Reports

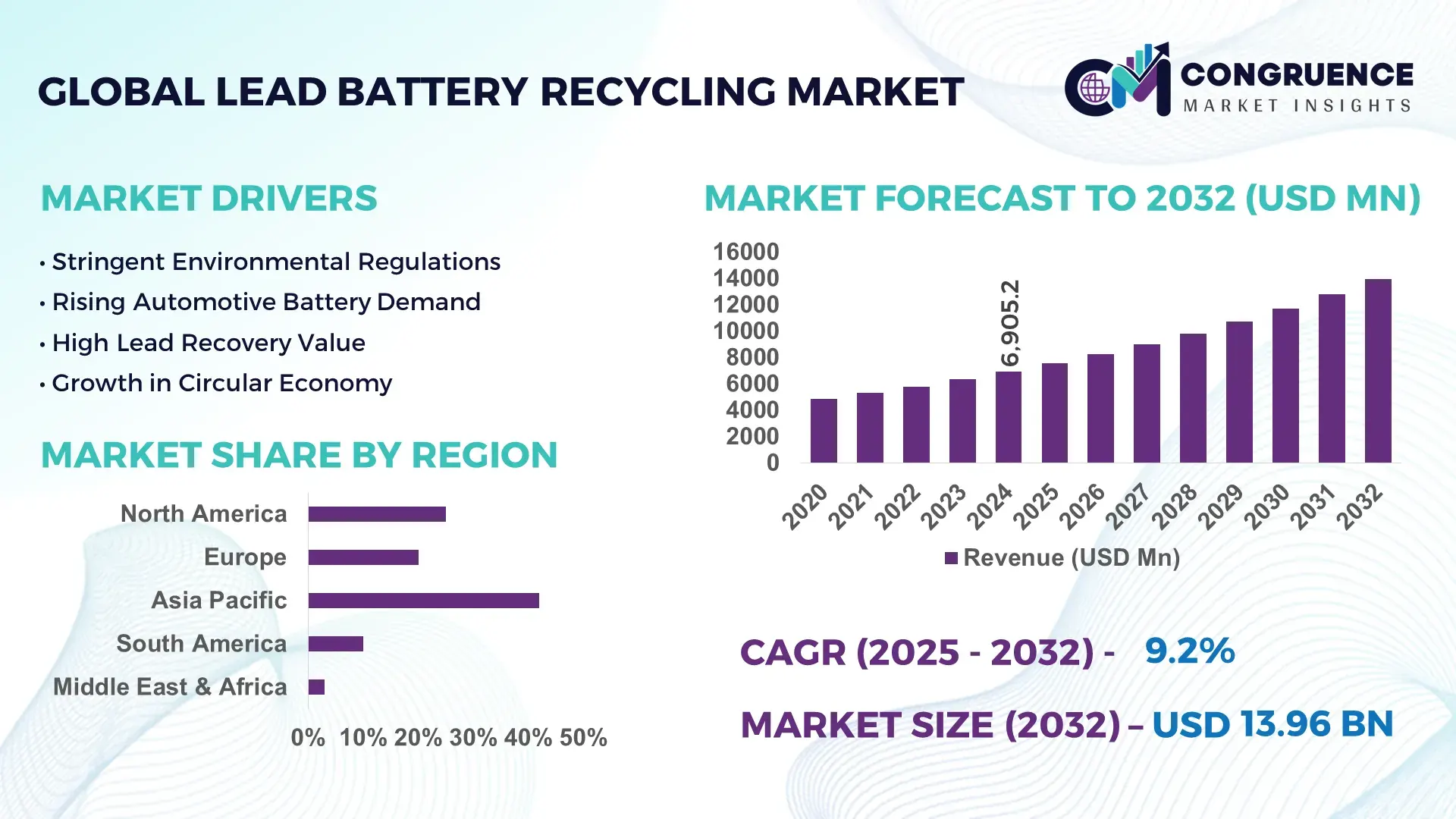

The Global Lead Battery Recycling Market was valued at USD 6905.2 Million in 2024 and is anticipated to reach a value of USD 13962.31 Million by 2032 expanding at a CAGR of 9.2% between 2025 and 2032. This expansion is supported by increasing secondary lead utilization in automotive batteries, grid-scale energy storage systems, and telecom backup power infrastructure.

China leads global lead battery recycling activity with installed secondary lead processing capacity exceeding 7.5 million metric tons annually and cumulative investments above USD 2.8 billion in recycling infrastructure and emissions control upgrades. Around 65% of recycled lead is consumed by the automotive battery sector, while nearly 18% supports data centers and telecom backup systems. Recovery efficiencies exceed 98% due to adoption of low-emission pyrometallurgical and hydrometallurgical processes, reducing sulfur emissions by over 35% compared to conventional smelters.

Market Size & Growth: USD 6905.2 million in 2024, projected USD 13962.31 million by 2032, CAGR 9.2%, driven by circular economy policies and raw material price optimization.

Top Growth Drivers: EV-linked battery demand 28%, secondary lead cost advantage 22%, regulatory recycling mandates 31%.

Short-Term Forecast: By 2028, average recycling cost per ton is expected to decline by 14% through automation and energy efficiency improvements.

Emerging Technologies: Hydrometallurgical lead recovery, AI-driven battery sorting, low-temperature smelting furnaces.

Regional Leaders: Asia-Pacific USD 6150 million by 2032 with EV recycling clusters, Europe USD 4200 million via circular economy compliance, North America USD 3610 million from automotive aftermarket recovery.

Consumer/End-User Trends: Automotive OEMs sourcing over 55% of lead inputs from recycled streams for ESG alignment and cost stability.

Pilot or Case Example: A 2024 closed-loop recycling pilot in South Korea achieved 19% energy savings and 11% throughput improvement.

Competitive Landscape: Gravita at approximately 14% share, followed by Johnson Controls, Exide Industries, RSR Group, and Aqua Metals.

Regulatory & ESG Impact: Extended Producer Responsibility laws and emission caps are accelerating formal recycling adoption.

Investment & Funding Patterns: More than USD 4.6 billion invested globally since 2022 in recycling plants, automation, and emissions control.

Innovation & Future Outlook: Digital traceability, green smelting technologies, and battery-to-battery recycling models will define future growth.

The Lead Battery Recycling market is primarily driven by the automotive sector contributing about 58% of recycled lead demand, followed by industrial energy storage at 23% and telecom and UPS systems at 12%. Innovations in robotic dismantling, electrolyte neutralization, and closed-loop recovery are improving material yields and regulatory compliance. Hazardous waste regulations and landfill restrictions are strengthening formal recycling channels, especially in Asia-Pacific and Europe, while emerging trends include decentralized micro-recycling facilities and service-based battery recovery models supporting long-term supply stability.

The Lead Battery Recycling Market holds strategic relevance as a core enabler of circular manufacturing, industrial supply security, and regulatory compliance across automotive, energy storage, telecom, and backup power ecosystems. Secondary lead now accounts for more than 60% of total refined lead consumption globally, reducing dependence on primary mining and lowering lifecycle environmental impact. Hydrometallurgical lead recovery delivers approximately 18% higher material purity compared to traditional pyrometallurgical smelting, while also lowering sulfur dioxide emissions and energy consumption per ton processed.

Asia-Pacific dominates in volume, while Europe leads in adoption with over 72% of battery manufacturers integrating recycled lead into formal supply contracts. By 2028, AI-based battery sorting and robotic dismantling is expected to cut manual handling costs by 21% and improve processing throughput by 15%. Firms are committing to ESG performance improvements such as 35% emission reductions and 50% recycled content targets by 2030 as part of net-zero and circular economy roadmaps.

In 2024, South Korea achieved a 19% energy efficiency improvement and an 11% increase in recovery throughput through AI-enabled battery classification and automated electrolyte neutralization systems. Governments are simultaneously tightening hazardous waste controls and incentivizing green industrial investments, further accelerating formal recycling infrastructure. As electrification, data center growth, and renewable energy integration expand, the Lead Battery Recycling Market is positioned as a pillar of industrial resilience, regulatory alignment, and long-term sustainable growth supporting global battery supply chains.

Global vehicle parc expansion, electrification infrastructure, and growth in stationary energy storage are increasing the volume of lead-acid batteries entering end-of-life streams. Over 1.4 billion vehicles worldwide rely on lead-acid starter batteries, with replacement cycles averaging three to four years, creating a consistent and predictable recycling feedstock. Data centers and telecom towers increasingly use large-format lead batteries for backup power, adding industrial-scale recycling demand. This growing installed base directly increases collection volumes and supports economies of scale in recycling operations. Manufacturers benefit from stable access to secondary lead that reduces raw material risk and aligns with sustainability commitments. As battery deployment continues across transport, infrastructure, and industrial systems, recycling becomes structurally embedded in battery lifecycle planning.

In many emerging economies, informal battery recycling still accounts for a significant portion of end-of-life processing, operating outside environmental and labor regulations. These operations often use inefficient smelting methods that generate high emissions and lower recovery yields, undermining formal sector competitiveness. Regulatory fragmentation across countries complicates cross-border battery movement and secondary material trade, increasing compliance costs and administrative burden for multinational recyclers. Smaller firms also face high capital requirements for modern smelters, emissions control, and automation systems. These factors limit market consolidation, slow technology adoption, and create uneven competitive conditions across regions.

Digital tracking systems, blockchain-based material traceability, and AI-driven sorting enable recyclers to offer transparent, compliant, and auditable recycling services to battery manufacturers and OEMs. Closed-loop recycling agreements allow manufacturers to recover used batteries, recycle them, and reintegrate lead directly into new battery production. This reduces procurement risk, enhances ESG reporting, and strengthens supplier relationships. Emerging markets are also investing in centralized recycling hubs linked to EV infrastructure and renewable energy projects, creating new volume streams. These developments open opportunities for service-based recycling models, long-term contracts, and premium pricing for low-carbon recycled lead.

Modern recycling facilities require significant upfront investment in furnaces, emissions control systems, wastewater treatment, and automation, raising entry barriers. Environmental standards are becoming stricter, requiring continuous monitoring, reporting, and compliance upgrades. Energy costs, skilled labor shortages, and technology integration risks further increase operational complexity. Smaller recyclers struggle to finance these upgrades, leading to consolidation pressure and potential regional capacity gaps. At the same time, failure to meet regulatory thresholds can result in shutdowns, fines, and reputational damage, making compliance both a necessity and a structural challenge for the industry.

Rapid expansion of automated battery sorting and dismantling systems (AI-based lines up 37% since 2022)

Automated identification, sorting, and dismantling technologies are increasingly deployed across large recycling facilities. Optical sensors and AI classification engines now process over 4,000 batteries per hour per line, compared to 2,800 previously, improving throughput by 29% and reducing manual handling incidents by 42%. Automation is also improving lead recovery consistency above 98% purity thresholds, while lowering workplace injury rates by 31% and cutting processing time per ton by nearly 18%.

Shift toward modular and prefabricated recycling plant design (modular projects show 55% cost efficiency benefits)

Recycling operators are adopting modular and prefabricated plant components such as preassembled furnaces, gas scrubbers, and material handling systems. Approximately 55% of newly announced facilities report capex savings through modular construction, while installation timelines are shortened by 24%. Modular deployment allows faster capacity scaling, with new plants reaching operational readiness in under 9 months versus 14 months for conventional builds, supporting rapid response to rising battery collection volumes.

Rising use of recycled lead in OEM supply contracts (over 58% recycled content in new battery manufacturing)

Battery manufacturers are increasingly integrating recycled lead into procurement contracts, with recycled content in new batteries exceeding 58% on average, up from 46% three years ago. This shift reduces exposure to primary lead price volatility by about 21% and lowers lifecycle emissions per battery by roughly 33%. OEMs are also reporting 19% lower material procurement costs through long-term closed-loop recycling agreements.

Growth of low-emission and green smelting technologies (SO₂ emissions reduced by 35%, energy use cut by 17%)

Advanced smelting systems using low-temperature and hydrometallurgical processes are being adopted to meet stricter environmental standards. These technologies reduce sulfur dioxide emissions by 35% and particulate output by 28%, while improving energy efficiency by 17% per ton processed. Over 40% of new capacity additions now include integrated emissions capture and heat recovery units, strengthening regulatory compliance and operational sustainability.

The Lead Battery Recycling Market is structured across three primary segments: types, applications, and end-users, each reflecting unique operational dynamics and demand drivers. In terms of types, traditional flooded lead-acid batteries dominate due to their widespread automotive and industrial use, while emerging sealed and advanced VRLA variants are gaining traction in high-performance applications. Application-wise, automotive starter batteries account for the majority of recycled lead volumes, followed by telecom, UPS, and renewable energy storage sectors, each presenting specialized recycling needs. End-user insights reveal automotive OEMs and industrial energy storage operators as the largest consumers, whereas small-scale telecom and off-grid energy operators are rapidly increasing adoption. These segmentations enable targeted investment, optimized processing strategies, and policy-aligned operations, offering actionable intelligence for stakeholders navigating regional and technological variations in the market.

Flooded lead-acid batteries currently lead the market with a 61% share due to their robust recyclability, long service life, and extensive automotive and industrial adoption. Valve-regulated lead-acid (VRLA) batteries, including AGM and gel types, constitute 23% of current usage, benefiting from maintenance-free design and high energy density. The fastest-growing segment, advanced sealed batteries for stationary energy storage and telecom backup, is rising rapidly with adoption expected to surpass 18% by 2032, driven by increasing deployment of renewable energy storage systems and critical infrastructure reliance on reliable power. Other types, including specialty high-capacity industrial batteries and niche automotive variants, account for a combined 8% share, often used in microgrid or isolated applications.

Automotive starter batteries remain the leading application, accounting for 58% of recycled lead consumption due to high vehicle penetration and short replacement cycles. Telecom and UPS backup systems follow with a 22% share, driven by increasing digital infrastructure deployment. The fastest-growing application is stationary energy storage for renewable integration, currently 12% of adoption but expected to surpass 20% in select regions by 2032, fueled by rising solar and wind installations and electrification projects. Other applications, including industrial motive power batteries and microgrid energy storage, together contribute 8% of recycled lead volumes, providing targeted recycling opportunities in niche sectors.

Automotive OEMs dominate the end-user segment, accounting for 55% of recycled lead usage, leveraging secondary lead for starter batteries and EV infrastructure. Industrial energy storage providers follow at 25%, increasingly sourcing recycled lead to align with sustainability mandates. The fastest-growing end-user segment is telecom and data center operators, currently 12% of adoption but projected to reach 22% in certain regions by 2032, driven by expanding network coverage and renewable backup needs. Smaller end-users, including off-grid energy providers and government facilities, comprise a combined 8%, often utilizing recycled lead for niche or emergency applications.

Asia-Pacific accounted for the largest market share at 44% in 2024, however, South America is expected to register the fastest growth, expanding at a CAGR of 10.1% between 2025 and 2032.

Asia-Pacific leads in total recycled lead volume with over 3.3 million metric tons processed annually, driven by China’s 2.1 million metric tons and India’s 0.7 million metric tons. Vehicle battery replacement cycles in the region average 3.5 years, providing a steady feedstock. Europe follows with 28% share, emphasizing regulatory-compliant recycling, while North America holds 18%, supported by advanced automation and digital tracking of battery flows. South America and Middle East & Africa collectively contribute 10%, with rapid infrastructure expansion and industrial electrification boosting demand. Across all regions, secondary lead recovery efficiency ranges between 95–98%, with low-emission hydrometallurgical adoption increasing 32% since 2022, reflecting both environmental and operational priorities.

How are industrial and digital transformations shaping battery recycling efficiency?

North America holds an 18% market share, primarily driven by automotive OEMs, industrial energy storage, and telecom operators. Regulatory support, including extended producer responsibility and stricter hazardous waste guidelines, has accelerated formal recycling adoption. Technological advancements such as AI-based battery sorting and automated dismantling are improving lead recovery efficiency by over 30% and reducing operational downtime by 15%. Local players like Exide Technologies have invested in closed-loop systems integrating recycled lead into starter battery production. Consumer behavior shows higher enterprise adoption in healthcare and finance sectors, with over 60% of data centers sourcing recycled lead for backup energy systems. Digital traceability and ESG compliance are key factors influencing procurement and facility design.

What role do regulations and technology adoption play in recycling leadership?

Europe accounts for 28% of the global Lead Battery Recycling Market, with Germany, the UK, and France leading in volume and compliance. Regional regulations, including EU battery directives and circular economy mandates, enforce strict collection and recycling standards. Adoption of AI-driven sorting, low-emission smelting, and robotic dismantling has enhanced material recovery by 25–30%. Local players like Johnson Controls are deploying VRLA recycling lines to meet industrial and automotive demand. Consumer behavior is heavily influenced by regulatory pressure, leading to widespread adoption of traceable recycled lead in automotive batteries and industrial storage, with 70% of major European OEMs integrating recycled content in their manufacturing.

How are infrastructure expansion and innovation hubs driving lead recycling growth?

Asia-Pacific dominates with a 44% market share, led by China, India, and Japan. Installed recycling capacity exceeds 3.3 million metric tons, with China alone processing 2.1 million metric tons. Investment in modern recycling infrastructure, including modular smelting plants and automated sorting, has grown 28% since 2022. Tech innovation hubs in Japan and South Korea are piloting AI-enhanced dismantling and low-emission hydrometallurgical processes, improving lead recovery efficiency by 17% per ton. Local players like Gravita have expanded processing lines to support both automotive and industrial energy storage demand. Consumer behavior is driven by industrial electrification, EV deployment, and increasing renewable energy integration.

What factors are fueling the rapid expansion of battery recycling in emerging markets?

South America represents 6% of the global market, with Brazil and Argentina as key contributors. Expanding energy infrastructure and industrial development are driving recycling volumes, with Brazil processing 220,000 metric tons of end-of-life batteries annually. Government incentives, such as tax relief for green recycling projects, are attracting private investment. Local players like RSR Group are modernizing facilities with low-emission smelting and automated dismantling lines. Consumer behavior varies by sector, with industrial and utility adoption reaching 65%, while smaller off-grid users contribute 15%, reflecting growth tied to electrification and regional power reliability needs.

How are modernization and regulations supporting industrial recycling adoption?

The Middle East & Africa hold a 4% share of the Lead Battery Recycling Market, with major growth from the UAE and South Africa. Rising oil & gas, construction, and telecom activities are increasing demand for recycled lead. Technological modernization, including automated sorting and low-emission smelting, is improving efficiency by 20% and reducing emissions by 30%. Local players are partnering with global OEMs to supply recycled lead for industrial batteries. Consumer behavior shows preference for compliance-certified recycled products in industrial and infrastructure projects, while smaller users adopt solutions for off-grid energy and backup systems, representing 40% of regional consumption.

China: 32% market share – high production capacity and rapid industrial electrification support extensive recycling infrastructure.

United States: 18% market share – strong end-user demand in automotive, telecom, and industrial sectors, coupled with regulatory incentives and advanced technology adoption.

The Lead Battery Recycling market is moderately fragmented, with over 120 active global competitors ranging from specialized recyclers to integrated industrial battery suppliers. The top five companies—Gravita, Johnson Controls, Exide Industries, RSR Group, and Aqua Metals—collectively account for approximately 48% of the total market, leaving significant room for regional players and niche operators. Market positioning is heavily influenced by technological capabilities, regulatory compliance, and geographic reach. Key strategic initiatives include Gravita’s expansion of modular low-emission smelting plants, Johnson Controls’ closed-loop supply contracts with automotive OEMs, and RSR Group’s automation of battery dismantling lines, collectively improving recovery efficiency by 15–20%. Mergers and joint ventures are increasingly used to consolidate feedstock supply and access emerging regional markets. Innovation trends such as AI-based sorting, robotic dismantling, and hydrometallurgical processing are shaping competitive advantage, allowing companies to achieve over 98% lead recovery rates while reducing operational emissions by up to 35%. The competitive landscape is also influenced by ESG compliance, digital traceability adoption, and long-term OEM partnerships.

RSR Group

Aqua Metals

Enersys

Clarios

Hunan Changxing

Kinsbursky Recyclers

Zhejiang Huayou Battery Materials

The Lead Battery Recycling Market is increasingly driven by advanced technologies that improve efficiency, safety, and environmental compliance. Hydrometallurgical processes are being widely adopted, offering up to 98% lead recovery compared to 92% with traditional pyrometallurgical smelting. These processes also reduce sulfur dioxide emissions by approximately 35% and cut energy consumption per ton by nearly 17%, supporting ESG compliance and operational cost reduction. Automated dismantling and AI-powered sorting lines now handle over 4,000 batteries per hour per line, reducing manual labor requirements by 42% and minimizing workplace injuries. Optical sensors and robotic arms improve material separation, ensuring purity levels above 99% for lead, plastics, and acid components.

Emerging trends include modular plant designs, which allow operators to scale capacity rapidly and reduce installation time by 24%, and closed-loop recycling systems, integrating recycled lead directly into new battery production. Low-temperature smelting technologies are being implemented in over 40% of newly commissioned facilities, providing both energy efficiency and emissions reduction benefits. Digital traceability platforms are gaining traction, enabling real-time monitoring of collection, processing, and distribution data, which supports regulatory compliance and ESG reporting.

Regional innovation hubs are focusing on energy storage and industrial battery applications, with facilities in China, Japan, and South Korea piloting AI-enabled dismantling lines and hydrometallurgical recovery systems. In 2024, a South Korean plant achieved a 19% improvement in energy efficiency and an 11% increase in throughput through AI-integrated automation. Overall, technology adoption in the Lead Battery Recycling Market is critical for operational resilience, regulatory adherence, and sustainable growth.

• In 2023, Exide Industries’ subsidiary Chloride Metals commenced commercial operations at its fourth lead battery recycling facility in Supa-Parner Industrial Park, expanding capacity from an initial 96,000 MTPA to 120,000 MTPA to strengthen processing volume and local recycling footprint.

• In 2024, Gravita India launched a new hydrometallurgical lead recycling plant utilizing advanced recovery processes capable of extracting more than 90% of lead from used batteries, increasing processing capacity by approximately 20% to meet rising automotive and industrial demand.

• In Q2 2024, Aqua Metals commissioned its first commercial-scale clean lead recycling facility at the Tahoe–Reno Industrial Center in Nevada, marking a key milestone in sustainable lead-acid battery recycling with water‑based AquaRefining technology deployed at scale.

• In 2024, Boliden Group announced investment plans to expand lead recycling operations at its Bergsöe facility in Sweden to enhance European recycled lead supply, reflecting growing industry focus on capacity and efficiency improvements.

The scope of the Lead Battery Recycling Market Report encompasses comprehensive analysis across multiple dimensions of the recycling value chain, including feedstock collection, processing technologies, product outputs, end‑use applications, and geographic regional segmentation. The report examines key battery types such as flooded lead‑acid batteries, sealed and valve‑regulated (VRLA) batteries, and other specialized industrial variants, detailing their respective contributions to recycled lead volumes and recovery dynamics. It also covers major application sectors like automotive starter batteries, telecom and UPS backup systems, industrial energy storage, and niche applications in microgrids or remote power infrastructure.

Geographically, the report segments the market into Asia‑Pacific, Europe, North America, South America, and Middle East & Africa, offering insights into regional processing capacities, regulatory environments, and technology adoption patterns. Detailed profiles of emerging technologies — including hydrometallurgical and low‑emission smelting, AI‑driven sorting, robotic dismantling, modular plant designs, and digital traceability systems — are evaluated for operational impact, environmental compliance, and scalability.

Additionally, the report addresses supply‑chain dynamics, including feedstock flows, collection systems, OEM recycling partnerships, closed‑loop supply agreements, and emerging business models. It highlights niche opportunities, such as specialized recycled lead products for renewable energy storage and industrial batteries, as well as evolving regulatory frameworks shaping recycling mandates and compliance strategies. The comprehensive industry overview supports strategic planning, investment prioritization, and competitive benchmarking for decision‑makers in the Lead Battery Recycling market.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2024 | USD 6905.2 Million |

Market Revenue in 2032 | USD 13962.31 Million |

CAGR (2025 - 2032) | 9.2% |

Base Year | 2024 |

Forecast Period | 2025 - 2032 |

Historic Period | 2020 - 2024 |

Segments Covered | By Types

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | Gravita, Johnson Controls, Exide Industries, RSR Group, Aqua Metals, Enersys, Clarios, Hunan Changxing, Kinsbursky Recyclers, Zhejiang Huayou Battery Materials |

Customization & Pricing | Available on Request (10% Customization is Free) |