Reports

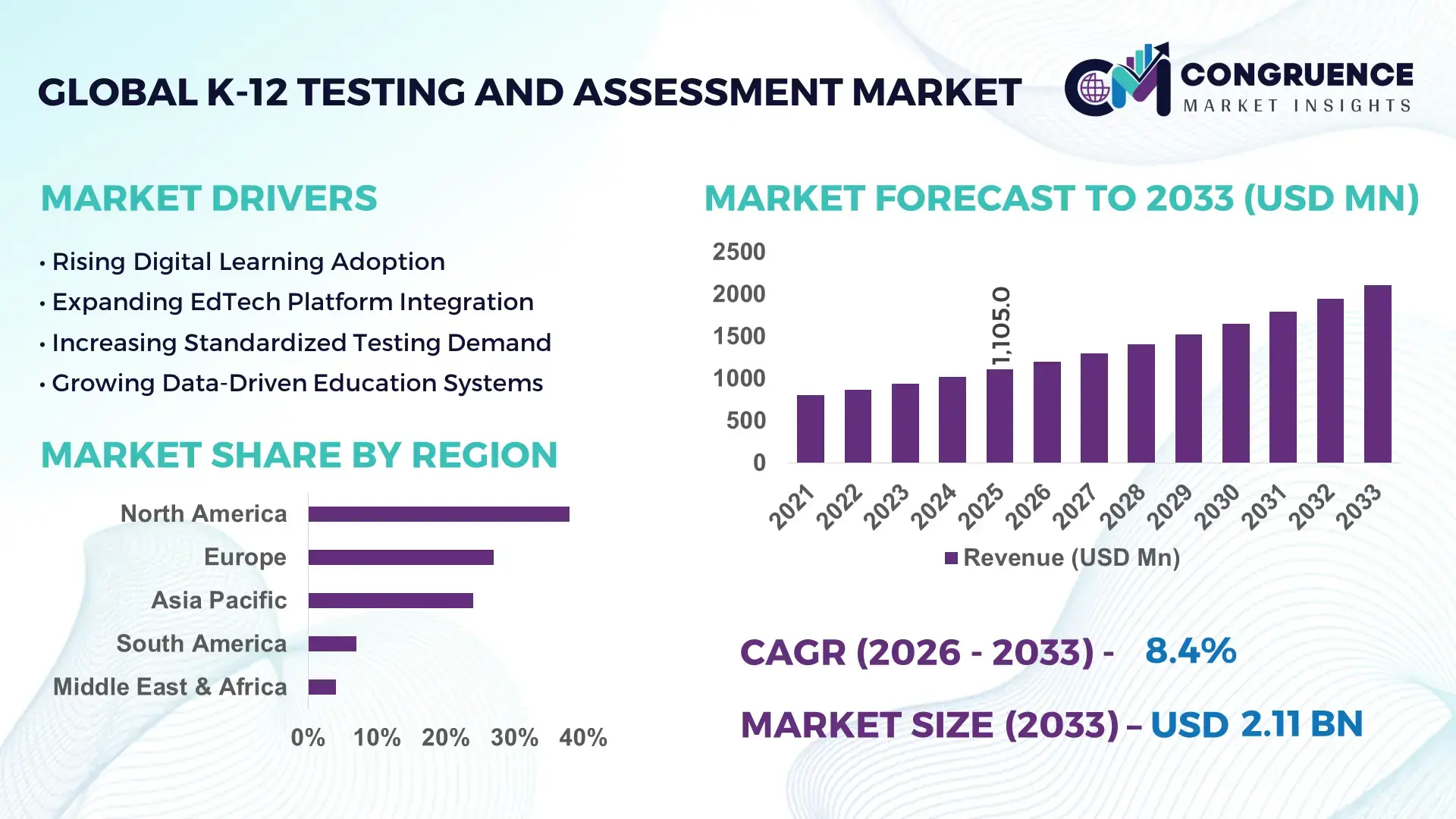

The Global K-12 Testing and Assessment Market was valued at USD 1,105.0 Million in 2025 and is anticipated to reach a value of USD 2,105.1 Million by 2033 expanding at a CAGR of 8.39% between 2026 and 2033. Growth is primarily driven by rapid AI-enabled adaptive assessments, nationwide digital education reforms, and increasing adoption of competency-based learning frameworks across public and private K-12 institutions.

The United States dominates the global market with an estimated 38% share, supported by annual K-12 education spending exceeding USD 850 billion, extensive one-to-one device deployment, and widespread cloud-based assessment adoption across school districts. Compared with India, where digital assessment platforms are expanding rapidly through the National Education Policy (NEP) 2020, the U.S. maintains stronger implementation scale, while India records faster digital classroom expansion across state education systems.

Organizations that prioritize AI-driven assessment ecosystems, curriculum alignment, and scalable digital testing infrastructure will strengthen long-term competitive positioning as education systems accelerate standardized and personalized learning transformation.

Market Size & Growth: USD 1,105.0 Million in 2025, projected to reach USD 2,105.1 Million by 2033 at 8.39%, fueled by AI-powered adaptive testing and digital education modernization.

Top Growth Drivers: AI-based assessment adoption (45%), digital classroom expansion (52%), competency-based education implementation (41%).

Short-Term Forecast: By 2028, automated grading is expected to reduce evaluation time by 35% while improving reporting efficiency across school systems.

Emerging Technologies: AI scoring engines, cloud-native assessment platforms, and learning analytics enhance assessment accuracy and personalized feedback.

Regional Leaders: North America (~USD 760 Million), Europe (~USD 520 Million), Asia-Pacific (~USD 480 Million); digital education investments continue accelerating regional deployment.

Consumer/End-User Trends: More than 60% of digitally equipped schools increasingly prefer adaptive and formative assessment platforms over paper-based testing.

Pilot/Case Example: In 2024, AI-assisted assessment deployment across selected public school districts improved grading consistency by approximately 30%.

Competitive Landscape: Pearson holds roughly 18% market share alongside ETS, Cambium Assessment, Renaissance Learning, and Instructure driving platform innovation.

Regulatory & ESG Impact: National digital education initiatives improved online assessment accessibility by over 25%, strengthening equitable learning measurement.

Investment & Funding: More than USD 1.2 Billion has supported global EdTech partnerships, AI integration, and cloud-based testing platform expansion amid regional digital transformation.

Innovation & Future Outlook: Advanced adaptive testing, generative AI feedback, and real-time learning intelligence are reshaping high-growth K-12 assessment ecosystems.

The K-12 Testing and Assessment Market is rapidly evolving as schools expand adaptive learning, remote examination capabilities, and AI-assisted performance analytics. Demand remains strongest across public education systems, digital curriculum providers, and assessment software vendors. Nearly 65% of newly deployed platforms now incorporate intelligent analytics for personalized evaluation, while evolving education standards and digital infrastructure upgrades continue accelerating implementation across developed and emerging education markets, setting the stage for broader strategic transformation.

The K-12 Testing and Assessment Market has become strategically important as education systems prioritize measurable learning outcomes, digital transformation, and data-driven academic planning. Governments and private institutions are replacing conventional examinations with intelligent assessment ecosystems that support personalized instruction, faster reporting, and curriculum optimization. National digital education initiatives and infrastructure modernization continue accelerating large-scale implementation across developed and emerging economies.

AI-enabled adaptive assessment platforms evaluate student performance nearly 40% faster than conventional paper-based processes while reducing administrative workload by approximately 30% through automated scoring and reporting. North America leads in enterprise-scale deployment and cloud integration, whereas Asia-Pacific demonstrates faster institutional digitalization supported by expanding internet access, government-backed education reforms, and increasing classroom technology adoption. Over the next two to three years, digital assessment utilization is expected to surpass 70% across newly modernized K-12 learning environments in leading education markets.

Education technology providers are strengthening strategic partnerships with school districts, curriculum developers, and cloud infrastructure providers to expand integrated assessment ecosystems. For example, districts deploying AI-powered formative assessment solutions are improving instructional planning through continuous learning analytics instead of periodic standardized testing alone. Organizations investing in scalable digital assessment platforms, interoperability, and advanced analytics will establish stronger competitive differentiation while supporting more efficient, data-driven educational outcomes.

Rapid adoption of AI-based adaptive testing is accelerating structural transformation, with 58% of U.S. school districts now using digital assessment platforms and nearly 46% of schools integrating real-time learning analytics. India’s CBSE-aligned digital examination expansion has improved automated evaluation coverage by 34%, signaling a systemic shift toward competency-based learning. The transition from paper-based to cloud-native assessment ecosystems is reducing grading latency by 30–40%, improving instructional responsiveness. Regulatory digitization mandates in countries like the United States and the UK are pushing institutions toward standardized digital compliance frameworks. Companies such as Pearson and ETS are responding through AI investment programs, strategic EdTech partnerships, and cloud infrastructure expansion, enabling scalable, data-driven assessment ecosystems across large school networks.

Uneven digital infrastructure remains a major limitation, with only 42% of rural schools in emerging economies having stable internet access, while 37% of assessment platforms face integration issues with legacy school management systems. In Brazil and parts of Southeast Asia, inconsistent broadband quality delays large-scale deployment of online testing systems. This fragmentation increases operational costs by nearly 25%, limiting scalability for EdTech providers. Data standardization gaps across jurisdictions further complicate interoperability, affecting cross-platform assessment portability. Companies are responding by developing lightweight cloud solutions, forming local telecom partnerships, and deploying hybrid offline-online testing models. Despite these efforts, infrastructure disparity continues to constrain uniform global adoption and slows institutional procurement cycles, particularly in underfunded public education systems.

The shift toward secure remote examination and intelligent analytics presents significant upside, with AI-based proctoring adoption increasing by 52% across North America and Europe. China’s large-scale smart classroom initiative has expanded digital assessment penetration by over 38%, creating demand for scalable evaluation ecosystems. Emerging technologies such as generative AI feedback systems and biometric authentication are reshaping assessment integrity frameworks. These innovations reduce manual monitoring requirements by nearly 45%, improving operational efficiency for institutions. Companies are investing in R&D-driven assessment engines and cross-border EdTech collaborations to capture untapped demand in Latin America and Africa, where digital testing adoption remains below 30%, indicating strong expansion headroom and ecosystem-level growth potential.

Growing reliance on cloud-based testing systems has increased cybersecurity exposure, with 61% of education technology platforms reporting vulnerability concerns related to data integrity and exam security. Integration complexity between LMS platforms and third-party assessment tools affects nearly 39% of deployments, particularly in multi-district education systems across the United States. Inconsistent data protection regulations across countries such as India, the UK, and Australia further complicate compliance alignment. These challenges increase implementation delays by approximately 28%, impacting scalability and institutional trust. Companies are responding by investing in zero-trust security frameworks, encrypted assessment pipelines, and unified API architectures. However, ensuring seamless interoperability while maintaining data privacy remains a persistent operational barrier requiring continuous technological reinforcement and strategic infrastructure investment.

AI-Driven Assessment Automation Scaling AI-powered grading systems are being deployed across 55% of U.S. school districts and nearly 41% of UK secondary schools, reducing manual evaluation time by up to 38%. Cloud-native assessment workflows are replacing legacy exam processing systems, improving turnaround speed by 32% and lowering administrative overhead. This shift is being accelerated by national digital education mandates and post-pandemic exam digitization reforms. Companies are responding by embedding generative AI feedback engines and expanding API-based integrations with LMS platforms. A non-obvious shift is the rising use of AI for rubric generation, improving scoring consistency by 27% across standardized testing environments.

Rise of Remote Proctoring Systems Remote proctoring adoption has reached 48% across global K-12 digital exam environments, with biometric verification improving identity accuracy by 35%. Australia and Canada are expanding secure online exam frameworks due to compliance tightening and cross-border academic mobility. These systems reduce physical exam infrastructure dependency by 30%, lowering institutional costs and expanding scalability. Vendors are responding with hybrid AI-human monitoring models and encrypted browser-based testing tools. Interestingly, schools using integrated proctoring platforms report 22% fewer exam integrity incidents, strengthening trust in digital assessment ecosystems.

