Reports

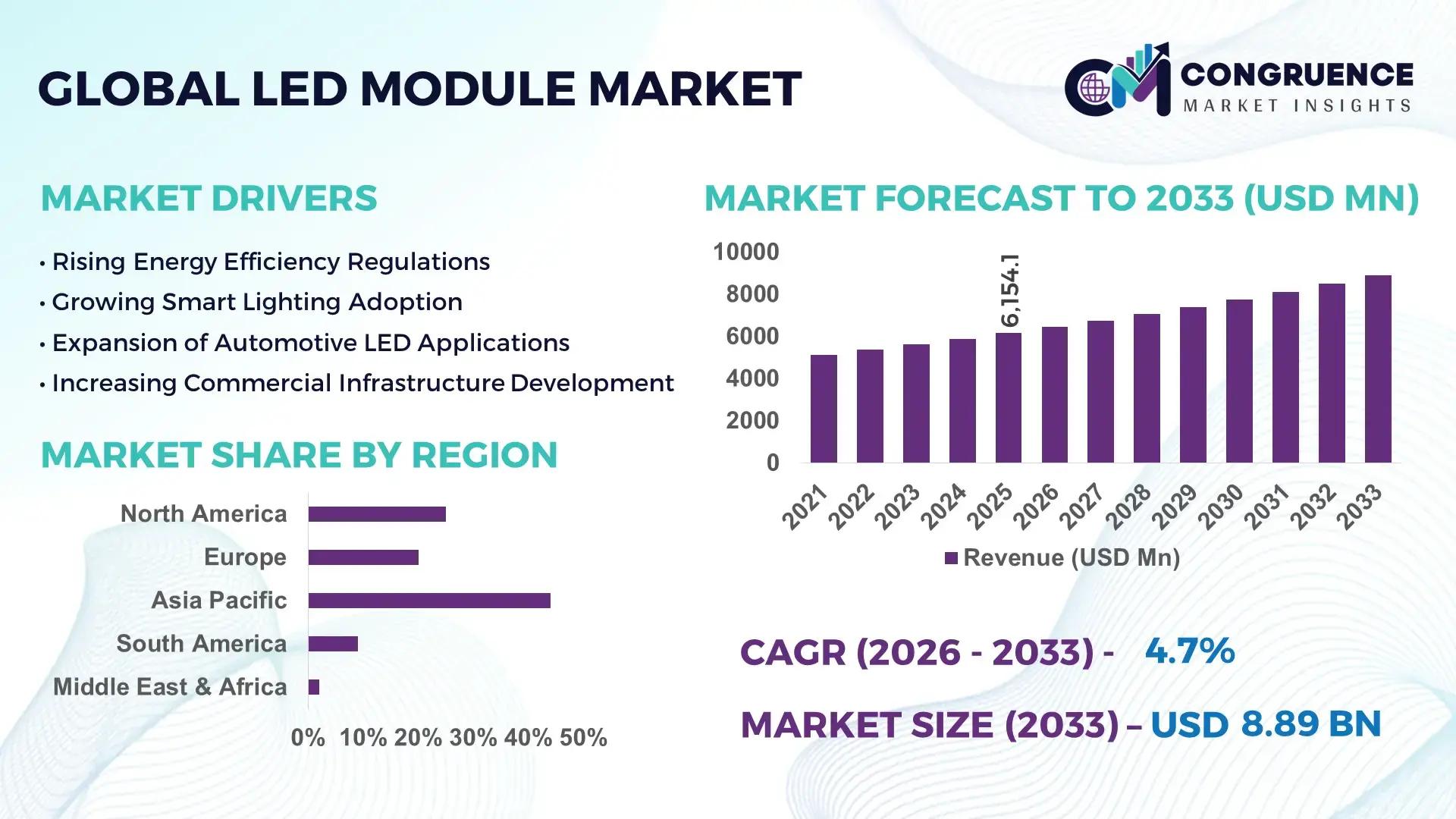

The Global LED Module Market was valued at USD 6154.11 Million in 2025 and is anticipated to reach a value of USD 8886.67 Million by 2033 expanding at a CAGR of 4.7% between 2026 and 2033. The market expansion is primarily driven by accelerating adoption of energy-efficient lighting systems across commercial infrastructure, smart cities, automotive, and industrial automation sectors.

China remains the dominant production hub for LED modules, supported by an extensive semiconductor manufacturing ecosystem and vertically integrated supply chains. The country accounts for over 60% of global LED packaging output capacity, with annual LED chip production exceeding 250 billion units. Major manufacturing clusters in Shenzhen, Xiamen, and Jiangsu support large-scale exports of SMD and COB LED modules for architectural, signage, and automotive applications. Investments exceeding USD 5 billion in advanced mini-LED and micro-LED fabrication lines over the past three years have strengthened high-lumen and precision lighting output. Domestic adoption in urban infrastructure projects covers more than 70% of newly installed street lighting systems using modular LED configurations, reflecting robust local consumption alongside export leadership.

Market Size & Growth: Valued at USD 6154.11 Million in 2025 and projected to reach USD 8886.67 Million by 2033 at 4.7% CAGR, supported by rapid transition to high-efficiency LED lighting systems across infrastructure and automotive sectors.

Top Growth Drivers: Energy savings up to 65%, smart lighting adoption rising 40%, automotive LED penetration exceeding 55%.

Short-Term Forecast: By 2028, advanced driver integration is expected to reduce module energy losses by 18% and improve luminous efficacy by 12%.

Emerging Technologies: Mini-LED backlighting, micro-LED display modules, and IoT-enabled intelligent LED modules.

Regional Leaders: Asia Pacific projected above USD 4200 Million by 2033 with strong manufacturing depth; North America near USD 1900 Million driven by retrofit upgrades; Europe around USD 1600 Million supported by energy directives.

Consumer/End-User Trends: Commercial real estate, automotive OEMs, and industrial facilities prioritize modular LED retrofits for 50,000+ hour lifespan and low maintenance.

Pilot Example: In 2024, a municipal smart lighting project achieved 32% electricity reduction using sensor-based LED modules.

Competitive Landscape: Signify holds approximately 18% share, followed by Osram, Samsung Electronics, Nichia, and Cree LED.

Regulatory & ESG Impact: Energy efficiency mandates target 30% power reduction in public lighting installations by 2030.

Investment Trends: Over USD 3 billion invested globally in mini-LED and smart lighting production facilities since 2023.

Innovation Outlook: Integrated thermal management, tunable white modules, and AI-enabled adaptive lighting systems shaping next-generation LED module applications.

The LED Module Market is diversified across commercial lighting contributing nearly 35% of total demand, automotive applications around 20%, consumer electronics approximately 18%, and industrial lighting close to 15%. Recent advancements in chip-scale packaging and high-density COB modules have improved luminous efficacy beyond 180 lumens per watt in premium installations. Environmental regulations promoting low mercury and reduced carbon footprints accelerate retrofit demand in Europe and North America, while Asia Pacific leads in consumption due to infrastructure modernization. Growing demand for customizable RGB modules in entertainment and smart retail environments indicates sustained innovation momentum and future product differentiation strategies.

The LED Module Market holds strategic relevance as governments and enterprises prioritize energy efficiency, digital infrastructure modernization, and sustainable lighting ecosystems. Compared to conventional fluorescent systems, integrated smart LED modules deliver nearly 60% improvement in energy efficiency and 3x longer operational lifespan, significantly lowering lifecycle costs for municipalities and commercial operators. Mini-LED technology delivers 25% higher brightness uniformity compared to traditional SMD modules, enabling advanced display and architectural applications.

Asia Pacific dominates in production volume, while Europe leads in adoption intensity with over 68% of enterprises deploying LED-based retrofit programs aligned with energy transition targets. By 2028, AI-enabled adaptive lighting controls are expected to cut operational energy consumption in commercial buildings by 20% through occupancy sensing and daylight harvesting algorithms.

Firms are committing to ESG performance metrics such as 40% carbon emission reduction in lighting infrastructure by 2030, supported by recyclable aluminum heat sinks and RoHS-compliant components. In 2024, Germany achieved a 28% public lighting energy reduction through nationwide smart LED modernization initiatives integrating remote monitoring systems. Strategically, the LED Module Market is evolving toward intelligent, modular, and sensor-driven architectures. Integration with IoT platforms, smart grids, and electric vehicle infrastructure positions the LED Module Market as a foundational pillar of resilience, regulatory compliance, and sustainable growth across global urban and industrial ecosystems.

Global infrastructure modernization programs are rapidly replacing legacy lighting with energy-efficient LED modules capable of reducing electricity consumption by up to 65%. More than 300 million streetlights worldwide are undergoing retrofit initiatives, with modular LED solutions forming the core technology due to durability exceeding 50,000 operating hours. Commercial buildings account for nearly 40% of lighting electricity usage, prompting facility managers to deploy high-lumen LED modules integrated with smart drivers. Automotive manufacturers are also expanding LED module integration, with over 55% of new passenger vehicles equipped with LED-based lighting systems. These quantifiable improvements in performance, maintenance savings, and environmental compliance continue to drive strong institutional and industrial demand.

The LED Module Market faces pressure from fluctuating prices of gallium, indium, aluminum substrates, and semiconductor wafers, which directly influence production costs. In recent years, semiconductor lead times extended beyond 20 weeks in certain regions, delaying module assembly and shipment cycles. Advanced mini-LED fabrication requires precision equipment costing millions per production line, limiting smaller manufacturers’ entry capacity. Additionally, thermal management components such as high-grade aluminum heat sinks have experienced price increases exceeding 15% during peak supply shortages. These cost uncertainties and dependency on specialized chip fabrication infrastructure create operational challenges and margin constraints for LED module manufacturers globally.

Smart city programs across more than 100 countries are integrating sensor-enabled LED modules into traffic systems, public spaces, and security infrastructure. Intelligent lighting networks can reduce municipal electricity consumption by 30% while enabling remote diagnostics and predictive maintenance. Modular LED luminaires embedded with IoT connectivity allow data collection for traffic density, environmental monitoring, and public safety analytics. Growing demand for adaptive RGB and tunable white modules in retail and entertainment sectors also opens high-margin customization opportunities. Furthermore, electric vehicle charging hubs increasingly deploy high-efficiency LED canopy modules for enhanced illumination and branding, creating new cross-sector revenue streams for manufacturers.

Although LED modules offer long-term savings, upfront integration costs for smart lighting systems can be 25–35% higher than conventional replacements due to control systems, sensors, and network infrastructure. Compliance with regional standards such as electromagnetic compatibility, photobiological safety, and environmental directives requires extensive testing and certification, extending product launch timelines. Recycling mandates for electronic waste management further increase logistical obligations. Additionally, compatibility issues between legacy infrastructure and advanced modular LED systems create retrofitting complexities in older industrial facilities. These regulatory, technical, and financial hurdles require strategic planning and capital allocation, posing measurable challenges for stakeholders within the LED Module Market.

Mini-LED and Micro-LED Penetration Exceeds 35% in Premium Installations

Adoption of advanced mini-LED and micro-LED modules has crossed 35% within high-end display backlighting and architectural lighting projects. Mini-LED arrays now integrate over 10,000 micro diodes per square meter, delivering brightness levels exceeding 1,500 nits and improving contrast ratios by 40% compared to traditional SMD modules. In automotive adaptive headlamps, pixelated LED modules enable up to 84 individually controlled lighting zones, enhancing road visibility by nearly 30%. This measurable performance improvement is accelerating replacement cycles across premium applications.

Smart and IoT-Enabled LED Modules Achieve 45% Deployment in Urban Projects

Approximately 45% of newly installed municipal lighting systems now incorporate sensor-enabled LED modules integrated with wireless control networks. These intelligent systems reduce electricity consumption by 25%–35% through motion sensing and daylight harvesting features. Over 120 major cities have deployed centralized monitoring platforms managing more than 1 million LED nodes collectively. Data-driven dimming capabilities extend module lifespan by nearly 20%, lowering maintenance frequency and enabling predictive servicing across smart infrastructure networks.

High-Efficiency COB Modules Surpass 180 Lumens per Watt Benchmark

Chip-on-board (COB) LED modules are achieving luminous efficacy levels above 180 lm/W in commercial installations, representing a 15% efficiency improvement over earlier generation arrays. Industrial warehouses replacing metal halide systems report up to 60% reduction in power usage after COB module retrofits. Thermal resistance in advanced aluminum substrate designs has decreased by 12%, improving heat dissipation and operational stability in high-output environments exceeding 50,000 operational hours.

Customization and Tunable White Modules Grow by 28% in Commercial Interiors

Demand for tunable white and RGB LED modules in retail and hospitality environments has increased by 28%, driven by human-centric lighting strategies. Adjustable color temperatures ranging from 2,700K to 6,500K improve occupant comfort and can enhance workplace productivity by nearly 12%. Entertainment venues are deploying programmable LED modules capable of 16 million color variations, increasing dynamic branding visibility by 20%. These modular customization capabilities are strengthening differentiation strategies for lighting manufacturers and integrators.

The LED Module Market segmentation reflects diversified demand across product types, applications, and end-user categories. By type, surface-mounted device (SMD), chip-on-board (COB), and high-power LED modules form the core product clusters, collectively addressing over 80% of industry demand. Application-wise, general lighting accounts for a dominant share due to infrastructure retrofits, while automotive and display backlighting demonstrate rapid technological integration. End-user analysis indicates strong penetration in commercial real estate, industrial manufacturing, automotive OEMs, and municipal authorities implementing energy modernization initiatives. More than 60% of infrastructure upgrade projects now prioritize modular LED solutions for durability exceeding 50,000 hours and energy efficiency improvements above 50%. This structured segmentation highlights the LED Module Market’s alignment with energy mandates, digital transformation strategies, and industrial automation investments.

Surface-Mounted Device (SMD) LED modules currently account for approximately 48% of total adoption due to their flexibility, compact design, and suitability for signage, retail lighting, and display applications. Their multi-chip configuration allows uniform light distribution and improved heat management, making them preferred in commercial interiors and outdoor digital billboards. Chip-on-Board (COB) LED modules hold nearly 32% of adoption, offering higher lumen density and superior thermal performance. However, mini-LED modules represent the fastest-growing type, expanding at an estimated CAGR of 8.2% due to rising demand in premium displays and automotive adaptive lighting systems. Mini-LED arrays enable up to 20% higher brightness and 30% improved contrast over conventional SMD configurations. High-power and specialty LED modules, including UV and infrared variants, collectively contribute around 20%, serving niche applications in industrial curing, medical devices, and horticulture lighting.

General lighting applications dominate with approximately 52% share, driven by large-scale retrofits in commercial buildings and public infrastructure. LED modules reduce electricity consumption by up to 65% compared to fluorescent systems, making them central to municipal and enterprise sustainability programs. Automotive lighting accounts for around 22% of adoption, with LED modules integrated into headlamps, daytime running lights, and interior ambient systems. However, display backlighting and digital signage represent the fastest-growing application segment, expanding at an estimated CAGR of 9.1% due to demand for high-resolution, energy-efficient panels in consumer electronics and commercial advertising. Other applications—including horticulture lighting, industrial machinery illumination, and healthcare equipment—collectively contribute roughly 26%, benefiting from spectral customization and durability exceeding 50,000 hours.

Commercial real estate leads with nearly 38% of total LED module adoption, supported by office complexes, shopping malls, and hospitality infrastructure seeking 50%–60% energy savings through lighting modernization. Industrial facilities account for about 24%, leveraging high-lumen modules for warehouse and production floor illumination. Automotive manufacturers represent the fastest-growing end-user segment, expanding at an estimated CAGR of 7.5%, as over 55% of new vehicles integrate advanced LED headlamp modules for adaptive beam control and safety compliance. Municipal authorities contribute roughly 18% through smart street lighting initiatives incorporating sensor-enabled modules. Other end-users—including healthcare institutions, educational campuses, and entertainment venues—collectively account for around 20%, driven by demand for tunable white lighting and programmable RGB systems.

Asia-Pacific accounted for the largest market share at 46% in 2025 however, North America is expected to register the fastest growth, expanding at a CAGR of 6.1% between 2026 and 2033.

Asia-Pacific’s dominance is supported by annual LED chip production exceeding 250 billion units and over 60% of global LED packaging capacity concentrated in China, Japan, and South Korea. More than 70% of new urban infrastructure lighting installations in major Asian economies now utilize modular LED configurations. North America holds approximately 24% share, driven by large-scale retrofit projects covering over 35 million commercial luminaires. Europe represents nearly 20%, influenced by strict energy efficiency directives targeting 30% electricity reduction in public lighting by 2030. South America and Middle East & Africa collectively account for around 10%, with over 15 million streetlight upgrades underway across emerging urban corridors. Industrial and automotive demand continues to rise across all regions, with automotive LED penetration surpassing 55% in developed economies and commercial building LED adoption exceeding 75% in newly constructed facilities.

How Are Digital Infrastructure Upgrades Accelerating Smart Lighting Transformation?

North America LED Module Market holds approximately 24% of global demand, supported by widespread commercial retrofitting and smart city modernization programs. Over 35 million lighting points in the United States and Canada have transitioned to LED-based modular systems, reducing electricity consumption by nearly 50% in municipal deployments. Healthcare, retail, and financial services sectors represent more than 40% of commercial installations, reflecting higher enterprise adoption. Federal energy efficiency standards targeting 45 lumens per watt minimum performance benchmarks continue to shape procurement decisions. IoT-enabled LED modules now account for nearly 38% of new installations, integrating wireless controls and occupancy sensors. Cree LED, headquartered in the United States, continues expanding high-power LED module production, introducing next-generation silicon carbide-based designs improving thermal performance by 15%. Regional consumers prioritize durability exceeding 50,000 operational hours and integration with building automation platforms, particularly in healthcare and finance environments where reliability and compliance remain critical.

How Are Sustainability Mandates Reshaping Energy-Efficient Lighting Adoption?

Europe LED Module Market contributes close to 20% of total global demand, with Germany, the United Kingdom, and France collectively accounting for over 60% of regional consumption. More than 75% of new commercial construction projects incorporate LED modules aligned with eco-design regulations targeting 30% energy savings in public infrastructure. Regulatory frameworks emphasizing carbon neutrality by 2050 drive rapid replacement of halogen and fluorescent systems. Advanced tunable white modules have witnessed 28% higher adoption in office environments focused on human-centric lighting. Osram, based in Germany, has expanded digital LED module solutions with integrated smart drivers, enhancing luminous efficacy beyond 180 lumens per watt. Enterprises across the region emphasize compliance, recyclability, and RoHS standards, with over 65% of procurement contracts requiring environmental certification. Consumer preference leans toward sustainable and explainable lighting technologies that demonstrate measurable energy and carbon reductions.

What Manufacturing Scale and Urbanization Trends Are Fueling Massive Lighting Deployment?

Asia-Pacific LED Module Market leads globally with 46% share, supported by dominant manufacturing clusters in China, Japan, South Korea, and India. China alone accounts for more than 60% of global LED packaging output, while Japan and South Korea lead innovation in mini-LED and micro-LED technologies. Over 70% of newly installed public streetlights in major Asian cities now utilize modular LED systems. Rapid urbanization has resulted in more than 200 smart city initiatives deploying IoT-connected lighting networks across India and Southeast Asia. Samsung Electronics continues advancing mini-LED module integration into premium displays, increasing brightness levels above 1,500 nits. Regional buyers emphasize cost efficiency and scalability, with industrial parks and logistics hubs driving high-lumen installations exceeding 200 watts per module. Consumer behavior in this region reflects strong infrastructure expansion and high-volume production demand.

How Are Energy Reforms and Urban Modernization Shaping Lighting Investments?

South America LED Module Market represents approximately 6% of global share, with Brazil and Argentina contributing over 70% of regional demand. More than 5 million streetlights across Brazil are undergoing LED retrofitting programs aimed at reducing electricity consumption by up to 55%. Government-backed energy efficiency initiatives encourage municipalities to adopt modular LED systems with operational lifespans exceeding 50,000 hours. Industrial facilities and sports infrastructure projects account for nearly 35% of installations. Trade policies supporting import duty reductions on LED components have increased product availability by 18% over the past three years. Regional consumers increasingly demand RGB modules for entertainment venues and stadium lighting, reflecting media-driven infrastructure growth. Local distributors report a 25% rise in smart lighting inquiries tied to public-private partnership projects.

How Are Mega Infrastructure Projects and Energy Diversification Driving Lighting Upgrades?

Middle East & Africa LED Module Market accounts for nearly 4% of global demand, driven by large-scale construction and oil & gas infrastructure projects in the UAE, Saudi Arabia, and South Africa. Over 3 million LED streetlight replacements are underway in Gulf Cooperation Council countries as part of national energy diversification strategies targeting 30% electricity savings. Smart city initiatives such as those in the UAE integrate sensor-enabled LED modules into transportation corridors and commercial hubs. South Africa’s industrial facilities contribute approximately 28% of regional demand due to warehouse and mining illumination needs. Local regulations increasingly mandate minimum luminous efficacy thresholds above 120 lumens per watt. Regional consumers prioritize high-durability modules capable of operating in extreme temperatures exceeding 45°C, reflecting climatic requirements and infrastructure modernization priorities.

China – 34% share in LED Module Market: High production capacity exceeding 250 billion LED chips annually and extensive export-oriented manufacturing ecosystem support sustained leadership.

United States – 18% share in LED Module Market: Strong commercial retrofit demand and advanced smart lighting integration across healthcare, retail, and municipal infrastructure drive substantial domestic adoption.

The LED Module Market exhibits a moderately fragmented yet strategically competitive structure, with more than 120 active global and regional manufacturers participating across packaging, module integration, and smart lighting solutions. The top five companies collectively account for approximately 48% of total market presence, reflecting a semi-consolidated environment where scale, intellectual property, and vertical integration drive competitive advantage. Leading players continue investing heavily in mini-LED and micro-LED fabrication lines, with over USD 3 billion allocated globally toward capacity expansion and automation upgrades since 2023.

Strategic initiatives include cross-industry partnerships between semiconductor firms and lighting integrators to accelerate high-density chip development, as well as mergers aimed at strengthening regional distribution networks. More than 35 significant product launches were recorded in the past 24 months, focusing on high-efficacy modules exceeding 180 lumens per watt and IoT-enabled smart drivers. Competitive differentiation increasingly centers on thermal management innovation, silicon carbide substrates, and tunable white capabilities offering 2,700K–6,500K flexibility.

Companies are also expanding localized assembly facilities to reduce supply chain risks, particularly in North America and Europe, where lead times previously exceeded 20 weeks during semiconductor shortages. The growing demand for ESG-compliant and recyclable components further intensifies innovation competition, positioning sustainability metrics as a decisive procurement criterion for commercial and municipal buyers.

Signify

Osram

Samsung Electronics

Nichia Corporation

Cree LED

Lumileds

Seoul Semiconductor

Everlight Electronics

Toyoda Gosei

LG Innotek

Stanley Electric

Technological advancement within the LED Module Market is centered on efficiency optimization, miniaturization, digital integration, and advanced thermal management. High-efficacy LED packages now exceed 200 lumens per watt under laboratory conditions, while commercially deployed premium modules consistently achieve 170–190 lumens per watt in large-scale installations. Chip-on-board (COB) technology continues to gain traction, delivering up to 30% higher lumen density compared to conventional multi-package SMD configurations. Improved phosphor coatings and flip-chip architectures have reduced forward voltage losses by nearly 8%, enhancing overall module performance stability.

Mini-LED and micro-LED technologies are transforming high-resolution display and automotive adaptive lighting systems. Mini-LED backlighting modules integrate thousands of diodes per panel, enabling local dimming zones exceeding 2,000 segments in advanced displays. In automotive applications, matrix LED modules with more than 80 individually addressable pixels improve visibility range by 25% while reducing glare for oncoming vehicles.

Thermal innovation remains critical, with aluminum nitride substrates and graphene-enhanced heat spreaders reducing junction temperature by up to 12%, thereby extending operational lifespans beyond 60,000 hours. Digital drivers integrated with IoT communication protocols such as Zigbee and DALI-2 are now embedded in over 35% of new commercial LED module installations, supporting adaptive dimming and remote diagnostics. Additionally, human-centric lighting modules offering tunable white ranges from 2,700K to 6,500K are increasingly deployed in office and healthcare environments to enhance occupant well-being and productivity metrics. These technological trends collectively reinforce performance reliability, digital interoperability, and long-term cost efficiency across the LED Module Market.

• In March 2024, Signify launched its Philips UltraEfficient LED tubes and luminaires delivering up to 210 lumens per watt and designed with a lifetime of 100,000 hours, targeting a 50% reduction in energy consumption compared to conventional LED products. Source: www.signify.com

• In May 2024, ams OSRAM introduced its new OSLON® Black Flat X LED for automotive adaptive driving beam systems, offering 10% higher brightness and improved thermal resistance for matrix headlamp modules. Source: www.ams-osram.com

• In January 2025, Samsung Electronics unveiled its next-generation mini-LED backlight technology for premium displays, integrating over 20,000 mini-LEDs per TV panel to enhance contrast performance and achieve peak brightness exceeding 2,000 nits.

• In February 2025, Nichia Corporation announced the commercialization of a high-power 219F LED series achieving luminous efficacy above 200 lumens per watt for industrial lighting modules, supporting extended lifespan beyond 60,000 hours.

The LED Module Market Report provides a comprehensive evaluation of product types, applications, end-user industries, technological advancements, and regional dynamics shaping global demand. The scope covers major product categories including SMD, COB, high-power, mini-LED, and specialty ultraviolet and infrared modules, collectively representing over 90% of deployed lighting components in commercial and industrial installations. Application coverage spans general lighting, automotive lighting, display backlighting, horticulture, industrial machinery, and smart city infrastructure, reflecting diversified usage across more than 15 core industry verticals.

Geographic analysis includes North America, Europe, Asia-Pacific, South America, and Middle East & Africa, with country-level insights into more than 20 high-demand markets such as China, the United States, Germany, Japan, India, and Brazil. The report evaluates infrastructure modernization programs covering over 300 million global streetlight units and commercial retrofits exceeding 75% LED penetration in new constructions across developed economies.

Technology assessment encompasses advancements in chip-scale packaging, high-density COB integration, IoT-enabled smart drivers, tunable white modules, and mini-LED display architectures incorporating thousands of diodes per panel. The scope further includes evaluation of regulatory compliance standards such as minimum luminous efficacy thresholds above 120 lumens per watt and environmental directives targeting 30% energy reduction in public lighting systems.

Additionally, the report addresses competitive benchmarking of over 100 active manufacturers, supply chain structures, semiconductor material trends, and ESG-focused procurement strategies influencing investment decisions. Emerging niche segments, including horticulture LED modules with spectrum customization and UV disinfection modules for healthcare facilities, are also analyzed to provide a holistic industry outlook tailored for executive-level planning and strategic decision-making.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

4.7% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Signify, Osram, Samsung Electronics, Nichia Corporation, Cree LED, Lumileds, Seoul Semiconductor, Everlight Electronics, Toyoda Gosei, LG Innotek, Stanley Electric |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |