Reports

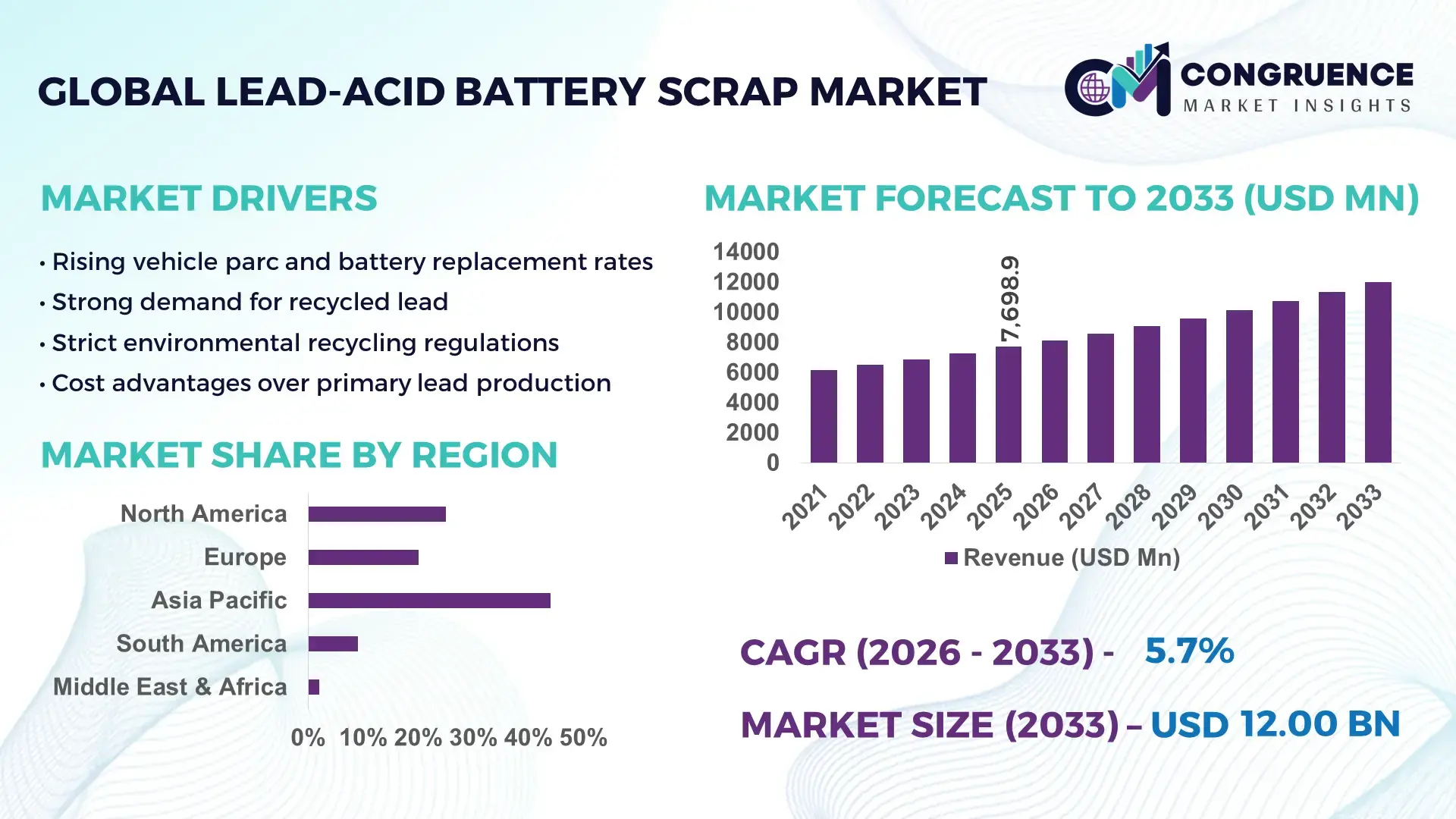

The Global Lead-acid Battery Scrap Market was valued at USD 7698.85 Million in 2025 and is anticipated to reach a value of USD 11995.7 Million by 2033 expanding at a CAGR of 5.7% between 2026 and 2033. This growth is supported by rising secondary lead recovery requirements and increasing regulatory focus on battery recycling efficiency.

