Reports

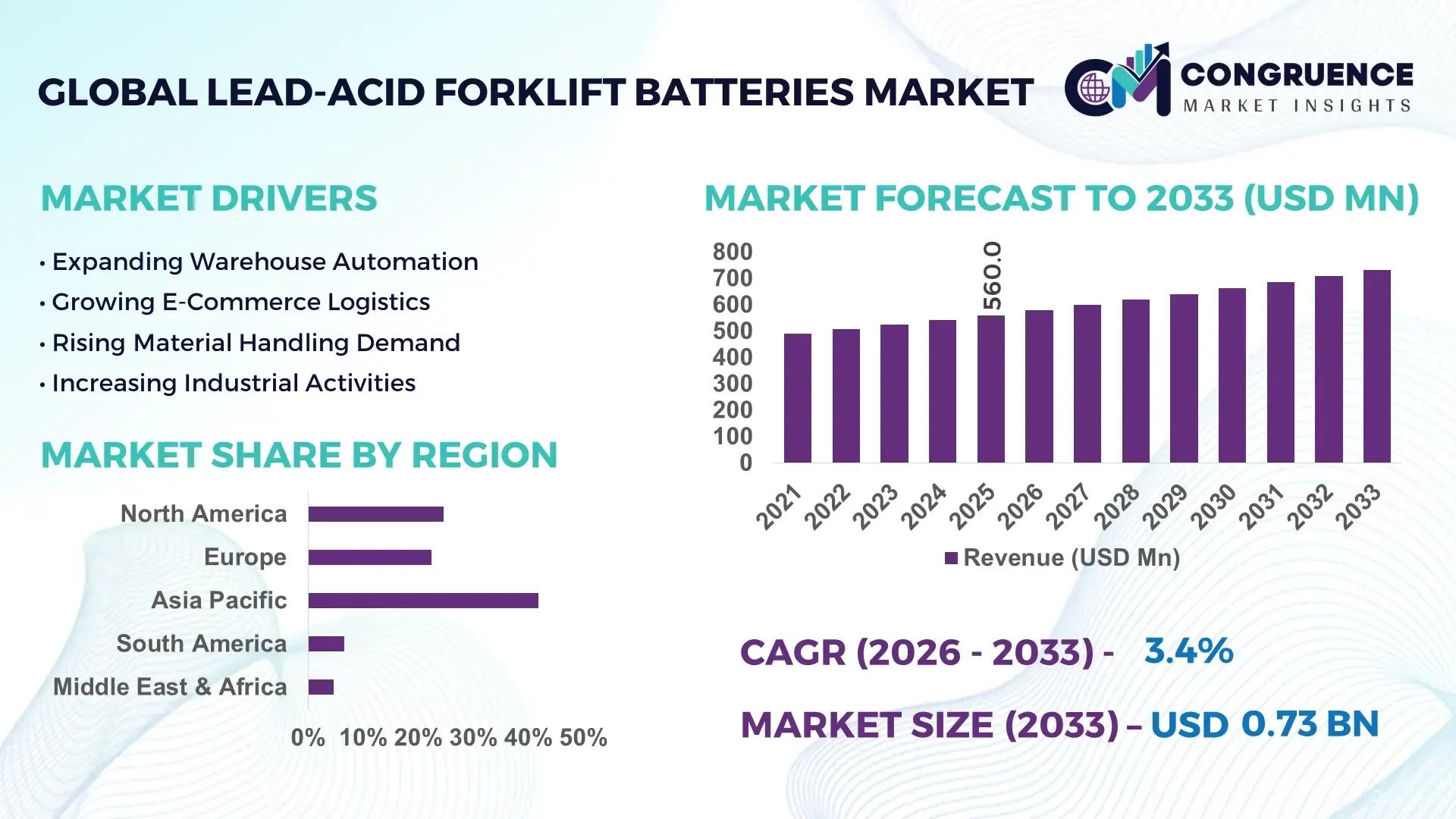

The Global Lead-Acid Forklift Batteries Market was valued at USD 560.0 Million in 2025 and is anticipated to reach a value of USD 731.7 Million by 2033 expanding at a CAGR of 3.4% between 2026 and 2033. Growth is primarily supported by warehouse electrification, rising forklift fleet replacement cycles, and continued deployment of cost-efficient motive power systems across logistics, manufacturing, and distribution facilities.

China remains the dominant country in the market, accounting for approximately 38% of global lead-acid forklift battery production capacity, supported by investments exceeding USD 2 billion across industrial battery manufacturing clusters serving e-commerce, automotive, and export-oriented logistics sectors. China’s electric forklift penetration exceeds 70% of new forklift sales compared with approximately 64% in Germany, while battery recycling rates surpass 90%, strengthening raw-material security amid ongoing global supply-chain realignment and industrial localization initiatives.

The market's strategic significance lies in balancing affordability, recyclability, and operational reliability for high-volume material handling fleets while supporting industrial productivity optimization.

Market Size & Growth: Valued at USD 560.0 Million in 2025 and projected to reach USD 731.7 Million by 2033, supported by a 22% rise in warehouse automation deployments and expanding forklift fleet electrification.

Top Growth Drivers: E-commerce warehouse expansion (+28%), industrial automation adoption (+24%), and battery recycling efficiency above 90% continue strengthening market demand.

Short-Term Forecast: By 2028, battery charging efficiency is expected to improve by 12% while fleet maintenance costs decline by nearly 8% through smart monitoring integration.

Emerging Technologies: IoT-enabled battery diagnostics, predictive maintenance platforms, and advanced lead-carbon battery designs are improving operational uptime by up to 15%.

Regional Leaders: Asia-Pacific exceeds USD 250 Million, Europe approaches USD 160 Million, and North America surpasses USD 130 Million, driven by logistics modernization and warehouse expansion.

Consumer/End-User Trends: More than 68% of industrial warehouses continue utilizing lead-acid systems due to lower acquisition costs and established charging infrastructure.

Pilot/Case Example: In 2024, a large logistics fleet modernization project reduced battery downtime by 18% through centralized charging and monitoring systems.

Competitive Landscape: East Penn Manufacturing holds an estimated 12% share alongside EnerSys, Exide Technologies, GS Yuasa, Crown Battery, and Hoppecke.

Regulatory & ESG Impact: Battery recycling rates above 90% support circular-economy targets, while industrial sustainability programs have reduced waste generation by approximately 14%.

Investment & Funding: More than USD 1.5 Billion has been directed toward battery manufacturing expansion, recycling facilities, and supply-chain localization initiatives.

Innovation & Future Outlook: Smart battery management systems and lead-carbon technologies are extending cycle life by 20% while supporting advanced warehouse operations.

Lead-Acid Forklift Batteries remain a critical power source for warehousing, manufacturing, ports, and distribution centers due to proven reliability and extensive recycling infrastructure. Recent innovations include IoT-enabled battery monitoring, fast-charging technologies, and enhanced lead-carbon formulations that improve cycle performance by nearly 20%. Growing supply-chain localization efforts and stricter industrial sustainability targets are accelerating investment in high-efficiency battery ecosystems, creating a strong foundation for strategic market evolution.

The Lead-Acid Forklift Batteries Market is becoming increasingly important as industrial operators prioritize cost-efficient fleet electrification, supply-chain resilience, and warehouse productivity. Rising investments in distribution centers, manufacturing automation, and logistics infrastructure are expanding the installed base of electric forklifts worldwide. Simultaneously, supply-chain restructuring following global trade disruptions has encouraged localized battery manufacturing and recycling networks, improving material availability and operational security.

Technology improvements are enhancing the competitive position of modern lead-acid systems. Advanced lead-carbon batteries deliver up to 18% longer cycle life and approximately 10% lower maintenance requirements compared with conventional flooded lead-acid designs. China and Germany continue leading large-scale deployment through dense manufacturing ecosystems and strong industrial automation adoption, while emerging markets such as India and Vietnam are expanding forklift electrification across logistics and industrial corridors. Over the next two to three years, smart battery monitoring adoption is expected to exceed 35% among large warehouse operators seeking higher fleet utilization rates.

A practical example can be seen in logistics operators deploying centralized charging infrastructure integrated with battery analytics platforms, reducing downtime and improving asset utilization. Companies are responding through recycling investments, strategic partnerships, and localized production expansion. Organizations that strengthen battery lifecycle management, operational efficiency, and supply-chain integration will secure a durable competitive advantage in the evolving material handling ecosystem.

Warehouse electrification is accelerating demand for lead-acid forklift batteries as logistics operators scale fleet utilization and distribution capacity. Electric forklifts now account for more than 65% of new forklift deployments across major industrial economies, while e-commerce warehouse footprints have expanded by over 25% during the past five years. The ongoing shift toward automated fulfillment facilities is increasing battery cycling frequency and replacement requirements. Industrial operators continue favoring lead-acid systems because acquisition costs remain approximately 30–40% lower than comparable lithium-ion alternatives. In response, manufacturers are expanding production facilities, strengthening recycling partnerships, and integrating digital battery diagnostics. A notable strategic insight is that battery recyclability exceeding 90% provides a stable secondary raw-material stream, reducing procurement volatility while supporting long-term fleet operating economics.

Lead price fluctuations and charging infrastructure constraints continue limiting deployment flexibility. Battery-grade lead costs have experienced periodic swings exceeding 15% in recent years, directly affecting manufacturing margins and procurement planning. Many industrial facilities still require dedicated charging rooms, creating infrastructure costs that can account for nearly 10% of warehouse electrical investments. In countries heavily dependent on imported industrial materials, supply disruptions can extend battery procurement lead times by more than 20%. These pressures affect operational scalability and replacement planning. To mitigate risks, manufacturers are diversifying supplier networks, increasing recycled lead utilization, and localizing component sourcing. An important operational insight is that facilities with mature recycling ecosystems maintain stronger cost stability than markets dependent on imported raw-material supply chains.

The integration of smart battery management technologies presents a significant opportunity across industrial logistics networks. IoT-enabled monitoring platforms can reduce unplanned battery failures by approximately 20% while improving charging efficiency by nearly 12%. India’s industrial corridor developments and Southeast Asia’s manufacturing expansion are creating new deployment opportunities as warehouse construction activity continues rising. Battery analytics platforms, predictive maintenance software, and lead-carbon chemistry improvements are enhancing fleet productivity without requiring full infrastructure replacement. Companies are positioning themselves through R&D investments, software partnerships, and service-based battery lifecycle management programs. A less obvious opportunity lies in combining advanced monitoring with recycling data to optimize battery replacement schedules, generating measurable cost savings and stronger operational continuity for high-utilization forklift fleets.

As warehouses become increasingly automated, maintaining consistent battery performance across intensive operating cycles is emerging as a major challenge. Large fulfillment centers frequently operate 16–24 hours daily, placing sustained stress on battery assets and increasing maintenance complexity. Studies indicate that improper charging practices can reduce effective battery life by more than 25%, while equipment downtime can lower warehouse productivity by nearly 8%. Automated facilities also demand tighter integration between battery monitoring systems, fleet management software, and operational planning tools. Companies must address these issues through workforce training, intelligent charging infrastructure, and digital asset-management platforms. A key strategic challenge is ensuring that battery performance remains predictable across expanding multi-site operations where uptime, consistency, and lifecycle optimization directly influence competitiveness.

Smart Fleet Monitoring Expansion – Industrial operators are integrating battery telemetry and predictive maintenance platforms across forklift fleets, with smart monitoring adoption increasing by approximately 32% over the past two years. Real-time state-of-charge visibility has reduced unplanned battery-related downtime by nearly 18% while improving asset utilization rates by 12%. Labor shortages in warehouse operations are accelerating deployment of automated battery diagnostics. Manufacturers are responding through software partnerships, connected charging infrastructure, and digital fleet-management integration that supports higher throughput and maintenance efficiency.

Recycling-Centered Supply Strategies – Battery producers are restructuring procurement models around recycled lead streams, with secondary lead now contributing more than 55% of raw-material requirements in several mature industrial markets. Recycling efficiency above 90% is reducing exposure to commodity volatility while shortening material sourcing cycles by approximately 15%. Supply-chain resilience concerns following recent trade disruptions have accelerated localized recycling investments. Companies are expanding closed-loop collection programs and strengthening recycler partnerships to improve cost predictability and material security.

Lead-Carbon Technology Adoption – Advanced lead-carbon battery systems are gaining traction in high-cycle warehouse environments, delivering up to 20% longer service life and approximately 15% better charge acceptance than conventional flooded batteries. Distribution centers operating multi-shift schedules are increasingly adopting these systems to reduce maintenance interruptions and improve equipment availability. Battery manufacturers are prioritizing product portfolio upgrades, targeted industrial deployments, and performance-focused partnerships to capture replacement demand from large logistics operators.

Localized Manufacturing Networks – Industrial battery suppliers are expanding domestic production capabilities as enterprises seek greater supply continuity and shorter delivery timelines. Localized sourcing initiatives have reduced procurement lead times by nearly 20% in several manufacturing hubs, while regional production capacity additions have increased operational flexibility. Industrial policy support and infrastructure modernization programs are reinforcing this shift. Companies are investing in production expansion, supplier diversification, and vertically integrated operations to strengthen competitiveness and improve responsiveness to industrial fleet requirements.

Flooded Lead-Acid Batteries remain the leading segment, accounting for an estimated 48% of market demand due to their proven reliability, lower acquisition costs, and compatibility with large industrial forklift fleets. Major warehouse operators and manufacturing facilities continue to deploy flooded systems because they offer predictable performance under heavy-duty operating conditions while benefiting from established maintenance and charging infrastructure. Their extensive recycling ecosystem further strengthens lifecycle economics, with lead recovery rates exceeding 90% in mature markets. Manufacturers continue supporting this segment through service-network expansion, battery refurbishment programs, and productivity-focused charging solutions. Lead-Carbon Batteries represent the fastest-growing segment as industrial operators seek higher cycle durability and improved charge acceptance without transitioning fully to lithium-ion systems. Lead-carbon deployments have increased by nearly 18% across high-utilization logistics facilities, where multi-shift operations require greater operational flexibility. Sealed Lead-Acid (SLA) batteries continue gaining traction in facilities prioritizing reduced maintenance requirements, while AGM batteries remain strategically important in specialized indoor applications requiring enhanced safety and vibration resistance. Companies are increasing investments in advanced plate technologies, smart battery monitoring, and performance optimization to strengthen differentiation and address evolving warehouse productivity requirements.

Warehousing & Distribution Centers constitute the largest application segment, representing approximately 42% of battery demand. Rapid expansion of fulfillment networks, automated storage systems, and inventory-intensive logistics operations has significantly increased forklift utilization rates. Facilities increasingly operate extended shifts, creating sustained demand for dependable battery replacement cycles and charging infrastructure. Operators are integrating centralized charging systems and battery analytics platforms to improve uptime while reducing maintenance disruptions. Demand remains particularly strong among large third-party logistics providers managing high-volume inventory movements. Retail & E-Commerce Logistics is emerging as the fastest-growing application segment, supported by continued growth in omnichannel fulfillment and same-day delivery models. Forklift utilization within e-commerce facilities has increased by nearly 20% over recent years as operators expand distribution footprints. Manufacturing Facilities remain a mature yet stable application area where batteries support continuous production workflows, while Ports & Freight Terminals are increasingly modernizing equipment fleets to improve cargo-handling efficiency. Companies are responding through application-specific battery designs, expanded service support, and integrated fleet-management solutions that align battery performance with operational productivity objectives.

Logistics & Transportation represents the dominant end-user segment, accounting for an estimated 38% of market demand due to extensive forklift deployment across warehouses, cross-docking centers, and freight-handling facilities. The segment benefits from high equipment utilization rates and frequent battery replacement requirements driven by intensive operating schedules. Many large logistics providers manage fleets exceeding several hundred electric forklifts, creating recurring demand for battery procurement, maintenance, and recycling services. Suppliers are strengthening customer relationships through lifecycle service contracts, fleet analytics, and infrastructure support offerings. Retail & E-Commerce is the fastest-growing end-user category as fulfillment networks continue expanding to support faster delivery expectations and inventory decentralization. Battery demand within this segment has increased by approximately 17% as operators invest in automated distribution centers and material-handling equipment. Manufacturing Industry remains a significant consumer due to production-line logistics requirements, while Automotive & Industrial Equipment companies continue deploying electric forklifts to improve operational efficiency and workplace sustainability objectives. Manufacturers are increasingly tailoring pricing strategies, maintenance programs, and battery-performance packages to address the specific operational priorities of each customer group.

Asia-Pacific accounted for the largest market share at 41.8% in 2025 however, Middle East & Africa is expected to register the fastest growth, expanding at a CAGR of 4.3% between 2026 and 2033.

North America represents approximately 24.6% of global market activity, supported by extensive warehouse automation, mature logistics networks, and a large installed base of electric forklifts. The region continues to generate strong replacement demand as distribution centers prioritize operational continuity and lifecycle cost management. More than 65% of forklift fleets within large logistics facilities continue utilizing lead-acid battery platforms due to established charging infrastructure and recycling ecosystems. Major operators are increasingly integrating battery telemetry and centralized charging management systems, improving fleet availability by nearly 15%. Investments in regional manufacturing and battery recycling capacity are also strengthening supply-chain resilience and reducing procurement volatility.

United States Market Outlook: The United States remains the region’s primary demand center due to its extensive warehousing footprint, advanced logistics sector, and high concentration of distribution hubs. E-commerce fulfillment facilities continue expanding across Texas, California, and Ohio, supporting sustained forklift deployment. More than 70% of electric forklifts operating in large-scale warehouse environments rely on lead-acid systems. Domestic battery manufacturers are strengthening recycling partnerships and service networks while industrial operators increasingly adopt battery monitoring technologies to optimize utilization rates and maintenance planning.

Europe accounts for approximately 22.4% of global demand, supported by advanced manufacturing, strong industrial automation adoption, and well-established environmental compliance frameworks. Battery recycling infrastructure remains a significant competitive advantage, with recovery rates exceeding 90% across several industrial markets. Manufacturers are modernizing production processes while logistics operators continue upgrading electric forklift fleets to support warehouse efficiency targets. Industrial facilities are increasingly implementing digital battery monitoring systems, reducing maintenance-related interruptions by approximately 12%. Sustainability-driven procurement policies and equipment modernization initiatives continue supporting stable battery replacement demand across manufacturing and logistics sectors.

Germany Market Outlook: Germany serves as the region's strategic anchor through its automotive manufacturing base, industrial automation leadership, and advanced logistics infrastructure. Electric forklifts account for more than 60% of industrial truck deployments within major manufacturing facilities. The country's dense network of distribution centers and export-oriented industries creates consistent battery replacement demand. German enterprises are prioritizing intelligent fleet management platforms, predictive maintenance systems, and energy-efficient charging operations to improve equipment availability and operational productivity.

Asia-Pacific remains the largest regional market, contributing approximately 41.8% of global demand. The region benefits from extensive battery manufacturing capacity, rapidly expanding warehouse infrastructure, and strong industrial output across multiple countries. Rising adoption of electric forklifts in manufacturing clusters and e-commerce logistics facilities continues driving battery deployment. Battery production capacity has expanded by more than 20% across key industrial hubs over the past several years, strengthening supply availability. Local manufacturers are increasing investments in recycling operations, lead-carbon technologies, and production automation to improve competitiveness while supporting growing domestic and export demand.

China Market Outlook: China dominates global lead-acid forklift battery production and consumption through its large-scale industrial ecosystem and extensive logistics infrastructure. The country accounts for roughly 38% of global production capacity and maintains electric forklift penetration exceeding 70% of new industrial truck sales. Strong domestic manufacturing, integrated supply chains, and advanced recycling capabilities provide significant operational advantages. Chinese battery producers continue expanding automated production lines and enhancing battery performance technologies to maintain leadership in both domestic and international markets.

South America accounts for approximately 6.5% of global market demand, supported by expanding warehouse capacity, agricultural logistics modernization, and industrial material-handling requirements. Adoption remains concentrated within manufacturing, food processing, and export-oriented logistics operations. Infrastructure development programs and distribution network expansion are increasing forklift utilization across major industrial corridors. However, uneven charging infrastructure availability and periodic economic fluctuations continue affecting deployment speed. Companies are addressing these challenges through localized service networks, strategic distributor partnerships, and targeted investments in battery maintenance support to improve operational reliability and fleet performance.

Brazil Market Outlook: Brazil represents the largest market within South America due to its manufacturing scale, agricultural exports, and expanding logistics sector. Distribution centers supporting consumer goods, food processing, and retail operations continue increasing forklift fleet sizes. Industrial operators are prioritizing cost-efficient battery solutions capable of supporting intensive daily operations. Battery replacement demand remains strong as warehouse modernization initiatives accelerate around São Paulo and other industrial centers. Manufacturers are expanding local distribution capabilities and aftermarket service programs to strengthen customer retention and operational support.

Middle East & Africa contributes approximately 4.7% of global market demand but is emerging as the fastest-developing regional opportunity. Large-scale logistics projects, industrial diversification programs, and port modernization initiatives are increasing electric forklift deployment across warehousing and cargo-handling operations. Investments in logistics infrastructure have expanded materially across Gulf economies, improving demand for industrial battery systems. Free-trade zones and industrial parks are creating new deployment environments for material-handling equipment. Suppliers are strengthening regional partnerships, expanding technical service capabilities, and establishing localized distribution channels to support growing operational requirements.

Saudi Arabia Market Outlook: Saudi Arabia is the most strategically significant market within the region due to ongoing industrial diversification, logistics corridor development, and major infrastructure investments. Warehousing and distribution capacity continues expanding under national economic transformation initiatives, increasing demand for electric material-handling equipment. Industrial cities and logistics hubs are adopting advanced warehouse operations to improve efficiency and throughput. Equipment suppliers are establishing partnerships with local distributors and service providers while battery manufacturers target long-term opportunities linked to industrial expansion and supply-chain modernization projects.

The market is led by global battery specialists such as EnerSys, East Penn Manufacturing, GS Yuasa Corporation, Exide Industries, and Hoppecke, which collectively control approximately 48–52% of global demand. Competition primarily occurs between global technology leaders and regional cost-focused suppliers serving local forklift fleets. Price remains critical, but battery lifecycle performance, charging efficiency, and recycling capabilities increasingly influence purchasing decisions. Advanced lead-carbon and maintenance-free solutions can improve cycle life by 15–20%, while digital battery monitoring reduces downtime by nearly 18%, creating differentiation beyond acquisition cost. Companies are competing through manufacturing expansion, recycling integration, aftermarket service contracts, and fleet-management partnerships. Vertical integration strategies are strengthening control over lead supply and battery recovery networks where recycling rates exceed 90%. The competitive shift is moving from pure battery sales toward lifecycle management and operational services. High recycling infrastructure requirements and established distribution networks remain significant entry barriers. Winning requires superior service coverage, battery reliability, recycling capabilities, and fleet productivity optimization.

East Penn Manufacturing

Exide Industries Limited

Hoppecke Batterien GmbH & Co. KG

Crown Battery Manufacturing Company

Stryten Energy

Amara Raja Energy & Mobility Limited

Trojan Battery Company

Midac Batteries S.p.A.

TAB Batteries

Discover Battery

Sunlight Group

Leoch International Technology Limited

Lead-acid forklift battery technology is evolving from conventional flooded systems toward intelligent, performance-optimized energy platforms. Flooded batteries still dominate industrial deployments, accounting for more than 60% of installed forklift battery assets due to cost advantages and extensive service infrastructure. However, maintenance-free valve-regulated lead-acid (VRLA) and absorbent glass mat (AGM) technologies are gaining traction in high-utilization facilities where maintenance reduction and operational consistency are priorities. Advanced battery monitoring systems now improve fleet utilization by approximately 12% while reducing unexpected failures by nearly 18%.

The most significant emerging trend is the adoption of lead-carbon battery technology. Compared with traditional flooded batteries, lead-carbon designs deliver up to 20% longer cycle life and approximately 15% faster charge acceptance under intensive operating conditions. Smart battery management systems integrated with warehouse management platforms are being deployed across nearly 35% of large logistics facilities. These technologies enable predictive maintenance, charging optimization, and improved battery lifecycle planning. Logistics operators and third-party warehouse providers benefit most from these operational efficiencies.

Between 2026 and 2028, connected battery ecosystems, AI-assisted maintenance analytics, and advanced charging infrastructure will become key competitive differentiators. Manufacturers investing in digital diagnostics, lead-carbon innovation, and automated battery monitoring platforms will secure stronger fleet performance, lower operating costs, and greater customer retention as industrial operators increasingly prioritize uptime and asset productivity.

April 2025 – EnerSys announced a strategic manufacturing restructuring, transferring flooded lead-acid battery production from Monterrey, Mexico, to Richmond, Kentucky. The initiative includes approximately USD 20 million in restructuring actions, strengthening production efficiency and supply-chain responsiveness for industrial battery customers.

May 2025 – EnerSys completed a 34,000-square-foot expansion of its Sumter facility through a USD 6.7 million investment. The expansion increases manufacturing capacity for industrial battery technologies and reinforces domestic supply-chain resilience supporting motive power applications. Source: www.enersys.com.cn

April 2025 – GS Yuasa showcased advanced industrial battery technologies at ees Europe 2025, highlighting next-generation VRLA solutions and energy-storage platforms. The initiative strengthened product positioning across industrial power applications and expanded visibility among enterprise infrastructure operators.

April 2025 – GS Yuasa announced commercial operation of a 2 MWh battery energy system supplied to Honda’s Hosoe facility in Japan. The deployment demonstrates scalable industrial battery integration capabilities and strengthens the company’s advanced energy infrastructure portfolio.

The report provides a comprehensive assessment of the global Lead-Acid Forklift Batteries Market across battery types, applications, end-user industries, and regional markets. Coverage includes flooded lead-acid batteries, sealed lead-acid batteries, AGM batteries, and lead-carbon technologies used across warehousing, manufacturing, retail logistics, and port operations. The study evaluates demand distribution, deployment patterns, battery replacement cycles, recycling ecosystems, and evolving industrial fleet requirements. More than 65% of electric forklift fleets globally continue utilizing lead-acid systems, making lifecycle management and infrastructure compatibility central analytical themes.

The report further examines competitive positioning, technology adoption, regional manufacturing concentration, and enterprise procurement trends across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa. Strategic analysis covers battery monitoring systems, charging technologies, recycling integration, and lead-carbon innovation. The assessment supports investment planning, capacity expansion decisions, partnership strategies, market-entry evaluation, and long-term competitive positioning while identifying operational priorities expected to shape industry development between 2026 and 2033.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 560.0 Million |

| Market Revenue (2033) | USD 731.7 Million |

| CAGR (2026–2033) | 3.4% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | EnerSys; East Penn Manufacturing; GS Yuasa Corporation; Exide Industries Limited; Hoppecke Batterien GmbH & Co. KG; Crown Battery Manufacturing Company; Stryten Energy; Amara Raja Energy & Mobility Limited; Trojan Battery Company; Midac Batteries S.p.A.; TAB Batteries; Discover Battery; Sunlight Group; Leoch International Technology Limited |

| Customization & Pricing | Available on Request (10% Customization Free) |