Reports

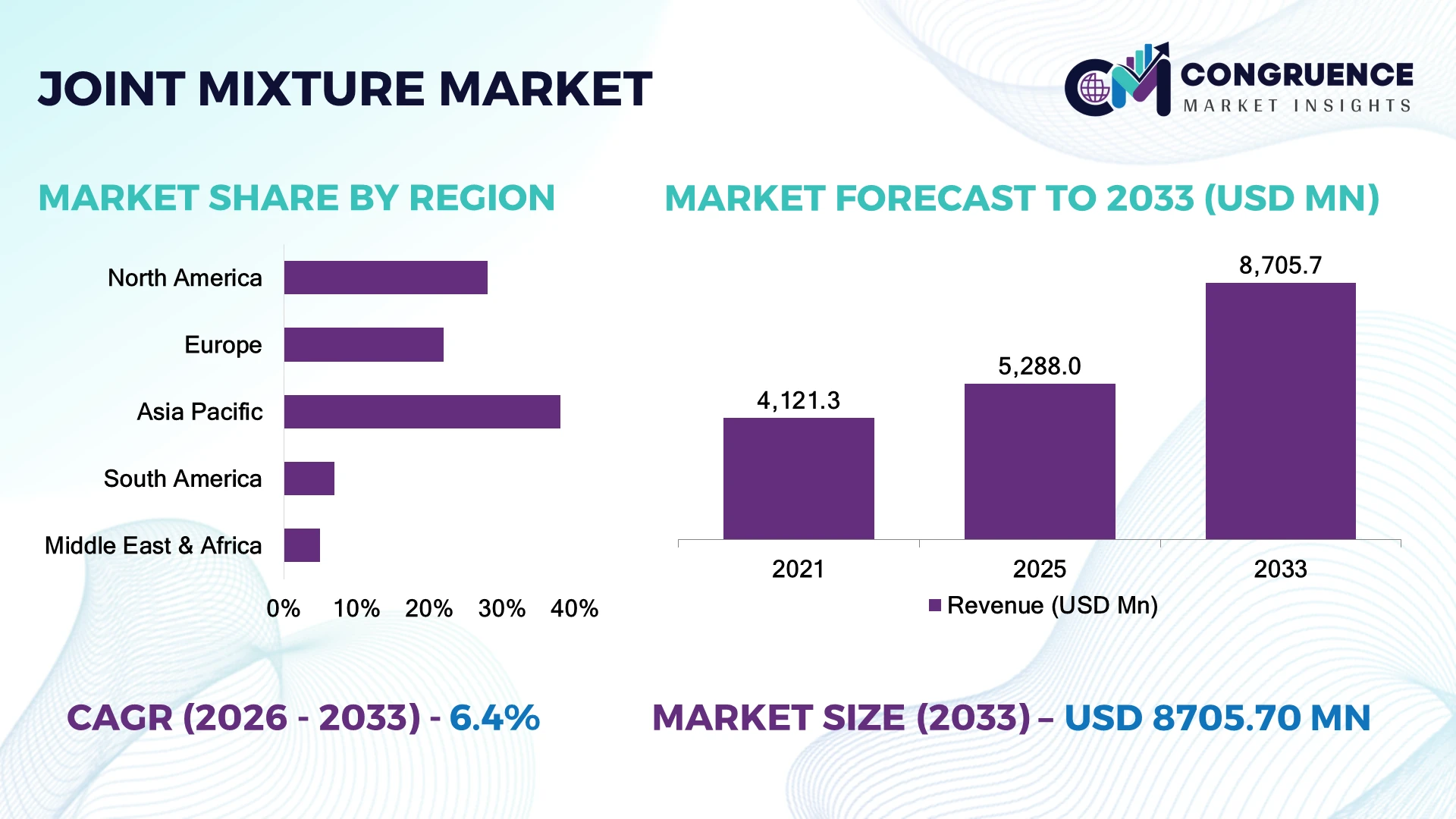

The Global Joint Mixture Market was valued at USD 5,288.0 Million in 2025 and is anticipated to reach a value of USD 8,705.7 Million by 2033 expanding at a CAGR of 6.43% between 2026 and 2033. Growth is driven by rising infrastructure rehabilitation projects, increasing adoption of high-performance construction materials, and demand for durable joint sealing solutions in commercial, industrial, and transportation applications.

China holds a leading position with around 32% market share due to extensive infrastructure modernization, urban development projects, and large-scale construction activity under initiatives such as the Belt and Road Initiative. The United States accounts for nearly 24% share, supported by bridge restoration programs, highway upgrades, and advanced construction technologies. China’s infrastructure spending exceeds USD 1 trillion annually, while the U.S. transportation infrastructure sector continues expanding through federal investment programs.

Strategic focus on regional production capacity and material innovation will define competitive advantage.

Market Size & Growth: USD 5,288.0 Million in 2025 to USD 8,705.7 Million by 2033 at 6.43% CAGR, supported by infrastructure repair and advanced construction material adoption.

Top Growth Drivers: Infrastructure refurbishment (35%), commercial construction expansion (28%), and demand for durable sealing solutions (22%).

Short-Term Forecast: By 2028, automated mixing technologies reduce material wastage by 15% and improve application efficiency by 20%.

Emerging Technologies: AI-based material optimization, automated mixing equipment, and polymer-enhanced joint compounds are reshaping product development.

Regional Leaders: Asia Pacific reaches USD 3.2 billion with urban infrastructure adoption; North America reaches USD 2.1 billion with renovation projects; Europe reaches USD 1.8 billion with sustainable construction practices.

Consumer/End-User Trends: More than 60% of contractors prioritize high-durability joint mixtures for long-life infrastructure projects.

Pilot/Case Example: In 2024, smart construction material trials reduced application errors by 18% in large-scale infrastructure projects.

Competitive Landscape: Leading manufacturers hold approximately 35% combined share, with key players including Sika AG, Saint-Gobain, MAPEI, BASF, and Fosroc.

Regulatory & ESG Impact: Green construction standards increased demand for low-emission materials by over 25% across developed markets.

Investment & Funding: More than USD 500 million invested in construction material innovation, focusing on advanced polymers and regional manufacturing expansion.

Innovation & Future Outlook: Next-generation joint mixtures with improved flexibility, faster curing, and recycled material integration are driving long-term industry transformation.

Joint mixture products are gaining importance across infrastructure, flooring, and industrial construction segments due to improved durability, faster installation, and enhanced resistance against environmental stress. Manufacturers are introducing polymer-modified formulations and low-maintenance solutions, with approximately 30% of new product launches emphasizing improved sustainability performance. Supply-chain localization and stricter construction standards are influencing procurement strategies globally, creating opportunities for advanced material suppliers.

The Joint Mixture Market is becoming strategically important as infrastructure owners, construction companies, and material manufacturers prioritize longer service life, reduced maintenance costs, and improved project efficiency. Aging transportation networks and accelerated urban development are increasing the need for advanced joint solutions capable of handling heavy loads, temperature variation, and environmental exposure.

The industry is shifting toward localized supply chains and technology-driven manufacturing as global construction markets respond to material shortages and sustainability regulations. Polymer-enhanced joint mixtures deliver improved flexibility and durability compared with traditional cement-based solutions, reducing repair frequency by nearly 20% in demanding applications.

Asia Pacific leads in deployment scale due to large infrastructure projects, while North America and Europe emphasize high-performance materials, renovation programs, and sustainable construction practices. Over the next 2–3 years, contractors are expected to increase adoption of automated application systems and digitally monitored construction processes.

Companies are expanding manufacturing capacity, forming technology partnerships, and investing in environmentally optimized formulations. Competitive positioning will depend on material innovation, supply reliability, and the ability to deliver efficient, durable, and sustainable joint mixture solutions.

Infrastructure rehabilitation programs and demand for high-durability construction materials are accelerating joint mixture adoption across transportation and industrial projects. More than 40% of global infrastructure spending is directed toward repair, maintenance, and modernization activities, increasing demand for specialized joint solutions. In the United States, bridge rehabilitation programs are expanding the use of polymer-modified mixtures, while China’s large-scale urban construction projects are supporting domestic material innovation. Companies are responding through investments in advanced formulations, automated production systems, and regional manufacturing facilities. The strategic advantage is shifting toward suppliers capable of delivering faster curing, improved flexibility, and lifecycle cost reductions for large infrastructure operators.

Joint mixture manufacturers face operational pressure from fluctuations in polymer, resin, and chemical additive costs, with raw material prices experiencing variations of nearly 15–20% in recent supply cycles. Dependence on specialty chemical suppliers in countries such as Germany, China, and the United States creates procurement risks and affects production margins. Regulatory requirements related to volatile organic compound emissions are also increasing compliance costs for manufacturers. Companies are reducing exposure through supplier diversification, localized production networks, and long-term procurement agreements. The key operational challenge is maintaining consistent product performance while controlling input costs across highly competitive construction material markets.

The market is opening new opportunities through eco-friendly formulations, automated application technologies, and digitally monitored construction processes. Sustainable joint mixture solutions incorporating recycled materials are gaining adoption, with green construction projects increasing demand for low-emission products by more than 25% in developed economies. Japan and Germany are advancing material efficiency through precision construction technologies and sustainability-focused infrastructure programs. Companies are expanding R&D partnerships to develop faster-curing compounds, improved weather-resistant mixtures, and application-specific solutions. A significant opportunity lies in integrating smart monitoring systems with joint materials to enable predictive maintenance, reducing repair cycles and creating value-driven service models for infrastructure owners.

Maintaining consistent performance across different climates, construction environments, and application conditions remains a major execution challenge for joint mixture suppliers. Approximately 30% of construction delays are linked to material compatibility issues, installation errors, or coordination gaps between contractors and suppliers. Extreme weather conditions in countries such as Canada, India, and Australia require specialized formulations that can withstand temperature fluctuations and heavy usage. Companies must address workforce training gaps, improve quality-control systems, and develop application guidelines for diverse infrastructure projects. Long-term competitiveness depends on achieving reliable field performance through advanced testing, contractor partnerships, and technology-enabled installation processes.

Advanced Polymer Formulations Rise Manufacturers are shifting toward polymer-modified and high-performance joint mixtures to improve flexibility, durability, and environmental resistance. Adoption of advanced formulations has increased by nearly 25% as infrastructure owners prioritize longer service life and reduced maintenance cycles. Construction companies in the United States and Germany are integrating enhanced joint compounds into bridge, industrial flooring, and commercial projects. Suppliers are responding through expanded R&D programs, strategic material partnerships, and localized production to reduce dependency on specialized chemical inputs.

Automation Improves Application Efficiency Automated mixing and precision application systems are transforming joint mixture installation workflows, reducing material waste by approximately 15% and improving project completion speed by nearly 20%. Large contractors in China and Japan are adopting digitally controlled equipment to achieve consistent quality across large infrastructure projects. Companies are investing in smart machinery partnerships and process automation to address skilled labor shortages and improve operational reliability.

Sustainable Materials Gain Adoption Environmental compliance and green construction requirements are accelerating the development of low-emission and recycled-content joint mixtures. Demand for sustainable construction materials has increased by more than 30% in major commercial projects as developers align with carbon reduction targets. European contractors are prioritizing eco-friendly formulations, encouraging manufacturers to redesign products with lower environmental impact and improved lifecycle performance.

Localized Supply Chains Expand Supply-chain disruptions in chemical raw materials are driving manufacturers to establish regional production networks and alternative sourcing strategies. More than 40% of construction material companies are increasing supplier diversification efforts to improve resilience. Companies are expanding manufacturing capacity in India, the United States, and Southeast Asia while forming regional partnerships to secure critical inputs and maintain delivery consistency.

Polymer-modified joint mixtures represent the leading type segment, accounting for approximately 42% of market adoption due to superior flexibility, bonding strength, and resistance to temperature variations compared with conventional cement-based mixtures. Their performance advantages make them highly preferred in transportation infrastructure, industrial flooring, and commercial construction applications. Traditional cementitious mixtures maintain a significant presence with nearly 35% share because of cost advantages and established contractor familiarity, particularly in developing construction markets. Fastest growth is observed in hybrid and advanced composite mixtures, supported by increasing demand for multifunctional materials that combine durability and sustainability benefits. Adoption of these solutions is expanding by nearly 20% annually in premium infrastructure projects. Manufacturers are increasing investments in formulation improvements, regional production, and contractor training programs. The shifting investment focus toward lifecycle performance is encouraging companies to move from low-cost materials toward application-specific joint mixture solutions.

Infrastructure repair and rehabilitation represent the dominant application segment, contributing nearly 45% of joint mixture consumption due to aging roads, bridges, and industrial structures requiring maintenance solutions. Government-led modernization programs in countries such as the United States, China, and India are increasing demand for durable joint systems capable of supporting heavy traffic and environmental stress. Commercial construction applications account for around 30% share, supported by rising use in flooring, warehouses, and large-scale facilities. The fastest-growing application is industrial and specialized construction, where adoption is increasing through automated installation methods and performance-focused material selection. Demand in this segment is expanding by approximately 22% as manufacturers develop mixtures designed for chemical resistance, vibration control, and extreme operating conditions. Companies are strengthening partnerships with contractors and engineering firms to customize products for specific project requirements. The market shift toward preventive maintenance is creating stronger demand for advanced joint solutions across infrastructure networks.

Infrastructure operators and government agencies represent the leading end-user segment with approximately 48% market share, driven by large-scale transportation networks, public construction programs, and maintenance requirements. These buyers prioritize long-lasting joint solutions that reduce downtime and improve asset reliability. Construction contractors follow with nearly 32% share as they integrate advanced joint mixtures into commercial, industrial, and residential projects. The fastest-growing end-user group is industrial facility operators, with adoption increasing by nearly 25% due to demand for durable flooring systems, manufacturing environments, and high-load applications. Companies are targeting this segment through customized formulations, technical support services, and direct partnerships with industrial developers. Smaller commercial users continue adopting ready-to-use solutions, while specialized engineering firms are influencing product selection through performance-based specifications. Future demand is shifting toward customers seeking complete material solutions rather than standalone products, encouraging manufacturers to expand technical consulting and application support capabilities.

Asia-Pacific accounted for the largest market share at 38% in 2025 however, Middle East & Africa is expected to register the fastest growth, expanding at a CAGR of 7.2% between 2026 and 2033.

North America accounted for approximately 28% of the global joint mixture market in 2025, supported by extensive transportation rehabilitation, commercial construction, and industrial flooring demand. The United States represents the largest contributor due to aging bridges, highway maintenance programs, and increased adoption of polymer-enhanced construction materials. More than 45% of major infrastructure contractors in the region are prioritizing durable repair materials to reduce lifecycle maintenance requirements. Canada is also expanding adoption through infrastructure modernization initiatives and climate-resistant construction practices. Manufacturers are strengthening local production capacity, automation capabilities, and contractor partnerships to improve supply reliability and application efficiency. The regional shift toward performance-based construction specifications is increasing demand for advanced joint mixture solutions.

United States Market Outlook: The United States remains the primary North American market due to large-scale infrastructure renewal programs and strong construction activity. Federal transportation modernization initiatives are supporting demand for specialized joint systems, with bridge and road rehabilitation projects representing a significant application base. Over 60% of large contractors increasingly evaluate material durability and maintenance reduction benefits during procurement decisions.

Europe accounted for nearly 22% of global joint mixture adoption in 2025, driven by strict construction standards, infrastructure refurbishment, and sustainability-focused building practices. Countries such as Germany, France, and the United Kingdom are accelerating demand for low-emission and high-performance joint materials across industrial and commercial projects. More than 30% of new construction specifications in developed European markets now include sustainability-related material criteria. Regulatory pressure around environmental performance is encouraging manufacturers to develop recyclable and low-VOC formulations. Companies are expanding research partnerships and upgrading production facilities to meet evolving technical requirements. The region’s mature construction sector is increasingly shifting from replacement-based maintenance toward preventive infrastructure management.

Germany Market Outlook: Germany leads Europe’s advanced construction material adoption due to strong industrial manufacturing capabilities and engineering expertise. The country’s focus on energy-efficient buildings and infrastructure modernization supports demand for durable joint solutions. More than 50% of industrial construction projects prioritize lifecycle performance, encouraging suppliers to introduce specialized formulations for manufacturing facilities and transportation assets.

Asia-Pacific dominated the joint mixture market with approximately 38% share in 2025, supported by rapid urbanization, infrastructure expansion, and manufacturing growth. China, India, Japan, and Southeast Asian economies represent major demand centers due to large transportation, commercial, and industrial construction projects. China contributes significantly through extensive infrastructure development, while India’s highway expansion and urban redevelopment programs are accelerating material adoption. More than 40% of regional demand is concentrated in infrastructure repair and large construction applications. Manufacturers are increasing local production, forming distribution partnerships, and introducing cost-efficient advanced mixtures to serve diverse project requirements. The region’s manufacturing strength provides advantages in material availability and supply-chain integration.

China Market Outlook: China remains the largest Asia-Pacific market due to its extensive infrastructure network and domestic construction material manufacturing base. Large-scale urban development and transportation projects continue driving joint mixture consumption. The country’s construction sector uses advanced material solutions across thousands of infrastructure projects annually, creating strong opportunities for suppliers with scalable production capabilities and localized technical support.

South America accounted for approximately 7% of global joint mixture demand in 2025, supported by infrastructure rehabilitation, mining operations, and commercial construction activity. Brazil represents the largest market due to its transportation networks, industrial facilities, and urban development projects. Infrastructure limitations and uneven construction investment remain key factors affecting adoption speed across several countries. However, increased focus on road maintenance and industrial modernization is improving demand for durable joint materials. More than 25% of construction companies in major South American economies are shifting toward higher-performance materials to reduce maintenance frequency. Suppliers are strengthening regional distribution networks and forming partnerships with contractors to improve market penetration.

Brazil Market Outlook: Brazil leads South America through its large construction sector, mining infrastructure, and transportation modernization requirements. The country’s expanding industrial facilities and road improvement programs are creating demand for reliable joint solutions. More than 35% of infrastructure-related construction activity involves rehabilitation and maintenance projects, supporting continued adoption of advanced joint mixtures.

Middle East & Africa accounted for approximately 5% of global joint mixture consumption in 2025, with demand concentrated in large-scale infrastructure, commercial developments, and industrial projects. Gulf countries are driving adoption through airport expansions, smart city developments, and high-value construction programs. Saudi Arabia and the United Arab Emirates are increasing usage of advanced construction materials to support long-term infrastructure performance. More than 20% of major construction projects in Gulf markets now incorporate enhanced durability requirements for materials exposed to extreme climates. Companies are expanding regional partnerships, improving supply networks, and introducing climate-resistant formulations. The market is transitioning toward premium solutions designed for harsh operating environments.

Saudi Arabia Market Outlook: Saudi Arabia represents the most strategically significant Middle Eastern market due to infrastructure transformation programs and large-scale urban development projects. The country’s construction modernization initiatives are increasing demand for durable joint systems in commercial, transportation, and industrial applications. More than 30% of major infrastructure projects emphasize long-life materials capable of operating under high-temperature conditions.

The Joint Mixture Market features global construction chemical leaders such as Sika, Saint-Gobain, MAPEI, BASF, and Fosroc competing against regional manufacturers focused on cost efficiency and localized supply. The top five players account for approximately 35% combined market share, creating a moderately consolidated structure. Competition is based on formulation technology, product durability, application speed, pricing, and technical support, with premium solutions capturing nearly 40% of infrastructure projects. Global players are expanding through acquisitions, partnerships, and manufacturing localization, while regional suppliers compete through lower costs and faster delivery. Innovation in polymer modification and sustainable formulations is shifting competition toward performance differentiation. Entry barriers remain high due to certification requirements, contractor relationships, and material expertise. Winning requires companies to combine advanced product development, reliable supply chains, customization capabilities, and strong application support to outperform established suppliers.

Saint-Gobain

MAPEI S.p.A.

BASF SE

Fosroc International

Pidilite Industries Limited

RPM International Inc.

H.B. Fuller Company

3M Company

Tremco Incorporated

Dow Inc.

Arkema Group

Advanced polymer chemistry is transforming joint mixture performance through flexible, weather-resistant, and high-strength formulations. Polymer-modified systems improve crack resistance and durability by approximately 20% compared with conventional materials, while automated blending technologies reduce production inconsistencies by nearly 15%. Construction chemical manufacturers are increasing adoption of precision formulation platforms to deliver application-specific solutions.

Digital construction workflows are integrating smart monitoring, automated dispensing equipment, and quality-control systems. These technologies improve installation accuracy by around 18% and reduce material waste during large infrastructure projects. Compared with manual preparation methods, automated application systems provide nearly 25% faster deployment, giving large contractors and global suppliers a competitive advantage through improved productivity.

Between 2026 and 2028, sustainable formulations and data-driven material selection will become major competitive differentiators. Low-emission joint mixtures, recycled-content materials, and predictive maintenance integration are gaining adoption across advanced construction markets. Companies investing in R&D partnerships and localized technology platforms will benefit from faster project execution, improved lifecycle performance, and stronger positioning with infrastructure developers.

June 2024 Sika expanded its joint sealing capabilities through integrated EMSEAL and Watson Bowman Acme solutions, strengthening construction joint offerings. The portfolio supports waterproof, seismic, and traffic applications across commercial infrastructure. The integration improved global solution coverage for specialized projects. Source: www.usa.sika.com

June 2024 Saint-Gobain announced the acquisition agreement for Fosroc, strengthening construction chemicals presence in India and Middle East markets. The transaction valued Fosroc at approximately USD 1 billion and supported expansion through broader product integration. Source: www.reuters.com

March 2025 Sika highlighted advanced joint sealing solutions featuring high movement capability of up to +100% and -50% for demanding construction applications. The development supports improved structural flexibility and longer service performance in building projects. Source: www.gbr.sika.com

May 2025 Fosroc continued promoting specialized joint sealant technologies including polyurethane, polysulphide, and methyl silyl solutions for construction applications. The product strategy strengthened performance-focused sealing adoption across infrastructure and industrial projects.

The Joint Mixture Market Report covers comprehensive analysis across major product types, including polymer-modified, cementitious, and advanced composite mixtures, along with applications spanning infrastructure repair, commercial construction, industrial facilities, and specialized projects. The study evaluates adoption patterns among infrastructure operators, contractors, industrial users, and commercial developers across North America, Europe, Asia-Pacific, South America, and Middle East & Africa.

The report examines technology trends, competitive positioning, supply-chain strategies, sustainability developments, and emerging opportunities shaping the market between 2026 and 2033. It provides strategic insights into material innovation, automation adoption, regional expansion, and investment priorities, helping companies identify growth opportunities, optimize product portfolios, strengthen partnerships, and improve competitive positioning in evolving construction environments.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 5,288.0 Million |

| Market Revenue (2033) | USD 8,705.7 Million |

| CAGR (2026–2033) | 6.43% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Companies Profiled | Sika AG; Saint-Gobain; MAPEI S.p.A.; BASF SE; Fosroc International; Pidilite Industries Limited; RPM International Inc.; H.B. Fuller Company; 3M Company; Tremco Incorporated; Dow Inc.; Arkema Group |

| Customization & Pricing | Available on Request (10% Customization Free) |