Reports

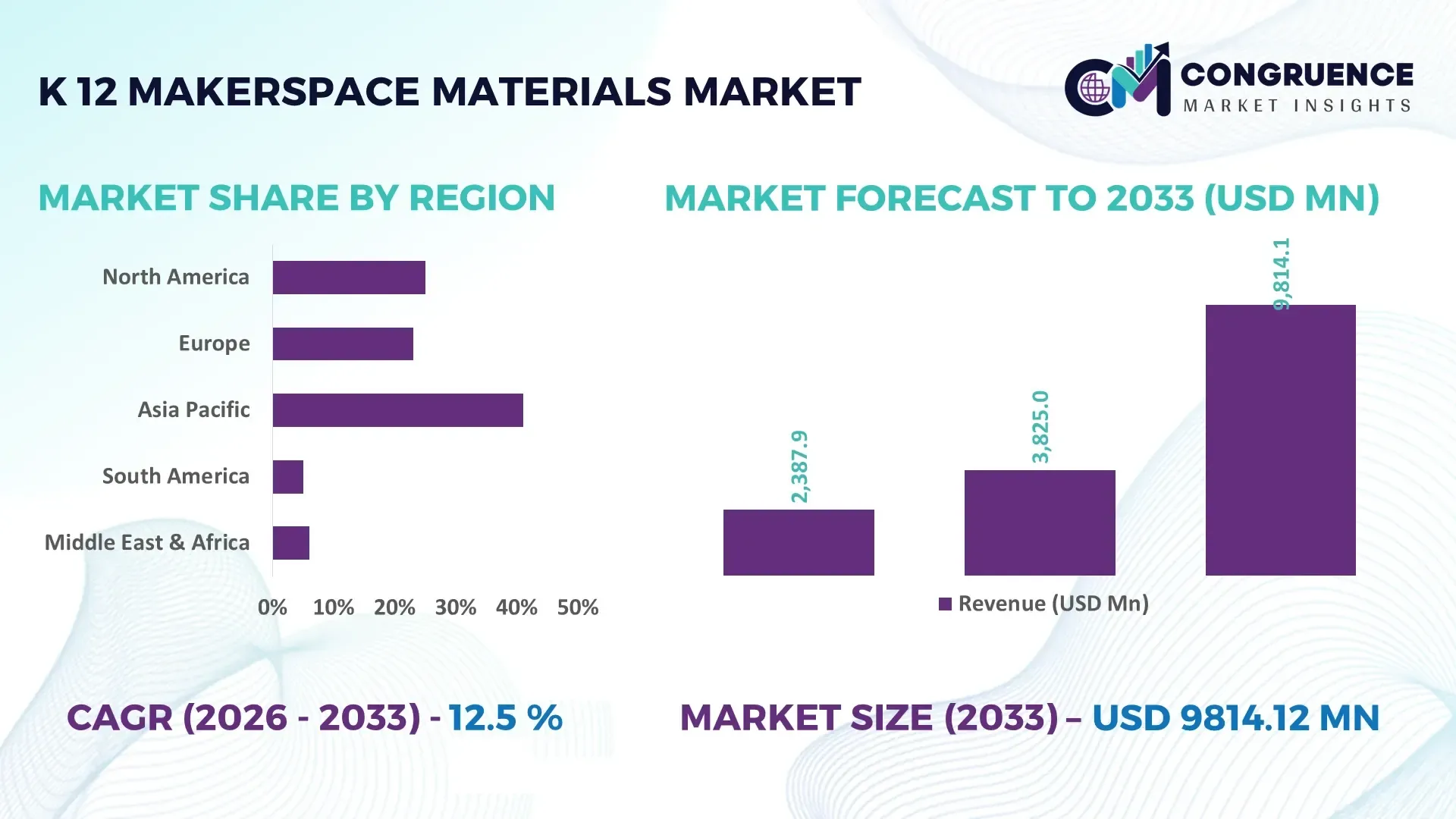

The Global K-12 Makerspace Materials Market was valued at USD 3825 Million in 2025 and is anticipated to reach a value of USD 9814.12 Million by 2033 expanding at a CAGR of 12.5% between 2026 and 2033. Rising integration of AI-enabled learning platforms, project-based STEM education, digital fabrication technologies, and curriculum-linked hands-on innovation programs is accelerating institutional procurement of advanced K-12 makerspace materials.

