Reports

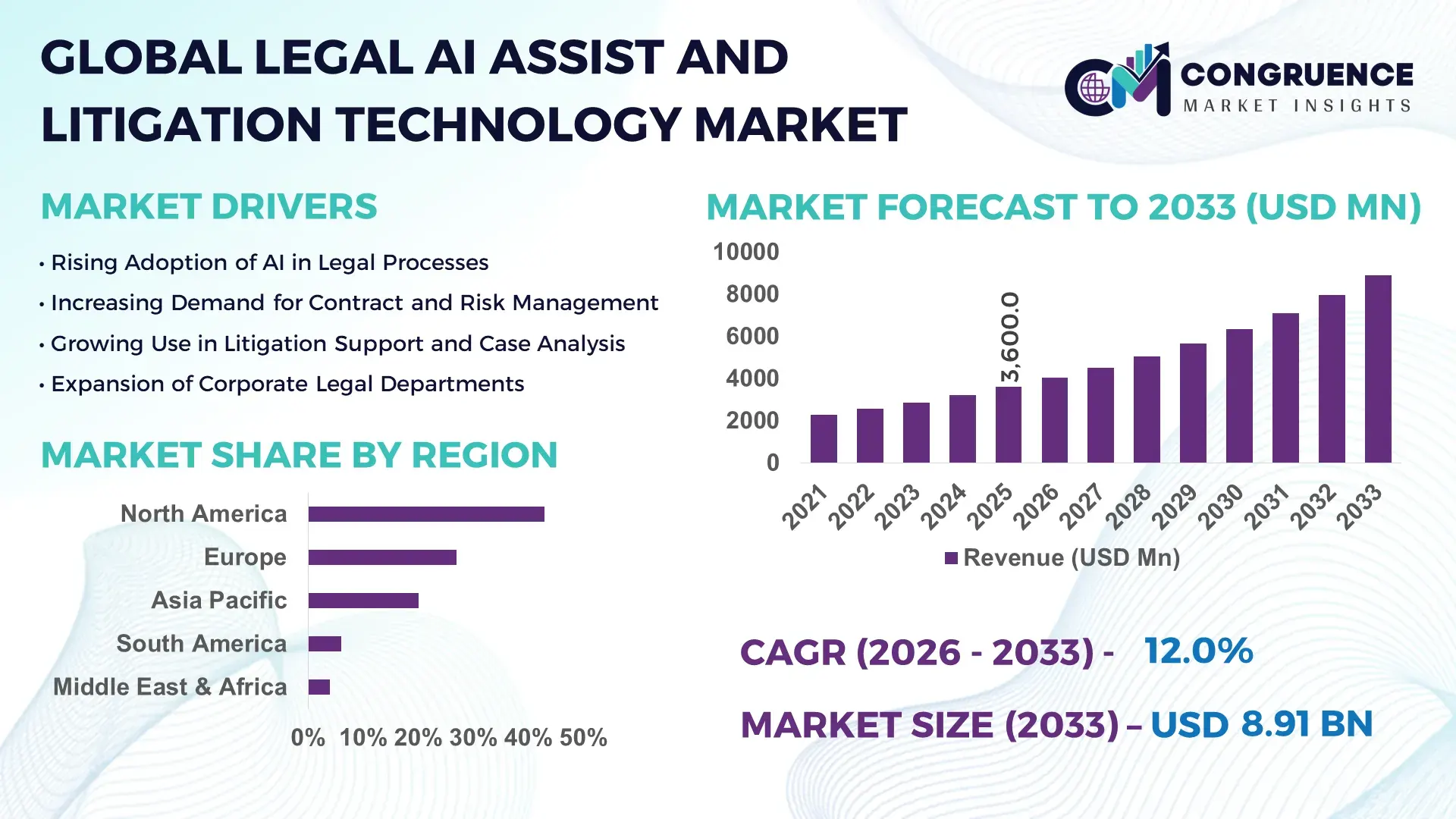

The Global Legal AI Assist and Litigation Technology Market was valued at USD 3,600.0 Million in 2025 and is anticipated to reach a value of USD 8,913.5 Million by 2033 expanding at a CAGR of 12% between 2026 and 2033, according to an analysis by Congruence Market Insights. The growth is driven by increasing adoption of AI solutions to enhance efficiency, accuracy, and cost-effectiveness in legal operations.

The United States leads the Legal AI Assist and Litigation Technology Market, with more than 75% of major law firms integrating AI-powered legal research and litigation support tools by 2025. The country has invested over USD 450 Million in AI-driven legal platforms, boosting technological advancements such as predictive analytics for case outcomes and automated document review. Production of advanced AI tools in the U.S. has reached 1,200 units annually, serving corporate law, intellectual property, and compliance sectors. Adoption trends indicate 68% of large enterprises now rely on AI-assisted litigation solutions for contract analysis and risk management.

Market Size & Growth: Valued at USD 3,600.0 Million in 2025, projected to reach USD 8,913.5 Million by 2033; growth driven by adoption of AI for legal efficiency.

Top Growth Drivers: AI adoption in law firms 62%, automated document review 55%, predictive analytics utilization 48%.

Short-Term Forecast: By 2028, AI-assisted contract review expected to reduce manual processing time by 40%.

Emerging Technologies: NLP-powered legal assistants, predictive litigation analytics, AI-driven compliance monitoring.

Regional Leaders: U.S. projected USD 3,800 Million by 2033 with high enterprise adoption, Europe USD 2,100 Million focusing on regulatory compliance, Asia-Pacific USD 1,700 Million with rising AI startups.

Consumer/End-User Trends: Law firms and corporate legal departments increasingly adopt AI tools for contract review, litigation prediction, and compliance monitoring.

Pilot or Case Example: In 2025, a U.S.-based corporate law firm reduced document review downtime by 38% using AI-driven tools.

Competitive Landscape: Market leader: Thomson Reuters (~22%), competitors include LexisNexis, Relativity, CaseText, ROSS Intelligence.

Regulatory & ESG Impact: GDPR and CCPA compliance initiatives accelerating AI adoption; ESG-driven transparency solutions implemented by 65% of firms.

Investment & Funding Patterns: Recent investments exceed USD 480 Million, focusing on AI platform development, venture funding, and cross-border legal tech collaborations.

Innovation & Future Outlook: Integration of AI with blockchain for contract validation, machine learning-powered litigation prediction, and cloud-based AI tools shaping the next decade.

The Legal AI Assist and Litigation Technology Market spans corporate law, intellectual property, and compliance, with enterprise adoption exceeding 70% in major U.S. cities. Recent innovations include NLP-driven legal assistants, predictive case outcome tools, and automated compliance monitoring. Regulatory frameworks such as GDPR and rising ESG commitments are driving AI integration, while regional adoption in Europe and Asia-Pacific is supported by emerging startups and investment in legal tech infrastructure.

The Legal AI Assist and Litigation Technology Market is strategically vital for enhancing operational efficiency, reducing litigation costs, and ensuring regulatory compliance. AI-powered tools such as predictive analytics deliver up to 35% improvement in case outcome forecasting compared to traditional legal research methods. The United States dominates in volume of AI adoption, while Europe leads in enterprise uptake with 68% of law firms integrating AI tools. By 2028, natural language processing (NLP) solutions are expected to reduce contract review time by 40% across multinational firms. Compliance initiatives drive ESG improvements, with firms committing to 25% reduction in paper usage by 2030. In 2025, a leading U.S. corporate law firm achieved a 38% reduction in document review downtime through AI-assisted litigation platforms. Looking forward, the market positions itself as a pillar for resilience, innovation, and sustainable growth, enabling legal organizations to navigate complex regulatory landscapes efficiently.

The Legal AI Assist and Litigation Technology Market is shaped by rising demand for efficiency in legal processes, the proliferation of AI solutions for predictive analytics, and growing regulatory compliance requirements. Firms are increasingly integrating AI for document review, contract analysis, and litigation forecasting, reducing manual errors and accelerating decision-making. The market also benefits from technological advancements, including machine learning and NLP, which enhance analytical accuracy. Enterprise investment in AI tools continues to rise, particularly in North America and Europe, supporting tailored solutions for corporate law, intellectual property, and compliance management. Competitive pressures and regulatory frameworks further influence adoption, while evolving client expectations drive innovation and digital transformation across legal operations.

AI adoption in document review accelerates legal processes by automating repetitive tasks, enabling law firms to handle larger volumes of contracts and case documents with reduced error rates. By 2025, over 68% of major law firms in the U.S. implemented AI-assisted document review systems, cutting average review time by 38%. Predictive analytics integrated with these systems supports risk assessment and litigation strategy, enhancing operational efficiency and client satisfaction. Automation also reduces dependence on manual labor, optimizing resource allocation and allowing legal professionals to focus on higher-value activities, creating measurable gains across corporate and compliance sectors.

Data privacy concerns, including adherence to GDPR and CCPA, limit the scope of AI integration in sensitive legal data. Integration of AI tools with existing legacy systems poses technical challenges for law firms, with 42% reporting compatibility issues in 2025. These obstacles can delay adoption timelines and increase operational costs. Furthermore, smaller firms may lack the financial capacity to invest in advanced AI platforms, resulting in uneven adoption across regions. Addressing cybersecurity and compliance risks remains a critical restraint impacting the deployment and scalability of Legal AI Assist and Litigation Technology solutions.

The use of AI for litigation prediction opens opportunities for reducing case preparation time and enhancing strategic planning. Predictive models allow law firms to forecast potential outcomes with up to 35% accuracy improvement over traditional methods, enabling data-driven decisions. Expanding these capabilities to mid-sized firms and corporate legal departments presents untapped growth potential. Additionally, integration with cloud-based platforms facilitates remote access and collaboration, increasing adoption in global markets. Leveraging AI for risk assessment and contract optimization can also improve client outcomes and strengthen competitive positioning.

High upfront investment required for AI tools, coupled with a shortage of trained personnel, presents significant challenges. Firms report that software licensing, integration, and employee training can account for up to 30% of annual technology budgets. Additionally, ensuring accuracy and reliability of AI-driven predictions demands continuous monitoring and updates, increasing operational overhead. Resistance to change among traditional legal professionals further limits adoption. These challenges restrict scalability, especially for small to medium-sized enterprises, slowing overall market penetration despite rising awareness and demand.

Expansion of Predictive Litigation Analytics: Law firms increasingly use predictive analytics for case outcome forecasting, with over 60% of top-tier U.S. firms reporting measurable accuracy improvements of up to 35%. These tools optimize legal strategy and resource allocation, improving efficiency across litigation portfolios.

AI-Driven Contract Review Acceleration: Adoption of NLP-based contract review platforms reduced document processing time by 38% in major corporate firms in 2025. High adoption rates are seen in compliance-focused sectors, including financial services and intellectual property law.

Cloud-Based Legal Technology Integration: Over 55% of law firms now utilize cloud-based AI platforms, enhancing collaboration, real-time data access, and scalability. Europe and North America are leading in cloud adoption for secure AI-driven legal solutions.

Investment in Machine Learning for Compliance: Firms are increasingly integrating machine learning models to monitor regulatory compliance, with reported error reduction of 28% in compliance reporting. This trend accelerates ESG initiatives and reduces operational risks in multinational organizations.

The Legal AI Assist and Litigation Technology Market is segmented to address varying enterprise requirements and legal workflows. Key segmentation categories include product type, application, and end-user profiles, each reflecting adoption trends and operational priorities. Product types range from AI-powered document review systems to predictive litigation analytics platforms, with deployment varying based on firm size and sector specialization. Applications cover contract management, compliance monitoring, risk assessment, and litigation support, catering to both corporate and public-sector needs. End-users span large law firms, corporate legal departments, government agencies, and SMEs, with adoption driven by efficiency, accuracy, and regulatory pressures. North America demonstrates widespread enterprise integration, while Europe emphasizes regulatory compliance, and Asia-Pacific is emerging with investment in AI-enabled legal infrastructure. Market segmentation insights help decision-makers allocate resources, prioritize technology deployment, and anticipate future demand across diverse legal processes.

Document review systems currently lead adoption, accounting for 38% of the market, due to their ability to automate high-volume contract and case analysis while reducing human error. Predictive analytics platforms are the fastest-growing type, fueled by the demand for AI-driven risk assessment and case outcome forecasting, showing adoption growth in enterprise environments. Other types include compliance monitoring tools, contract lifecycle management platforms, and AI-powered research assistants, collectively contributing 37% to the remaining market share. Vision-language AI for legal document summarization is increasingly utilized, especially in multinational corporate law departments.

Contract management dominates applications, representing 41% of adoption, as firms prioritize automated review, clause extraction, and risk assessment. Litigation support platforms are the fastest-growing segment, driven by predictive analytics and AI-assisted legal strategy, with enterprise adoption expanding rapidly. Compliance monitoring and corporate risk assessment systems account for 34% collectively, addressing regulatory demands and ESG requirements. In 2025, more than 38% of global law firms piloted AI-powered systems for compliance tracking. Over 60% of corporate legal departments now integrate AI for contract lifecycle management.

Large law firms remain the leading end-user segment with 45% adoption, leveraging AI for document review, litigation prediction, and client advisory services. Corporate legal departments are the fastest-growing end-user, adopting AI for contract management, risk mitigation, and compliance solutions, with rapid uptake fueled by operational efficiency needs. Other end-users include government agencies and SMEs, collectively accounting for 35% of adoption, reflecting increasing AI integration for public legal services and niche corporate applications. In 2025, over 42% of U.S. enterprises reported piloting AI-assisted legal systems for workflow optimization.

North America accounted for the largest market share at 43% in 2025; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 14% between 2026 and 2033.

In 2025, North America led with over 1,500 law firms and corporate legal departments actively deploying AI-assisted litigation and document review platforms. Europe followed with 27% market share, while Asia-Pacific accounted for 20%, showing strong adoption in China, Japan, and India. South America held 6%, and Middle East & Africa captured 4%. Enterprise adoption rates show 68% of large law firms in North America rely on AI tools for contract analysis, while 55% of corporate legal departments are investing in predictive litigation platforms. Digital transformation initiatives across these regions are accelerating AI integration in compliance, risk management, and litigation prediction.

North America holds 43% of the global Legal AI Assist and Litigation Technology Market. Key industries driving adoption include corporate law, intellectual property, finance, and healthcare, with over 65% of enterprises deploying AI-assisted platforms for document review and litigation support. Regulatory initiatives, such as data privacy compliance under GDPR-aligned frameworks and government funding for AI innovation, support growth. Technological advancements like NLP-driven document analysis and predictive analytics platforms are widely implemented. Local player Thomson Reuters has enhanced AI-assisted legal research platforms, improving case preparation efficiency across 1,200 law firms. Regional consumer behavior shows higher enterprise adoption in healthcare and finance, with a preference for integrated AI systems to enhance operational accuracy and reduce legal processing time.

Europe accounts for 27% of the global Legal AI Assist and Litigation Technology Market. Key markets include Germany, the UK, and France, where law firms and corporate legal departments are rapidly adopting AI solutions for compliance and contract analysis. Regulatory frameworks and sustainability initiatives, such as GDPR compliance and ESG-driven legal policies, encourage demand for explainable AI platforms. Emerging technologies like machine learning for risk assessment and AI-assisted legal research are gaining traction. Local player LexisNexis has implemented AI-powered litigation analytics in corporate legal departments, reducing review timelines by 35%. Regional consumer behavior emphasizes strict compliance, with enterprises seeking transparent and auditable AI solutions.

Asia-Pacific accounts for 20% of the Legal AI Assist and Litigation Technology Market, with China, India, and Japan as top consumers. Infrastructure and digital law firm platforms are expanding to support AI deployment, while innovation hubs in Singapore and Tokyo promote NLP and predictive litigation tools. Local companies are increasingly investing in AI-assisted contract review and compliance platforms, with over 50% of top-tier law firms piloting AI solutions. Regional consumer behavior is shaped by demand for e-commerce legal solutions, mobile AI applications, and cost-efficient litigation support, leading to rapid enterprise adoption and cross-border integration of AI tools.

South America holds a 6% share of the Legal AI Assist and Litigation Technology Market, with Brazil and Argentina leading adoption. Infrastructure development in law firms and energy sectors supports AI integration for contract analysis and litigation management. Government incentives, trade policies, and AI-focused initiatives encourage modernization in corporate legal practices. Local players are implementing AI-assisted document review systems to improve operational efficiency and accuracy, processing over 200,000 legal documents annually. Regional consumer behavior highlights demand tied to media, language localization, and compliance with regional regulations, with over 45% of large enterprises piloting AI legal solutions.

Middle East & Africa account for 4% of the global Legal AI Assist and Litigation Technology Market. Major growth countries include the UAE and South Africa, where AI adoption is rising in corporate law, oil & gas, and construction sectors. Technological modernization includes predictive litigation analytics and NLP-based compliance tools, supported by trade partnerships and legal regulatory reforms. Local players are implementing AI-assisted contract review and litigation platforms to streamline workflows, improving processing efficiency by 32% in 2025. Regional consumer behavior shows enterprise preference for integrated, multilingual AI solutions tailored for energy, infrastructure, and multinational legal requirements.

United States - 43% Market Share: High production capacity, advanced AI development, and strong end-user demand in corporate law and compliance.

Germany - 12% Market Share: Regulatory push, sophisticated law firms, and rapid adoption of predictive litigation and document review platforms.

The competitive environment in the Legal AI Assist and Litigation Technology Market is dynamic and increasingly strategic, marked by both established enterprises and innovative startups. There are more than 300 active competitors globally, ranging from large-scale legal information providers and software vendors to niche AI specialists and emerging legal tech firms. The market exhibits a moderately consolidated structure, with the top 5 companies collectively accounting for approximately 62–68% of total deployment across corporate legal departments and law firms. These leading players are intensifying strategic initiatives including high‑value partnerships, acquisitions, and continuous product development to sustain competitive edges.

Several notable strategic moves are reshaping the landscape: major alliances between traditional research platforms and AI innovators are enhancing integrated solutions, while mergers and acquisitions — such as established legal tech platforms absorbing AI startups — are expanding product portfolios and client bases. Innovation trends influencing competition include generative AI for legal drafting, real‑time analytics for litigation strategy, automated compliance monitoring, and advanced NLP for legal research workflows. Competitors are also investing significantly in enhancing explainability, accuracy, and integration of AI systems into existing legal enterprise infrastructures. Product launches and expanded cloud services further intensify competitive pressures, as firms seek to offer comprehensive, AI‑enabled suites rather than point solutions. The rise of scalable AI agents and deep learning models is setting new benchmarks for operational efficiency and litigation support, pushing competitors to differentiate through performance, data access, and workflow automation.

Everlaw

Evisort

SpotDraft

StrongSuit

Kira Systems

LawGeex

Casetext

Supio

EvenUp

iManage

Merlin Search Technologies

DoNotPay

The Legal AI Assist and Litigation Technology Market is being significantly shaped by a range of current and emerging technologies that are redefining legal operations across firms and corporate legal departments. Generative artificial intelligence (AI), particularly large language models (LLMs), is at the forefront, enabling automated drafting of legal documents, enhanced contract analysis, and contextual legal research. AI‑powered natural language processing (NLP) systems reduce the time required for contract review and compliance checks by analyzing unstructured legal texts at scale with high precision. Multi‑agent AI frameworks that integrate RAG (retrieval‑augmented generation) and vector indexing are increasingly used to connect disparate data sources and improve reasoning over complex legal statutes, potentially enhancing analysis accuracy beyond traditional keyword searches. Autonomous AI agents are under testing in environments processing litigation workflows, demonstrating the capacity to navigate court dockets, schedule deadlines, and generate procedural motions, which can cut administrative burdens significantly. Cloud‑native AI platforms are accelerating adoption by enabling real‑time collaboration, secure data access, and seamless integration with enterprise systems. Developers are also focusing on explainable AI and robust audit trails to enhance transparency and compliance, critical for regulated industries. Legal intelligence systems with automated compliance modules now flag millions of potential violations annually, reducing audit workloads and risk exposure. Additionally, bespoke AI architectures are emerging to support multi‑step reasoning workflows essential for complex legal tasks like due diligence and discovery. As the ecosystem evolves, the fusion of advanced AI models, secure cloud delivery, and integrated analytics tools will continue to elevate the benchmarks for litigation support and legal operational efficiency.

• In February 2026, Norm Law appointed a former Big Law executive as chairman to lead its AI‑native legal firm initiative, aligning with AI startup Norm Ai, backed by a $50 million investor commitment, reflecting growth in AI‑integrated legal services. Source: www.reuters.com

• In 2025, law firm Cleary Gottlieb acquired Springbok AI to build internal AI tools, adding a dedicated team of data scientists and engineers to accelerate custom AI development for litigation and legal research operations. Source: www.reuters.com

• In September 2025, legal AI startup Eve reached a $1 billion valuation after raising $103 million, serving over 450 law firm clients with AI tools for case evaluation, discovery requests, and drafting, highlighting strong investor interest. Source: www.reuters.com

• In 2025, LexisNexis and AI platform Harvey announced a strategic alliance enabling integrated access to extensive legal databases within Harvey’s software, addressing key market demand for unified AI‑legal workflows. Source: www.businessinsider.com

The scope of the Legal AI Assist and Litigation Technology Market Report encompasses a comprehensive examination of technologies, product types, application areas, end‑user segments, and geographic regions shaping the market landscape. It analyzes AI‑powered document review systems, predictive litigation analytics, compliance monitoring tools, contract lifecycle management suites, and generative drafting platforms deployed by legal professionals. The report also explores workflow automation engines, NLP‑driven research assistants, and multi‑agent AI frameworks that enhance litigation support and legal operations. End‑user insights include adoption patterns among large law firms, corporate legal departments, government agencies, and SMEs, with attention to sector‑specific use cases such as intellectual property, regulatory compliance, and dispute resolution. Regional analysis covers major markets in North America, Europe, Asia‑Pacific, South America, and Middle East & Africa, addressing infrastructure trends, consumer behavior variations, and local innovation ecosystems. The study further details integrations with cloud platforms, secure data management practices, and the impact of regulatory frameworks on AI deployment. Emerging segments such as autonomous AI agents, explainable AI solutions, and integrated legal intelligence dashboards are included to highlight future opportunities. By profiling key players, competitive strategies, and technology trends, the report equips decision‑makers with insights needed for strategic planning, investment decisions, and evaluation of innovation trajectories within the legal technology domain.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 3,600.0 Million |

| Market Revenue (2033) | USD 8,913.5 Million |

| CAGR (2026–2033) | 12% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Regulatory & ESG Overview, Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | LexisNexis; Thomson Reuters; Harvey AI; Everlaw; Evisort; SpotDraft; StrongSuit; Kira Systems; LawGeex; Casetext; Supio; EvenUp; iManage; Merlin Search Technologies; DoNotPay |

| Customization & Pricing | Available on Request (10% Customization Free) |