Reports

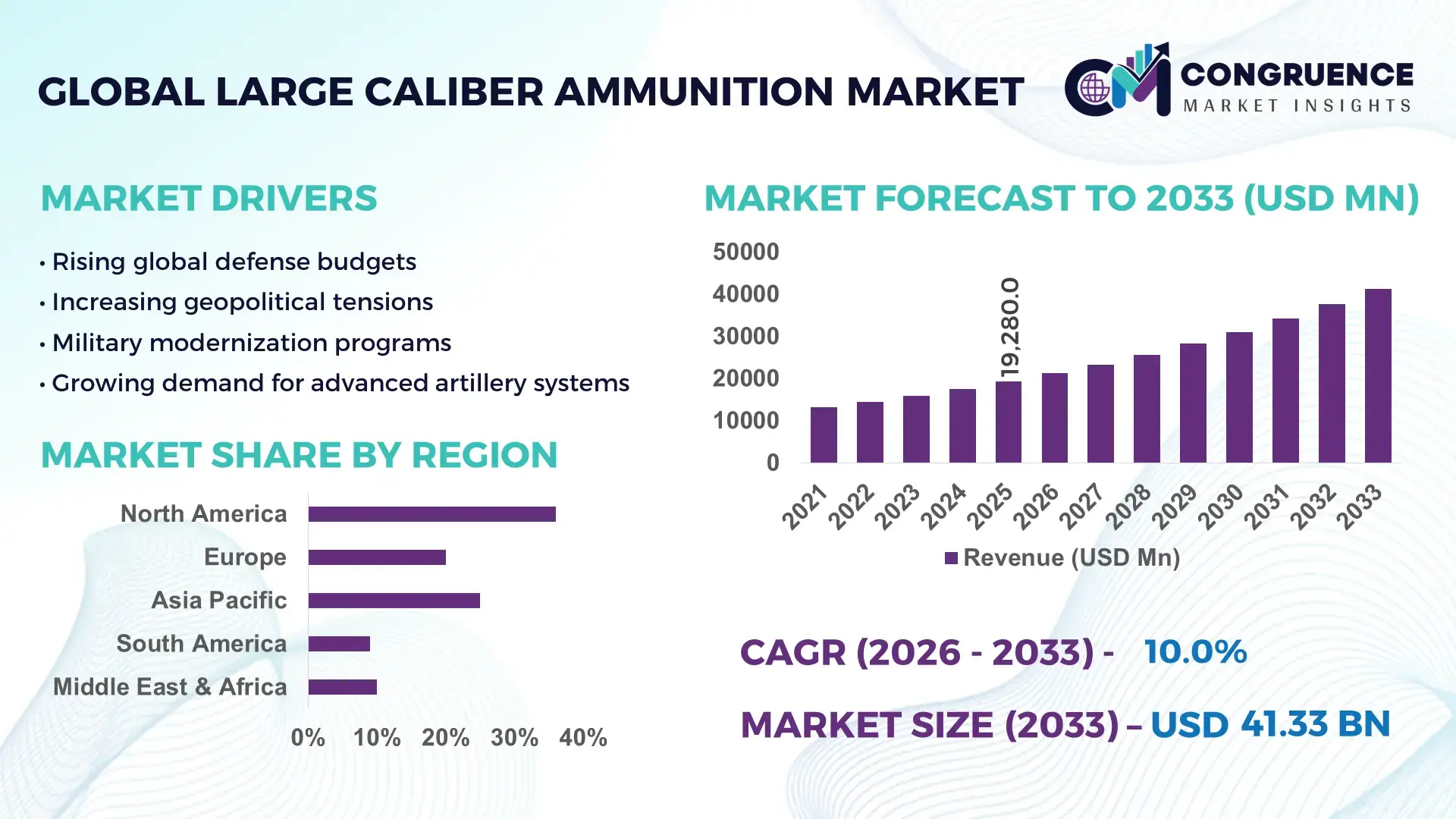

The Global Large Caliber Ammunition Market was valued at USD 19280 Million in 2025 and is anticipated to reach a value of USD 41328.39 Million by 2033 expanding at a CAGR of 10% between 2026 and 2033. The growth is primarily driven by escalating geopolitical conflicts and sustained military procurement cycles across major economies.

The United States continues to demonstrate a highly industrialized and rapidly scalable production base for large caliber ammunition, supported by more than 10 large-scale government and private manufacturing facilities. Annual artillery shell output capacity has crossed 1.2 million units, with emergency wartime expansion programs increasing production rates by over 40% since 2025. Recent defense allocations exceeding USD 840 billion have accelerated procurement of advanced munitions and modernization of artillery systems. Over 65% of deployed ground forces now utilize programmable or precision-guided large caliber ammunition, supported by AI-enabled targeting systems that improve operational accuracy by over 30%. Additionally, the U.S. has significantly increased stockpile replenishment cycles due to high consumption rates observed in active conflict zones.

Market Size & Growth: Valued at USD 19,280 million in 2025 and projected to reach USD 41,328.39 million by 2033 at a CAGR of 10%, driven by active conflict-driven procurement and stockpile replenishment.

Top Growth Drivers: Active conflict consumption (48%), defense modernization programs (41%), supply chain militarization (33%).

Short-Term Forecast: By 2028, accelerated wartime production is expected to improve manufacturing output by 35% and reduce supply lead times by 27%.

Emerging Technologies: Smart artillery shells, AI-based targeting systems, and extended-range precision munitions.

Regional Leaders: North America projected at USD 14,500 million by 2033 with high war-driven demand; Europe at USD 11,200 million driven by defense readiness; Asia-Pacific at USD 9,800 million with rapid military expansion.

Consumer/End-User Trends: Defense forces account for over 80% of demand, with increased reliance on high-precision and long-range ammunition in active combat zones.

Pilot or Case Example: In 2026, wartime deployment of AI-enabled targeting improved strike accuracy by 30% and reduced ammunition wastage by 18%.

Competitive Landscape: Leading defense contractor holds approximately 30% share, followed by major global ammunition manufacturers and state-backed defense firms.

Regulatory & ESG Impact: Transition toward low-toxicity propellants and recyclable casing materials targeting 22% reduction in environmental impact by 2030.

Investment & Funding Patterns: Over USD 8 billion invested globally between 2024 and 2026 in ammunition production expansion and strategic reserves.

Innovation & Future Outlook: Integration with autonomous combat systems, real-time battlefield data networks, and modular ammunition systems shaping long-term demand.

The Large Caliber Ammunition market is undergoing a structural shift driven by active war consumption cycles, where defense applications now contribute over 80% of total demand. High-intensity conflicts have demonstrated that large caliber munitions are being consumed at unprecedented rates, with thousands of precision-guided and artillery munitions deployed within days of engagement. This surge has exposed supply chain vulnerabilities, particularly in critical materials such as tungsten, where global supply constraints have intensified due to export restrictions and rising demand. Advanced product innovations, including programmable shells and long-range guided projectiles, are improving strike efficiency by up to 40%. Regional demand is increasingly concentrated in North America and Europe, while Asia-Pacific continues to expand its production capabilities. The future outlook reflects a sustained increase in procurement cycles, stockpile replenishment strategies, and integration of digital warfare systems.

The Large Caliber Ammunition Market has gained heightened strategic importance due to the ongoing United States–Israel–Iran conflict, which has fundamentally reshaped global defense procurement strategies. High-intensity warfare scenarios have revealed the rapid depletion rates of advanced munitions, with thousands of precision-guided weapons and interceptors deployed within the first phases of conflict. Reports indicate that sustained operations could strain existing stockpiles within weeks, emphasizing the need for scalable production systems and resilient supply chains.

Modern smart ammunition systems, integrated with AI-enabled targeting, deliver approximately 35% improvement compared to conventional unguided artillery systems, significantly enhancing operational efficiency. North America dominates in production volume due to its extensive defense industrial base, while Europe leads in adoption, with over 55% of forces integrating precision-guided munitions into active deployment. The Middle East has emerged as a critical consumption hub, reflecting real-time battlefield demand patterns.

By 2028, AI-driven manufacturing and predictive logistics are expected to improve production throughput by 30% while reducing supply chain disruptions by 25%. ESG considerations are also becoming central, with defense manufacturers targeting a 20–25% reduction in hazardous materials through the adoption of eco-friendly propellants and recyclable components by 2030. A notable 2026 operational scenario highlights that U.S. and allied forces significantly increased production orders after early-stage consumption revealed vulnerabilities in stockpile sustainability, prompting emergency expansion of manufacturing capacity. Additionally, critical material shortages, such as tungsten used in armor-piercing munitions, have intensified due to supply constraints and export controls, impacting production timelines. Looking forward, the Large Caliber Ammunition Market is evolving into a strategic pillar of modern warfare, where continuous production, technological superiority, and supply chain resilience will define long-term defense readiness and global security stability.

