metrics and potential impact across sectors like construction, automotive, electronics, and textiles. Additionally, regional market dynamics and country-specific adoption trends are examined to guide strategic decision-making. The report also addresses sustainability considerations and the role of innovation in shaping market trajectories. Overall, this comprehensive study provides stakeholders with actionable intelligence to capitalize on market potential and anticipate future developments.

| Report Attribute / Metric | Report Details |

|---|---|

| Market Name | Global Light-to-heat Conversion Functional Material Market |

| Market Revenue (2024) | USD 818.0 Million |

| Market Revenue (2032) | USD 1,641.9 Million |

| CAGR (2025–2032) | 9.1% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Report Deliverables | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape, Technological Insights, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | BASF SE, Dupont de Nemours, Inc., Arkema S.A., Mitsubishi Chemical Corporation, Covestro AG, Evonik Industries AG, Saint-Gobain S.A., 3M Company, Solvay S.A., Mitsui Chemicals, Inc. |

| Customization & Pricing | Available on Request (10% Customization is Free) |