Reports

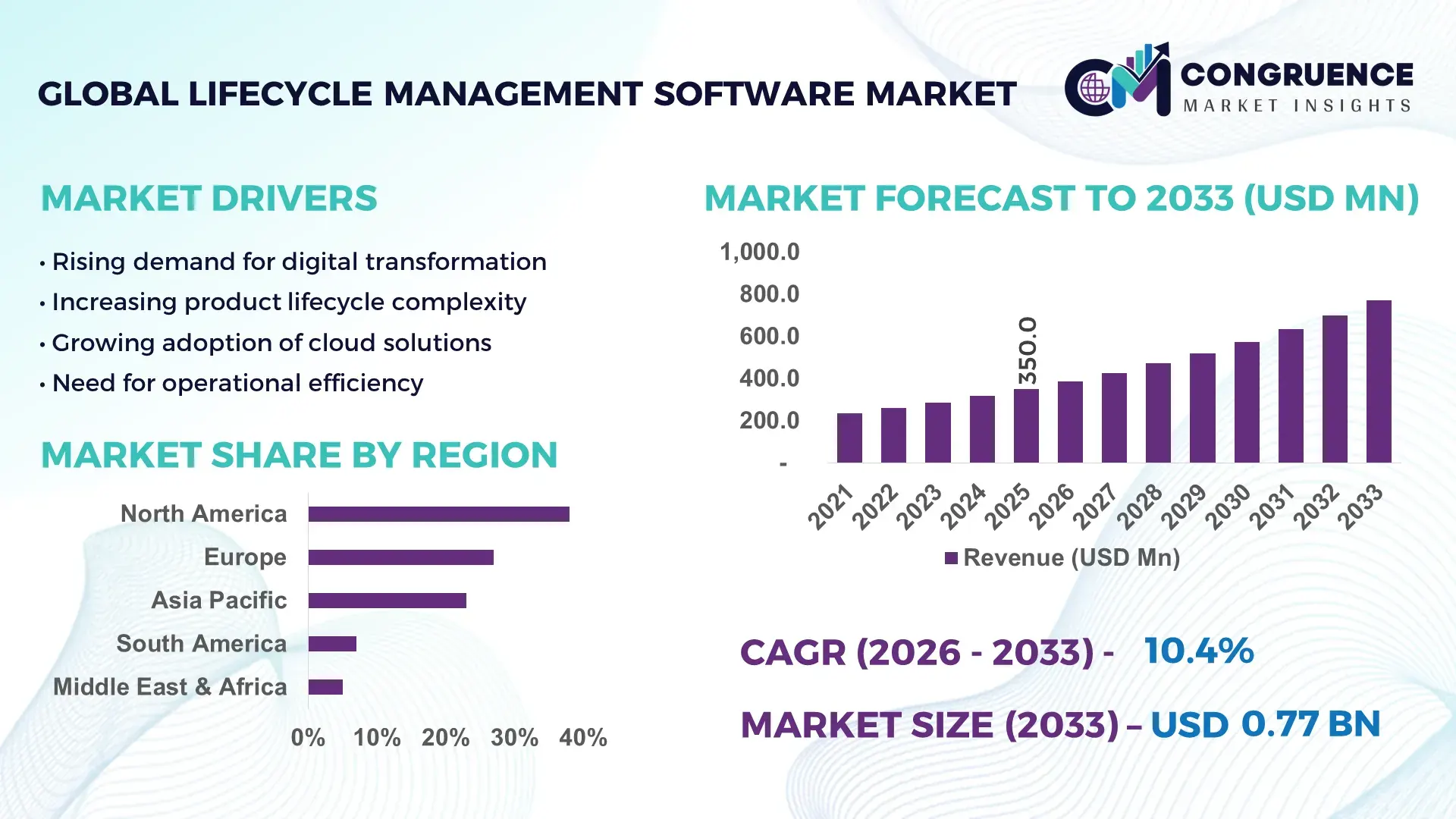

The Global Lifecycle Management Software Market was valued at USD 350.0 Million in 2025 and is anticipated to reach a value of USD 772.4 Million by 2033 expanding at a CAGR of 10.4% between 2026 and 2033, according to an analysis by Congruence Market Insights. This growth is primarily driven by increasing enterprise demand for integrated product, application, and asset lifecycle visibility to improve operational efficiency and compliance.

The United States continues to demonstrate strong industrial and technological positioning in the Lifecycle Management Software Market, supported by high enterprise digitization rates and advanced IT infrastructure. Over 68% of large enterprises in the U.S. have implemented lifecycle management platforms across product development and IT operations. The country hosts more than 40% of global PLM and ALM solution providers, with annual enterprise software investments exceeding USD 120 billion. Key sectors such as aerospace, automotive, and healthcare contribute significantly, with over 55% of manufacturing firms integrating lifecycle software into production workflows. Additionally, cloud-based lifecycle management deployments account for nearly 62% of new implementations, reflecting strong adoption of SaaS-based enterprise solutions. AI-driven lifecycle analytics tools have seen a 35% increase in deployment across Fortune 500 firms, further enhancing predictive maintenance and product lifecycle optimization capabilities.

Market Size & Growth: USD 350.0 Million in 2025, projected to reach USD 772.4 Million by 2033 at a CAGR of 10.4%, driven by enterprise-wide digital transformation and lifecycle optimization needs.

Top Growth Drivers: 64% enterprises adopting cloud PLM systems, 52% efficiency improvement in product development cycles, 48% increase in demand for compliance automation tools.

Short-Term Forecast: By 2028, lifecycle automation tools are expected to reduce operational costs by 28% and improve workflow efficiency by 32%.

Emerging Technologies: AI-based lifecycle analytics, digital twin integration, and low-code lifecycle management platforms are gaining traction.

Regional Leaders: North America to reach USD 310 Million by 2033 with high SaaS adoption, Europe USD 210 Million driven by regulatory compliance, Asia-Pacific USD 180 Million fueled by manufacturing digitization.

Consumer/End-User Trends: Manufacturing and IT sectors account for over 60% of adoption, with increasing uptake among SMEs leveraging cloud-based lifecycle tools.

Pilot or Case Example: In 2025, a global automotive firm reduced product development time by 35% through AI-enabled PLM deployment.

Competitive Landscape: Market leader holds approximately 18% share, followed by key players including Siemens, Dassault Systèmes, PTC, IBM, and Oracle.

Regulatory & ESG Impact: Over 45% of enterprises align lifecycle systems with ESG reporting frameworks and regulatory compliance mandates.

Investment & Funding Patterns: More than USD 2.5 Billion invested in lifecycle software innovation and SaaS platforms over the past two years.

Innovation & Future Outlook: Integration of IoT-enabled lifecycle monitoring and predictive analytics is expected to redefine product lifecycle optimization strategies.

Lifecycle Management Software Market is influenced by manufacturing (38%), IT services (27%), and healthcare (14%) sectors, with rapid adoption of AI-driven lifecycle analytics and cloud-native PLM platforms. Regulatory compliance frameworks such as digital traceability mandates and sustainability reporting are shaping demand, while Asia-Pacific consumption is rising due to industrial automation. Future growth is driven by digital twin integration and predictive lifecycle intelligence.

The Lifecycle Management Software Market holds strategic importance as enterprises increasingly seek unified platforms to manage product, application, and asset lifecycles across complex digital ecosystems. Organizations are leveraging lifecycle management tools to streamline product development, ensure regulatory compliance, and enhance operational transparency. AI-powered lifecycle platforms deliver up to 35% improvement in predictive maintenance accuracy compared to traditional monitoring systems, significantly reducing downtime and operational risks.

North America dominates in volume, while Asia-Pacific leads in adoption with over 58% of manufacturing enterprises actively deploying lifecycle management solutions to support industrial automation and smart factory initiatives. The integration of digital twins and IoT sensors is further strengthening lifecycle monitoring capabilities, enabling real-time asset performance tracking across industries such as automotive, aerospace, and energy.

By 2028, AI-driven lifecycle analytics is expected to improve operational efficiency by 30% and reduce product development cycles by approximately 25%. Enterprises are also aligning lifecycle systems with ESG goals, with firms committing to 40% reduction in carbon emissions through optimized product design and lifecycle sustainability practices by 2030.

In 2025, a leading German automotive manufacturer achieved a 33% reduction in production defects through the deployment of AI-enabled PLM systems, highlighting measurable operational gains. As organizations prioritize digital transformation and regulatory compliance, the Lifecycle Management Software Market is positioned as a critical pillar for resilience, efficiency, and sustainable business growth in the global economy.

The Lifecycle Management Software Market is characterized by rapid technological evolution, increasing enterprise digitization, and growing demand for integrated lifecycle visibility across industries. Organizations are adopting lifecycle management platforms to streamline workflows, enhance product quality, and improve compliance with regulatory frameworks. Approximately 62% of enterprises globally have transitioned to cloud-based lifecycle systems, enabling real-time collaboration and scalability. The market is influenced by the rise of Industry 4.0, where over 55% of manufacturers rely on lifecycle tools to manage complex production processes. Additionally, the growing importance of data-driven decision-making has led to a 40% increase in demand for analytics-enabled lifecycle platforms. Integration with enterprise systems such as ERP and CRM is further driving adoption, with nearly 48% of organizations prioritizing unified digital ecosystems. However, factors such as high implementation complexity and cybersecurity concerns continue to shape market dynamics, requiring strategic investments and robust IT governance frameworks.

The rapid pace of digital transformation across industries is a primary driver for the Lifecycle Management Software Market. Over 70% of enterprises are investing in digital platforms to enhance operational efficiency and streamline product development cycles. Lifecycle management software enables centralized data management, reducing product development time by up to 35% and improving cross-functional collaboration by 45%. Manufacturing industries, accounting for nearly 55% of adoption, are integrating lifecycle tools with IoT and automation systems to enhance production efficiency. Additionally, cloud-based lifecycle solutions have witnessed a 60% adoption rate among large enterprises due to scalability and cost-effectiveness. The growing need for regulatory compliance and digital traceability has further accelerated adoption, with over 50% of organizations implementing lifecycle systems to meet industry standards and reduce compliance risks.

Despite strong demand, the Lifecycle Management Software Market faces challenges related to implementation complexity and system integration. Nearly 42% of enterprises report difficulties in integrating lifecycle platforms with existing legacy systems, leading to extended deployment timelines. High initial setup costs and the need for specialized IT expertise further limit adoption, particularly among small and medium-sized enterprises. Additionally, data migration issues affect approximately 35% of organizations, impacting system performance and reliability. Cybersecurity concerns also play a significant role, with over 48% of enterprises citing data protection risks as a barrier to adoption. These challenges require organizations to invest in robust IT infrastructure and skilled personnel, increasing the overall cost and complexity of lifecycle software implementation.

The integration of artificial intelligence and digital twin technologies presents significant growth opportunities for the Lifecycle Management Software Market. AI-driven lifecycle platforms can improve predictive maintenance accuracy by up to 40%, enabling organizations to reduce downtime and optimize asset performance. Digital twin adoption is increasing, with over 38% of manufacturing firms utilizing virtual replicas of physical assets to simulate and optimize production processes. The rise of smart factories and Industry 4.0 initiatives is further driving demand for advanced lifecycle solutions, particularly in sectors such as automotive and aerospace. Additionally, cloud-based deployment models are expanding market accessibility, with nearly 50% of SMEs adopting SaaS lifecycle platforms to enhance operational efficiency. These technological advancements are creating new avenues for innovation and market expansion.

Data security and regulatory compliance remain critical challenges in the Lifecycle Management Software Market. Approximately 52% of enterprises identify cybersecurity threats as a major concern, particularly in cloud-based lifecycle deployments. The increasing volume of sensitive product and operational data requires advanced security protocols, with organizations investing up to 20% of their IT budgets in cybersecurity measures. Regulatory complexities across regions also pose challenges, as companies must comply with multiple standards and data protection laws. For instance, over 45% of organizations report difficulties in aligning lifecycle systems with evolving compliance requirements. Additionally, the lack of standardized frameworks for lifecycle data management creates inconsistencies, affecting system interoperability and performance. These challenges necessitate continuous innovation in security and compliance solutions.

• Rising adoption of AI-powered lifecycle analytics: Over 58% of enterprises have integrated AI-based analytics into lifecycle platforms, enabling predictive maintenance improvements of 35% and reducing operational downtime by 28%, particularly in manufacturing and IT sectors.

• Increasing shift toward cloud-native lifecycle platforms: Approximately 62% of new deployments are cloud-based, with enterprises reporting 30% faster implementation times and 25% lower infrastructure costs compared to on-premise systems, especially across SMEs and mid-sized organizations.

• Expansion of digital twin integration across industries: Around 41% of industrial enterprises are leveraging digital twins, resulting in 33% improvement in asset performance monitoring and 27% reduction in production inefficiencies through real-time simulation and optimization.

• Growing focus on ESG and compliance-driven lifecycle management: Nearly 47% of enterprises are integrating sustainability metrics into lifecycle systems, achieving up to 22% reduction in carbon emissions through optimized product design and lifecycle resource management.

The Lifecycle Management Software Market demonstrates a well-defined segmentation structure across type, application, and end-user categories, reflecting its widespread adoption across industries. From a type perspective, cloud-based solutions dominate due to scalability and integration capabilities, while on-premise systems retain relevance in regulated sectors. Application-wise, product lifecycle management (PLM) and application lifecycle management (ALM) collectively account for a significant share, driven by digital transformation initiatives across manufacturing and IT industries. End-user segmentation highlights large enterprises as primary adopters, leveraging lifecycle tools for operational efficiency and compliance. Meanwhile, SMEs are steadily increasing adoption due to cost-effective SaaS offerings. Across all segments, the market reflects strong alignment with automation, data analytics, and AI-driven decision-making trends. Increasing enterprise digitization, rising complexity in product development, and regulatory compliance requirements continue to shape segmentation dynamics, making lifecycle management software a critical enterprise solution globally.

The Lifecycle Management Software Market is segmented into cloud-based, on-premise, and hybrid solutions. Cloud-based lifecycle management software dominates the market, accounting for approximately 58% share, primarily due to its scalability, cost efficiency, and ease of integration with enterprise systems. Organizations increasingly prefer cloud deployment as it enables remote accessibility, real-time collaboration, and seamless updates, particularly beneficial for globally distributed teams. In comparison, on-premise solutions hold around 27% share, largely driven by industries such as defense, healthcare, and banking, where data security and regulatory compliance are critical. However, hybrid solutions are emerging as the fastest-growing segment, expected to expand at a CAGR of 14.8%, as enterprises seek to balance flexibility with data control by combining cloud and on-premise infrastructures. Other niche segments, including industry-specific lifecycle platforms and AI-integrated lifecycle tools, collectively contribute nearly 15% of the market. These solutions are gaining traction in sectors requiring customized workflows and predictive analytics capabilities. The increasing integration of AI and machine learning into lifecycle management platforms is further enhancing decision-making and operational efficiency.

• In 2025, a global technology research initiative reported that over 65% of Fortune 500 companies transitioned at least one lifecycle management function to cloud-based platforms, significantly improving cross-functional collaboration and reducing deployment time.

Lifecycle management software serves multiple application areas, including product lifecycle management (PLM), application lifecycle management (ALM), service lifecycle management (SLM), and asset lifecycle management. Among these, PLM leads the market with approximately 41% share, driven by its critical role in managing product design, development, and innovation processes across manufacturing, automotive, and electronics industries. ALM follows with around 28% share, widely adopted in IT and software development sectors for managing application development cycles and ensuring faster time-to-market. However, asset lifecycle management is the fastest-growing application segment, projected to expand at a CAGR of 15.2%, fueled by increasing demand in infrastructure, energy, and utilities sectors for predictive maintenance and asset optimization. Service lifecycle management is also gaining traction, particularly in customer-centric industries such as telecom and healthcare. Other applications collectively account for nearly 31% of the market, reflecting diversified use cases across industries. Consumer adoption trends further reinforce market growth. In 2025, over 44% of global enterprises reported implementing lifecycle management tools to enhance product innovation cycles. Additionally, nearly 52% of IT organizations integrated ALM platforms to streamline DevOps processes and improve software delivery timelines.

• In 2025, a global industry study highlighted that lifecycle-based predictive maintenance systems were deployed across more than 200 industrial facilities, reducing equipment downtime by up to 30% and improving operational efficiency.

The Lifecycle Management Software Market is segmented into large enterprises, small & medium enterprises (SMEs), and industry-specific end-users such as manufacturing, IT & telecom, healthcare, BFSI, and retail. Large enterprises dominate the market with approximately 62% share, as they require robust lifecycle management solutions to handle complex operations, ensure compliance, and integrate multiple business processes. SMEs account for around 24% share, but their adoption is increasing rapidly due to the availability of cost-effective cloud-based solutions. Among end-users, the IT & telecom sector represents the fastest-growing segment, expected to expand at a CAGR of 16.1%, driven by increasing demand for application lifecycle management and DevOps integration. Manufacturing remains a key contributor, with over 35% adoption rate within the segment, leveraging PLM solutions to optimize production and reduce time-to-market. Healthcare and BFSI sectors are also witnessing steady adoption, particularly for compliance management and data security purposes. Other end-users collectively contribute nearly 14% of the market, reflecting growing penetration in retail, energy, and logistics sectors. Consumer adoption insights indicate that in 2025, more than 48% of enterprises globally adopted lifecycle management software to improve operational transparency. Additionally, over 55% of organizations in digital-first industries reported integrating lifecycle tools with AI-driven analytics for better decision-making.

• In 2025, a major enterprise technology survey revealed that over 500 SMEs globally implemented lifecycle management platforms, resulting in a 25% improvement in project delivery timelines and enhanced resource utilization.

North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 12.1% between 2026 and 2033.

North America’s dominance is supported by strong enterprise IT infrastructure, with over 65% of large organizations implementing lifecycle management platforms across operations. Europe follows with approximately 27% market share, driven by stringent regulatory frameworks and increasing demand for compliance-focused lifecycle solutions. Asia-Pacific holds around 23% share, with rapid industrialization and digital transformation initiatives accelerating adoption, particularly in China, India, and Japan. South America contributes nearly 7%, supported by growing IT investments in Brazil and Argentina, while the Middle East & Africa accounts for approximately 5%, driven by infrastructure development and energy sector demand. Across regions, cloud-based lifecycle solutions represent over 60% of new deployments, reflecting a global shift toward scalable and cost-effective enterprise software models.

North America holds approximately 38% of the Lifecycle Management Software Market, driven by high adoption across manufacturing, aerospace, healthcare, and financial services industries. The region benefits from strong government support for digital transformation, including initiatives promoting Industry 4.0 and smart manufacturing. Over 68% of enterprises in the region have integrated lifecycle management tools into their operations. Technological advancements such as AI integration and digital twin implementation are widely adopted, with nearly 50% of firms utilizing advanced analytics within lifecycle platforms. A key player, Autodesk, has expanded its cloud-based lifecycle solutions, enabling real-time collaboration across distributed teams. Consumer behavior in the region shows higher adoption among large enterprises, particularly in healthcare and finance, where compliance and data security are critical factors influencing lifecycle software usage.

Europe accounts for nearly 27% of the Lifecycle Management Software Market, with major contributions from Germany, the UK, and France. The region’s growth is driven by stringent regulatory requirements such as digital product traceability and sustainability mandates. Approximately 54% of enterprises in Europe use lifecycle management tools for compliance and reporting purposes. Adoption of emerging technologies such as AI and digital twins is increasing, with over 45% of manufacturers integrating these capabilities into lifecycle workflows. A notable player, Dassault Systèmes, continues to expand its 3DEXPERIENCE platform, supporting collaborative product development across industries. Consumer behavior reflects strong demand for explainable and compliant lifecycle systems, as regulatory pressure pushes organizations to adopt transparent and auditable software solutions.

Asia-Pacific represents one of the fastest-growing regions in the Lifecycle Management Software Market, holding approximately 23% share with rapid expansion across China, India, and Japan. The region is driven by large-scale manufacturing activities, with over 60% of industrial enterprises adopting lifecycle solutions to enhance productivity and efficiency. Infrastructure development and smart factory initiatives are key drivers, particularly in China, where industrial automation adoption exceeds 55%. Local players and global vendors are investing heavily in cloud-based lifecycle platforms tailored to SMEs. Consumer behavior in the region is influenced by mobile-first adoption, with over 58% of users accessing lifecycle platforms through mobile-enabled interfaces, supporting real-time decision-making and operational agility.

South America accounts for approximately 7% of the Lifecycle Management Software Market, with Brazil and Argentina leading adoption. The region’s growth is supported by increasing investments in IT infrastructure and enterprise software solutions. Over 42% of organizations in South America have adopted lifecycle management tools to improve operational efficiency and compliance. The energy and infrastructure sectors play a significant role, contributing nearly 35% of regional demand. Government initiatives promoting digital transformation and trade policies encouraging technology adoption are further supporting market growth. Consumer behavior highlights a growing preference for localized lifecycle solutions, particularly in media and language-intensive industries where customization is essential for effective implementation.

The Middle East & Africa region holds around 5% of the Lifecycle Management Software Market, driven by demand in oil & gas, construction, and infrastructure sectors. Countries such as the UAE and South Africa are leading adoption, with over 38% of enterprises implementing lifecycle solutions to enhance operational efficiency. Technological modernization initiatives, including smart city projects and digital transformation programs, are accelerating demand for lifecycle management tools. Local regulations and international trade partnerships are encouraging technology adoption across industries. Consumer behavior in the region reflects increasing reliance on cloud-based solutions, with over 52% of organizations preferring SaaS lifecycle platforms for scalability and cost efficiency.

United States – 34% Market share: Strong enterprise IT infrastructure and high adoption across manufacturing and aerospace industries

China – 18% Market share: Rapid industrialization and large-scale manufacturing digitization driving demand

The Lifecycle Management Software Market is moderately consolidated, with the top five companies accounting for approximately 55% of the total market share. The competitive landscape is characterized by the presence of over 120 active global and regional players, ranging from established enterprise software providers to emerging SaaS-based innovators. Leading companies focus on strategic initiatives such as mergers, acquisitions, and partnerships to expand their product portfolios and geographic presence. For instance, several vendors have integrated AI and digital twin technologies into their lifecycle platforms, resulting in up to 30% improvement in operational efficiency for enterprise users.

Cloud-based lifecycle solutions dominate competitive strategies, with more than 60% of vendors offering SaaS-based platforms to cater to SMEs and large enterprises. Product innovation remains a key differentiator, with companies investing heavily in low-code development tools and predictive analytics capabilities. Additionally, partnerships with manufacturing and IT service providers have increased by nearly 25% in recent years, enabling vendors to deliver industry-specific lifecycle solutions. The market also witnesses increasing competition from niche players specializing in application lifecycle management and asset lifecycle optimization, intensifying innovation and pricing strategies across the industry.

Dassault Systèmes

PTC

IBM

Oracle

SAP

Autodesk

Hewlett Packard Enterprise

Infor

Arena Solutions

Aras Corporation

Propel Software

Centric Software

Jama Software

ServiceNow

The Lifecycle Management Software Market is undergoing rapid transformation driven by advanced technologies such as artificial intelligence, digital twins, cloud computing, and IoT integration. AI-enabled lifecycle platforms are now used by over 48% of enterprises, enabling predictive analytics and automation across product and application lifecycles. These systems can improve maintenance accuracy by up to 35%, reducing downtime and operational disruptions. Digital twin technology is another key innovation, with approximately 40% of manufacturing firms adopting virtual asset models to simulate and optimize production processes in real time.

Cloud computing continues to dominate deployment models, accounting for more than 60% of lifecycle software implementations, providing scalability, flexibility, and cost efficiency. Low-code and no-code platforms are gaining traction, with nearly 32% of organizations adopting these tools to accelerate application lifecycle management and reduce development complexity. Additionally, IoT integration allows real-time data collection and monitoring, with over 55% of industrial enterprises leveraging connected devices to enhance lifecycle visibility.

Cybersecurity technologies are also evolving, with organizations allocating up to 20% of their IT budgets to secure lifecycle data and ensure compliance with regulatory standards. Blockchain integration is emerging as a solution for secure data traceability, particularly in supply chain and manufacturing applications. These technological advancements are reshaping lifecycle management strategies, enabling organizations to achieve higher efficiency, improved compliance, and enhanced decision-making capabilities.

• In August 2025, Siemens Digital Industries Software announced that its Teamcenter platform was ranked #1 in ABI Research’s PLM competitive assessment, scoring highest in both innovation and implementation. The platform’s integration of industrial-grade AI and digital thread capabilities significantly enhanced product lifecycle efficiency and cross-domain collaboration. Source: www.siemens.com

• In November 2025, Siemens introduced the Teamcenter Service Lifecycle Management (SLM) 2512 release, featuring AI-powered authoring tools for automated service plan creation, advanced spare parts visibility, and enhanced analytics for lifecycle optimization. These upgrades improved service planning accuracy and enabled faster decision-making across distributed engineering teams.

• In December 2025, IBM released version 7.2 of its Engineering Lifecycle Management (ELM) platform, introducing enhanced automation, improved requirements management, and upgraded configuration control features. The update also delivered faster workflow execution and improved reporting capabilities, strengthening lifecycle traceability for complex engineering systems.

• In March 2025, Propel Software launched “Propel One,” an AI-driven agentic platform built on Salesforce Agentforce, designed to automate lifecycle processes across engineering, quality, and supply chain functions. The solution introduced a unified product data model (“Product Graph”), improving real-time decision-making and cross-functional collaboration.

The Lifecycle Management Software Market Report provides a comprehensive analysis of key segments, applications, and regional dynamics shaping the industry. The report covers various software types including product lifecycle management, application lifecycle management, and asset lifecycle management, highlighting their adoption across industries such as manufacturing, IT, healthcare, BFSI, and energy. Manufacturing alone contributes over 45% of total adoption, reflecting its reliance on lifecycle tools for product development and process optimization.

Geographically, the report examines major regions including North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, each contributing distinct adoption patterns and technological advancements. North America leads with strong enterprise adoption, while Asia-Pacific demonstrates rapid growth driven by industrial automation and digital transformation initiatives. The report also explores application areas such as product design, maintenance, compliance management, and IT lifecycle automation, providing insights into their operational significance and adoption trends.

Additionally, the report highlights technological advancements including AI, digital twins, IoT, and cloud computing, which are transforming lifecycle management processes. Emerging segments such as low-code lifecycle platforms and blockchain-enabled traceability are also analyzed for their future potential. The scope further includes competitive benchmarking, innovation trends, and enterprise adoption patterns, offering decision-makers a holistic view of market opportunities and strategic pathways for growth.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 350.0 Million |

| Market Revenue (2033) | USD 772.4 Million |

| CAGR (2026–2033) | 10.4% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Siemens; Dassault Systèmes; PTC; IBM; Oracle; SAP; Autodesk; Hewlett Packard Enterprise; Infor; Arena Solutions; Aras Corporation; Propel Software; Centric Software; Jama Software; ServiceNow |

| Customization & Pricing | Available on Request (10% Customization Free) |