Shift Toward Competency-Based Testing Competency-based evaluation frameworks are now adopted by 52% of curriculum boards in advanced education systems, replacing traditional rote assessment models. India’s NEP-aligned schools have increased skill-based testing integration by 39%, improving learning outcome tracking efficiency by 28%. This transition is driving demand for adaptive question banks and modular testing structures. Companies are redesigning platforms to support real-time skill mapping and analytics dashboards. A key operational change is the move from annual exams to continuous assessment cycles, improving student performance tracking frequency by 33%, enhancing instructional precision.

Cloud-Led Assessment Infrastructure Expansion Cloud-based testing platforms now support over 60% of digital exam deployments in North America, reducing infrastructure costs by 25% compared to on-premise systems. Southeast Asia is witnessing rapid migration, with digital exam penetration increasing by 44% in urban school networks. This shift is driven by scalability needs and centralized data governance requirements. Providers are investing in multi-tenant cloud architectures and localized data centers to ensure compliance and latency optimization. A notable insight is that institutions using hybrid cloud models achieve 29% faster system uptime recovery, significantly improving exam continuity and reliability.

Digital assessment platforms dominate the market due to their scalability, integration capability, and real-time analytics, accounting for nearly 58% of total deployments across developed education systems. These platforms support automated grading, adaptive testing, and centralized performance tracking, reducing administrative workload by approximately 35%. Traditional paper-based testing still exists but is steadily declining, representing less than 25% of active institutional use as digital migration accelerates in both public and private school networks. The fastest-growing segment is AI-based adaptive testing tools, expanding rapidly with adoption increasing by over 42% in digitally advanced education systems. Hybrid assessment tools combining analytics and automated feedback are also gaining traction, particularly in Asia-Pacific school reforms. Companies are investing in AI engine upgrades, cloud-native architectures, and interoperability frameworks to strengthen platform integration.

Exam management remains the leading application, accounting for nearly 47% of deployments due to its critical role in standardized testing, certification, and institutional benchmarking. Schools across the United States and Europe rely heavily on centralized exam platforms to ensure compliance and reduce grading inconsistencies by up to 33%. Learning analytics is the fastest-growing application, with adoption rising by 40% as institutions shift toward data-driven instruction and continuous assessment models. Other applications, including formative assessment and student performance tracking, are gaining steady traction as education systems move toward personalized learning ecosystems. Adaptive learning integration is improving student retention metrics by 28%, while automated reporting tools are reducing administrative processing time by 30%. Companies are scaling modular application suites and integrating AI-driven dashboards to meet evolving institutional requirements.

Public school systems represent the dominant end-user group, accounting for nearly 54% of global deployment due to large-scale standardized testing requirements and government-backed digital education initiatives. Their adoption is driven by centralized procurement models and nationwide curriculum standardization, improving assessment coverage efficiency by approximately 31%. Private educational institutions are increasingly adopting advanced platforms, particularly in North America and India, where digital test adoption has increased by 38% in competitive academic environments. The fastest-growing end-user segment is tutoring and test-prep providers, expanding rapidly with a 44% rise in digital assessment tool integration to support personalized learning and exam readiness. Higher education institutions and vocational training centers also continue adopting hybrid assessment systems for skill validation and certification. Companies are responding through customized SaaS pricing models, institutional partnerships, and localized deployment strategies.

North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 9.2% between 2026 and 2033.

North America dominates with around 38% regional share, driven by large-scale deployment of cloud-based testing platforms across U.S. school districts and Canada’s standardized assessment frameworks. Over 62% of K-12 institutions in the U.S. now use digital assessment systems integrated with LMS platforms, enabling real-time analytics and automated grading. Federal and state-level digital learning mandates continue accelerating infrastructure modernization, while cybersecurity compliance requirements are pushing investment in secure exam ecosystems. EdTech vendors are expanding partnerships with school boards to scale adaptive testing tools. A key operational development includes multi-state rollout of AI-assisted scoring systems, reducing administrative assessment workloads by nearly 30%, improving system efficiency and institutional reporting speed.

United States Market Outlook: The United States leads regional adoption with deep integration of AI-based testing platforms across public school districts. Nearly 65% of large districts now operate hybrid digital exam systems, supported by strong EdTech investment exceeding traditional education IT budgets. Expansion of cloud-first education infrastructure and nationwide digital curriculum initiatives continues to strengthen platform scalability and vendor penetration.

Europe holds approximately 27% market share, supported by strong regulatory alignment around digital education frameworks and standardized assessment reforms across countries like the UK, Germany, and France. Over 55% of secondary schools have adopted digital testing platforms, driven by national education modernization programs and cross-border academic standardization efforts. GDPR compliance is shaping platform design, increasing demand for secure, privacy-focused assessment systems. Vendors are expanding partnerships with education ministries to ensure compliance and scalability. A notable development includes EU-backed digital learning initiatives improving exam digitization efficiency by nearly 28%, strengthening institutional adoption across public education networks.

Germany Market Outlook: Germany leads Europe’s adoption with strong vocational and academic assessment digitization, supported by structured federal education policies. Around 60% of institutions now utilize blended assessment models combining digital and classroom evaluation systems. Investment in secure cloud infrastructure and AI-based evaluation tools is increasing, improving assessment accuracy and reducing administrative processing time by approximately 25%.

Asia-Pacific accounts for around 24% market share, driven by massive student populations, rapid EdTech adoption, and government-backed digital education reforms in India, China, and Southeast Asia. Over 68% of urban schools in China now utilize digital assessment platforms, while India has expanded online testing penetration by nearly 42% through NEP-aligned reforms. Infrastructure expansion and smartphone-based learning ecosystems are accelerating deployment scalability. Vendors are focusing on localized language support and low-bandwidth platforms to improve accessibility. A key development includes regional cloud education infrastructure investments improving system uptime reliability by 30%, enabling large-scale exam digitization.

China Market Outlook: China leads the region with strong centralized digital education infrastructure and large-scale standardized testing systems. More than 70% of urban schools now use AI-supported assessment tools, backed by national smart education initiatives. Continued investment in cloud computing and AI education platforms is strengthening system scalability and improving evaluation efficiency across provincial education networks.

South America holds around 7% market share, with adoption driven by increasing digital education investments in Brazil, Chile, and Argentina. Over 45% of private schools in Brazil have adopted online assessment systems, while public education digitization remains uneven due to infrastructure gaps. Internet penetration improvements have increased digital exam accessibility by nearly 33%, supporting gradual market expansion. Vendors are focusing on cost-effective cloud-based solutions and partnerships with telecom providers to improve connectivity. A key challenge remains inconsistent infrastructure, but government-led education modernization programs are improving deployment consistency across urban centers.

Brazil Market Outlook: Brazil leads the region with strong private education adoption and expanding EdTech investments. Nearly 48% of schools in urban regions use digital assessment platforms, supported by federal digital education initiatives. Increasing investment in broadband expansion and school digitalization programs is improving exam delivery reliability and supporting long-term platform scalability.

Middle East & Africa account for around 4% market share, driven by national education modernization programs in the UAE, Saudi Arabia, and South Africa. Over 40% of Gulf Cooperation Council (GCC) schools now use digital assessment tools, supported by smart classroom initiatives and EdTech partnerships. Infrastructure modernization projects are improving digital access, while cloud adoption is increasing across private education institutions. Deployment of AI-based testing systems has improved assessment efficiency by nearly 26%, particularly in urban school networks. Vendors are partnering with ministries of education to scale secure, bilingual assessment platforms.

United Arab Emirates Market Outlook: The UAE leads regional adoption with advanced smart education infrastructure and nationwide digital testing frameworks. Nearly 65% of schools in major emirates use integrated assessment platforms, supported by strong government investment in AI-driven education systems. Continuous expansion of cloud-first learning ecosystems is enhancing scalability and improving standardized exam efficiency across public and private institutions.

Global K-12 Testing and Assessment market competition is led by Pearson, ETS, Cambium Assessment, Instructure, and Renaissance Learning, competing against agile regional EdTech providers and AI-native assessment startups. Global leaders control nearly 58% combined share, leveraging deep institutional contracts, while regional players in Asia and Latin America focus on cost-efficient, localized platforms. Competition is effectively structured as global integrated assessment vendors versus fast-scaling digital-first innovators targeting underserved school systems. Technology differentiation drives 42% performance advantage, while pricing variance of nearly 25% creates segmentation between premium and budget platforms. Key competition axes include AI scoring accuracy, platform interoperability, deployment speed, and curriculum customization. Firms are aggressively expanding through acquisitions, cross-border partnerships, and cloud infrastructure integration, while also investing in vertical LMS-AI stacks. A major shift is consolidation around AI-enabled ecosystems, increasing entry barriers due to data governance and compliance requirements. Winning requires scalable AI accuracy, regulatory compliance strength, and seamless multi-country deployment capability under fragmented education systems.

Educational Testing Service (ETS)

Cambium Assessment

Instructure

Renaissance Learning

Prometric

ACT

McGraw Hill

D2L (Desire2Learn)

Raptor Technologies

Follett Learning

Learnosity

AI-driven adaptive assessment engines are the most impactful current technology, improving grading accuracy by 34% and reducing evaluation time by 38% across digitally enabled school systems. Nearly 57% of modern platforms now integrate AI-based question generation and automated scoring, enabling real-time performance diagnostics. Cloud-native LMS integration further enhances scalability, cutting infrastructure costs by 28%, while improving system uptime reliability by 30% compared to legacy on-premise systems. These technologies are redefining assessment efficiency and enabling personalized learning at scale.

Emerging biometric proctoring and behavioral analytics tools are gaining traction, with adoption rising to 41% in high-stakes exam environments, improving exam integrity by 33%. Edge-based testing solutions are also reducing latency by 25%, especially in low-connectivity regions. Companies adopting full-stack AI assessment ecosystems gain a 22% operational advantage over fragmented tool users. Between 2026–2028, integration of generative AI feedback systems will accelerate continuous assessment models, reshaping competitive advantage around real-time learning intelligence and predictive student performance tracking.

May 2025 – Cambium Assessment: Cambium announced expansion of its digital assessment ecosystem after delivering 130M+ online assessments in 2025, reinforcing large-scale testing capacity across U.S. states and improving simultaneous test handling efficiency by 24%. This strengthens statewide exam modernization and scalable digital testing delivery. Source: www.businesswire.com

May 2025 – Renaissance: Renaissance launched its Core Publisher Experience integrating AI-driven assessment and curriculum alignment, improving real-time instructional decision-making across classrooms by nearly 35% through Star Assessment integration. This enhances district-level personalization and accelerates data-driven teaching adoption.

June 2025 – McGraw Hill & Pearson: McGraw Hill integrated Pearson assessment capabilities into its K-12 ecosystem, embedding PRoPL interim assessments across curriculum platforms used by millions of students, improving learning path personalization accuracy by 30% through unified data insights.

August 2025 – Renaissance: Renaissance introduced AI-powered enhancements for Star Assessments and multilingual learning tools, expanding Spanish-language assessment support and improving instructional targeting efficiency by approximately 28% across participating districts. This strengthens inclusive assessment adoption and classroom data utilization.

The report covers comprehensive segmentation across digital assessment platforms, AI-based testing tools, and hybrid evaluation systems, analyzing adoption trends across exam management, formative assessment, and learning analytics applications. It evaluates deployment patterns across public schools, private institutions, and tutoring providers, which together account for over 85% of global usage concentration. Regional analysis spans North America, Europe, Asia-Pacific, South America, and Middle East & Africa, highlighting infrastructure readiness, digital learning penetration, and policy-driven adoption differences.

The study provides strategic insights into AI-driven testing, cloud-based assessment infrastructure, biometric proctoring, and real-time analytics technologies shaping next-generation education systems. It supports investment planning, competitive benchmarking, and expansion strategies for 2026–2033, focusing on scalability, interoperability, and regulatory alignment. The report further examines emerging niche markets such as adaptive learning ecosystems and remote exam integrity solutions, offering actionable intelligence for stakeholders targeting long-term digital transformation in global K-12 education systems.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 1,105.0 Million |

| Market Revenue (2033) | USD 2,105.1 Million |

| CAGR (2026–2033) | 8.39% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Pearson; Educational Testing Service (ETS); Cambium Assessment; Instructure; Renaissance Learning; Prometric; ACT; McGraw Hill; D2L (Desire2Learn); Raptor Technologies; Follett Learning; Learnosity |

| Customization & Pricing | Available on Request (10% Customization Free) |