Reports

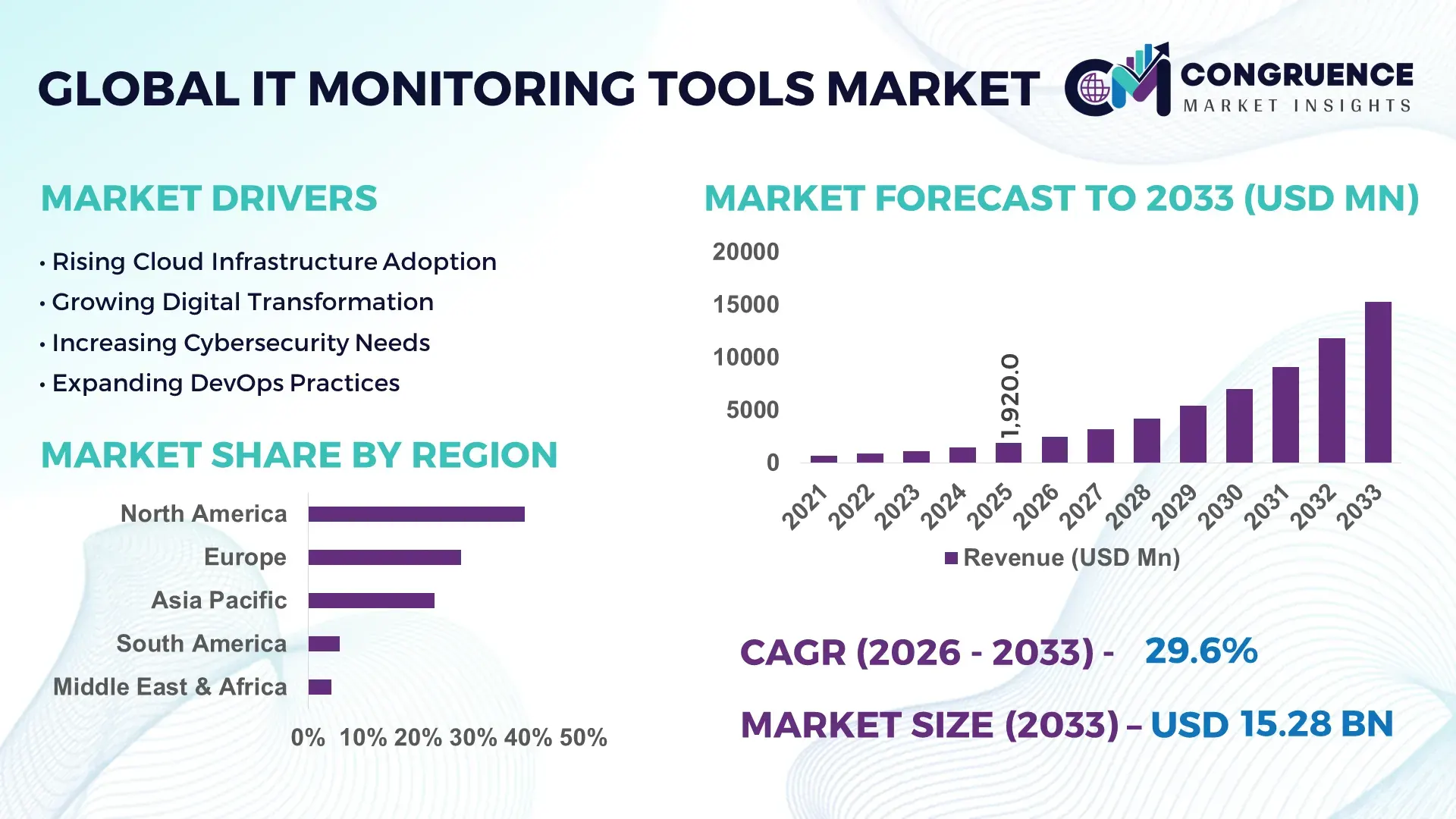

The Global IT Monitoring Tools Market was valued at USD 1,920.0 Million in 2025 and is anticipated to reach a value of USD 15,280.6 Million by 2033 expanding at a CAGR of 29.6% between 2026 and 2033. Rapid enterprise migration toward hybrid cloud infrastructure, AI-powered observability platforms, and zero-trust cybersecurity architectures is accelerating deployment of advanced IT monitoring tools across mission-critical digital environments.

The United States dominates the global IT Monitoring Tools Market with approximately 38% market share, supported by hyperscale cloud investments, over 5,500 operational data centers, and widespread adoption across BFSI, healthcare, telecommunications, and government sectors. Enterprise observability adoption exceeds 72% among large organizations, while Germany continues strengthening industrial monitoring through Industry 4.0 initiatives, creating a notable technology deployment gap with North America. Rising digital resilience priorities following global cyber threat escalation further reinforce long-term enterprise monitoring investments.

Organizations prioritizing AI-driven monitoring platforms gain stronger operational resilience, lower outage risks, and faster infrastructure optimization across increasingly distributed IT ecosystems.

Market Size & Growth: USD 1,920.0 Million in 2025, projected to reach USD 15,280.6 Million by 2033 at 29.6% CAGR, driven by enterprise-wide AI observability and hybrid cloud expansion.

Top Growth Drivers: Hybrid cloud adoption 68%, AIOps implementation 54%, zero-trust cybersecurity deployment 47%.

Short-Term Forecast: By 2028, automated monitoring is expected to reduce incident resolution time by 45% while improving infrastructure availability.

Emerging Technologies: AI analytics, predictive observability, OpenTelemetry integration, and automation are reshaping advanced enterprise monitoring.

Regional Leaders: North America (~USD 6.1 Billion), Europe (~USD 4.2 Billion), Asia-Pacific (~USD 3.8 Billion), supported by cloud modernization and regional digital expansion.

Consumer/End-User Trends: More than 70% of large enterprises deploy unified monitoring platforms across hybrid IT environments.

Pilot/Case Example: In 2024, enterprise AIOps deployments reduced critical incident response times by approximately 40% through automated root-cause analysis.

Competitive Landscape: Top vendors collectively hold nearly 58% market share, led by Datadog, Dynatrace, Splunk, IBM, and Cisco.

Regulatory & ESG Impact: Continuous compliance monitoring lowered audit preparation efforts by nearly 30% across regulated industries.

Investment & Funding: Over USD 8 Billion has been directed toward cloud observability, AI partnerships, and monitoring platform expansion amid global infrastructure modernization.

Innovation & Future Outlook: Autonomous observability, GenAI-assisted diagnostics, and unified telemetry platforms are strengthening enterprise operational intelligence.

The IT Monitoring Tools Market is witnessing robust demand across cloud-native applications, financial services, telecommunications, and industrial digital infrastructure where uninterrupted system performance is essential. AI-powered anomaly detection, unified observability, and OpenTelemetry-based monitoring continue to improve operational visibility, while nearly 65% of enterprises are consolidating multiple monitoring platforms into integrated solutions. Growing cybersecurity regulations and resilient infrastructure initiatives are further accelerating next-generation platform adoption, setting the stage for broader strategic transformation.

The IT Monitoring Tools Market has become a strategic priority as enterprises modernize digital infrastructure, expand hybrid cloud operations, and strengthen cyber resilience against increasingly sophisticated threats. Infrastructure modernization, stricter compliance requirements, and distributed application environments are encouraging organizations to replace fragmented monitoring systems with unified observability platforms. This transition is improving operational visibility while enabling faster business decision-making across critical digital assets.

Modern AI-driven monitoring platforms identify infrastructure anomalies nearly 60% faster than traditional rule-based systems while reducing manual troubleshooting efforts by approximately 40% through automated root-cause analysis. North America continues leading enterprise-scale deployments with mature cloud ecosystems, whereas Asia-Pacific records faster implementation across manufacturing, financial services, and digital public infrastructure initiatives. Over the next two to three years, enterprise adoption of full-stack observability platforms is expected to expand significantly as organizations standardize telemetry collection and automated incident response.

Large enterprises increasingly integrate monitoring tools with DevOps, cybersecurity, and IT service management platforms to create unified operational ecosystems. For example, multinational financial institutions are deploying AI-assisted observability across multi-cloud environments to reduce service disruptions and improve application availability. Technology vendors are responding through strategic acquisitions, ecosystem partnerships, and platform integration, strengthening competitive positioning while enabling customers to achieve greater operational efficiency, business continuity, and long-term digital resilience.

Rapid adoption of hybrid cloud infrastructure and AI-powered observability platforms is fundamentally reshaping enterprise IT operations. More than 72% of large organizations now operate hybrid or multi-cloud environments, while nearly 65% have integrated centralized monitoring into mission-critical workloads to improve operational resilience. In the United States, increasing adoption of zero-trust cybersecurity frameworks and stricter operational resilience standards are driving investment in continuous infrastructure visibility. This structural shift enables predictive issue detection, minimizes unplanned downtime, and improves service reliability. Leading vendors are expanding AI capabilities through acquisitions, cloud partnerships, and unified observability platforms that combine infrastructure, application, and security telemetry. Organizations implementing automated monitoring increasingly treat operational intelligence as a strategic business asset rather than a standalone IT function.

Legacy infrastructure remains a significant structural limitation for organizations modernizing enterprise monitoring architectures. Approximately 58% of large enterprises continue operating mixed legacy and cloud-native environments, while over 45% report interoperability challenges between monitoring platforms and existing IT service management systems. Germany's highly industrialized manufacturing sector illustrates this constraint, where decades-old operational technology often lacks compatibility with modern observability frameworks. These integration barriers increase deployment costs, extend implementation timelines, and complicate enterprise-wide visibility. To reduce operational risk, technology providers are developing API-first architectures, standardized telemetry protocols, and migration services while customers increasingly adopt phased modernization strategies instead of replacing mission-critical infrastructure through disruptive large-scale implementations.

The convergence of generative AI, predictive analytics, and autonomous IT operations is creating substantial opportunities beyond conventional infrastructure monitoring. Nearly 70% of enterprises are evaluating AIOps-enabled automation, while intelligent incident management has demonstrated operational efficiency improvements exceeding 40% in complex digital environments. India is emerging as a major innovation hub as enterprises accelerate cloud-native transformation and managed observability deployments across financial services, digital commerce, and telecommunications. Growing adoption of OpenTelemetry standards is enabling vendor-neutral ecosystem development and faster platform interoperability. Companies are responding through AI-focused research, strategic cloud alliances, and industry-specific monitoring solutions that integrate cybersecurity, application performance, and business analytics into unified operational platforms, strengthening long-term customer retention.

Maintaining consistent observability across increasingly distributed digital ecosystems remains a major long-term execution challenge. Enterprises now manage environments where cloud services account for over 60% of production workloads, yet nearly 48% report persistent visibility gaps across multi-cloud, edge, and containerized infrastructure. The United States continues experiencing heightened cybersecurity pressure as ransomware attacks and sophisticated threat activity demand continuous monitoring without increasing operational complexity. These conditions require scalable telemetry processing, skilled observability engineers, and standardized governance across thousands of connected assets. Technology vendors are investing in automation, AI-assisted diagnostics, cloud-native architectures, and ecosystem partnerships to simplify deployment while ensuring reliable performance, operational consistency, and sustainable enterprise-scale monitoring.

AI-Native Observability Expansion Enterprise monitoring platforms are rapidly embedding generative AI and predictive analytics to automate incident detection and root-cause analysis. Nearly 68% of large enterprises are implementing AI-assisted observability, while automated alert correlation reduces false positives by approximately 45%. Following rising cyber incidents and stricter operational resilience requirements in the United States, vendors are integrating AI copilots into monitoring workflows. Companies are expanding partnerships with hyperscale cloud providers to accelerate intelligent operations and improve service availability.

OpenTelemetry Standardization Accelerates OpenTelemetry has become the preferred telemetry framework as organizations seek vendor-neutral monitoring architectures. More than 55% of cloud-native enterprises now standardize telemetry collection, reducing deployment complexity by nearly 30% across multi-cloud environments. Japan's enterprise modernization initiatives are encouraging standardized observability deployments across financial institutions and manufacturers. Software vendors are restructuring product portfolios around open APIs, enabling faster ecosystem integration while lowering long-term migration costs.

Unified Security Operations Growth Organizations increasingly combine infrastructure monitoring with cybersecurity operations to improve enterprise resilience. Approximately 62% of security teams now integrate observability data into threat detection workflows, while unified monitoring reduces incident investigation time by around 35%. Growing regulatory scrutiny surrounding critical infrastructure protection is accelerating this operational convergence. Platform providers continue expanding XDR and SIEM integrations through strategic acquisitions and technology alliances.

Edge Infrastructure Monitoring Evolution Distributed computing is shifting enterprise monitoring closer to operational endpoints. Nearly 40% of industrial organizations now monitor edge environments alongside centralized cloud platforms, reducing latency by approximately 25% for mission-critical workloads. Germany's smart manufacturing expansion is increasing demand for real-time operational visibility across factory networks. Technology providers are scaling lightweight monitoring agents and edge-native analytics to support autonomous industrial operations with lower infrastructure overhead.

Infrastructure Monitoring Tools represent the largest segment of the IT Monitoring Tools Market, accounting for approximately 41% of enterprise deployments due to their critical role in maintaining server, network, storage, and cloud infrastructure availability. Organizations continue prioritizing these platforms because they provide centralized visibility, scalable monitoring, and rapid fault detection across increasingly distributed IT environments. Security Monitoring Tools also maintain strong demand as enterprises integrate cyber resilience into operational monitoring, while End-User Experience (EUX) Monitoring Tools are becoming strategically important for digital service optimization and workforce productivity. Application Performance Monitoring (APM) Tools are the fastest-growing segment as enterprises modernize cloud-native applications and microservices architectures. Nearly 63% of digital-first organizations have expanded APM deployment across customer-facing workloads, while integrated observability platforms improve troubleshooting efficiency by approximately 38%. Vendors are investing heavily in AI-driven diagnostics, unified telemetry, and cloud-native platform integration to differentiate offerings. Product innovation increasingly focuses on combining infrastructure, application, security, and user experience insights into a single operational platform, reflecting shifting enterprise investment priorities toward end-to-end observability.

IT & Telecommunications remains the leading application segment, representing nearly 34% of enterprise demand due to continuous digital infrastructure expansion, cloud migration, and large-scale network operations. Telecom operators require continuous monitoring across distributed data centers, edge infrastructure, and cloud-native platforms to maintain service quality. BFSI follows closely as financial institutions strengthen operational resilience, while Healthcare increasingly deploys monitoring tools to support electronic health records, connected medical devices, and cybersecurity compliance across mission-critical environments. Manufacturing is emerging as the fastest-growing application segment as Industry 4.0 initiatives expand industrial connectivity and smart factory deployments. Approximately 57% of large manufacturers now integrate IT monitoring with operational technology environments to improve production continuity and predictive maintenance. Retail & E-commerce continues strengthening omnichannel monitoring capabilities, while Government, Energy & Utilities, and Media organizations are expanding digital infrastructure observability through automation and cloud modernization. Technology vendors are responding through industry-specific platforms, managed monitoring services, and ecosystem partnerships tailored to operational requirements.

Large Enterprises account for roughly 72% of IT Monitoring Tools deployments due to extensive hybrid infrastructure, multi-cloud operations, and complex cybersecurity requirements. These organizations operate thousands of interconnected assets requiring centralized observability, automated incident management, and integrated performance analytics. Global financial institutions, cloud providers, manufacturers, and telecommunications companies continue expanding enterprise-wide monitoring strategies to improve operational continuity while reducing infrastructure downtime. Vendors prioritize this segment through premium AI-powered platforms, customized deployment models, and strategic technology alliances. Small & Medium Enterprises (SMEs) represent the fastest-growing buyer group as cloud-delivered monitoring platforms reduce implementation complexity and upfront infrastructure costs. Nearly 48% of SMEs now prefer SaaS-based observability solutions that simplify deployment while improving operational visibility across distributed workforces. Subscription pricing, managed services, and simplified automation are lowering adoption barriers for resource-constrained organizations. Technology providers continue expanding channel partnerships and cloud marketplace offerings to strengthen SME penetration while building scalable customer ecosystems supporting long-term digital transformation.

North America accounted for the largest market share at 39.4% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 32.1% between 2026 and 2033.

North America remains the largest IT Monitoring Tools Market due to extensive cloud infrastructure, advanced enterprise IT environments, and widespread adoption of AI-enabled observability platforms. Large enterprises across financial services, healthcare, telecommunications, and public administration continue consolidating monitoring, cybersecurity, and automation capabilities into unified operational platforms. The region contributes approximately 39.4% of global demand, supported by more than 5,500 operational data centers and rapid multi-cloud deployment. Strategic partnerships between hyperscale cloud providers and observability vendors continue accelerating platform integration, while enterprise investment increasingly prioritizes predictive analytics, autonomous incident management, and operational resilience across mission-critical digital ecosystems.

United States Market Outlook: The United States remains the regional growth engine through its leadership in cloud computing, enterprise software, cybersecurity innovation, and hyperscale infrastructure. Approximately 72% of large enterprises have deployed centralized observability platforms supporting hybrid cloud environments. Financial institutions, healthcare providers, and technology companies continue integrating AI-assisted monitoring into DevOps and security operations. Strong enterprise software ecosystems, continuous data center expansion, and high digital transformation spending position the country as the global benchmark for next-generation IT monitoring deployments.

Europe continues strengthening enterprise monitoring through digital modernization, cybersecurity compliance, and industrial digital transformation initiatives. The region accounts for nearly 27.8% of global market activity, supported by increasing adoption across manufacturing, banking, utilities, and healthcare sectors. Regulations promoting operational resilience and data governance are accelerating deployment of integrated observability platforms capable of supporting complex hybrid environments. Cloud migration continues expanding steadily, while enterprises increasingly combine application performance monitoring with security analytics. Technology providers are strengthening regional partnerships and localized cloud offerings to address compliance requirements while improving operational visibility across distributed enterprise infrastructures.

Germany Market Outlook: Germany leads the European market through its advanced manufacturing sector, industrial automation ecosystem, and strong Industry 4.0 implementation. Nearly 60% of large industrial enterprises have integrated centralized infrastructure monitoring with production-related digital systems to improve operational continuity. Manufacturing leaders continue expanding AI-assisted monitoring across factory networks, logistics platforms, and industrial cloud environments. Strong enterprise software adoption and sustained industrial digitalization make Germany a strategic innovation center for enterprise observability solutions.

Asia-Pacific represents the fastest-expanding regional market as enterprises rapidly modernize digital infrastructure and adopt cloud-native technologies. The region contributes approximately 22.9% of global market demand, driven by expanding hyperscale data centers, digital public infrastructure, and enterprise cloud migration. More than 65% of newly deployed enterprise workloads are now cloud-based across several leading economies, strengthening demand for scalable monitoring platforms. Technology vendors continue expanding regional development centers, cloud partnerships, and managed observability services to address growing enterprise requirements across manufacturing, banking, retail, and telecommunications sectors.

China Market Outlook: China remains the largest contributor within Asia-Pacific due to extensive cloud infrastructure investment, large enterprise digitalization programs, and expanding artificial intelligence deployment. More than 450 large-scale data centers support rapidly growing enterprise cloud adoption, creating sustained demand for intelligent infrastructure monitoring. Domestic technology providers continue strengthening AI-powered observability capabilities while major enterprises integrate monitoring platforms across manufacturing, logistics, telecommunications, and smart city initiatives to improve operational efficiency and digital resilience.

South America is experiencing increasing adoption of enterprise monitoring platforms as organizations modernize digital infrastructure and migrate toward hybrid cloud operations. The region represents approximately 5.7% of global market activity, with banking, retail, telecommunications, and public services driving deployment. Enterprise investment increasingly emphasizes automated infrastructure visibility and cybersecurity monitoring as digital services expand. Although legacy infrastructure and connectivity disparities continue affecting deployment consistency, technology providers are strengthening managed service offerings and regional cloud partnerships to simplify implementation while improving operational reliability.

Brazil Market Outlook: Brazil dominates the South American market through its mature banking industry, expanding cloud ecosystem, and large enterprise technology base. Nearly 58% of medium and large enterprises have accelerated hybrid cloud adoption, increasing demand for integrated monitoring and application observability. Domestic financial institutions and telecommunications operators continue modernizing IT operations through AI-enabled monitoring platforms, while international cloud providers expand regional infrastructure supporting long-term enterprise digital transformation.

The Middle East & Africa market is advancing through national digital transformation programs, expanding cloud infrastructure, and modernization of government and enterprise technology ecosystems. The region contributes around 4.2% of global market demand, supported by increasing investment in smart cities, financial services, and critical infrastructure modernization. Organizations are strengthening operational monitoring to support cybersecurity readiness and service continuity across increasingly connected environments. International technology vendors continue expanding cloud partnerships, regional support centers, and managed monitoring capabilities to accelerate enterprise deployment while addressing operational complexity.

United Arab Emirates Market Outlook: The United Arab Emirates leads regional adoption through ambitious digital economy initiatives, advanced cloud infrastructure, and government-backed technology modernization. More than 70% of government digital services operate through cloud-enabled platforms requiring continuous infrastructure observability and cybersecurity monitoring. Financial institutions, aviation companies, and public-sector organizations continue deploying AI-powered monitoring solutions to improve operational resilience, while strategic partnerships with global cloud providers strengthen the country's position as a regional technology hub.

The IT Monitoring Tools Market is led by Datadog, Dynatrace, Cisco Splunk, New Relic, and IBM, competing directly against cloud-native challengers including Grafana Labs and LogicMonitor, while ManageEngine and SolarWinds strengthen cost-focused enterprise offerings. The top five vendors collectively control approximately 58% of the market, reflecting moderate consolidation. Competition centers on AI-powered observability, unified telemetry, deployment speed, and platform integration rather than price alone. Enterprises report up to 40% faster incident resolution and nearly 30% lower operational overhead from unified observability platforms, shifting purchasing decisions toward full-stack solutions. Vendors are expanding through acquisitions, cloud-provider partnerships, OpenTelemetry integration, and security platform convergence. The competitive landscape is rapidly moving from standalone monitoring tools toward integrated observability ecosystems, increasing consolidation pressure. High switching costs, complex enterprise integrations, and extensive historical telemetry create significant entry barriers. Sustainable success depends on delivering AI-driven automation, open interoperability, rapid deployment, and measurable operational outcomes that outperform established enterprise platforms.

Dynatrace

Cisco Splunk

IBM

New Relic

SolarWinds

ManageEngine

Grafana Labs

LogicMonitor

Broadcom

Paessler AG

ScienceLogic

BMC Software

Elastic

Artificial intelligence, AIOps, and full-stack observability have become the core technologies transforming enterprise monitoring. AI-powered anomaly detection reduces alert noise by nearly 45%, while automated root-cause analysis shortens incident resolution by approximately 40%. More than 68% of large enterprises now deploy AI-assisted monitoring across hybrid cloud environments. OpenTelemetry has emerged as the preferred telemetry standard, enabling vendor-neutral integration and improving data portability across multi-cloud architectures. Organizations adopting unified telemetry gain faster deployment, lower maintenance complexity, and stronger operational visibility.

Modern observability platforms significantly outperform legacy rule-based monitoring. AI-driven monitoring identifies infrastructure anomalies nearly 60% faster than conventional threshold-based systems while reducing manual troubleshooting effort by approximately 35%. Datadog, Dynatrace, Cisco Splunk, and Grafana Labs benefit most from this transition by offering integrated platforms combining logs, metrics, traces, security analytics, and application performance within a unified operational ecosystem. This convergence strengthens competitive differentiation while reducing tool fragmentation for enterprise customers.

Between 2026 and 2028, autonomous remediation, generative AI copilots, digital twins for IT operations, and edge observability will become mainstream deployment priorities. Enterprise adoption of predictive observability is expected to exceed 75% among large organizations as infrastructure complexity increases. Organizations investing early in AI-native observability, open telemetry architectures, and cloud-integrated automation will achieve stronger operational resilience, lower downtime, faster software delivery, and sustained competitive advantage across increasingly distributed digital ecosystems.

April 2025 – Datadog acquired Metaplane, expanding AI-powered data observability with machine-learning monitoring and column-level lineage across enterprise data stacks. The acquisition strengthens end-to-end observability supporting 100% of the data lifecycle for AI applications and analytics. Business impact: broader enterprise observability portfolio. Source: www.datadoghq.com

May 2025 – Datadog acquired Eppo, integrating feature-flagging and experimentation capabilities into its observability platform. The reported transaction value was approximately USD 220 million, strengthening product analytics and AI application testing. Business impact: expanded developer workflow integration.

April 2026 – Dynatrace announced the acquisition of Bindplane, adding telemetry pipeline technology to optimize logs, metrics, and traces while reducing ingestion complexity. Business impact: stronger cloud-native observability and AI monitoring capabilities across enterprise environments.

April 2026 – Cisco announced its intent to acquire Galileo Technologies, enhancing AI observability and protection for the Splunk platform. The integration strengthens agentic AI monitoring across enterprise environments. Business impact: accelerated AI-native observability innovation and security convergence.

The report provides comprehensive analysis of the global IT Monitoring Tools Market across four technology segments, eight application categories, two end-user groups, and five major geographic regions. It evaluates enterprise adoption patterns, deployment models, competitive positioning, cloud observability, AIOps, OpenTelemetry integration, application performance monitoring, infrastructure monitoring, security monitoring, and end-user experience management. Regional assessments examine deployment concentration, enterprise digital transformation, cloud infrastructure expansion, and technology investment trends across mature and emerging markets.

The study delivers strategic intelligence supporting investment planning, product development, partnership evaluation, expansion strategy, and competitive benchmarking between 2026 and 2033. It analyzes adoption behavior, enterprise modernization priorities, technology innovation, industry-specific deployment trends, and operational performance indicators while profiling leading solution providers. The report also highlights emerging opportunities in AI-native observability, cloud-native monitoring, edge infrastructure visibility, unified telemetry, managed observability services, and digital operations, enabling stakeholders to identify high-priority growth segments and strengthen long-term competitive positioning.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 1,920.0 Million |

| Market Revenue (2033) | USD 15,280.6 Million |

| CAGR (2026–2033) | 29.6% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Datadog; Dynatrace; Cisco Splunk; IBM; New Relic; SolarWinds; ManageEngine; Grafana Labs; LogicMonitor; Broadcom; Paessler AG; ScienceLogic; BMC Software; Elastic |

| Customization & Pricing | Available on Request (10% Customization Free) |