Reports

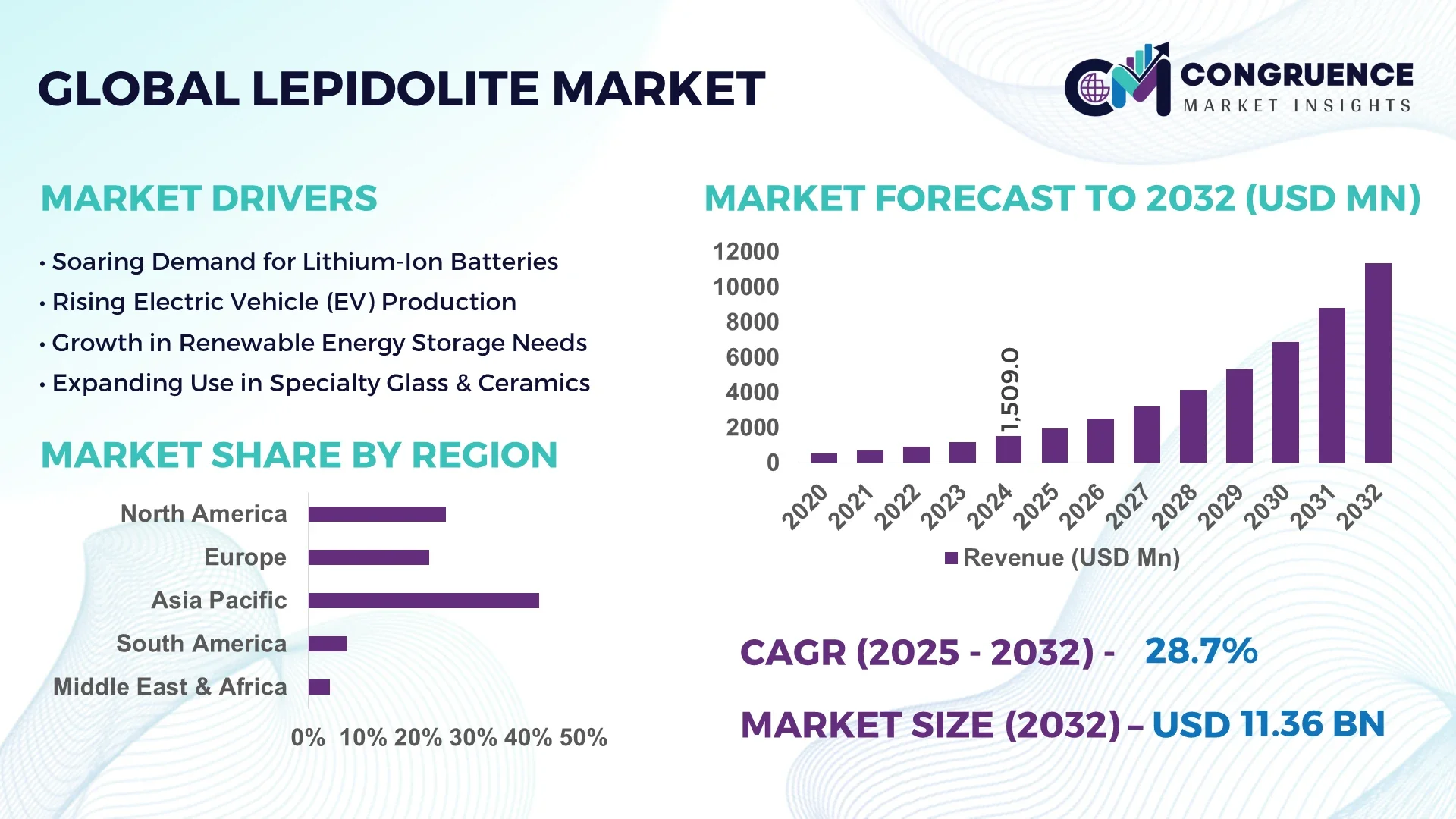

The Global Lepidolite Market was valued at USD 1,509.0 Million in 2024 and is anticipated to reach a value of USD 11,344.3 Million by 2032 expanding at a CAGR of 28.7% between 2025 and 2032.

To Learn More About This Report, Request A Free Sample Copy

China dominates the lepidolite marketplace due to its extensive lithium reserves and strong position in lithium battery manufacturing. The country's rapid growth in electric vehicle production and renewable energy initiatives significantly drives the demand for lepidolite, making it a key supplier and processor in the global market.

Lepidolite serves as a crucial source of lithium, widely used in lithium-ion batteries, ceramics, glass, and lubricants. Technological advancements in mining and processing have improved the efficiency and quality of lithium extraction from lepidolite deposits. Increasing global demand for energy storage solutions, especially in automotive and electronics sectors, underpins the market’s expansion. Sustainable mining practices and environmental regulations are influencing supply chain decisions and prompting investments in eco-friendly extraction technologies.

Artificial Intelligence (AI) is transforming the lepidolite market by enhancing exploration, extraction, and processing operations. AI-driven data analytics enables precise identification of lepidolite-rich deposits, significantly reducing exploration time and operational costs. Machine learning algorithms improve ore grade estimation and automate sorting processes, leading to higher recovery rates and reduced waste. In mining operations, AI-powered autonomous machinery boosts productivity while minimizing safety risks to human workers.

AI technologies facilitate predictive maintenance of mining equipment, helping prevent unplanned downtime and extending equipment lifespan. Additionally, AI enhances supply chain management by forecasting demand and optimizing logistics, ensuring the steady supply of lepidolite to battery manufacturers and industrial consumers. Real-time environmental monitoring driven by AI assists companies in meeting regulatory standards and minimizing ecological impacts.

These AI-driven innovations contribute to increased operational efficiency, reduced costs, and improved sustainability in the lepidolite market, positioning the industry to better meet growing global lithium demand.

“In 2024, a leading mining firm adopted an AI-based mineral detection system that improved lepidolite ore identification accuracy by 35%, accelerating extraction processes and reducing operational waste significantly.”

The rapid growth of electric vehicles and renewable energy storage systems is driving demand for lithium sourced from lepidolite. Governments globally are encouraging clean energy adoption, fueling expansion in lithium-ion battery production. This increased consumption is a primary growth factor for the lepidolite market, pushing companies to enhance extraction and processing capabilities.

Environmental concerns related to land disturbance, water consumption, and waste disposal impose restrictions on lepidolite mining. Regulatory compliance costs and stringent environmental laws limit large-scale mining projects, slowing market growth. Additionally, social opposition and community concerns in mining areas pose challenges to new developments.

Innovative extraction methods such as direct lithium extraction and hydrometallurgical techniques offer higher lithium recovery and lower environmental impact. Adoption of these technologies presents growth opportunities for the lepidolite market by improving resource utilization and reducing operational costs, encouraging investment in new and existing mining operations.

The fluctuating price of lithium impacts lepidolite mining profitability. Market uncertainties caused by changes in demand, geopolitical tensions, and production adjustments create unstable revenue prospects. This price volatility complicates investment decisions and long-term project planning for companies operating in the lepidolite sector.

Automation and Digitalization in Mining: The lepidolite market is witnessing increased adoption of automated machinery for drilling, hauling, and ore sorting. Automation reduces reliance on manual labor and improves safety by minimizing worker exposure to hazardous mining environments. This trend is more pronounced in regions with advanced mining technologies and infrastructure.

Focus on Sustainability and Environmental Compliance: Mining companies are implementing water recycling, waste reduction, and energy-efficient processes to lower the environmental impact of lepidolite extraction. These sustainability initiatives help meet stringent environmental regulations and address growing concerns from local communities and stakeholders.

Expansion of Lithium Battery Manufacturing Capacity: The growth in lithium-ion battery production, especially in Asia and Europe, is driving steady demand for lepidolite. Strategic partnerships between mining firms and battery manufacturers are strengthening supply chains and encouraging collaborative innovations in lithium sourcing and processing.

Diversification of End-Use Applications: Beyond lithium batteries, lepidolite is increasingly used in ceramics, glass, and pharmaceutical industries. This diversification expands the market potential by reducing dependence on a single sector and opening new avenues for revenue generation.

The lepidolite market is segmented based on type, application, and end-user industries to better understand demand patterns and growth opportunities. Types of lepidolite include raw ore, concentrates, and processed lithium compounds, each serving different supply chain needs. Applications span lithium-ion batteries, ceramics and glass manufacturing, lubricants, and pharmaceuticals. End-user insights focus on industries such as automotive, electronics, energy storage, and specialty chemicals. This segmentation helps identify market dynamics, with certain segments showing faster adoption due to technological advances or changing consumer preferences.

The lepidolite market is primarily divided into raw ore, concentrates, and lithium compounds. Raw ore remains the most abundant segment, accounting for a significant volume share due to its direct extraction from mining operations and broad usage in industrial applications. Concentrates are gaining momentum as they offer higher lithium content, enabling more efficient processing and reduced transportation costs. Lithium compounds, derived from lepidolite processing, represent the fastest-growing segment owing to their direct use in lithium-ion battery manufacturing and other high-value applications.

The increasing demand for lithium compounds is driven by the rapid expansion of electric vehicles and energy storage solutions, where high-purity lithium chemicals are critical. This shift towards processed forms of lepidolite enhances supply chain efficiency and aligns with growing industry standards for battery-grade lithium. While raw ore continues to dominate in volume, lithium compounds lead in value growth due to their specialized applications and premium pricing.

Applications of lepidolite are diverse, with lithium-ion batteries being the leading segment due to the surge in electric vehicle production and portable electronics. This segment commands the largest market share, driven by technological advancements and global policies promoting clean energy. The ceramics and glass segment remains substantial, using lepidolite to improve product durability and thermal properties. Lubricants and pharmaceuticals are niche applications but show steady growth fueled by specialized industrial needs.

Lithium-ion batteries are also the fastest-growing application, reflecting the global shift towards electrification and renewable energy storage. Innovations in battery chemistries and increasing battery capacity demand high-quality lithium sources, which boosts lepidolite usage. Meanwhile, traditional applications like ceramics maintain steady demand, supported by construction and consumer goods industries. This diversified application base ensures resilience in market growth, balancing emerging technologies with established industrial uses.

The automotive sector is the dominant end-user of lepidolite, primarily due to its pivotal role in electric vehicle battery production. This segment accounts for the largest market share as automakers ramp up EV manufacturing to meet climate goals and consumer demand. The energy storage sector is the fastest-growing end-user segment, driven by the need for grid-scale battery installations and renewable energy integration.

Electronics manufacturers also contribute significantly, utilizing lepidolite-derived lithium for portable devices and consumer electronics batteries. Specialty chemical industries, using lepidolite in lubricants and pharmaceuticals, represent a smaller yet consistent portion of the market. The automotive segment’s dominance is attributed to large-scale investments and government incentives, while the energy storage sector’s rapid growth reflects the ongoing transition to cleaner energy infrastructure worldwide.

Asia-Pacific accounted for the largest market share at 42% in 2024; however, South America is expected to register the fastest growth, expanding at a CAGR of 30.1% between 2025 and 2032.

To Learn More About This Report, Request A Free Sample Copy

Asia-Pacific's dominance is driven by major lithium reserves in countries like China and Australia, coupled with rapid electric vehicle adoption and battery manufacturing capacities. South America's growth is fueled by increasing exploration activities and investments in lithium mining projects, particularly in countries such as Brazil and Argentina. North America and Europe also hold significant shares, supported by government incentives and expanding renewable energy infrastructure.

Expanding Electric Vehicle and Energy Storage Demand

North America’s lepidolite market is growing steadily with rising electric vehicle production in the U.S. and Canada. Increased investments in battery manufacturing facilities have driven demand for high-purity lithium compounds derived from lepidolite. Additionally, the growing focus on renewable energy storage systems across the region supports steady lepidolite consumption. Though smaller in reserve size compared to Asia-Pacific, North America benefits from advanced mining technologies and regulatory support for sustainable lithium sourcing, contributing to a balanced regional market presence.

Growth in Green Energy and Battery Manufacturing Hubs

Europe is emerging as a significant player in the lepidolite market due to its strong focus on decarbonization and green energy initiatives. Countries like Germany and France are expanding lithium-ion battery production to meet automotive and industrial electrification goals. The region’s demand for sustainable lithium sources has increased interest in lepidolite mining and processing. Additionally, Europe’s rigorous environmental standards are driving investments in eco-friendly extraction technologies, supporting long-term growth in the market.

Dominance in Lithium Mining and Battery Production

Asia-Pacific leads the global lepidolite market with China, Australia, and India playing pivotal roles. China’s large lithium reserves and massive battery manufacturing industry drive continuous demand for lepidolite. Australia’s significant mining operations contribute raw materials essential for global lithium supply chains. Additionally, emerging economies like India are investing in lithium extraction and battery manufacturing capacities, further boosting regional demand. The region’s infrastructure developments and government policies favor rapid market expansion.

Emerging Lithium Mining Frontier

South America is rapidly gaining prominence in the lepidolite market, primarily due to abundant lithium deposits in countries like Brazil and Argentina. Increased exploration activities and foreign investments in lithium mining projects are accelerating regional growth. South America’s favorable geological conditions and expanding industrial base are attracting key market players. This growth is supported by the rising global demand for lithium and ongoing efforts to develop sustainable mining practices, positioning the region as a future growth hotspot.

Developing Market with Growing Exploration Activities

The Middle East & Africa region is witnessing early-stage growth in the lepidolite market with exploration activities increasing in countries such as Zimbabwe and Namibia. Though currently smaller in market share compared to other regions, ongoing investments in mining infrastructure and strategic partnerships aim to unlock lithium resources. The region’s potential for supplying raw materials for battery manufacturing is gradually attracting attention, complemented by emerging renewable energy projects and industrial diversification efforts.

Top Two Countries by Market Share in 2024

China: USD 635 Million — Leading due to vast lithium reserves and dominance in battery manufacturing.

Australia: USD 420 Million — Significant mining operations and raw material exports fueling global lithium supply.

The lepidolite market features a competitive landscape dominated by a mix of mining corporations, chemical producers, and specialized lithium processing companies. Key players focus on expanding their lithium extraction capacities and securing supply contracts with battery manufacturers and automotive companies. Strategic collaborations, joint ventures, and mergers are common as companies seek to strengthen their positions in the rapidly growing lithium market. Investment in sustainable mining technologies and downstream processing facilities is a priority to meet rising environmental standards and customer demand for high-purity lithium products. Companies are also diversifying product portfolios to include lithium hydroxide, lithium carbonate, and other value-added compounds derived from lepidolite. Geographic expansion into emerging lithium-rich regions is another key tactic, allowing companies to reduce dependency on single sources and mitigate supply risks. Overall, innovation, resource control, and vertical integration characterize the competitive dynamics of the lepidolite market.

Albemarle Corporation

Tianqi Lithium Corporation

Sociedad Química y Minera de Chile (SQM)

Livent Corporation

Ganfeng Lithium Co., Ltd.

Lithium Americas Corporation

Pilbara Minerals Ltd.

Orocobre Limited

Nemaska Lithium Inc.

Galaxy Resources Limited

Technological advancements are pivotal in enhancing lepidolite extraction, processing, and refinement. Modern mining operations are increasingly employing automated drilling and sorting systems powered by AI and machine learning to improve ore grade detection and reduce waste. Hydrometallurgical techniques, such as direct lithium extraction (DLE), are gaining traction as they enable higher lithium recovery from lepidolite with lower environmental impact compared to traditional roasting and leaching methods. Additionally, advancements in solvent extraction and ion-exchange resins facilitate the efficient separation of lithium from other minerals in lepidolite concentrates. Continuous improvements in battery-grade lithium compound production enhance purity levels, supporting the quality requirements of advanced lithium-ion batteries. Digital twin technology is being adopted for real-time monitoring and predictive maintenance of mining equipment, optimizing operations and reducing downtime. These technological developments drive cost efficiencies, environmental compliance, and product quality improvements, positioning the lepidolite market for robust growth aligned with rising lithium demand.

In November 2023, Livent Corporation announced the expansion of its lithium extraction facility in Argentina, increasing its production capacity by 20% to meet growing demand from electric vehicle manufacturers.

In March 2024, Tianqi Lithium Corporation partnered with a European battery manufacturer to supply high-purity lithium hydroxide derived from lepidolite, strengthening supply chain resilience for EV production.

In July 2023, Albemarle Corporation deployed AI-based mineral exploration technology at its lithium mines in Australia, enhancing ore detection accuracy and reducing exploration costs significantly.

In January 2024, Lithium Americas Corporation commenced construction of a new processing plant in Nevada, USA, focused on refining lithium compounds from lepidolite concentrates using advanced hydrometallurgical methods.

The scope of the lepidolite market report encompasses a comprehensive analysis of the global market landscape, covering market size, segmentation, trends, and competitive dynamics. It provides detailed insights into type-based segments including raw ore, concentrates, and lithium compounds, highlighting their market shares and growth drivers. The report examines applications ranging from lithium-ion batteries and ceramics to lubricants and pharmaceuticals, assessing demand patterns across industries. End-user analysis focuses on automotive, energy storage, electronics, and specialty chemicals sectors. Regional market insights include detailed coverage of key geographies such as Asia-Pacific, North America, Europe, South America, and Middle East & Africa. Additionally, the report explores technological advancements, regulatory impacts, and sustainability initiatives shaping market growth. Key company profiles and recent developments offer a strategic view of competitive positioning. Overall, the report serves as a vital resource for stakeholders aiming to understand market opportunities and challenges in the evolving lepidolite industry.

| Report Attribute / Metric | Report Details |

|---|---|

| Market Name | Global Lepidolite Market |

| Market Revenue (2024) | USD 1,509.0 Million |

| Market Revenue (2032) | USD 11,344.3 Million |

| CAGR (2025–2032) | 28.7% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Report Deliverables | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape, Technological Insights, Recent Developments |

| Regions Covered | Asia-Pacific, North America, Europe, South America, Middle East & Africa |

| Key Players Analyzed | Albemarle Corporation, Tianqi Lithium Corporation, Sociedad Química y Minera de Chile (SQM), Livent Corporation, Ganfeng Lithium Co., Ltd., Lithium Americas Corporation, Pilbara Minerals Ltd., Orocobre Limited, Nemaska Lithium Inc., Galaxy Resources Limited |

| Customization & Pricing | Available on Request (10% Customization is Free) |