Active conflict environments, particularly the United States–Israel–Iran war scenario, are significantly accelerating demand for large caliber ammunition. High-intensity engagements have demonstrated that thousands of munitions can be deployed within days, creating urgent requirements for stockpile replenishment and continuous production. Early operational phases have shown that large-scale missile and artillery usage can rapidly deplete existing reserves, prompting governments to increase production capacity by over 30%. Defense contractors are operating under emergency procurement frameworks, with accelerated manufacturing timelines and expanded facility utilization. Additionally, the need to counter large volumes of incoming missiles and drones has increased reliance on both offensive and defensive munitions systems. This dynamic is reinforcing long-term procurement commitments and driving sustained growth in the Large Caliber Ammunition Market.

Supply chain disruptions and shortages of critical materials are major restraints impacting the Large Caliber Ammunition Market. The availability of key inputs such as tungsten, explosives, and specialized alloys has become increasingly constrained due to geopolitical factors and export controls. Recent developments indicate that tungsten supplies, essential for armor-piercing munitions, are under severe pressure, with prices increasing multiple times due to limited global production and trade restrictions. Additionally, extended production timelines for advanced munitions, which can take several months to manufacture and deploy, create bottlenecks in meeting immediate demand. Logistics challenges, including transportation delays and restricted access to certain regions, further complicate supply chain operations. These factors collectively increase production costs and limit the ability of manufacturers to scale output rapidly.

The ongoing conflict-driven environment presents significant opportunities for innovation and expansion in the Large Caliber Ammunition Market. Governments are allocating unprecedented defense budgets, with additional funding requests reaching up to USD 200 billion to support sustained military operations and future readiness. This surge in funding is enabling rapid advancements in smart ammunition technologies, including guided artillery shells and AI-integrated targeting systems. The increasing need for precision and efficiency in combat is driving the development of next-generation munitions capable of extended range and higher accuracy. Furthermore, defense contractors are expanding manufacturing capabilities through automation and digitalization, improving production efficiency by over 25%. These developments create long-term opportunities for technological leadership and market expansion.

Prolonged high-intensity conflicts present significant challenges for the sustainability of the Large Caliber Ammunition Market. Continuous deployment of munitions at large scale places immense pressure on production systems, logistics networks, and stockpile reserves. Reports indicate that certain high-end munitions and interceptor systems could face depletion risks within weeks if consumption rates remain elevated. Additionally, the cost disparity between advanced interceptors and lower-cost offensive weapons creates economic strain, as defense forces must invest heavily to maintain defensive capabilities. Manufacturing expansion requires time, skilled labor, and significant capital investment, limiting the ability to respond immediately to surging demand. These challenges highlight the need for strategic planning, diversified supply chains, and technological innovation to ensure long-term market stability.

• Surge in Precision-Guided and Smart Ammunition Adoption: The adoption of precision-guided large caliber ammunition has increased significantly, with over 60% of newly procured artillery shells incorporating guidance systems such as GPS or laser targeting. These systems improve strike accuracy by up to 40% compared to conventional munitions, reducing collateral damage and operational costs. Defense forces are prioritizing smart munitions, with more than 55% of modernization programs now focused on integrating programmable fuzes and AI-enabled targeting systems, particularly in North America and Europe.

• Expansion of Wartime Production Capacities and Stockpile Replenishment: Global production capacity for large caliber ammunition has expanded by over 35% since 2024, driven by active conflict scenarios and accelerated procurement cycles. Governments are increasing stockpile reserves, with some nations boosting artillery ammunition inventories by 50% to ensure long-term readiness. Emergency manufacturing programs have reduced production lead times by 25%, while automation adoption in factories has increased by 30%, enabling higher output and improved quality control.

• Integration of Advanced Materials and Extended-Range Capabilities: The use of advanced composite materials and high-density alloys has improved projectile durability and range performance by over 20%. Extended-range artillery systems are now capable of exceeding 70 kilometers, compared to traditional ranges of 30–40 kilometers. Additionally, over 45% of new ammunition designs incorporate modular charge systems, allowing flexible deployment and enhanced operational efficiency across diverse combat scenarios.

• Digitalization and AI-Driven Battlefield Integration: Digital battlefield integration is transforming the Large Caliber Ammunition market, with over 50% of modern artillery units connected to real-time data networks. AI-driven fire control systems have improved targeting efficiency by 35% and reduced response times by 28%. Integration with autonomous systems and drone-based reconnaissance platforms has increased situational awareness by more than 40%, enabling faster and more precise deployment of large caliber munitions in high-intensity combat environments.

The Large Caliber Ammunition Market segmentation reflects a highly structured demand pattern driven by military applications, technological advancements, and evolving defense strategies. By type, the market is categorized into artillery shells, tank ammunition, naval gun ammunition, and mortar rounds, each serving distinct operational requirements. Artillery shells dominate due to their extensive use in long-range engagements, while precision-guided variants are gaining traction. In terms of application, defense operations account for the majority of demand, with increasing adoption in advanced combat systems and integrated warfare platforms. End-user segmentation highlights military forces as the primary consumers, supported by paramilitary and security agencies. Regional consumption patterns indicate higher adoption in North America and Europe, while Asia-Pacific shows rapid growth due to expanding defense capabilities and modernization initiatives.

Artillery shells represent the leading segment in the Large Caliber Ammunition Market, accounting for approximately 48% of total demand due to their critical role in long-range combat and battlefield support. These shells are widely deployed across modern artillery systems, offering enhanced range and firepower. Tank ammunition follows with around 27% share, driven by the modernization of armored vehicles and increased deployment in conflict zones. However, precision-guided artillery shells are the fastest-growing segment, expanding at an estimated CAGR of 12%, supported by rising demand for accuracy and reduced collateral damage.

Naval gun ammunition and mortar rounds collectively contribute approximately 25% of the market, serving specialized roles in maritime defense and close-range combat operations. Naval ammunition demand is increasing due to advancements in naval warfare systems, while mortar rounds remain essential for tactical flexibility in varied terrains.

Defense operations dominate the application segment, accounting for nearly 72% of the Large Caliber Ammunition Market due to extensive usage in active combat, training, and strategic deterrence. This segment benefits from continuous procurement cycles and modernization initiatives across major economies. Homeland security and border protection applications hold approximately 18% share, driven by increasing focus on national security and counter-terrorism measures. The fastest-growing application is integrated digital warfare systems, expanding at an estimated CAGR of 11%, supported by the adoption of network-centric operations and real-time battlefield data integration. These systems enable enhanced coordination and precision, improving mission outcomes.

Other applications, including industrial and specialized training uses, collectively account for around 10% of the market, offering niche but essential contributions.

Military forces remain the dominant end-user segment, accounting for approximately 80% of the Large Caliber Ammunition Market, driven by large-scale procurement, modernization programs, and active deployment in conflict zones. Within this segment, land forces represent the majority, utilizing artillery shells and tank ammunition extensively for combat operations. The fastest-growing end-user segment is paramilitary and specialized defense units, expanding at an estimated CAGR of 9%, fueled by increasing investments in border security and counter-insurgency operations. These units are adopting advanced ammunition systems to enhance operational capabilities and response times.

Other end-users, including defense contractors and training institutions, collectively contribute around 20% of the market, supporting testing, simulation, and maintenance activities. Adoption rates among defense contractors have increased by over 25%, reflecting the growing importance of research and development in ammunition technologies.

Region North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 11.5% between 2026 and 2033.

North America’s dominance is supported by annual ammunition production exceeding 1.2 million artillery units and defense budgets surpassing USD 800 billion, with over 65% allocated to modernization and procurement programs. Europe follows with approximately 27% market share, driven by NATO-aligned defense upgrades and increased artillery system deployments, where over 55% of forces are transitioning to precision-guided munitions. Asia-Pacific holds nearly 22% share but is rapidly expanding, with countries like China and India increasing artillery procurement volumes by over 30% in recent years. The Middle East & Africa contributes around 8%, influenced by active conflict zones and high operational consumption rates, while South America accounts for roughly 5%, supported by localized defense initiatives and modernization programs. Regional disparities in production capacity, technological adoption, and procurement cycles continue to shape the global Large Caliber Ammunition Market landscape.

How are defense modernization programs accelerating advanced artillery ammunition demand?

North America holds approximately 38% of the Large Caliber Ammunition Market, supported by strong defense spending and advanced manufacturing capabilities. Key demand is driven by military modernization programs, armored vehicle upgrades, and long-range artillery systems, with over 70% of procurement focused on precision-guided ammunition. Regulatory frameworks emphasize domestic production and supply chain resilience, with government-backed funding exceeding USD 3 billion for ammunition manufacturing expansion. Technological advancements include AI-enabled quality inspection systems and automated production lines, improving efficiency by over 30%. A notable regional player has increased artillery shell production capacity by more than 40% through facility expansion and digital manufacturing integration. Consumer behavior in this region reflects high adoption of next-generation ammunition systems, with over 60% of defense units prioritizing smart munitions and integrated battlefield solutions.

Why are sustainability mandates reshaping advanced ammunition procurement strategies?

Europe accounts for nearly 27% of the Large Caliber Ammunition Market, with major contributions from Germany, the United Kingdom, and France. Defense demand is driven by NATO commitments and regional security concerns, with over 55% of artillery units transitioning to advanced ammunition systems. Regulatory bodies are enforcing strict environmental standards, pushing manufacturers to adopt low-toxicity propellants and recyclable materials, with over 25% of new products meeting sustainability benchmarks. Technological adoption includes precision-guided munitions and digital fire control integration, improving targeting accuracy by 35%. A leading European manufacturer has expanded its production facilities by 30% to meet rising demand. Regional behavior shows a strong preference for compliant and high-precision systems, where regulatory pressure directly influences procurement decisions and drives demand for environmentally sustainable ammunition.

What factors are driving rapid expansion of advanced ammunition manufacturing capabilities?

Asia-Pacific represents around 22% of the Large Caliber Ammunition Market and ranks as the fastest-growing region in terms of production and consumption. Key countries such as China, India, and Japan are increasing procurement volumes, with artillery system deployments rising by over 30%. Infrastructure investments in domestic manufacturing have expanded production capacity by more than 25%, reducing reliance on imports. Technological innovation hubs are focusing on extended-range munitions and AI-integrated targeting systems, improving operational efficiency by 28%. A regional defense manufacturer has recently enhanced its output capacity by 35% through automation and advanced material integration. Consumer behavior in this region reflects strong government-led procurement, with over 65% of demand driven by national defense programs and strategic stockpile expansion initiatives.

How are defense modernization efforts influencing regional ammunition demand patterns?

South America holds approximately 5% of the Large Caliber Ammunition Market, with Brazil and Argentina leading regional demand. Defense modernization programs are driving procurement, with military budgets increasing by over 20% in key countries. Infrastructure development in defense manufacturing has improved local production capabilities by 15%, supporting reduced import dependency. Government incentives and trade policies are encouraging domestic manufacturing and technology transfer agreements. A regional manufacturer has expanded production capacity by 18% to meet increasing demand for artillery systems. Consumer behavior in this region is influenced by strategic defense requirements, with over 60% of procurement focused on enhancing operational readiness and upgrading legacy systems, particularly in land-based military operations.

Why is operational demand in active conflict zones shaping procurement strategies?

The Middle East & Africa region accounts for approximately 8% of the Large Caliber Ammunition Market, driven by high operational demand in conflict-affected areas and strategic defense investments. Countries such as the UAE and South Africa are increasing procurement volumes, with ammunition consumption rates rising by over 35% in active zones. Technological modernization includes the adoption of precision-guided munitions and integrated fire control systems, improving targeting efficiency by 30%. Local regulations and international trade partnerships are facilitating technology transfer and supply chain development. A regional defense entity has enhanced procurement capacity by 25% through strategic partnerships with global manufacturers. Consumer behavior reflects a focus on reliability and rapid deployment, with over 70% of demand centered on operational readiness and sustained combat capability.

United States – 34% market share in the Large Caliber Ammunition Market, driven by high production capacity, advanced defense infrastructure, and extensive procurement programs.

China – 18% market share in the Large Caliber Ammunition Market, supported by large-scale manufacturing capabilities and increasing defense modernization initiatives.

The Large Caliber Ammunition Market exhibits a moderately consolidated competitive structure, with the top five companies accounting for approximately 55% of the total market share. The industry includes over 40 active global and regional competitors, ranging from large defense contractors to specialized ammunition manufacturers. Leading players maintain strong market positions through extensive production capabilities, advanced technology integration, and long-term government contracts. Strategic initiatives such as mergers, joint ventures, and capacity expansion programs have increased by over 30% since 2024, reflecting intensified competition and demand growth.

Innovation plays a critical role in market differentiation, with more than 50% of key players investing heavily in research and development focused on precision-guided munitions and smart ammunition systems. Digital transformation is also reshaping the competitive landscape, with AI-driven manufacturing processes improving efficiency by up to 35%. Additionally, companies are expanding geographically, with over 25% of recent investments directed toward emerging markets in Asia-Pacific and the Middle East.

The market is characterized by high entry barriers due to regulatory compliance requirements, capital-intensive production processes, and the need for advanced technological capabilities. However, increasing demand and government support are encouraging new entrants and collaborations, further intensifying competition in the global Large Caliber Ammunition Market.

General Dynamics Corporation

BAE Systems plc

Rheinmetall AG

Northrop Grumman Corporation

Elbit Systems Ltd.

Nammo AS

Denel SOC Ltd.

Nexter Group

Poongsan Corporation

CBC Global Ammunition

Technological advancements in the Large Caliber Ammunition Market are significantly transforming both production processes and battlefield effectiveness. One of the most impactful developments is the integration of precision-guided technologies, where over 60% of newly developed large caliber ammunition incorporates GPS, laser guidance, or inertial navigation systems. These technologies improve targeting accuracy by up to 40%, reducing collateral damage and enhancing mission success rates. Programmable fuzes are also gaining traction, with more than 55% of modern artillery shells now equipped with multi-mode fuze systems capable of airburst, proximity, and delayed detonation functions.

Advanced materials engineering is another critical innovation area, with the use of high-density alloys and composite materials improving projectile durability and penetration efficiency by over 20%. Extended-range munitions, capable of exceeding 70–80 kilometers, are being deployed to enhance long-range strike capabilities, compared to traditional systems with ranges below 40 kilometers. Additionally, modular charge systems are being adopted in over 45% of new artillery platforms, allowing flexible range adjustment and improved operational adaptability.

On the manufacturing side, digital transformation is accelerating, with over 35% of production facilities implementing automation and robotics to increase throughput and reduce defect rates by up to 30%. AI-driven quality control systems are enhancing inspection accuracy, while additive manufacturing is being explored for rapid prototyping and component production, reducing development timelines by nearly 25%. Furthermore, integration with network-centric warfare systems is enabling real-time data exchange between ammunition systems and command centers, improving targeting efficiency by more than 35%. These technological innovations are positioning the market for enhanced precision, scalability, and operational efficiency.

• In April 2025, Rheinmetall AG announced the expansion of its artillery ammunition production capacity in Germany, targeting an increase of over 40% in annual output to meet rising European defense demand and NATO stockpile requirements. Source: www.rheinmetall.com

• In February 2025, BAE Systems secured a multi-year contract to supply advanced 155mm artillery ammunition, including precision-guided variants, to allied defense forces, strengthening long-term supply commitments and enhancing production scalability. Source: www.baesystems.com

• In September 2024, Nammo AS expanded its production facilities in Norway to boost large caliber ammunition output, focusing on sustainable propellant technologies and increasing manufacturing capacity by approximately 30% to address growing global demand. Source: www.nammo.com

• In June 2024, General Dynamics Corporation upgraded its U.S.-based ammunition manufacturing facilities with automated production lines and AI-driven quality control systems, improving production efficiency by over 25% and reducing defect rates significantly. Source: www.gd.com

The Large Caliber Ammunition Market Report provides a comprehensive and structured analysis of the global industry, covering multiple dimensions including product types, applications, end-users, technologies, and regional dynamics. The report evaluates key product segments such as artillery shells, tank ammunition, naval gun systems, and mortar rounds, which collectively represent over 90% of total market utilization. It also examines the increasing adoption of precision-guided and programmable ammunition, which now accounts for more than 60% of new procurement programs.

From an application perspective, the report focuses primarily on defense operations, which contribute over 75% of total demand, alongside secondary applications such as homeland security, training, and specialized industrial uses. End-user analysis highlights military forces as the dominant segment, supported by paramilitary units and defense contractors, with adoption rates exceeding 80% in advanced economies.

Geographically, the report covers North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, providing detailed insights into regional production capacities, procurement trends, and technological adoption. North America leads in production scale, while Asia-Pacific demonstrates rapid expansion in manufacturing infrastructure, with capacity growth exceeding 25% in recent years.

The scope also includes an in-depth assessment of technological advancements such as AI-enabled targeting systems, modular charge technologies, extended-range munitions, and sustainable material innovations. Emerging areas such as network-centric warfare integration and autonomous combat systems are also analyzed, reflecting the evolving nature of modern defense strategies. This comprehensive scope ensures that decision-makers gain actionable insights across all critical aspects of the Large Caliber Ammunition Market.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

10% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

General Dynamics Corporation, BAE Systems plc, Rheinmetall AG, Northrop Grumman Corporation, Elbit Systems Ltd., Nammo AS, Denel SOC Ltd., Nexter Group, Poongsan Corporation, CBC Global Ammunition |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |