Reports

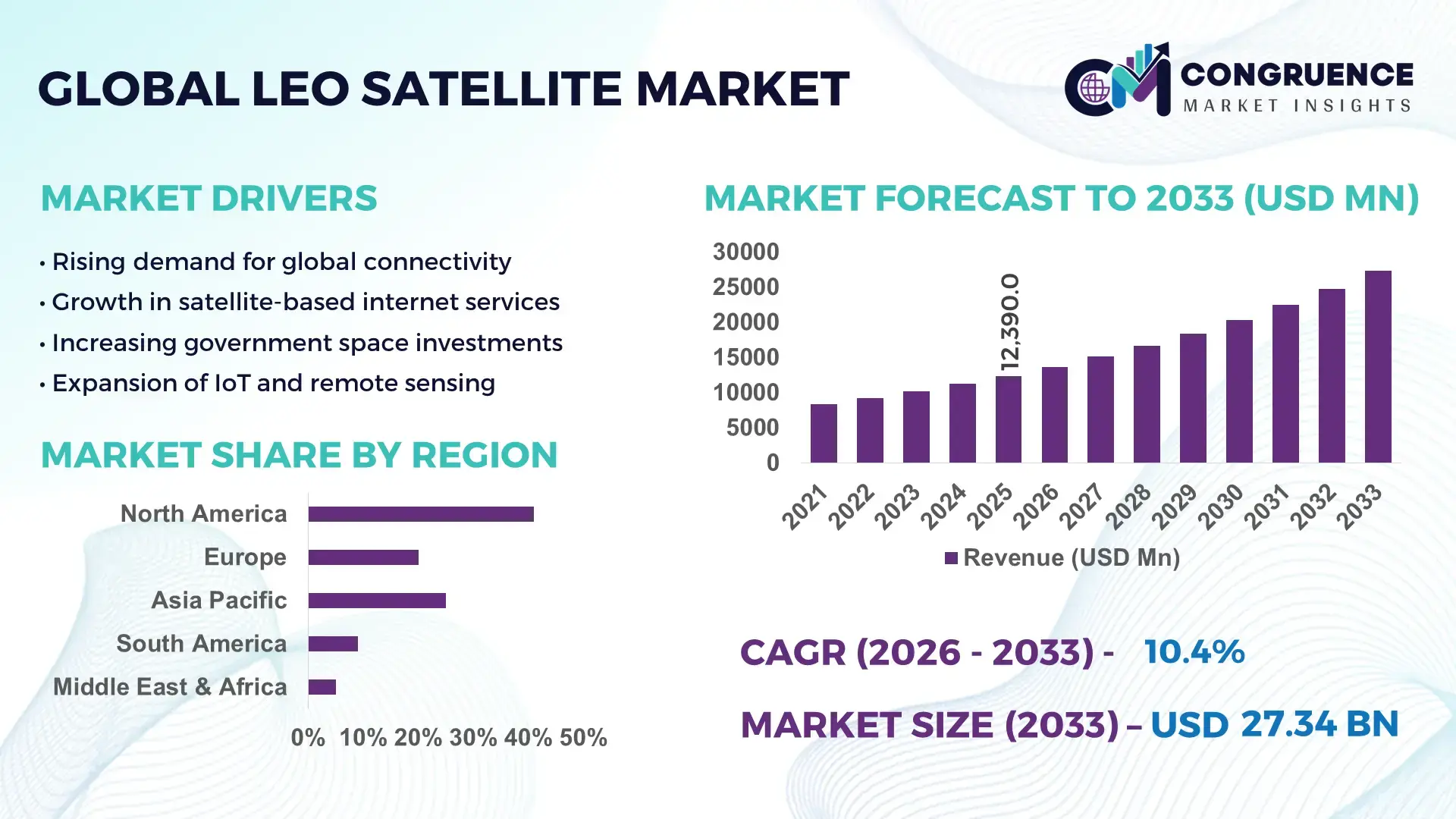

The Global Leo Satellite Market was valued at USD 12390 Million in 2025 and is anticipated to reach a value of USD 27341.59 Million by 2033 expanding at a CAGR of 10.4% between 2026 and 2033. This growth is primarily driven by increasing demand for high-speed, low-latency communication networks across commercial and defense sectors.

The United States continues to play a pivotal role in shaping the global LEO satellite market, supported by strong industrial infrastructure, advanced aerospace manufacturing capabilities, and substantial private-sector investment. The country has launched over 4,500 active LEO satellites as of 2025, accounting for a significant portion of global satellite deployments. Leading aerospace firms and satellite operators are investing heavily in mega-constellation projects, with investments exceeding USD 20 billion in recent years. Key applications include broadband internet coverage, military surveillance, Earth observation, and IoT connectivity. Additionally, the U.S. is advancing satellite miniaturization technologies, with nanosatellite launches increasing by over 30% annually, reinforcing its technological leadership in reusable launch systems and satellite communication innovation.

Market Size & Growth: USD 12390 Million in 2025 projected to reach USD 27341.59 Million by 2033, expanding at 10.4% CAGR, driven by demand for low-latency global connectivity.

Top Growth Drivers: Satellite broadband adoption increased by 38%, launch cost efficiency improved by 45%, and IoT satellite integration rose by 33%.

Short-Term Forecast: By 2028, network latency is expected to reduce by 25% through advanced LEO constellation optimization.

Emerging Technologies: AI-powered satellite traffic management, phased array antennas, and inter-satellite laser communication systems.

Regional Leaders: North America projected at USD 11,000 Million by 2033 with defense integration; Asia-Pacific at USD 8,500 Million driven by telecom expansion; Europe at USD 6,200 Million with strong regulatory frameworks.

Consumer/End-User Trends: Telecommunications and defense sectors account for over 60% of deployments, with growing enterprise adoption in remote connectivity.

Pilot or Case Example: In 2024, a satellite constellation pilot improved rural internet speeds by 40% and reduced downtime by 22%.

Competitive Landscape: Market leader holds approximately 42% share, followed by key players focusing on constellation scalability and launch innovation.

Regulatory & ESG Impact: Governments enforcing space debris mitigation policies targeting 30% reduction by 2030.

Investment & Funding Patterns: Over USD 25 billion invested globally in satellite constellations and launch infrastructure.

Innovation & Future Outlook: Integration of AI and edge computing in satellite networks is expected to redefine global communication infrastructure.

The LEO satellite market is supported by diverse industry sectors including telecommunications, defense, agriculture, maritime, and logistics, with telecom contributing nearly 45% of total deployments. Technological advancements such as reusable rockets, compact satellite designs, and onboard data processing systems are accelerating deployment efficiency. Regulatory frameworks focusing on orbital debris management and spectrum allocation are shaping operational strategies. Asia-Pacific is witnessing rapid consumption growth due to increasing rural connectivity initiatives, while Europe emphasizes sustainable satellite operations. Emerging trends such as satellite-enabled IoT ecosystems, real-time Earth observation analytics, and hybrid satellite-terrestrial networks are expected to further enhance market penetration and long-term scalability.

The strategic relevance of the Leo Satellite Market is deeply tied to its ability to deliver high-speed, low-latency connectivity across underserved and remote regions, enabling digital transformation across industries. Advanced satellite communication technologies, including inter-satellite laser links, deliver nearly 50% improvement in data transmission speed compared to traditional geostationary satellite systems. This technological shift is reshaping global telecommunications infrastructure, particularly in areas where terrestrial networks remain economically unviable.

North America dominates in deployment volume due to large-scale constellation launches, while Asia-Pacific leads in adoption with over 35% of enterprises integrating satellite-based connectivity solutions into their operations. This contrast highlights a strong regional diversification in market maturity and application focus. By 2028, AI-driven network optimization is expected to reduce signal latency and bandwidth congestion by approximately 30%, significantly improving service reliability for both commercial and defense applications. From an ESG perspective, companies are committing to sustainable space operations, including a targeted 25% reduction in orbital debris through improved satellite deorbiting technologies by 2030. Regulatory bodies are also enforcing stricter compliance standards for satellite lifecycle management and spectrum usage.

A notable micro-scenario emerged in 2024, where a leading satellite operator achieved a 28% improvement in network efficiency through AI-based traffic routing and predictive maintenance systems. Such measurable outcomes demonstrate the practical impact of technological integration in the sector. The Leo Satellite Market is increasingly positioned as a critical enabler of resilient communication ecosystems, regulatory compliance, and sustainable digital infrastructure, reinforcing its role as a cornerstone of future global connectivity strategies.

The increasing need for high-speed internet connectivity in remote and underserved regions is a major driver of the Leo Satellite Market. Approximately 2.6 billion people globally still lack reliable internet access, creating a substantial demand for satellite-based broadband solutions. LEO satellites provide latency as low as 20–40 milliseconds, significantly outperforming traditional satellite systems, which often exceed 600 milliseconds. This performance advantage enables seamless video streaming, real-time communication, and cloud-based applications in rural and geographically isolated areas. Telecommunication companies are rapidly integrating LEO satellite networks into their service offerings, with over 35% of global telecom operators exploring satellite partnerships to expand coverage. Additionally, governments are investing in satellite infrastructure to support digital inclusion initiatives, particularly in developing economies. The expansion of 5G networks is also complementing LEO satellite deployment, creating hybrid connectivity models that enhance network reliability and coverage.

Despite significant technological advancements, the Leo Satellite Market faces considerable financial challenges associated with satellite deployment and maintenance. Launching a single satellite can cost between USD 500,000 to USD 1 million depending on size and payload, while maintaining large constellations requires continuous investment in ground infrastructure and operational management. Additionally, satellite lifespans in low Earth orbit typically range from 5 to 7 years, necessitating frequent replacements and increasing long-term costs. Space debris management is another critical concern, with over 36,000 tracked debris objects posing collision risks that can lead to costly damage or mission failures. Insurance premiums for satellite launches have also risen by nearly 20% in recent years due to increased risk exposure. These financial and operational constraints limit market entry for smaller players and create dependency on large-scale funding and government support.

The rapid growth of IoT and smart infrastructure presents significant opportunities for the Leo Satellite Market. With an estimated 30 billion connected devices expected globally by 2030, there is a growing need for reliable, wide-area connectivity that terrestrial networks alone cannot provide. LEO satellites offer seamless coverage for remote industrial operations, including oil and gas monitoring, precision agriculture, and maritime logistics. Satellite-enabled IoT solutions are increasingly being adopted in sectors such as agriculture, where they improve crop monitoring efficiency by up to 35% through real-time data analytics. Smart city initiatives are also leveraging satellite connectivity for traffic management, environmental monitoring, and disaster response systems. Furthermore, advancements in edge computing integration with satellite networks are enabling faster data processing and reduced latency, creating new business models and revenue streams for service providers.

Regulatory complexities and spectrum allocation challenges represent significant obstacles for the Leo Satellite Market. The increasing number of satellite launches has intensified competition for limited radio frequency spectrum, leading to potential interference issues and operational inefficiencies. International coordination is required to manage spectrum allocation, but differing regulatory frameworks across countries often create delays and compliance challenges. Additionally, licensing procedures for satellite operations can take several years, slowing down deployment timelines and increasing project costs. Governments are also implementing stricter regulations related to space debris mitigation and satellite deorbiting, requiring operators to invest in additional technologies and compliance mechanisms. These regulatory hurdles not only impact operational efficiency but also create uncertainty for investors and stakeholders, potentially limiting the pace of market expansion.

• Rapid Expansion of Mega-Constellations with Over 60% Deployment Growth: The Leo Satellite market is witnessing a substantial increase in large-scale constellation deployments, with active satellite counts exceeding 7,500 units globally in 2025, reflecting a 60% rise over the past three years. Operators are focusing on deploying satellites in batches of 50–60 per launch to optimize cost efficiency and orbital coverage. This trend is significantly improving global internet penetration, particularly in remote areas where connectivity gaps previously exceeded 45%. The increased launch frequency, now averaging over 180 launches annually, is further accelerating constellation expansion and enhancing service availability.

• Adoption of Inter-Satellite Laser Communication Improving Data Speeds by 50%: A notable technological trend in the Leo Satellite market is the integration of optical inter-satellite links, which enhance data transmission speeds by approximately 50% compared to traditional radio frequency systems. Over 35% of newly launched satellites are now equipped with laser communication systems, enabling real-time data relay across constellations without ground station dependency. This advancement reduces latency to below 30 milliseconds and improves network resilience, particularly for mission-critical applications such as defense communications and autonomous systems.

• Growth in Satellite-Enabled IoT Connectivity with 40% Device Integration Increase: The integration of IoT devices with LEO satellite networks has grown by over 40% in the last two years, driven by demand from industries such as agriculture, maritime, and energy. More than 15 million IoT endpoints are now connected via satellite systems, enabling real-time monitoring and predictive analytics. Precision agriculture applications alone have seen efficiency improvements of up to 32% through satellite-based data insights. This trend is expanding the market beyond traditional communication use cases into industrial automation and smart infrastructure.

• Rising Focus on Space Sustainability with 30% Debris Reduction Targets: Sustainability has become a key focus area, with over 70% of satellite operators implementing debris mitigation strategies aimed at reducing orbital waste by at least 30% by 2030. Advanced propulsion systems and automated deorbiting technologies are being integrated into over 45% of newly launched satellites. Additionally, regulatory bodies are enforcing stricter compliance requirements, leading to a 25% increase in investment toward sustainable satellite design. This trend is reshaping operational practices and driving innovation in eco-friendly space technologies.

The Leo Satellite market segmentation is structured across satellite types, diverse application areas, and a broad spectrum of end-users, reflecting the complexity and scalability of modern satellite ecosystems. By type, the market is categorized into small satellites, medium satellites, and large satellites, with small satellites accounting for the majority of deployments due to their cost efficiency and scalability. In terms of applications, satellite broadband and communication services dominate, followed by Earth observation, navigation, and IoT connectivity, collectively supporting over 65% of global use cases. End-user segmentation highlights telecommunications, defense, and government agencies as primary adopters, while sectors such as agriculture, maritime, and logistics are rapidly increasing their adoption rates. The segmentation landscape is evolving with technological advancements, enabling more specialized and industry-specific satellite solutions.

Small satellites, including nanosatellites and microsatellites, dominate the Leo Satellite market with approximately 68% of total deployments, driven by their low manufacturing costs, faster production cycles, and compatibility with rideshare launch services. These satellites typically weigh less than 500 kg and are widely used in large constellations for communication and Earth observation. Medium satellites account for around 22% of deployments, offering a balance between payload capacity and operational flexibility, making them suitable for advanced imaging and scientific missions. Large satellites represent the remaining 10%, primarily used in specialized defense and high-capacity communication applications.

While small satellites lead in adoption, medium satellites are emerging as the fastest-growing segment with an estimated growth rate of 12.8%, supported by increasing demand for enhanced payload capabilities and longer operational lifespans. The ability to integrate advanced sensors and onboard processing systems is driving their adoption in complex missions. Other satellite types, including hybrid and experimental platforms, collectively contribute to nearly 10% of the market, focusing on niche applications such as deep-space research and technology validation.

Satellite broadband and communication services lead the Leo Satellite market, accounting for approximately 52% of total applications due to the increasing demand for high-speed, low-latency internet connectivity. Earth observation follows with a 21% share, driven by the need for real-time environmental monitoring, disaster management, and geospatial intelligence. Navigation and positioning services contribute around 14%, supporting aviation, maritime, and autonomous vehicle operations.

While communication remains dominant, IoT connectivity is the fastest-growing application segment, expanding at a rate of 13.5%, fueled by the proliferation of connected devices and the need for global coverage. The integration of satellite networks with IoT platforms is enabling seamless data exchange across remote industrial operations. Other applications, including scientific research and weather forecasting, collectively account for approximately 13% of the market, providing critical insights for climate studies and space exploration.

The telecommunications sector is the leading end-user in the Leo Satellite market, accounting for nearly 48% of total adoption, driven by the need to expand broadband coverage and support next-generation communication networks. Defense and government agencies follow with a combined share of approximately 32%, leveraging LEO satellites for surveillance, reconnaissance, and secure communication systems. Commercial enterprises, including logistics, agriculture, and energy companies, represent around 20% of the market, increasingly adopting satellite solutions for operational efficiency.

Among these, commercial enterprises are the fastest-growing end-user segment, with an estimated growth rate of 14.2%, supported by the expansion of IoT applications and smart infrastructure projects. The adoption of satellite-enabled analytics is helping businesses optimize supply chains, reduce operational downtime, and improve decision-making processes. Other end-users, such as research institutions and environmental agencies, contribute to the remaining share, focusing on data-driven insights and scientific exploration.

Region North America accounted for the largest market share at 41% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 12.6% between 2026 and 2033.

North America leads with over 3,500 active LEO satellites in orbit, supported by strong private-sector investments exceeding USD 18 billion and advanced launch infrastructure. Europe holds approximately 24% of the global market, driven by sustainability-focused satellite programs and over 1,200 operational satellites. Asia-Pacific, with more than 1,800 satellites planned or deployed, is witnessing rapid expansion due to increasing digital connectivity demand across China, India, and Japan. South America contributes around 6% share, with over 150 satellites supporting remote connectivity and environmental monitoring. The Middle East & Africa region holds nearly 5%, with growing investments in satellite communication for oil, mining, and rural broadband. Regional disparities in infrastructure, regulatory frameworks, and enterprise adoption are shaping distinct growth trajectories across global markets.

How are advanced connectivity demands accelerating next-generation satellite deployment?

North America holds approximately 41% of the Leo Satellite market, driven by high deployment volumes and advanced aerospace capabilities. The region’s demand is largely fueled by telecommunications, defense, and enterprise connectivity sectors, which collectively account for over 65% of satellite utilization. Strong government backing, including over 25% increase in space-related budgets, supports satellite launches and research initiatives. Regulatory frameworks are well-established, enabling faster spectrum allocation and streamlined licensing processes. Technological advancements such as reusable launch vehicles and AI-powered satellite operations are widely adopted, with over 55% of operators integrating automation into satellite management systems. A key regional player has deployed more than 4,000 satellites as part of a large-scale constellation, improving broadband coverage and reducing latency below 25 milliseconds. Consumer behavior in this region reflects high enterprise adoption, particularly in healthcare and financial services, where over 45% of organizations rely on satellite-enabled connectivity for secure and uninterrupted operations.

What regulatory and sustainability initiatives are shaping satellite innovation trends?

Europe accounts for approximately 24% of the Leo Satellite market, supported by strong institutional frameworks and collaborative space programs across Germany, the UK, and France. The region emphasizes sustainability, with over 60% of satellite operators adopting eco-friendly designs and debris mitigation technologies. Regulatory bodies have introduced strict compliance measures, resulting in a 30% increase in investments toward sustainable satellite manufacturing and operations. Emerging technologies such as inter-satellite communication and advanced Earth observation systems are widely implemented, enhancing data accuracy by nearly 35%. A prominent regional operator is focusing on deploying multi-orbit satellite systems to improve connectivity resilience and coverage. Additionally, Europe’s satellite initiatives are closely aligned with environmental monitoring and climate tracking applications. Consumer behavior shows a strong preference for transparent and regulation-compliant solutions, with over 50% of enterprises prioritizing data security and sustainability in satellite service adoption.

How is rapid digital expansion driving satellite-based connectivity transformation?

Asia-Pacific ranks among the fastest-growing regions in the Leo Satellite market, with over 1,800 satellites either deployed or in development. China, India, and Japan are the leading contributors, collectively accounting for more than 70% of regional satellite activity. The region is witnessing large-scale infrastructure investments, including over 40% increase in satellite manufacturing capabilities and launch facilities. Technological innovation is concentrated in key hubs, with advancements in miniaturized satellites and cost-efficient launch systems reducing production costs by nearly 30%. A major regional operator has initiated a constellation project targeting over 1,000 satellites to enhance rural connectivity and IoT integration. Consumer adoption patterns highlight strong demand from e-commerce, mobile applications, and smart city projects, with over 55% of digital services relying on satellite-enabled networks for seamless operations across geographically diverse areas.

What role does connectivity expansion play in strengthening regional infrastructure?

South America represents approximately 6% of the global Leo Satellite market, with Brazil and Argentina leading regional adoption. The market is driven by increasing demand for connectivity in remote areas, particularly across the Amazon region, where over 40% of the population lacks reliable internet access. Satellite solutions are playing a critical role in bridging this gap, supporting education, healthcare, and environmental monitoring initiatives. Infrastructure development is closely linked to energy and agriculture sectors, with over 35% of satellite applications focused on resource management and monitoring. Governments are introducing incentives such as tax benefits and public-private partnerships to encourage satellite deployment. A regional operator has expanded satellite coverage to over 200 remote communities, improving connectivity access by nearly 30%. Consumer behavior indicates strong reliance on satellite services for media broadcasting and localized communication, particularly in rural and semi-urban areas.

How are modernization initiatives influencing satellite adoption across emerging economies?

The Middle East & Africa region accounts for nearly 5% of the Leo Satellite market, with increasing demand from oil & gas, mining, and infrastructure sectors. Countries such as the UAE and South Africa are leading regional growth, supported by investments in digital transformation and smart infrastructure projects. Over 45% of satellite usage in this region is linked to industrial applications requiring real-time data transmission. Technological modernization is evident through the adoption of advanced communication systems and satellite-enabled monitoring solutions, improving operational efficiency by up to 28%. Governments are establishing regulatory frameworks and international partnerships to support satellite deployment and spectrum management. A regional satellite initiative has successfully enhanced connectivity across over 100 remote industrial sites, reducing operational downtime by 22%. Consumer behavior reflects growing dependence on satellite-based internet services, particularly in areas with limited terrestrial network infrastructure.

United States Leo Satellite Market – 39% share, driven by large-scale satellite constellation deployments and strong private-sector investment.

China Leo Satellite Market – 21% share, supported by rapid satellite manufacturing expansion and government-backed space programs.

The Leo Satellite market is moderately consolidated, with over 70 active competitors operating across satellite manufacturing, launch services, and communication networks. The top five companies collectively account for approximately 58% of the global market share, indicating a competitive yet concentrated landscape. Leading players are heavily investing in mega-constellation projects, with individual companies deploying thousands of satellites to establish global coverage networks.

Strategic initiatives such as partnerships between satellite operators and telecommunications providers have increased by over 35% in the past three years, enabling integrated connectivity solutions. Mergers and acquisitions are also shaping the market, with more than 15 major deals recorded since 2023 aimed at expanding technological capabilities and geographic reach. Product innovation remains a key competitive factor, with over 40% of companies focusing on AI-driven satellite operations and advanced propulsion systems.

The market is characterized by high entry barriers due to capital-intensive infrastructure and regulatory requirements, yet innovation in reusable launch technologies is reducing costs by up to 45%, encouraging new entrants. Companies are also prioritizing sustainability, with over 60% integrating debris mitigation technologies into their satellite designs. This evolving competitive landscape reflects a balance between established leaders and emerging players, all striving to enhance efficiency, scalability, and global connectivity.

SpaceX

OneWeb

Amazon Kuiper

Telesat

Iridium Communications

Globalstar

Thales Alenia Space

Airbus Defence and Space

Lockheed Martin

Northrop Grumman

Planet Labs

Spire Global

The Leo Satellite market is undergoing rapid transformation driven by advanced technologies that enhance performance, reduce operational costs, and expand application capabilities. One of the most significant developments is the adoption of inter-satellite laser communication systems, now integrated into over 35% of newly deployed satellites. These systems enable data transfer speeds exceeding 10 Gbps and reduce reliance on ground stations, lowering latency to below 30 milliseconds. This advancement is particularly critical for real-time applications such as autonomous navigation and defense communications.

Miniaturization technologies are also reshaping the market, with satellites weighing under 500 kg accounting for nearly 68% of total deployments. Innovations in microelectronics and compact payload systems have reduced manufacturing time by up to 40%, allowing operators to scale constellations rapidly. Additionally, reusable launch vehicle technology has reduced launch costs by approximately 45%, enabling more frequent and cost-efficient satellite deployments.

Artificial intelligence and machine learning are increasingly embedded in satellite operations, with over 50% of operators utilizing AI for predictive maintenance, traffic routing, and anomaly detection. These technologies improve network efficiency by up to 30% and reduce operational downtime. Edge computing capabilities are also being integrated into satellites, enabling onboard data processing and reducing the need for data transmission to ground stations by nearly 25%.

Emerging propulsion technologies, including electric and hybrid propulsion systems, are being adopted in over 45% of new satellites, enhancing maneuverability and extending operational lifespan. Additionally, advancements in phased array antennas are improving signal strength and coverage, supporting high-capacity data transmission across global networks. These technological innovations collectively position the Leo Satellite market as a critical enabler of next-generation communication and data infrastructure.

• In January 2025, SpaceX successfully launched 23 Starlink satellites aboard a Falcon 9 rocket, including 13 equipped with direct-to-cell capabilities. This advancement enables satellite-to-smartphone connectivity, expanding mobile coverage to remote regions and enhancing global communication infrastructure. Source: www.spacex.com

• In September 2024, Eutelsat OneWeb completed the integration of its LEO satellite constellation, reaching over 630 satellites in orbit. This milestone enabled global broadband coverage, supporting enterprise and government connectivity solutions across more than 50 countries. Source: www.eutelsat.com

• In October 2024, Amazon’s Project Kuiper launched its first batch of operational prototype satellites, marking a key step toward deploying a planned constellation of over 3,200 satellites. The project aims to deliver low-latency internet services to underserved and rural communities worldwide. Source: www.aboutamazon.com

• In March 2025, Iridium Communications announced enhancements to its Iridium NEXT constellation, introducing improved data throughput capabilities and expanded IoT service coverage. The upgrade supports over 2 million connected devices, strengthening its position in satellite-based IoT connectivity. Source: www.iridium.com

The Leo Satellite Market Report provides a comprehensive analysis of the global satellite ecosystem, covering a wide range of segments, technologies, and industry applications. The report evaluates over 7,500 active satellites in low Earth orbit and examines deployment trends across small, medium, and large satellite categories, with small satellites representing nearly 68% of total units. It includes a detailed assessment of applications such as satellite broadband, Earth observation, navigation, and IoT connectivity, which collectively account for over 80% of market utilization. Geographically, the report spans five major regions—North America, Europe, Asia-Pacific, South America, and the Middle East & Africa—analyzing regional deployment volumes, infrastructure investments, and adoption patterns. North America leads with over 3,500 satellites, while Asia-Pacific is rapidly expanding with more than 1,800 planned or operational units. The report also explores emerging regional markets where satellite connectivity is addressing gaps in terrestrial infrastructure.

Technological coverage includes advancements in AI-driven satellite operations, inter-satellite communication, propulsion systems, and reusable launch vehicles, with over 50% of operators integrating automation and intelligent systems. The scope further extends to regulatory frameworks, including spectrum allocation and space debris mitigation policies, impacting over 70% of satellite operators globally. Additionally, the report examines key end-user industries such as telecommunications, defense, agriculture, and logistics, highlighting adoption rates exceeding 60% in telecom alone. It also addresses niche segments such as satellite-enabled IoT ecosystems and real-time analytics platforms, offering a forward-looking perspective on innovation, scalability, and global connectivity infrastructure.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

10.4% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

SpaceX, OneWeb, Amazon Kuiper, Telesat, Iridium Communications, Globalstar, Thales Alenia Space, Airbus Defence and Space, Lockheed Martin, Northrop Grumman, Planet Labs, Spire Global |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |