Reports

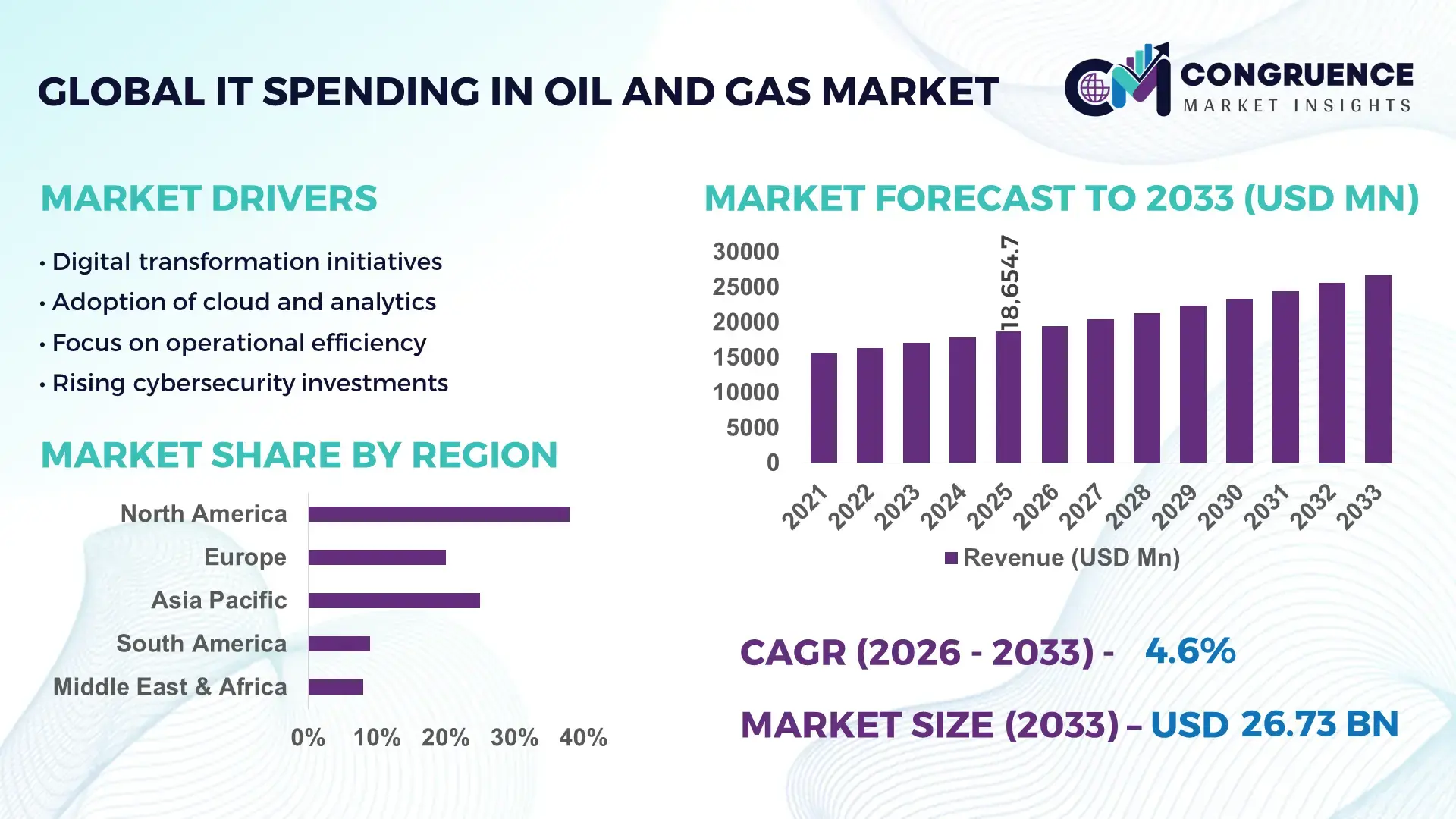

The Global IT Spending in Oil and Gas Market was valued at USD 18654.67 Million in 2025 and is anticipated to reach a value of USD 26732.6 Million by 2033 expanding at a CAGR of 4.6% between 2026 and 2033. This growth is driven by accelerated digital transformation efforts across upstream, midstream, and downstream operations that are enhancing efficiency and reducing operational risk.

The United States leads global IT spending in the oil and gas sector with substantial investments supporting extensive digital oilfield initiatives, advanced drilling analytics, and cloud-based asset management systems. In 2025, U.S. expenditure accounted for several billion USD in IT investments targeting predictive maintenance platforms, cybersecurity frameworks, and real-time monitoring networks deployed across shale, offshore, and pipeline operations. Companies increasingly integrate AI, IoT, and edge computing to optimize exploration and production, with more than half of major operators adopting cloud-native systems to handle large-scale data workloads. This robust technological infrastructure and high adoption rate of enterprise IT solutions underpin the country’s pivotal role in advancing digital capabilities in the sector.

Market Size & Growth: Valued at ~USD 18.65 B in 2025, projected to reach ~USD 26.73 B by 2033 at a CAGR of 4.6%, driven by digital transformation and operational optimization.

Top Growth Drivers: AI adoption (58%), IoT deployment (63%), cloud integration (55%).

Short‑Term Forecast: By 2028, cost efficiencies expected to improve with ~20% reduction in unplanned downtime across digital oilfield systems.

Emerging Technologies: Predictive analytics, digital twins, hybrid cloud infrastructure.

Regional Leaders: North America ~USD 9 B by 2033 (advanced IoT and cloud uptake); Europe ~USD 8 B by 2033 (focus on sustainability IT solutions); Asia‑Pacific ~USD 10 B by 2033 (rapid digital infrastructure build‑out).

Consumer/End‑User Trends: Upstream firms prioritize real‑time data analytics; midstream emphasizes pipeline monitoring; downstream invests in refinery automation.

Pilot or Case Example: 2025 digital twin deployment in a major North American basin reduced maintenance downtime by ~21%.

Competitive Landscape: Market leader IBM (~15%), followed by Microsoft, Oracle, SAP, Cisco.

Regulatory & ESG Impact: Increased cybersecurity mandates and compliance frameworks push IT investments; ESG reporting platforms adopted widely.

Investment & Funding Patterns: Recent IT capital expenditure exceeds USD 5 B globally, with venture funding focusing on AI and cloud solutions.

Innovation & Future Outlook: Expansion of edge computing, integration of blockchain for supply chain transparency, and advanced robotics for remote operations.

The IT Spending in Oil and Gas Market reflects dynamic sectoral shifts with upstream digitalization, midstream surveillance systems, and downstream process automation increasingly central to investment decisions. Recent innovations such as AI‑enabled predictive maintenance, high‑performance analytics platforms, and IoT sensor networks improve operational safety and efficiency while regional consumption patterns show strong growth in Asia Pacific driven by expanding refinery and pipeline infrastructure. Environmental regulations and economic drivers promoting cybersecurity and sustainable IT architectures further inform strategic technology adoptions, with future outlooks emphasizing integration of cloud‑native services and hybrid digital ecosystems that support real‑time decision‑making and asset optimization.

The IT Spending in Oil and Gas Market is strategically central to digital transformation agendas that drive operational excellence, cost management, and competitive differentiation across the energy sector. Investments in advanced analytics platforms, cloud-native infrastructure, and AI-driven automation deliver measurable efficiency gains, with predictive analytics delivering a 30% improvement compared to traditional reactive maintenance standards. In the competitive landscape, North America dominates in volume, while Europe leads in adoption with 68% of enterprises deploying advanced IT solutions across exploration, production, and midstream operations. Short-term projections emphasize that by 2028, edge computing integration is expected to cut unplanned downtime by 22% through real-time monitoring and remote management capabilities.

Strategically, firms are aligning IT spending with compliance and Environmental, Social, and Governance (ESG) commitments. Energy operators are committing to 30% reductions in greenhouse gas emissions intensity by 2030 through digital optimization of field operations, emissions monitoring systems, and predictive environmental risk assessment tools. In corporate micro-scenarios, a leading upstream operator in 2025 achieved a 27% improvement in drilling efficiency through the deployment of integrated AI-assisted drilling advisory systems, demonstrating how targeted IT investments translate into measurable operational gains.

Looking forward, IT Spending in Oil and Gas Market spending is positioned as a pillar of resilience, compliance, and sustainable growth—enabling digital-first business models, adaptive risk management frameworks, and strategic value generation across the energy sector.

Digital transformation initiatives are a primary driver of IT Spending in Oil and Gas Market growth, as energy companies seek to modernize legacy infrastructure with advanced technologies. Large-scale deployment of IoT sensors across drilling rigs and pipelines has increased operational visibility, enabling real-time monitoring that reduces unplanned outages by double-digit percentages. Companies are adopting cloud platforms for data consolidation and collaboration, with cloud uptake climbing above 60% across major operators. The integration of big data analytics supports predictive maintenance models that significantly lower equipment failure rates. Digitally enhanced supply chain systems improve inventory turnover and logistics coordination with measurable throughput improvements. These transformation efforts expand the scope of IT spending, as firms allocate capital to strategic projects that improve asset performance and competitive positioning in the face of fluctuating commodity prices and tightening regulatory requirements.

Rising cybersecurity risks present a significant restraint on the IT Spending in Oil and Gas Market, as integration of digital systems increases the attack surface for energy infrastructure. Oil and gas companies face persistent threats from ransomware, data breaches, and industrial control system intrusions, prompting firms to divert capital towards protective measures and risk mitigation. In recent years, energy sector cyber incidents have driven heightened concerns, leading to greater caution in technology deployment. Comprehensive security frameworks and compliance requirements add complexity and incremental cost burdens, slowing the pace of digital integration. The shortage of skilled cybersecurity professionals further challenges companies seeking to deploy advanced IT solutions securely. As a result, some operators delay or scale back digital initiatives until robust security measures are established, tempering market expansion.

AI-enabled asset optimization presents a compelling opportunity for the IT Spending in Oil and Gas Market, unlocking new performance enhancements across drilling, production, and maintenance operations. With AI models analyzing sensor-generated data at scale, companies can automate complex decision-making processes, reducing cycle times and manual intervention. Predictive maintenance systems, powered by machine learning, anticipate equipment degradation and schedule interventions that extend asset life while minimizing downtime. The emergence of digital twin technology provides virtual replicas of physical systems, enabling scenario planning and operational simulations that boost reliability and efficiency. Adoption of AI tools in logistics and supply chain functions improves demand forecasting and inventory allocation, leading to measurable reductions in carrying costs. As operators increasingly recognize the value of AI solutions, investment flows toward innovative IT projects that broaden capabilities and support strategic objectives.

Integration complexities pose a major challenge to the IT Spending in Oil and Gas Market, as firms must reconcile legacy systems with modern digital platforms. Many oil and gas operators maintain heterogeneous IT environments with disparate data formats, protocols, and vendor systems, complicating unified data management and interoperability. Upgrading infrastructure often requires extensive system reconfigurations, lengthy testing cycles, and cross‑functional coordination, delaying project timelines and increasing expenditures. Moreover, legacy equipment may lack digital interfaces, necessitating retrofits or middleware solutions to bridge connectivity gaps. The scarcity of skilled IT professionals with domain expertise in both industrial operations and advanced technologies further exacerbates integration efforts. These challenges can lead to implementation bottlenecks, increased project risk, and higher total cost of ownership, tempering the pace at which companies expand IT investments.

Rise in Modular and Prefabricated Construction: The adoption of modular and prefabricated construction techniques is transforming project execution in the IT Spending in Oil and Gas market. Around 55% of new projects report reduced costs and faster delivery timelines through off-site prefabrication of pre-bent and precision-cut components. Automated machinery minimizes labor needs and accelerates commissioning, with North America and Europe leading adoption at over 60% of major projects leveraging these practices for enhanced efficiency and safety.

Expansion of AI-Driven Predictive Maintenance: Operators increasingly implement AI-powered predictive maintenance platforms, improving equipment reliability and operational uptime. In 2025, installations of AI maintenance systems led to a 21% reduction in unplanned downtime and a 15% increase in machinery lifespan. Predictive analytics are now applied to over 70% of critical field assets in upstream and midstream operations, allowing faster anomaly detection and reduced emergency interventions.

Integration of Cloud and Edge Computing: Cloud and edge computing adoption is reshaping IT infrastructure, with 65% of enterprises deploying hybrid solutions to optimize data processing close to field operations. Edge-enabled monitoring allows real-time analysis of pipeline and drilling data, reducing latency by 30% compared to traditional centralized systems. This trend is particularly pronounced in Asia-Pacific, where rapid infrastructure growth demands scalable and agile IT platforms.

Proliferation of IoT-Connected Field Devices: The use of IoT sensors across drilling, pipeline, and refinery operations has expanded significantly, with over 80% of new installations in 2025 including smart sensors for temperature, pressure, and vibration monitoring. Real-time IoT integration has improved operational visibility, achieving a 25% reduction in equipment failures and enabling data-driven decision-making in remote or hazardous environments.

The IT Spending in Oil and Gas Market is segmented to reflect diverse infrastructure investments, enterprise applications, and end‑user priorities. By type, segmentation captures core IT categories such as enterprise resource planning (ERP), supervisory control and data acquisition (SCADA) systems, cloud computing services, and cybersecurity platforms, each supporting specific operational imperatives across exploration, production, and refining. Application segmentation details how IT expenditures are allocated to asset management, field operations optimization, risk and compliance monitoring, and supply chain digitization. End‑user insights reveal that upstream operators prioritize real‑time drilling analytics and predictive maintenance systems, while midstream segments emphasize pipeline integrity and remote monitoring technologies. Downstream facilities increasingly invest in automation, quality control, and regulatory compliance platforms. This layered segmentation enables decision‑makers to align technology priorities with business strategies that improve uptime, enhance safety, and streamline business workflows.

The leading IT type within the IT Spending in Oil and Gas Market is cloud computing services, accounting for approximately 38% share of total IT adoption due to widespread migration of enterprise systems and data analytics workloads to scalable platforms. SCADA systems hold around 30% share, sustaining legacy industrial control functions with high reliability. Meanwhile, cybersecurity platforms represent 18% share, reflecting the growing imperative to protect critical infrastructure. Other types, including mobile workforce solutions and edge computing devices, collectively represent the remaining 14% share, addressing niche requirements such as field data capture and low‑latency processing. Cloud adoption continues to expand because operators benefit from elastic storage, centralized data access, and integration with AI tools that enhance decision support.

In IT Spending in Oil and Gas Market applications, asset management systems lead with about 40% share, underpinning predictive maintenance, equipment tracking, and lifecycle optimization. Risk and compliance monitoring follows with 28% share, reflecting stringent regulatory reporting and safety oversight demands. Field operations optimization accounts for 20% share, focusing on real‑time drilling and production analytics, while supply chain digitization holds the remaining 12% share, enhancing logistics coordination and inventory forecasting. Field operations optimization is rising fastest as operators deploy digital twins and autonomous drilling support tools; these trends accelerate efficiency gains and reduce manual intervention.

Upstream operators are the dominant end‑user segment in the IT Spending in Oil and Gas Market, representing roughly 45% share, driven by investments in exploration analytics, reservoir modeling, and predictive maintenance tools. Midstream enterprises account for 30% share, with strong adoption of pipeline integrity monitoring and remote control systems. Downstream refiners contribute 25% share, prioritizing automation, quality assurance, and energy management platforms. Upstream remains the largest segment because of its complex asset base and high data processing requirements; however, downstream digital transformation is expanding rapidly, supported by advanced process control and analytics. Other relevant end‑users, such as service providers and drilling contractors, collectively represent additional adoption influence with approximately 15% combined share in specialized technology deployments.

North America accounted for the largest market share at 38% in 2025; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 5.1% between 2026 and 2033.

In North America, over 250 oil and gas operators have implemented advanced IT solutions across upstream and midstream operations, with enterprise adoption rates exceeding 65% for cloud and predictive analytics platforms. Europe follows with a 27% share, driven by regulatory compliance systems and digital twin deployments. Asia-Pacific represents 20% of global volume but leads in rapid IT infrastructure adoption in China, India, and Japan. South America accounts for 8%, with Brazil and Argentina accelerating digital automation in pipeline and refinery management. Middle East & Africa hold 7%, focusing on modernization of extraction, monitoring, and cybersecurity systems. Across these regions, investments in AI, IoT, edge computing, and predictive maintenance are reshaping operational efficiency and field-level decision-making, reflecting differentiated adoption patterns and technology preferences.

How are enterprises optimizing operational efficiency with advanced IT solutions?

North America commands approximately 38% of the IT Spending in Oil and Gas Market, led by major oil and gas hubs in the U.S. and Canada. Key industries driving demand include upstream shale production, midstream pipeline monitoring, and downstream refining operations. Regulatory changes such as stricter environmental reporting requirements and cybersecurity mandates have accelerated enterprise IT investments. Companies are implementing AI-driven predictive maintenance, cloud-based data platforms, and IoT-enabled monitoring systems, enhancing field productivity by over 20% in certain operations. Local players such as Schlumberger have deployed digital twin platforms to improve drilling efficiency across multiple U.S. basins. Regional consumer behavior shows higher enterprise adoption in real-time analytics, cybersecurity frameworks, and operational automation compared to other global markets, particularly in high-tech hubs and industrial zones.

How is digital compliance and sustainability shaping enterprise IT adoption?

Europe holds about 27% of the IT Spending in Oil and Gas Market, with Germany, the UK, and France representing the largest contributors. Regulatory oversight from bodies such as the EU Emissions Trading System drives investments in explainable IT, environmental monitoring, and risk management systems. Emerging technologies including AI, cloud analytics, and predictive maintenance are widely adopted, improving operational efficiency by up to 18% in refinery and upstream operations. Local companies like TotalEnergies have implemented integrated cloud and SCADA systems across their European assets, enhancing real-time production visibility. Regional consumer behavior emphasizes adherence to regulatory standards, ESG commitments, and sustainable IT adoption, which shapes the deployment of advanced analytics and compliance-focused digital platforms.

What factors are driving rapid IT infrastructure expansion in energy sectors?

Asia-Pacific accounts for 20% of the global IT Spending in Oil and Gas Market, with China, India, and Japan as top-consuming countries. The region is witnessing large-scale infrastructure projects, including pipeline expansions, offshore exploration, and refinery upgrades, which require extensive IT investment. Edge computing, cloud integration, and AI-assisted predictive maintenance are key technology trends driving efficiency improvements of 15–20% in operational workflows. Local players, such as Sinopec, have deployed IoT-enabled field monitoring platforms across hundreds of sites to enhance asset reliability. Consumer behavior reflects rapid adoption of mobile IT platforms, automation, and digital supply chain solutions, making the region a leader in technology-driven transformation.

How are digital automation and regulatory incentives shaping IT adoption?

South America holds roughly 8% of the IT Spending in Oil and Gas Market, with Brazil and Argentina as key contributors. Expansion in pipeline networks, refining, and offshore operations is driving investments in SCADA systems, cloud platforms, and predictive maintenance tools. Government incentives promoting local technological upgrades and favorable trade policies encourage adoption of advanced digital systems. Petrobras, a leading operator, has implemented cloud-based asset management solutions to enhance monitoring and reduce downtime across 150+ facilities. Regional consumer behavior emphasizes efficiency in process automation, energy monitoring, and technology localization, reflecting a growing focus on operational resilience and compliance with local standards.

What technological modernization initiatives are transforming oil and gas operations?

Middle East & Africa account for approximately 7% of the IT Spending in Oil and Gas Market, with major growth concentrated in the UAE and South Africa. Technological modernization includes IoT-enabled pipeline monitoring, AI-assisted predictive maintenance, and cloud-based operational analytics. Local regulations and trade partnerships support digital transformation projects, with government-backed programs incentivizing energy companies to adopt advanced IT systems. ADNOC in the UAE has implemented AI-driven drilling advisory platforms, improving field efficiency by 18%. Regional consumer behavior favors large-scale infrastructure digitization, cybersecurity integration, and remote operations, reflecting a high interest in modern IT applications despite variable adoption rates across countries.

United States: 35% market share – Dominates due to high production capacity, widespread adoption of digital oilfield technologies, and robust enterprise IT infrastructure.

China: 18% market share – Leads in adoption of AI, IoT, and cloud-based systems for upstream, midstream, and downstream operations, driven by large-scale infrastructure expansion and modernization initiatives.

The competitive environment in the IT Spending in Oil and Gas market is moderately consolidated yet includes a broad array of active technology providers, with over 60 companies competing globally. Top vendors collectively hold a combined share approximating 47–52% of the total market, indicating a competitive landscape where leading firms exert significant influence while a long tail of mid‑size specialists addresses niche segments. Major strategic initiatives shaping competition include partnerships, cloud product launches, AI and predictive analytics platforms, and managed services agreements with global oil majors. For example, several leading technology firms have expanded digital twin and IoT offerings, with adoption rates exceeding 55% among large upstream operators, and integrated cybersecurity enhancements that reduce incident response times by 30%. Technology leaders also engage in strategic alliances across regions to extend service portfolios and localize delivery models, with more than 40 new strategic collaborations announced in the past two years.

Innovation trends influencing competition include AI‑driven operational analytics, edge computing integration, and cloud‑native architecture rollouts that improve remote monitoring and real‑time decision‑making. Mid‑tier competitors are gaining traction through specialized solutions in asset management, edge device connectivity, and field automation, challenging incumbents with targeted offerings. Several firms are investing in cross‑industry platforms that enable seamless integration between IT (information technology) and OT (operational technology) stacks, providing enhanced scalability and security for oil and gas enterprises. The nature of the market reflects both consolidation around major platform providers and fragmentation where specialized IT services and software vendors serve defined sub‑segments.

SAP SE

Oracle Corporation

Cisco Systems, Inc.

Infosys Limited

Tata Consultancy Services (TCS)

Wipro Limited

HCL Technologies

Capgemini

Siemens AG

ABB Ltd.

Honeywell International Inc.

Schneider Electric

Dell Technologies

The IT Spending in Oil and Gas Market is increasingly shaped by a diverse set of current and emerging technologies that enhance operational efficiency, safety, and decision-making. Artificial intelligence (AI) and machine learning are widely deployed across upstream and midstream operations, enabling predictive maintenance for over 70% of critical field assets and reducing unplanned downtime by approximately 21%. AI-driven analytics also support reservoir modeling, production optimization, and anomaly detection, providing real-time insights that enhance both drilling efficiency and asset performance.

Cloud computing and hybrid cloud platforms have become foundational to IT infrastructure, supporting centralized data storage and multi-site access. Currently, more than 65% of large operators use cloud-enabled platforms to integrate data from remote wells, pipelines, and refineries, improving operational visibility and cross-functional collaboration. Complementing cloud systems, edge computing is deployed at field locations to process data locally, reducing latency by 30% compared to traditional centralized systems and enabling faster operational decisions.

IoT and sensor networks are driving digital transformation in field operations, with smart sensors deployed across over 80% of new drilling rigs and pipeline installations in 2025. These devices monitor temperature, pressure, vibration, and flow rates, providing actionable insights for predictive maintenance, leak detection, and energy optimization.

Emerging technologies, including digital twin platforms, robotic process automation (RPA), and blockchain-based supply chain solutions, are transforming asset management and operational transparency. Digital twins allow virtual simulations of equipment and pipelines, improving planning and reducing risk, while RPA automates repetitive operational tasks, enhancing efficiency by up to 15%. Blockchain solutions are being piloted in logistics and contract management, ensuring traceability and reducing administrative errors by over 20%. Collectively, these technologies position IT investments as a strategic lever for resilience, compliance, and innovation in the oil and gas sector.

• In June 2024, Microsoft expanded its strategic cloud partnership with Halliburton to accelerate digital transformation across upstream and downstream operations, enhancing data analytics, AI workloads, and edge‑to‑cloud orchestration for oil and gas IT environments.

• In May 2025, Capgemini secured a multi‑year contract with Shell to design and implement a scalable cloud and data platform for IT operations within the oil and gas sector, strengthening digital infrastructure and real‑time operational visibility.

• In April 2025, Infosys announced a strategic collaboration with Siemens to co‑create digital twin‑based solutions for energy assets, aimed at optimizing performance and predictive maintenance workflows across oil, gas, and energy sites.

• In November 2025, SLB introduced “Tela,” an AI‑driven tool integrated into its digital platform suite designed to automate workflows such as well log interpretation and drilling prediction, driving digital sales growth that rose 11% in Q3 compared to the prior quarter.

The IT Spending in Oil and Gas Market Report provides a comprehensive examination of the information technology expenditures and digital transformation initiatives within the global oil and gas industry. It encompasses a thorough review of market segmentation by product type — including cloud computing platforms, cybersecurity solutions, enterprise resource planning (ERP) systems, and supervisory control and data acquisition (SCADA) systems — and highlights how each supports upstream, midstream, and downstream operations. The report evaluates the deployment of advanced technologies such as AI‑driven predictive maintenance, IoT sensor networks for field monitoring, digital twin platforms, and edge computing solutions that enable real‑time decision‑making and operational resilience.

Geographically, the report covers regional dynamics across North America, Europe, Asia‑Pacific, South America, and Middle East & Africa, providing insights into market behavior based on infrastructure maturity, regulatory environments, and enterprise adoption patterns. Application analysis details how IT investments are allocated across asset management, risk and compliance monitoring, supply chain digitization, and field operations optimization. The report also assesses technology adoption trends and emerging niches such as blockchain for supply chain transparency, AR‑enabled field services, and hybrid cloud architectures tailored to oil and gas requirements. Additionally, it outlines competitive dynamics, innovation trends, and end‑user segments — including national oil companies, independent operators, and energy services firms — offering decision‑makers a clear view of the breadth and depth of IT spending priorities across the sector.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

4.6% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Microsoft Corporation Overview, IBM Corporation Profile, Accenture plc Company Details, SAP SE, Oracle Corporation, Cisco Systems, Inc., Infosys Limited, Tata Consultancy Services (TCS), Wipro Limited, HCL Technologies, Capgemini, Siemens AG, ABB Ltd., Honeywell International Inc., Schneider Electric, Dell Technologies |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |