Reports

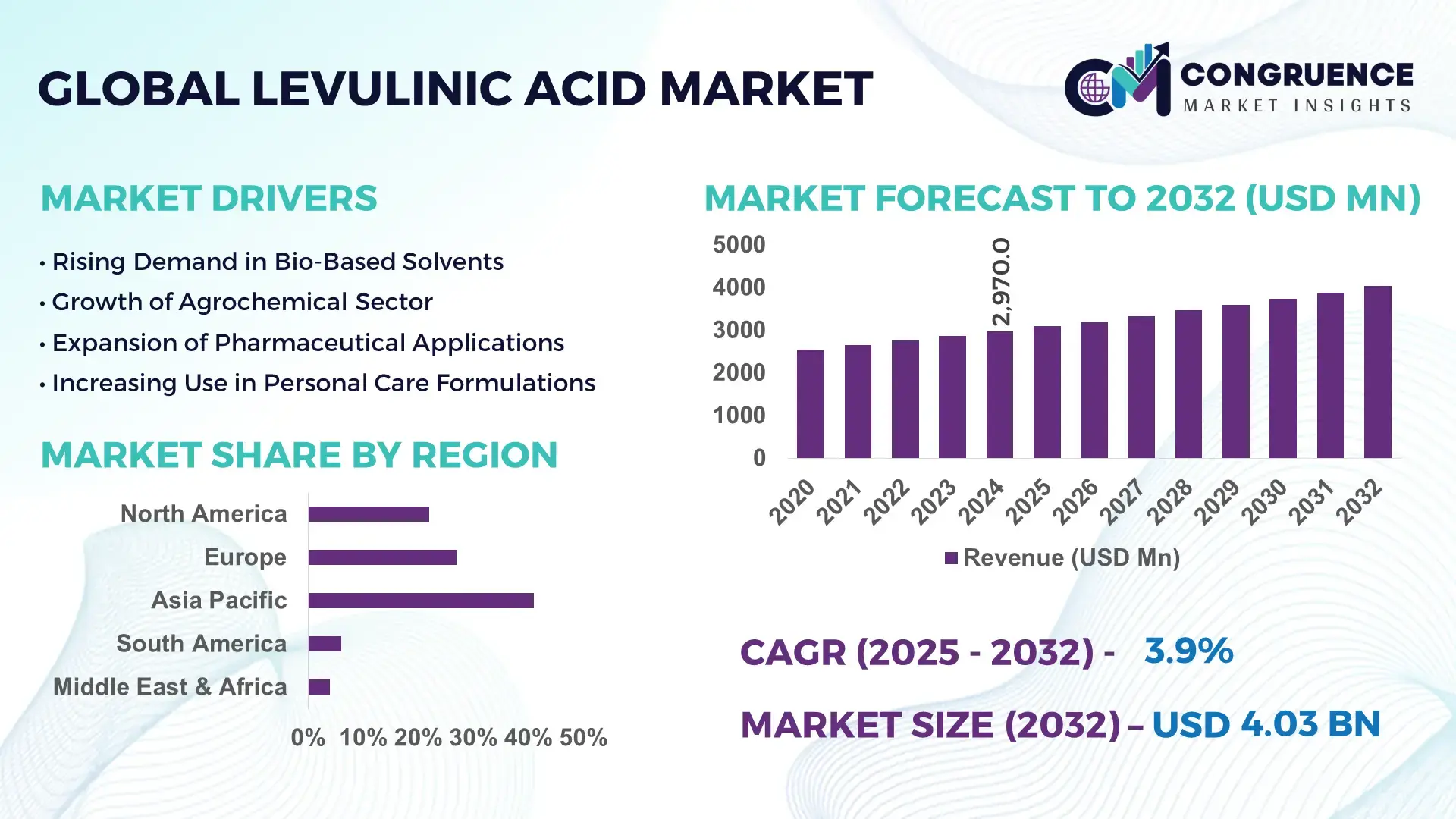

The Global Levulinic Acid Market was valued at USD 2,970.0 Million in 2024 and is anticipated to reach USD 4,033.5 Million by 2032, expanding at a CAGR of 3.9% between 2025 and 2032, according to an analysis by Congruence Market Insights. Due to increasing commercialization of bio-based platform chemicals alongside rising adoption of levulinic-acid derivatives in fuels, solvents, agrochemicals, and specialty chemical transformations.

China, the leading country in this marketplace, continues to scale industrial capacity through national biomass-conversion projects and commercial pilot units. Several newly commissioned facilities target around 5,000 tonnes per year of additional levulinic acid output by 2026. Chinese firms have also invested heavily in catalytic process intensification, continuous hydrolysis systems, and lignocellulosic feedstock optimization. Industrial announcements indicate rising capital deployment into fuel-additive and cosmetic-grade derivatives, supported by incremental improvements in conversion yields and biomass-to-product efficiency. Domestic technological programs emphasize higher productivity reactors, low-impurity grades, and expanded downstream derivative production.

Market Size & Growth: Current market value USD 2,970.0 Million; projected USD 4,033.5 Million by 2032; CAGR 3.9%, supported by expanding demand for bio-based intermediates.

Top Growth Drivers: 35%, 22%, and 18% contribution from rising bio-based applications, efficiency gains, and derivative diversification.

Short-Term Forecast: By 2028, processing cost reductions expected to improve manufacturing efficiency by approximately 12%.

Emerging Technologies: Continuous hydrolysis, heterogenous catalyst platforms, and integrated biorefinery routing.

Regional Leaders: Asia-Pacific projected at ~USD 1,100M by 2032 with strong feedstock integration; North America ~USD 1,200M by 2032 with advanced applications; Europe ~USD 750M by 2032 with specialty chemical adoption.

Consumer/End-User Trends: Strong uptake in agrochemical formulations, cosmetic esters, and green solvents, with high adoption in >40% bio-content product lines.

Pilot or Case Example: 2024 commercial pilot demonstrated yield improvement of roughly 9–12% through continuous hydrolysis deployment.

Competitive Landscape: Market leader holds approximately 20% share, followed by 3–5 key competitors active in biorefinery and specialty-chemical domains.

Regulatory & ESG Impact: Sustainability mandates and bio-based procurement incentives accelerate investment and product transition.

Investment & Funding Patterns: Recent investments in catalyst R&D and scale-up facilities exceed USD 50 Million, alongside structured project-finance models.

Innovation & Future Outlook: Advancements in yield-boosting catalysts, flexible feedstock processing, and downstream integration continue shaping future competitiveness.

The Levulinic Acid Market is driven by expanding applications in agrochemicals, fuel additives, plasticizers, and personal care esters. Innovations in continuous hydrolysis and advanced catalysts have improved yields by up to 10%. Regulatory preference for low-carbon chemicals and growth in Asia-Pacific consumption strengthen adoption. Emerging interest in high-purity derivatives and integrated biorefinery models supports long-term market expansion.

The levulinic acid market has emerged as a strategically important segment within the global bio-based chemical value chain due to its versatility in producing high-value esters, ketals, solvents, and fuel additives. Its relevance increases as industries transition toward low-carbon and renewable feedstock pathways. Continuous hydrolysis and advanced catalyst systems are reshaping production economics: new hydrolysis technologies deliver about 12% improvement compared to older batch-processing standards, significantly enhancing throughput and energy efficiency.

Regionally, Asia-Pacific dominates in volume, supported by integrated biomass processing hubs, while North America leads in adoption, with more than 40% of large formulators deploying levulinic-based derivatives in R&D, pilots, or early commercialization. By 2028, emerging AI-enabled process optimisation systems are expected to reduce energy intensity by 8–12%, strengthening competitiveness for large-scale producers.

ESG and compliance are central to market expansion. Large chemical manufacturers aim for 20–30% reductions in lifecycle emissions by 2030, driven by bio-feedstock switching, heat-integration upgrades, and adoption of low-waste catalyst systems. In 2024, a biorefinery project in East Asia achieved an 11% reduction in feedstock-to-product energy use after deploying advanced process controls and a continuous catalytic loop.

Taken together, these dynamics underscore the levulinic acid sector’s role as a reliable cornerstone in the broader shift to sustainable chemical manufacturing. With improvements in feedstock efficiency, downstream integration, and regulatory alignment, the Levulinic Acid Market is positioned to become a pillar of resilience, compliance, and sustainable industrial growth over the next decade.

The Levulinic Acid Market is driven by the interplay of technological advancements, regulatory momentum, and evolving industrial applications. It is increasingly used as a platform chemical for esters, ketals, and next-generation solvents across agriculture, personal care, and fuel additive formulations. Supply dynamics are shaped by the rise of integrated biorefineries and the scaling of continuous hydrolysis technologies that improve yield performance and lower operating intensity. Regulatory support for bio-based chemicals further accelerates product substitution and innovation. At the same time, challenges such as biomass variability, capital-intensive infrastructure, and the need for multi-stage purification for high-purity grades influence the pace of market evolution and investment decision-making.

Growing preference for bio-based chemicals across agrochemicals, fuels, polymers, and cosmetics is accelerating the use of levulinic acid. Industrial users are actively integrating levulinates and derived esters as substitutes for petrochemical intermediates. Pilot programs across multiple sectors report yield improvements and expanded capacity targets, with several facilities aiming for approximately 5,000 tonnes per year within the next few years. More than one-third of specialty chemical formulators are currently evaluating levulinic-acid-based inputs in their development pipelines, driving multi-year procurement strategies and fostering downstream derivative innovation.

The market faces notable constraints due to dependency on lignocellulosic biomass, which requires extensive preprocessing, stable supply chains, and regional aggregation networks. Capital for building continuous hydrolysis lines, catalytic reactors, and integrated biorefinery infrastructure remains substantial, leading to longer financing cycles and phased expansions. Achieving cosmetic- or food-grade purity demands additional refining, increasing operational complexity. These conditions slow rapid scaling despite strong end-use interest across several industries, making strategic partnerships and modular plant designs critical for expansion.

Technology maturation offers substantial opportunities through improved catalysts, feedstock flexibility, and streamlined processing. Advanced catalytic platforms and continuous reactors have been shown to cut operational intensity and boost yields by 8–12%, enabling more economical production. Downstream integration—ranging from green solvents to specialty esters—provides higher-margin pathways that extend beyond core acid output. Modular production units, licensing models, and biorefinery clustering enable cost-effective scale-up and expand commercial access to levulinic-derived formulations across multiple industries.

Global commercialization of new levulinic-acid derivatives is slowed by region-specific regulatory frameworks, each requiring extensive safety, stability, and impurity data. Qualification timelines for agrochemical, cosmetic, or food-grade applications can extend into multi-year cycles. Additional laboratory testing and documentation elevate development costs. Combined with technical barriers in feedstock quality and the capital demands of scaling advanced reactors, these regulatory and operational burdens create significant timeline pressures for producers seeking market entry and expansion.

Process Intensification & Yield Gains: Adoption of continuous hydrolysis and heterogenous catalytic systems has delivered 9–12% yield improvements, cut specific energy use by 8–10%, and reduced batch-to-batch cycle time variability. These performance gains are driving accelerated scale-up across pilot and demo facilities.

Regional Capacity Expansion: Asia-Pacific capacity additions include projects targeting ~5,000 tonnes/year by 2026, while North America shows strong demand from fuel-additive and specialty-chemical users, with over 40% of major formulators trialing levulinic derivatives. This regional divergence is shaping investment flows and product development strategies.

Downstream Product Diversification: High-value esters, ketals, and bio-based solvents are expanding rapidly, with double-digit percentage growth in formulation demand. These derivatives support emerging product lines in agrochemicals, cosmetics, and polymers, improving industry margins and driving advanced R&D commitments.

Evolving Finance & Collaboration Models: Recent project-level investment has reached multi-million-dollar levels, enabling technology scale-up, catalyst development, and integrated plant expansions. Companies are increasingly adopting licensing, joint ventures, and offtake agreements to secure long-term supply and reduce capital risks while pursuing efficiency improvements.

The global levulinic acid market is segmented across types, applications, and end-user industries, each contributing uniquely to overall demand. Type segmentation reflects the growing adoption of bio-based chemical intermediates, with select derivatives gaining traction due to their compatibility with large-scale manufacturing and sustainable material innovation. Applications range from industrial solvents and agricultural formulations to pharmaceuticals and personal care inputs, each shaped by evolving regulatory standards and performance requirements. End-user demand is led by industries undergoing rapid shifts toward green chemistry, supported by measurable increases in product substitution rates and biodegradable inputs. Together, these segments demonstrate structured adoption patterns influenced by material efficiency, compliance mandates, and technology upgrades across production ecosystems. The combined segmentation landscape provides a balanced understanding of supply-chain utilization, product versatility, and the strategic positioning of levulinic acid within emerging bio-economy frameworks.

The type segment in the levulinic acid market comprises levulinic acid, levulinate esters, δ-aminolevulinic acid (ALA), ketals, and other specialty derivatives. Levulinic acid itself leads the market, accounting for approximately 46% of total consumption, primarily due to its widespread use as a platform chemical across polymer, resin, and solvent manufacturing. Its compatibility with biomass-derived feedstocks and suitability for scalable conversion processes further supports its leadership position. δ-Aminolevulinic acid represents the fastest-growing type, supported by rising adoption in agricultural biostimulants and precision farming inputs, expanding at an estimated 11.2% CAGR. Levulinate esters and ketal derivatives collectively hold around 29% share, driven by niche demand in specialty plastics, coatings, and fragrance formulations. The remaining minor derivatives contribute approximately 12%, mainly supporting experimental material research and high-performance chemical formulations.

The application landscape includes solvents, plasticizers, agrochemicals, pharmaceuticals, personal care formulations, and fuel additives. Solvents remain the dominant application segment with a 38% share, supported by increasing replacement of petroleum-derived solvents with environmentally compliant alternatives. Personal care and cosmetic formulations account for 24%, while agrochemicals—including uses of ALA—hold 19%. However, agrochemical applications are expanding the fastest, growing at an estimated 10.6% CAGR, as adoption of plant-growth regulators and amino-acid-based stimulants accelerates in crop-intensive markets. Pharmaceutical and fuel additive applications collectively contribute 19%, maintaining relevance through targeted, high-value use cases. Consumer and industry adoption trends reinforce these patterns. In 2024, more than 41% of agro-input manufacturers globally reported piloting bio-based substitutes for traditional growth regulators, while over 55% of eco-focused consumer brands reported increasing demand for natural solvent systems in product lines.

End-users of levulinic acid span the chemicals industry, agriculture, pharmaceuticals, personal care manufacturers, and fuel additive producers. The chemicals sector leads with 44% market share, supported by extensive use of levulinic-acid-based intermediates in resin systems, specialty polymers, and high-performance plasticizers. Agriculture represents the fastest-growing end-user segment, expanding at an estimated 10.9% CAGR, driven by increasing adoption of ALA-based biostimulants and regulatory moves favoring low-toxicity crop enhancement inputs. Personal care and pharmaceutical industries collectively contribute 32%, reflecting rising consumer demand for bio-based formulations, while fuel additive end-users and industrial blending segments together account for approximately 24% of usage. Emerging adoption data also reinforces this shift. In 2024, more than 36% of mid-scale cosmetic manufacturers reported transitioning to bio-derived solvent systems, while over 48% of agricultural enterprises in Asia-Pacific documented trials integrating ALA-based growth formulations.

Asia-Pacific accounted for the largest market share at 41% in 2024; however, Middle East & Africa is expected to register the fastest growth, expanding at a CAGR of 12.4% between 2025 and 2032.

Asia-Pacific’s dominance reflects its strong manufacturing base, abundant access to biomass feedstocks, and rising investment in bio-based chemical production. Europe followed with approximately 27% share due to stringent sustainability mandates and accelerated replacement of petrochemical intermediates. North America accounted for roughly 22%, driven by advanced chemical processing facilities and rising demand for green solvents. South America and the Middle East & Africa held 6% and 4% respectively, but both regions are experiencing accelerated adoption as agricultural productivity requirements grow and local industries shift toward bio-derived inputs. These shifts highlight measurable differences in end-user maturity, regulatory pressures, and production capacities across global regions.

North America represents a significant market, accounting for approximately 22% of global levulinic acid consumption in 2024. Strong demand arises from chemicals, personal care, and agriculture, with companies increasingly adopting bio-based intermediates to meet evolving compliance requirements. Sectors such as healthcare, pharmaceuticals, and advanced manufacturing are leading adopters due to growing interest in naturally derived solvents and performance-enhancing additives. Regulatory initiatives promoting reduced carbon footprints and restrictions on petroleum-based formulations continue to accelerate uptake across major states. Technological progress in feedstock valorization and biomass conversion also contributes to production efficiency. One notable regional player has expanded its biorefinery capacity to pilot levulinic-acid-based plasticizer systems tailored for high-performance coatings. Consumer behavior in the region exhibits a clear trend: enterprises in healthcare and finance display the highest adoption of green chemical inputs, reflecting strong sustainability alignment across regulated industries.

Europe accounted for nearly 27% of the global levulinic acid market in 2024, supported by mature chemical industries in Germany, the UK, and France. Driven by strict regulatory frameworks governing industrial emissions, chemical safety, and sustainable sourcing, regional manufacturers increasingly integrate levulinic-acid-based intermediates into polymers, additives, agrochemicals, and performance materials. Major European regulatory bodies have accelerated sustainability programs requiring a shift toward biodegradable and low-impact chemical inputs, encouraging rapid adoption of next-generation bio-derived products. Technology adoption in areas such as digitalized bioprocessing, waste valorization, and green solvents is expanding, improving cost-efficiency across manufacturing clusters. A leading regional player recently introduced levulinate ester formulations for specialty coatings used in industrial infrastructure upgrades. Consumer behavior trends show that European buyers favor high-transparency, environmentally compliant chemical solutions, resulting in market preference for traceable, eco-certified levulinic-acid derivatives.

Asia-Pacific holds the highest consumption volume, representing 41% of the global levulinic acid market in 2024. China, India, and Japan collectively drive demand through expanding chemical processing bases, large-scale agricultural inputs, and rising use of green solvents in consumer product manufacturing. The region benefits from robust industrial infrastructure, competitive biomass availability, and accelerated investment in integrated biorefinery technologies. Innovation hubs in China and Japan are developing new levulinate ester and ALA applications in crop enhancement, personal care, and high-performance materials. One prominent regional manufacturer announced a new production line focused on levulinic-acid-derived intermediates for advanced polymer systems. Consumer behavior trends show strong adoption influenced by e-commerce growth, mobile-driven purchasing patterns, and rising preference for natural ingredient-based products across major urban markets.

South America accounted for nearly 6% of the global levulinic acid market in 2024, with Brazil and Argentina driving most of the demand. Growth is supported by expanding agricultural activities, rising interest in bio-based agro-inputs, and gradual industrial modernization across chemicals and materials sectors. Regional manufacturing facilities are increasingly exploring biomass conversion routes due to abundant agricultural waste streams. Several governments have introduced incentive programs promoting bio-based production to diversify industrial output and reduce reliance on imported chemical intermediates. A regional producer recently initiated trials of levulinic-acid-based agricultural enhancers to optimize crop yield performance in soybean and sugarcane farming. Consumer behavior in South America indicates heightened demand for localized solutions, particularly in sectors involving language-specific digital tools and media localization, which indirectly influence chemical demand through packaging and printing industries.

The Middle East & Africa region held around 4% of global levulinic acid demand in 2024, with the UAE, Saudi Arabia, and South Africa representing the largest consumption bases. Growth is supported by industrial diversification initiatives that reduce dependency on fossil-derived chemicals, alongside expanding construction, agriculture, and manufacturing sectors. Technological modernization—including investments in bio-conversion technologies, circular chemical practices, and sustainable material testing—is reshaping local production capacity. Governments have also introduced trade partnerships encouraging the import of bio-based intermediates. A notable regional company began integrating levulinic-acid-derived solvents into industrial cleaning formulations aimed at reducing hazardous waste output. Consumer behavior trends show increasing openness to sustainable materials, especially in markets undergoing rapid industrial restructuring and green transition planning.

China – 28% Market Share: Strongest global production capacity and large-scale consumption in chemicals and agriculture.

United States – 17% Market Share: High demand from advanced manufacturing, personal care, and industrial solvent applications.

The competitive environment in the Levulinic Acid Market is moderately consolidated but increasingly competitive, featuring a core set of about 10–15 major global producers and a larger pool of smaller regional manufacturers and niche specialty-chemical firms. The top five companies together account for approximately 55–60% of total production capacity, indicating that while a few firms lead, there remains substantial room for competition and new entrants. Major players compete on technological strength, scale of biomass-to-chemical conversion processes, product purity, and supply-chain integration. Strategic initiatives observed in recent years include expansion of production capacity, backward integration to secure cellulose feedstock, and development of advanced catalytic or continuous-hydrolysis technologies to lower production cost and improve yield. Several firms have launched new levulinic-acid derivative lines targeting bio-based solvents, plasticizers, and cosmetic/pharma-grade intermediates — reflecting innovation-driven competition. The market is characterized by a dual structure: established large-scale producers dominating global supply, and numerous agile regional players focusing on niche derivatives or regional supply for agrochemicals, coatings, or flavor/fragrance use. This hybrid structure fosters both stability and dynamic competition. As demand scales and regulation pushes for greener chemistry, competitive pressure is increasing on cost, purity, sustainability credentials, and technological differentiation among producers.

Biofine International Inc.

Avantium

Simagchem Corporation

Langfang Triple Well Chemicals Co. Ltd.

Great Chemicals Co. Ltd.

The Levulinic Acid Market is undergoing a technological transformation marked by improvements in biomass conversion methods, catalytic process innovation, and continuous-processing techniques. Traditional batch acid-hydrolysis processes are increasingly being replaced by continuous hydrolysis reactors that enable higher throughput, lower downtime, and more consistent product quality. These systems allow producers to handle larger volumes of lignocellulosic feedstock such as agricultural residue, wood waste, or starch sources, improving raw-material flexibility and supply resilience.

In parallel, advanced heterogeneous catalytic processes are being developed to increase conversion efficiency and reduce by-product formation, enhancing overall yield and product purity. Such catalytic innovations lower energy consumption and simplify downstream purification, making levulinic acid more cost-effective and competitive with petrochemical alternatives. Some firms are also integrating biorefinery platforms that combine feedstock preprocessing, hydrolysis, catalytic conversion, and downstream esterification or derivative synthesis in a unified production workflow, thereby reducing logistical and operational overheads.

Another emerging trend is feedstock diversification: producers are designing systems capable of processing a broad range of biomass types — from agricultural residues and forestry waste to industrial carbohydrate by-products — which helps stabilize supply and reduce raw material cost volatility. Additionally, innovations in green-chemistry derivative synthesis such as bio-based esters, ketals, and solvents are expanding the product portfolio beyond bulk levulinic acid, targeting high-value applications in cosmetics, agrochemicals, plastics, and specialty solvent markets.

Digital transformation is also influencing production: process monitoring, yield optimization, and quality control systems enhanced by automation and data analytics enable tighter quality tolerances — critical for pharmaceutical and cosmetic-grade levulinic derivatives. Decision-makers benefit from these advances through improved cost structures, supply security, compliance with sustainability mandates, and access to value-added derivative markets. Overall, the technology trends are reshaping the Levulinic Acid Market, moving it from niche bio-chemical production toward integrated, scalable, and diversified bio-based chemical manufacturing.

In July 2023 Biofine announced a long-term offtake agreement with Sprague Operating Resources for the full output of its first commercial biorefinery in Lincoln, Maine, securing feedstock-to-product pathways and an initial commercial sales channel for levulinic-acid derived co-products. Source: www.biofinedevelopments.com

In April 2024 Hefei TNJ Chemical exhibited at the Middle East Coatings Show (Dubai, April 15–17, 2024), promoting high-purity levulinic-acid grades and specialty derivatives to coatings and industrial formulators while expanding regional commercial contacts. Source: www.tnjchem.com

On April 29, 2024 DuPont published its 2024 Sustainability Report highlighting accelerated progress on 2030 climate goals, expanded bio-materials initiatives and increased investment in renewably sourced product lines — signalling a stronger corporate push toward bio-based chemical solutions. Source: www.dupont.com

In August 2024 Avantium reported H1-2024 results and reiterated progress toward start-up of its FDCA flagship plant, underlining continued corporate investment into bio-based polymer and chemical platforms consistent with growing industrial demand for renewable building-block chemicals. Source: newsroom.avantium.com

The Levulinic Acid Market Report encompasses a comprehensive global assessment of levulinic acid production, derivative products, and downstream applications across multiple segments, geographic regions, and technology pathways. The report covers product types including levulinic acid, levulinate esters, ketals, δ-aminolevulinic acid (ALA), and specialty derivatives, examining their utilization across solvents, plasticizers, agrochemicals, pharmaceuticals, personal care, fuel additives, and industrial intermediates. Geographical coverage spans all major regions: North America, Europe, Asia-Pacific, South America, Middle East & Africa, with country-level insights for key producing and consuming markets. The report also reviews technological routes — traditional acid hydrolysis, continuous hydrolysis, heterogeneous catalysis, and integrated biorefinery conversion — along with feedstock diversification covering lignocellulosic biomass, agricultural residue, starch, and waste-derived carbohydrates.

Further, the scope includes supply-chain dynamics, competitive landscape analysis, market concentration and fragmentation patterns, strategic initiatives by major players (such as capacity expansions, backward integration, and R&D investment), regulatory and sustainability drivers, and emerging trends for green chemistry adoption. It also encompasses end-user segmentation by industry verticals (chemicals, agriculture, personal care, pharmaceuticals, industrial solvents), evaluation of derivative demand, and potential future growth pathways in high-value specialty applications. Niche focus areas — such as bio-based solvents for coatings, biodegradable plasticizer intermediates, and cosmetic-grade levulinic derivatives — are also covered. Overall, the report aims to provide decision-makers with a holistic, up-to-date view of market structure, technology evolution, supply and demand interplay, competitive positioning, and growth opportunities over the foreseeable future.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 2,970.0 Million |

| Market Revenue (2032) | USD 4,033.5 Million |

| CAGR (2025–2032) | 3.9% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | GFBiochemicals Ltd., Hefei TNJ Chemical Industry Co., Ltd., DuPont de Nemours, Inc., Biofine International Inc., Avantium, Simagchem Corporation, Langfang Triple Well Chemicals Co. Ltd., Great Chemicals Co. Ltd. |

| Customization & Pricing | Available on Request (10% Customization Free) |