The United States accounts for nearly 36% of global K-12 makerspace materials deployment, supported by federal STEM initiatives, district-level digital learning investments, and widespread adoption of fabrication laboratories across public schools. More than 68% of newly established makerspaces integrate 3D printing, robotics, and electronics learning kits, while China continues expanding school innovation infrastructure through large-scale education modernization programs. Ongoing technology competition and national manufacturing resilience initiatives are further strengthening investments in future-ready classroom ecosystems.

Educational suppliers prioritizing scalable, sustainable, and curriculum-aligned makerspace portfolios will strengthen long-term procurement opportunities across institutional buyers.

Market Size & Growth: USD 3825 Million in 2025, projected to reach USD 9814.12 Million by 2033 at a CAGR of 12.5%, driven by expanding STEM education, AI-enabled classrooms, and digital fabrication adoption.

Top Growth Drivers: STEM curriculum expansion (+41%), classroom digitalization (+34%), and maker-based experiential learning adoption (+29%) continue accelerating institutional procurement.

Short-Term Forecast: By 2028, makerspace material utilization efficiency improves by 22% through inventory automation, standardized procurement, and digital resource management.

Emerging Technologies: AI-assisted design platforms, cloud-connected fabrication systems, recyclable polymers, and modular robotics kits are transforming advanced classroom innovation.

Regional Leaders: North America exceeds USD 3.8 Billion, Asia-Pacific surpasses USD 2.9 Billion, and Europe approaches USD 2.4 Billion through large-scale education modernization and regional expansion.

Consumer/End-User Trends: Over 63% of K-12 institutions prioritize reusable materials, modular STEM kits, and interdisciplinary project-based learning environments.

Pilot/Case Example: A 2026 district-wide makerspace implementation improved student engineering project completion by 31% while reducing material waste through standardized fabrication workflows.

Competitive Landscape: Leading suppliers collectively account for approximately 39% market share, with LEGO Education, Sphero, Makeblock, Cricut, and littleBits maintaining strong institutional presence.

Regulatory & ESG Impact: Sustainable procurement frameworks reduce single-use classroom materials by 24%, supporting circular education strategies and environmentally responsible purchasing.

Investment & Funding: More than USD 1.1 Billion in public-private funding supports manufacturing expansion, EdTech partnerships, and regional supply-chain diversification initiatives.

Innovation & Future Outlook: Smart makerspaces, AI-powered learning ecosystems, biodegradable fabrication materials, and connected classroom platforms are strengthening long-term competitive positioning.

Growing demand spans robotics laboratories, engineering classrooms, coding education, design thinking programs, and collaborative innovation spaces as institutions strengthen experiential STEM learning. AI-supported design software, sustainable fabrication materials, and modular electronics platforms continue improving classroom productivity, while over 58% of educational buyers prioritize interoperable learning ecosystems. Supply-chain regionalization and evolving education procurement standards are reinforcing product innovation and setting the foundation for the strategic discussion that follows.

The K-12 Makerspace Materials Market has become strategically important as education systems increasingly link STEM capability, workforce readiness, and advanced manufacturing skills to national competitiveness. School districts are shifting procurement from standalone classroom supplies toward integrated makerspace ecosystems combining robotics, fabrication tools, electronics, and sustainable materials. Infrastructure modernization and digital learning policies introduced after large-scale education reforms continue accelerating institutional investment, while localized sourcing strategies reduce procurement delays and strengthen supply resilience.

Modern modular makerspace platforms improve classroom resource utilization by nearly 25% compared with conventional project-based laboratories through reusable materials, AI-assisted design software, and centralized inventory management. The United States leads large-scale institutional deployment through district-wide STEM initiatives, while South Korea emphasizes technology-intensive makerspaces with higher automation density despite a smaller school base. During the next two to three years, more than 60% of newly established makerspaces are expected to incorporate cloud-connected learning platforms and interoperable fabrication equipment to improve operational consistency.

School systems are increasingly deploying modular robotics kits and recyclable fabrication materials through partnerships between education technology providers and curriculum developers, reducing material waste by approximately 20%. Companies are responding by expanding localized manufacturing, strengthening distributor networks, and developing curriculum-aligned product portfolios. Organizations capable of delivering scalable, standards-compliant, and technology-integrated makerspace solutions will secure stronger competitive positioning and long-term institutional procurement advantages.

Project-based STEM education is reshaping institutional procurement as schools integrate robotics, coding, engineering, and digital fabrication into core curricula. More than 68% of newly commissioned makerspaces now include programmable electronics and 3D fabrication resources, while reusable learning materials reduce classroom operating costs by nearly 18%. The United States continues expanding district-level innovation programs, encouraging long-term procurement frameworks instead of one-time equipment purchases. This structural transition is increasing demand for standardized, curriculum-aligned material portfolios. Manufacturers are responding through localized production, partnerships with educational technology providers, and expanded modular product lines that simplify deployment across multiple grade levels. A notable strategic advantage lies in companies offering interoperable materials compatible with multiple learning platforms, improving procurement efficiency and institutional retention.

Budget limitations and dependence on imported electronic components continue restricting large-scale makerspace deployment across public education systems. Specialized electronics, sensors, and microcontroller kits experience procurement cost fluctuations exceeding 16%, while shipping lead times remain approximately 20% longer for institutions dependent on overseas suppliers. Schools in developing economies frequently prioritize core infrastructure over advanced makerspace investments, delaying procurement cycles. Companies are reducing operational exposure by diversifying supplier networks, increasing regional assembly capacity, and negotiating long-term component contracts. Standardizing interchangeable materials and locally sourced classroom resources further minimizes procurement volatility while improving inventory planning and protecting institutional margins.

Artificial intelligence, adaptive learning software, and environmentally responsible fabrication materials are creating differentiated value across K-12 makerspace deployments. More than 62% of education technology providers are integrating AI-assisted design tools into classroom workflows, while recyclable polymers reduce material waste by nearly 24%. India is strengthening digital education infrastructure through large-scale smart classroom initiatives, creating opportunities for scalable makerspace ecosystems beyond metropolitan districts. Suppliers are increasing R&D investments in modular learning kits, cloud-connected classroom management platforms, and biodegradable fabrication materials. An emerging strategic opportunity lies in subscription-based replenishment models that combine consumables, software updates, and teacher training into integrated institutional procurement programs, strengthening long-term customer relationships.

Maintaining consistent makerspace performance across diverse school environments remains a significant execution challenge. Approximately 35% of institutions report shortages of qualified technical instructors, while interoperability issues between hardware, software, and curriculum platforms increase deployment complexity by nearly 22%. Japan and other advanced education markets emphasize standardized implementation, whereas many developing education systems continue operating with uneven digital infrastructure. Companies must invest in teacher certification programs, unified technology standards, and cloud-based device management to ensure consistent classroom outcomes. Strengthening ecosystem partnerships between hardware manufacturers, software developers, and curriculum providers has become essential for sustaining operational quality, competitive differentiation, and long-term institutional adoption.

AI-Enabled Classroom Workflows: AI-assisted design platforms and cloud-based makerspace management systems are becoming standard across advanced K-12 learning environments. More than 57% of newly deployed makerspaces integrate AI-supported project planning, while classroom preparation time declines by approximately 21% and equipment utilization improves by 18%. Digital education modernization and teacher productivity initiatives are accelerating adoption. Companies are expanding software partnerships and embedding analytics into makerspace ecosystems to improve operational visibility and curriculum alignment.

Localized Supply Chain Expansion: Procurement strategies are shifting toward regional manufacturing and inventory hubs following persistent logistics disruptions and education procurement reforms. Local sourcing has increased by nearly 24%, reducing average delivery cycles by 19% and lowering emergency procurement costs by 14%. Educational suppliers are restructuring distribution networks, increasing domestic assembly, and developing standardized component inventories. This transition enables faster institutional deployments while improving contract reliability for large school districts.

Sustainable Material Integration: Recyclable polymers, biodegradable craft materials, and reusable fabrication supplies are replacing conventional consumables as schools strengthen environmental procurement standards. Sustainable material adoption has increased by roughly 32%, while classroom waste falls by about 23% and consumable replacement frequency declines by 17%. Manufacturers are redesigning product portfolios, expanding certified sustainable materials, and collaborating with education partners to support long-term operational efficiency beyond regulatory compliance.

Modular Learning Kit Standardization: Schools increasingly prefer interoperable makerspace kits supporting robotics, coding, engineering, and design activities through common hardware platforms. Standardized modular systems improve equipment compatibility by approximately 28%, reduce teacher training requirements by 20%, and shorten deployment cycles by 16%. Technology transitions toward integrated STEM ecosystems are encouraging suppliers to develop scalable product families, strengthen curriculum partnerships, and simplify lifecycle management across multiple grade levels.

Robotics Kits represent the leading segment due to their broad curriculum integration, multi-disciplinary learning value, and compatibility with coding, engineering, and AI education programs. Nearly 42% of institutional makerspace deployments include robotics as their primary instructional platform because reusable hardware supports long-term classroom utilization and scalable lesson delivery. Electronics Kits remain strategically important through programmable sensors and microcontrollers, while Craft Materials continue serving foundational creativity and early-stage prototyping requirements. Coding Kits strengthen digital literacy initiatives by integrating seamlessly with robotics ecosystems. Suppliers continue expanding modular product portfolios and forming curriculum partnerships to improve institutional adoption and product interoperability.

3D Printing Materials are the fastest-growing segment as schools increasingly emphasize rapid prototyping and engineering design. Adoption of classroom additive manufacturing materials has expanded by approximately 29%, while reusable filament solutions reduce material waste by nearly 18%. Companies are investing in recyclable materials, localized production, and integrated classroom fabrication solutions to improve procurement efficiency and operational scalability. Investment priorities are shifting toward complete fabrication ecosystems instead of standalone classroom consumables.

STEM Education continues to dominate application demand because it serves as the foundation for integrated science, engineering, mathematics, and technology instruction across K-12 institutions. Approximately 48% of makerspace deployments are primarily aligned with STEM curriculum frameworks, supported by district-wide innovation strategies and standardized classroom modernization programs. Robotics Learning strengthens practical engineering skills, while Coding Education continues expanding through AI and computational thinking initiatives. Project-Based Learning remains an important instructional model, encouraging interdisciplinary collaboration and long-term knowledge retention. Suppliers are integrating unified learning platforms to improve curriculum compatibility and simplify deployment.

Design & Prototyping is emerging as the fastest-growing application as schools adopt fabrication technologies supporting engineering design and innovation workflows. Deployment of digital prototyping activities has increased by nearly 31%, while collaborative project completion improves by approximately 22% through integrated makerspace environments. Companies are expanding educator training, cloud-connected fabrication platforms, and curriculum partnerships to support advanced classroom implementation and scalable instructional delivery.

Public Schools remain the dominant end-user because of their large enrollment base, centralized procurement frameworks, and government-supported STEM modernization initiatives. Nearly 61% of institutional makerspace installations occur within public education systems, enabling large-scale deployment of standardized robotics, electronics, and fabrication resources. Elementary Schools emphasize foundational creativity and introductory STEM activities, while Middle Schools increasingly integrate interdisciplinary engineering projects. Private Schools maintain steady adoption through specialized innovation programs and differentiated curriculum offerings. Manufacturers continue strengthening public-sector partnerships, localized distribution, and flexible procurement models to support broad implementation.

High Schools represent the fastest-growing end-user segment as demand rises for engineering design, advanced manufacturing exposure, and career readiness pathways. Deployment of sophisticated makerspace technologies has increased by approximately 33%, while AI-enabled engineering projects improve laboratory utilization by nearly 19%. Companies are developing advanced equipment bundles, certification-ready learning modules, and industry partnerships to strengthen workforce-oriented education. Competitive positioning increasingly depends on delivering scalable solutions supporting both introductory and advanced technical education.

North America accounted for the largest market share at 38.4% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a 14.1% CAGR between 2026 and 2033.

Institutional STEM Modernization Strengthens Procurement Leadership

North America maintains the highest deployment concentration through established STEM funding programs, advanced classroom infrastructure, and widespread integration of digital fabrication technologies across K-12 education. The region contributes approximately 38.4% of global demand, supported by centralized district procurement and strong EdTech partnerships. More than 67% of newly developed innovation classrooms include robotics, electronics, and additive manufacturing resources. School systems increasingly standardize makerspace specifications, enabling suppliers to deliver interoperable product ecosystems and long-term service agreements. Investments in curriculum-aligned digital learning environments continue improving operational efficiency while supporting scalable implementation across urban and suburban education networks.

United States Market Outlook: The United States remains the regional leader due to its extensive public-school infrastructure, federal STEM initiatives, and mature educational technology ecosystem. Nearly 70% of large school districts have expanded hands-on STEM learning through makerspace programs, supported by procurement frameworks emphasizing interoperability and curriculum alignment. Manufacturers continue strengthening domestic distribution, educator training partnerships, and modular product portfolios, enabling faster deployment while improving institutional purchasing consistency across multiple states.

Sustainable Procurement and Digital Education Drive Market Evolution

Europe continues strengthening makerspace adoption through digital education strategies, sustainability requirements, and curriculum modernization initiatives. Approximately 27% of global deployment activity originates from the region, supported by coordinated investments in STEM learning infrastructure and environmentally responsible procurement policies. Nearly 46% of institutional buyers prioritize recyclable classroom materials and reusable fabrication resources within purchasing specifications. Educational suppliers increasingly align product development with circular economy objectives while expanding partnerships with schools and technology providers to improve deployment consistency and long-term operational value.

Germany Market Outlook: Germany leads the European market through its advanced engineering education ecosystem, strong manufacturing base, and nationwide emphasis on technical skills development. More than 58% of secondary schools implementing advanced STEM laboratories have incorporated makerspace resources supporting robotics and engineering design. Domestic suppliers continue expanding localized manufacturing, collaborative research initiatives, and vocational education partnerships to strengthen technology adoption while maintaining high equipment quality and curriculum integration.

Manufacturing Scale and Education Digitalization Accelerate Deployment

Asia-Pacific represents the fastest-expanding regional market, supported by extensive manufacturing capability, education digitalization programs, and rising investment in innovation-based learning. The region contributes approximately 25% of global deployment activity while maintaining the largest production ecosystem for robotics components, electronics kits, and classroom fabrication materials. More than 61% of newly established smart schools incorporate makerspace resources within STEM laboratories. Manufacturers continue expanding localized production, regional logistics networks, and curriculum partnerships to improve affordability and deployment efficiency across rapidly modernizing education systems.

China Market Outlook: China remains the region's most influential market through large-scale education infrastructure development, integrated manufacturing capacity, and strong government support for digital learning. Over 65% of newly equipped innovation classrooms include programmable robotics and digital fabrication equipment. Domestic manufacturers are investing in intelligent classroom ecosystems, localized component production, and AI-enabled educational platforms, strengthening both export competitiveness and domestic institutional adoption.

Education Infrastructure Investment Expands Practical Learning

South America is gradually increasing makerspace deployment as governments prioritize STEM capability, digital education access, and technical workforce preparation. Approximately 5% of global market activity is concentrated within the region, with deployment primarily occurring through public education modernization initiatives. Institutional procurement has increased by nearly 18% for modular robotics and coding resources supporting project-based instruction. Companies are expanding regional distributor partnerships and localized training programs while addressing infrastructure disparities that continue influencing implementation speed across rural education systems.

Brazil Market Outlook: Brazil leads the regional market through its large public education network, expanding digital learning initiatives, and growing educational technology ecosystem. Nearly half of recently modernized STEM classrooms incorporate robotics or coding-focused makerspace resources. Suppliers are strengthening partnerships with state education authorities, improving local inventory availability, and introducing cost-efficient modular learning kits designed to support large-scale classroom deployment within budget-sensitive institutions.

National Education Transformation Drives Technology Adoption

The Middle East & Africa market is expanding through education diversification strategies, smart school investments, and technology-focused curriculum reforms. The region represents approximately 4.6% of global deployment, supported by government-led modernization programs and increasing collaboration with international education technology providers. More than 35% of newly developed innovation schools incorporate makerspace laboratories emphasizing robotics and engineering education. Companies continue investing in regional partnerships, educator training, and localized support services to improve implementation quality while addressing infrastructure variability across emerging education systems.

United Arab Emirates Market Outlook: The United Arab Emirates leads regional adoption through advanced smart education policies, high digital infrastructure readiness, and sustained investment in innovation-focused learning environments. Approximately 60% of newly commissioned government-supported schools include dedicated STEM and makerspace facilities. Technology suppliers continue expanding strategic alliances with education authorities, introducing AI-enabled classroom platforms and integrated fabrication resources that strengthen operational efficiency and long-term institutional capability.

The competitive landscape is shaped by LEGO Education, Sphero, Makeblock, Cricut, and littleBits competing against regional STEM kit manufacturers, curriculum-focused suppliers, and low-cost educational hardware providers. Global technology leaders compete through integrated learning ecosystems, while regional suppliers emphasize pricing flexibility and localized curriculum alignment. The top five participants collectively control approximately 39% of the market, creating a moderately consolidated structure. Competition centers on technology integration, procurement efficiency, product customization, and supply-chain responsiveness. Modular product ecosystems reduce deployment complexity by nearly 24%, localized manufacturing lowers delivery times by approximately 18%, and standardized platforms improve institutional retention by around 21%. Companies are expanding regional distribution, forming curriculum partnerships, investing in AI-enabled learning tools, and vertically integrating consumables with software platforms. The competitive shift favors complete makerspace ecosystems over standalone classroom products as procurement increasingly values interoperability. The primary entry barrier remains curriculum validation combined with institutional procurement cycles. Winning requires scalable technology, localized supply capability, curriculum integration, and long-term education partnerships.

LEGO Education

Sphero

Makeblock

Cricut

littleBits

Arduino

Raspberry Pi

Ultimaker

Prusa Research

xTool

Thames & Kosmos

Pitsco Education

PASCO Scientific

TinkRworks

Artificial intelligence, cloud-connected classroom platforms, and digital fabrication technologies are becoming the operational foundation of advanced K-12 makerspaces. More than 58% of newly deployed learning environments integrate AI-assisted design or automated project management, reducing lesson preparation time by approximately 22%. Connected robotics platforms, programmable electronics, and centralized device management improve classroom utilization while enabling educators to monitor project progress through unified digital ecosystems. Institutions adopting integrated technology stacks achieve greater curriculum consistency and simplified equipment administration across multiple grade levels.

Emerging technologies include recyclable 3D printing materials, modular robotics architectures, edge-enabled microcontrollers, and interoperable coding environments. Compared with conventional standalone laboratory equipment, modular connected makerspace platforms improve equipment utilization by nearly 27% while reducing maintenance effort by approximately 19%. Technology innovators and curriculum-integrated solution providers gain the strongest competitive advantage because schools increasingly prefer interoperable ecosystems over isolated hardware purchases. Deployment of cloud-managed fabrication laboratories continues expanding as institutional buyers prioritize scalability, lifecycle management, and standardized classroom experiences.

Between 2026 and 2028, AI-driven adaptive learning, digital twins for engineering education, and predictive equipment diagnostics will reshape makerspace operations. More than 65% of advanced institutional deployments are expected to incorporate connected analytics supporting resource optimization and personalized instruction. Companies investing in integrated hardware, software, educator training, and sustainable fabrication materials will strengthen competitive positioning through lower operating costs, faster deployment, and stronger long-term institutional retention.

November 2024 Amazon launched its first Future Engineer Makerspace in Bengaluru with The Innovation Story, targeting hands-on robotics, AI, and 3D printing education for 4,000 students. The initiative expanded practical STEM access and strengthened early makerspace adoption across underserved schools. Source: The Economic Times

January 2026 LEGO Education introduced its Computer Science & AI learning solution featuring 30 curriculum-aligned lessons for K-8 classrooms. The platform expanded hands-on AI education while enabling schools to integrate computer science into existing STEM programs with standardized instructional resources.

March 2026 LEGO Education announced its partnership with FIRST will conclude after the 2026–2027 season, marking a strategic shift toward independently developed STEM learning programs. The decision reshapes the competitive ecosystem for school robotics and makerspace platforms worldwide. Source: Brick Fanatics

April 2026 Autodesk expanded its partnership with Howard University through a USD 1.95 million investment supporting an AI-powered digital fabrication makerspace. The initiative strengthens advanced engineering education while demonstrating increasing enterprise investment in collaborative makerspace infrastructure and workforce readiness. Source: StreetInsider

The report provides comprehensive analysis of market structure, competitive dynamics, technology evolution, procurement strategies, and operational developments shaping the K-12 Makerspace Materials Market between 2026 and 2033. It evaluates Robotics Kits, 3D Printing Materials, Electronics Kits, Craft Materials, and Coding Kits across STEM Education, Robotics Learning, Coding Education, Design & Prototyping, and Project-Based Learning. The assessment also covers Elementary Schools, Middle Schools, High Schools, Public Schools, and Private Schools, while benchmarking adoption patterns across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa.

The study incorporates technology deployment trends, AI-enabled learning platforms, sustainable materials, digital fabrication ecosystems, and regional supply-chain developments influencing institutional procurement. More than 60% of advanced school deployments emphasize interoperable makerspace solutions, while competitive benchmarking profiles leading manufacturers, innovation strategies, partnership activity, and product positioning. The report supports investment prioritization, regional expansion planning, portfolio optimization, procurement decisions, competitive positioning, and long-term strategic planning through detailed segmentation and operational intelligence.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2025 | USD 3825 Million |

Market Revenue in 2033 | USD 9814.12 Million |

CAGR (2026 - 2033) | 12.5% |

Base Year | 2025 |

Forecast Period | 2026 - 2033 |

Historic Period | 2021 - 2025 |

Segments Covered | By Type

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | LEGO Education, Sphero, Makeblock, Cricut, littleBits, Arduino, Raspberry Pi, Ultimaker, Prusa Research, xTool, Thames & Kosmos, Pitsco Education, PASCO Scientific, TinkRworks |

Customization & Pricing | Available on Request (10% Customization is Free) |