China represents the most prominent country in the global Lead-acid Battery Scrap Market, supported by large-scale battery manufacturing and recycling infrastructure. In 2024, China operated over 200 licensed lead recycling facilities with an estimated annual secondary lead processing capacity exceeding 6 million metric tons. The country accounts for more than 45% of global lead-acid battery production, with automotive, industrial UPS, and electric two-wheeler batteries as key application segments. Investments exceeding USD 1.8 billion between 2022 and 2024 were directed toward advanced smelting, hydrometallurgical recovery, and closed-loop recycling technologies. Automation adoption in battery dismantling facilities surpassed 60%, improving material recovery rates and reducing environmental emissions across industrial zones.

Market Size & Growth: Valued at USD 7698.85 Million in 2025, projected to reach USD 11995.7 Million by 2033, growing at a CAGR of 5.7%, driven by rising secondary lead demand and stricter recycling mandates.

Top Growth Drivers: Automotive battery replacement rates at 58%, industrial backup power adoption at 41%, recycling efficiency improvement at 32%.

Short-Term Forecast: By 2028, average lead recovery efficiency is expected to improve by 18% through process optimization and automation.

Emerging Technologies: Automated battery breaking systems, low-emission rotary furnace upgrades, AI-based scrap sorting solutions.

Regional Leaders: Asia-Pacific projected at USD 5200 Million by 2033 with strong EV battery recycling adoption; Europe at USD 3100 Million driven by circular economy compliance; North America at USD 2400 Million supported by regulated scrap collection networks.

Consumer/End-User Trends: Automotive OEMs and industrial power system operators increasingly favor closed-loop recycling contracts to stabilize lead supply.

Pilot or Case Example: A 2024 automated recycling pilot in Southeast Asia achieved a 22% reduction in processing downtime and 15% higher material yield.

Competitive Landscape: Market leader controls approximately 17% share, followed by several global secondary lead processors and regional recyclers.

Regulatory & ESG Impact: Tightened hazardous waste handling rules and extended producer responsibility policies are accelerating formal scrap recovery adoption.

Investment & Funding Patterns: Over USD 3.4 billion invested globally since 2022, with increased project finance for eco-efficient smelting upgrades.

Innovation & Future Outlook: Integration of digital tracking, cleaner smelting technologies, and cross-border scrap sourcing agreements will shape long-term market evolution.

The Lead-acid Battery Scrap Market is primarily supported by automotive batteries contributing approximately 62% of total scrap volume, followed by industrial stationary batteries at nearly 28%, and motive power applications covering the remaining share. Recent technological progress includes sealed smelting systems, enhanced desulfurization processes, and advanced plastic separation methods that improve material recovery while reducing emissions. Regulatory frameworks focused on hazardous waste control, recycling traceability, and emissions reduction continue to influence operational standards. Regionally, Asia-Pacific leads consumption due to dense vehicle populations and industrial energy storage use, while Europe emphasizes sustainability-driven recycling compliance. Future growth is expected from modernization of recycling infrastructure, increasing battery replacement cycles, and integration of digital monitoring across scrap value chains.

The strategic relevance of the Lead-acid Battery Scrap Market lies in its central role within the global circular economy, industrial resource security, and regulatory compliance frameworks. Secondary lead derived from battery scrap supplies nearly 55–60% of global refined lead demand, reducing dependence on primary mining and lowering energy consumption by up to 65% compared to virgin lead production. From a strategic standpoint, recyclers and battery manufacturers are increasingly aligning long-term sourcing strategies with closed-loop scrap recovery systems to stabilize raw material availability and pricing volatility.

Technologically, automated battery breaking and advanced hydrometallurgical recovery deliver 20% higher lead purity compared to conventional pyrometallurgical smelting standards. Asia-Pacific dominates in volume due to large vehicle fleets and industrial battery usage, while Europe leads in adoption with nearly 72% of licensed recyclers operating under digital tracking and extended producer responsibility systems. By 2028, AI-driven scrap sorting and process optimization platforms are expected to improve material recovery rates by 15% and reduce processing downtime by 18%.

From an ESG and compliance perspective, firms are committing to sustainability metrics such as 90% recycling efficiency and 30% emissions reduction by 2030, aligned with hazardous waste and circular economy regulations. In 2024, India achieved a 25% reduction in informal battery recycling through nationwide digital scrap traceability initiatives and licensed recycler expansion. Looking ahead, the Lead-acid Battery Scrap Market is positioned as a pillar of industrial resilience, regulatory compliance, and sustainable growth, supporting long-term supply chain stability across automotive, energy storage, and infrastructure sectors.

Rising automotive battery replacement cycles are a major growth driver for the Lead-acid Battery Scrap Market, as internal combustion engine vehicles and hybrid models continue to rely heavily on lead-acid batteries. Globally, more than 1.4 billion vehicles are in operation, with over 85% using lead-acid starter batteries. Average replacement cycles of 36–48 months generate a steady and predictable stream of end-of-life batteries. In high-density vehicle markets, annual scrap battery collection rates exceed 90% under regulated systems. Additionally, expanding commercial vehicle fleets and increased use of auxiliary batteries for safety and infotainment systems are increasing per-vehicle battery counts. This sustained scrap inflow supports higher utilization rates at recycling facilities and strengthens secondary lead supply reliability.

Environmental compliance complexity presents a significant restraint in the Lead-acid Battery Scrap Market, particularly in regions with fragmented regulatory enforcement. Lead handling, storage, and smelting require adherence to strict emissions, waste disposal, and worker safety standards. Compliance investments can account for up to 20–25% of total operating costs for recycling facilities. Smaller recyclers often struggle to upgrade furnaces, effluent treatment systems, and monitoring equipment to meet evolving standards. In some developing economies, delays in licensing and inspections further constrain formal sector capacity expansion. These challenges limit operational scalability, slow modernization efforts, and can temporarily reduce processing volumes despite growing scrap availability.

Digital traceability and automation present substantial growth opportunities for the Lead-acid Battery Scrap Market by improving collection efficiency, transparency, and recovery yields. Digital tracking platforms enable real-time monitoring of battery movement from collection to recycling, reducing leakage into informal channels by up to 30%. Automated battery dismantling systems can process 40–50% more units per hour than manual operations while improving worker safety. Additionally, data-driven process control supports higher lead recovery consistency and lower impurity levels. Governments and large OEMs increasingly favor recyclers with traceability capabilities, creating new contract-based supply opportunities and encouraging investment in technology-enabled recycling infrastructure.

Cost pressures and feedstock variability remain persistent challenges in the Lead-acid Battery Scrap Market. Scrap battery quality varies significantly based on age, usage conditions, and design, affecting recovery efficiency and processing time. Fluctuations in collection volumes can lead to underutilized capacity or supply bottlenecks at recycling plants. Logistics costs for hazardous material transport have risen steadily, increasing overall operational expenditure. Additionally, upgrading facilities to handle diverse battery designs requires continuous capital investment. These factors complicate cost management, forecasting accuracy, and margin stability for recyclers operating in highly regulated and competitive environments.

Expansion of Automated Battery Dismantling and Sorting Systems: Recycling facilities are rapidly adopting automation to improve throughput and recovery efficiency. Automated battery breaking and separation lines now process up to 4,000–5,000 units per hour, representing a 35% productivity increase compared to manual operations. Facilities using robotic sorting report impurity reduction levels of nearly 20% and worker safety incident declines of over 30%, strengthening compliance and operational consistency.

Integration of Modular and Prefabricated Infrastructure in Recycling Plants: The rise of modular and prefabricated construction is reshaping capacity expansion strategies in the Lead-acid Battery Scrap market. Around 55% of newly commissioned recycling projects report cost efficiencies through prefabricated plant components and modular smelting units. Off-site fabricated structures reduce construction timelines by approximately 25% and lower on-site labor requirements by nearly 40%, supporting faster capacity scaling in Europe and North America.

Growth in Formalized Collection and Digital Tracking Networks: Digital traceability platforms are becoming standard across regulated markets, covering nearly 65% of organized scrap collection volumes in developed regions. Battery serialization and QR-based tracking systems have improved documented scrap recovery rates by 28% while reducing informal leakage by nearly 22%. This trend enhances supply predictability and supports compliance with extended producer responsibility requirements.

Rising Demand from Industrial Energy Storage Replacement Cycles: Industrial backup power systems for telecom, data centers, and manufacturing facilities are generating increasing volumes of end-of-life batteries. Industrial applications now account for approximately 30% of total lead-acid battery scrap availability, up from 24% five years ago. Replacement cycles averaging 4–5 years are driving consistent scrap inflows, supporting stable feedstock availability and higher recycling plant utilization rates.

The Lead-acid Battery Scrap Market is segmented based on type, application, and end-user, each reflecting distinct material recovery pathways, operational requirements, and demand drivers. By type, segmentation depends on battery chemistry, construction, and use-life characteristics that influence scrap composition and recycling efficiency. Application-based segmentation highlights where scrap generation originates, such as automotive, industrial, and stationary power uses, each with different replacement cycles and regulatory handling needs. End-user segmentation focuses on entities involved in scrap generation, collection, processing, and reuse, including OEMs, recyclers, and industrial operators. These segmentation layers collectively determine scrap availability, processing complexity, compliance intensity, and technology adoption patterns. Understanding segmentation dynamics enables stakeholders to align capacity planning, technology investments, and sourcing strategies with the most stable and high-volume scrap streams.

The Lead-acid Battery Scrap Market by type includes flooded lead-acid batteries, valve-regulated lead-acid (VRLA) batteries, absorbed glass mat (AGM) batteries, and gel batteries. Flooded lead-acid batteries currently account for approximately 48% of total scrap volume due to their widespread use in conventional vehicles, forklifts, and industrial power systems, combined with shorter average service lives and higher unit weights. VRLA batteries hold nearly 27% of scrap availability, reflecting their extensive use in telecom and UPS systems. AGM batteries account for about 15% of adoption, while gel batteries and niche formats together represent a combined 10%.

AGM batteries are the fastest-growing scrap type, driven by rising use in start-stop automotive systems and premium vehicles, with scrap generation volume expanding at an estimated CAGR of 7.2%. Higher lead content per unit and accelerated replacement cycles support this growth. In contrast, gel batteries remain niche due to longer lifespans and limited automotive penetration.

By application, the Lead-acid Battery Scrap Market is led by automotive applications, contributing approximately 62% of total scrap generation. This dominance is supported by high vehicle parc volumes, replacement intervals of three to four years, and near-universal use of lead-acid starter batteries in internal combustion and hybrid vehicles. Industrial backup power systems account for around 23% of scrap volume, while motive power applications such as forklifts and warehouse equipment represent about 10%. Other applications, including renewable energy storage and marine systems, collectively contribute the remaining 5%.

Industrial backup power is the fastest-growing application segment, with scrap generation increasing at an estimated CAGR of 6.5%, supported by telecom tower expansion, data center growth, and grid reliability investments. Automotive scrap remains stable but mature, while renewable energy storage applications are gradually increasing their contribution due to shorter replacement cycles in harsh operating environments.

End-user segmentation in the Lead-acid Battery Scrap Market is led by licensed recycling companies, which handle approximately 46% of total scrap processing volumes due to centralized collection networks and regulatory authorization. Battery manufacturers operating closed-loop recycling systems account for nearly 28% of scrap utilization, while automotive service networks contribute around 16% through structured take-back programs. Other end-users, including industrial facility operators and energy service providers, collectively represent about 10%.

Battery manufacturers represent the fastest-growing end-user group, with adoption of in-house or partnered recycling expanding at a CAGR of 8.1%, driven by supply security and compliance requirements. Automotive OEM-led take-back programs show steady growth, while informal sector participation continues to decline in regulated markets.

Asia-Pacific accounted for the largest market share at 46.8% in 2025 however, Europe is expected to register the fastest growth, expanding at a CAGR of 6.2% between 2026 and 2033.

Asia-Pacific generated over 7.2 million metric tons of lead-acid battery scrap in 2025, supported by dense vehicle ownership, industrial battery usage, and high replacement frequencies. Europe followed with a 27.4% share, driven by structured recycling systems and extended producer responsibility enforcement across member states. North America held approximately 18.1% of global volumes, supported by mature automotive and industrial backup power sectors. South America and the Middle East & Africa together accounted for nearly 7.7%, with rising formalization improving collection efficiency. Regional disparities are evident in automation penetration, regulatory enforcement intensity, and scrap traceability adoption, directly influencing recovery efficiency, operating costs, and investment priorities across markets.

North America represents around 18.1% of the global Lead-acid Battery Scrap Market, supported by high vehicle ownership rates and regulated battery take-back programs. Automotive starter batteries account for nearly 64% of scrap volumes, followed by industrial UPS and data center batteries at 22%. Regulatory frameworks mandate recovery rates above 95% in several jurisdictions, driving formal recycling adoption. Digital inventory tracking and automated battery breaking systems are used by over 58% of licensed recyclers. Local players are investing in low-emission smelting and closed-loop partnerships with OEMs to secure stable scrap inflows. Consumer behavior reflects higher enterprise-driven collection from automotive service centers and fleet operators, with structured returns preferred over informal disposal.

Europe accounts for approximately 27.4% of global Lead-acid Battery Scrap volumes, with Germany, France, and the UK collectively contributing over 62% of regional processing capacity. Regulatory initiatives enforce recycling efficiency targets above 90%, accelerating investment in cleaner smelting and hydrometallurgical technologies. Over 70% of recyclers operate under digital traceability and compliance reporting systems. Advanced automation adoption exceeds 60% in Western Europe, improving material purity and reducing emissions. Regional players are expanding cross-border scrap sourcing agreements to optimize capacity utilization. Consumer behavior is shaped by regulatory pressure, leading to preference for certified recyclers and transparent material recovery practices.

Asia-Pacific leads the Lead-acid Battery Scrap Market with a 46.8% share and the highest processing volumes globally. China, India, and Japan together account for over 78% of regional scrap generation. High vehicle density, expanding industrial power infrastructure, and shorter battery replacement cycles drive volumes exceeding 7 million metric tons annually. Infrastructure investments include automated dismantling lines and modular smelting units, with automation penetration nearing 55% in major industrial zones. Local players focus on capacity expansion and process efficiency upgrades to manage scale. Consumer behavior favors cost-efficient recycling channels, with growing acceptance of formal collection platforms in urban centers.

South America contributes approximately 4.5% of global Lead-acid Battery Scrap volumes, led by Brazil and Argentina. Automotive and commercial transport fleets generate nearly 60% of regional scrap, while industrial backup power accounts for 25%. Energy sector reliability concerns are driving replacement of aging battery systems, increasing scrap availability. Governments are introducing incentives to formalize recycling and reduce hazardous waste leakage. Regional players are investing in centralized processing hubs to improve economies of scale. Consumer behavior varies, with higher participation from commercial fleets and energy operators compared to private vehicle owners.

The Middle East & Africa region holds around 3.2% of global Lead-acid Battery Scrap volumes, with South Africa and the UAE as key growth countries. Demand is driven by oil & gas operations, telecom towers, and construction-related backup power systems. Industrial batteries contribute nearly 48% of scrap volumes in the region. Technological modernization includes gradual adoption of automated dismantling and emissions-controlled furnaces. Trade partnerships and waste management regulations are strengthening formal recycling channels. Consumer behavior shows higher scrap generation from industrial and infrastructure operators than from passenger vehicle segments.

China – 32.5% market share: Dominates the Lead-acid Battery Scrap Market due to large-scale battery manufacturing, high vehicle density, and extensive secondary lead processing capacity.

United States – 15.2% market share: Strong position in the Lead-acid Battery Scrap Market supported by regulated take-back systems, high automotive battery replacement rates, and advanced recycling infrastructure.

The Lead-acid Battery Scrap market exhibits a moderately fragmented competitive structure, with a large number of regional recyclers operating alongside a smaller group of globally integrated secondary lead producers. Globally, more than 250 licensed recycling companies actively participate in battery scrap collection, processing, and secondary lead refining. The top five companies collectively account for approximately 38–42% of total processed scrap volumes, indicating consolidation at the upper tier while regional and local players remain critical for collection and preprocessing activities.

Competitive positioning is increasingly defined by processing scale, environmental compliance capability, and technological sophistication. Leading players operate multi-country recycling networks with individual plant capacities exceeding 150,000–300,000 metric tons per year, while smaller competitors typically remain below 50,000 metric tons annually. Strategic initiatives include long-term supply agreements with automotive OEMs, investments in automated battery breaking lines, and upgrades to low-emission smelting systems. Partnerships between recyclers and battery manufacturers now cover nearly 60% of formal scrap flows in regulated markets.

Innovation trends shaping competition include AI-enabled scrap sorting, digital traceability platforms, and modular plant designs that reduce setup time by 20–30%. Mergers and capacity expansions are primarily focused on improving regional coverage and compliance readiness, as environmental standards tighten globally. Overall, competition increasingly favors operators with scale, compliance reliability, and closed-loop recycling capabilities.

Gravita India Ltd.

Ecobat Technologies

Johnson Controls Recycling

Exide Industries Ltd.

EnerSys Recycling Operations

RSR Corporation

Glencore Secondary Lead Operations

Aqua Metals

Recylex Group

The Lead-acid Battery Scrap market is undergoing substantial technological transformation across the recycling value chain, driven by the need to increase material recovery rates, reduce environmental footprint, and improve operational efficiency. At the core of current technology adoption are automated battery dismantling and sorting systems, which process 4,000–5,500 units per hour in advanced facilities compared to 1,200–1,500 units per hour in manual operations. These systems integrate conveyor segmentation, robotic breaking arms, and optical sorters to separate lead, polypropylene, and electrolyte components with purity improvements of up to 20% versus conventional methods. Emerging hydrometallurgical recovery techniques are gaining traction as an alternative to traditional pyrometallurgical smelting. Advanced leaching and electrochemical extraction technologies enable recovery of lead at temperatures below 150°C, significantly reducing energy input and emissions. Digital process controls support tighter regulation of reagent usage, lowering waste generation by an estimated 15–18% in optimized plants.

AI-enabled scrap classification and predictive maintenance platforms are being deployed in nearly 45–55% of newly modernized facilities. These technologies leverage sensor data and machine learning to predict equipment failures and improve belt sorting accuracy, leading to uptime increases of 12–17%. Integration of IoT monitoring allows remote oversight of furnace emissions, battery acid neutralization systems, and material throughput, enhancing compliance with stringent environmental standards. Modular and prefabricated plant designs are now used in expansions and greenfield projects, cutting construction timelines by roughly 20–28% while lowering initial capital demands. These modular units often come pre-tested and calibrated, enabling faster commissioning.

• In January 2025, Gravita India announced a significant capacity expansion plan targeting over 500,000 metric tons of recycling operations by fiscal 2027, supported by a planned investment of approximately USD 11.5 million in new recycling segments to enhance processing of lead-acid battery scrap and meet rising demand from automotive and industrial sectors.

• In July 2024, First Battery commenced operations at its advanced lead-acid battery recycling facility in Benoni Industrial Sites, South Africa, with a daily processing capability of 80 tons, integrating battery breaking, lead smelting, acid treatment, and polypropylene reprocessing to support closed-loop material reuse.

• In early 2024, ECOBAT Technologies announced a strategic partnership with major automotive manufacturers to expand sustainable lead-acid battery scrap collection and recycling operations, positioning its services to handle an estimated 18% greater scrap throughput in targeted regions.

• In April 2024, Exide Technologies completed the acquisition of RSR Technologies, enhancing its recycling footprint to process over 100,000 metric tons of lead-acid batteries annually, significantly increasing its ability to secure end-of-life batteries and recycled lead streams.

The Lead-acid Battery Scrap Market Report comprehensively covers the entire value chain of lead-acid battery scrap recycling, from scrap collection and preprocessing through secondary lead recovery and reuse in battery manufacturing and allied industrial applications. The report segments the market by battery type—such as traditional flooded, valve-regulated lead-acid (VRLA), AGM, and gel batteries—highlighting variations in scrap characteristics, material composition, and processing requirements. It also analyzes application streams including automotive starter batteries, industrial UPS systems, motive power batteries (e.g., forklifts), and emerging stationary storage systems, with detailed breakdowns of scrap source contributions and end-of-life handling patterns.

Geographically, the report examines key regions including Asia-Pacific, Europe, North America, South America, and Middle East & Africa, providing insights into regional infrastructure maturity, regulatory frameworks, and collection efficiencies. The analysis includes technology-focused segments, covering process categories such as pyrometallurgical smelting, hydrometallurgical recovery, and mechanical/physical preprocessing, as well as emerging digital solutions like AI-enabled sorting, traceability platforms, and automation in battery dismantling. Industry focus areas in the report include environmental compliance and extended producer responsibility trends, secondary lead quality standards, and the influence of regulatory sustainability mandates on market operations. Additionally, the report highlights niche segments such as value-added plastic recovery, safe electrolyte neutralization systems, and cross-chemistry recycling initiatives involving lead-acid alongside emerging battery types. Structured for strategic decision-making, the report provides a holistic view of competitive dynamics, technological evolution, operational challenges, and long-term resource sustainability considerations targeting industry professionals and stakeholders.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

5.7% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Gravita India Ltd., Ecobat Technologies, Johnson Controls Recycling, Exide Industries Ltd., EnerSys Recycling Operations, RSR Corporation, Glencore Secondary Lead Operations, Aqua Metals, Recylex Group |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |